|

市場調査レポート

商品コード

1910588

プロジェクト物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Project Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| プロジェクト物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

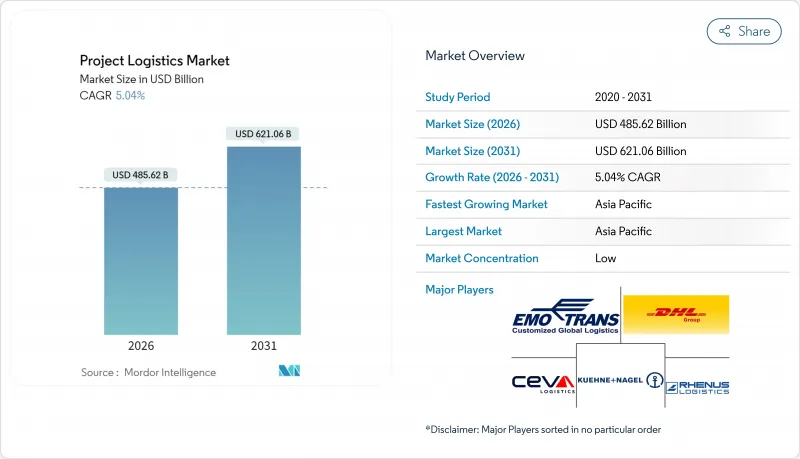

プロジェクト物流市場の規模は、2026年には4,856億2,000万米ドルと推定されており、2025年の4,623億米ドルから成長が見込まれます。

2031年の予測では6,210億6,000万米ドルに達し、2026年から2031年にかけてCAGR5.04%で拡大する見込みです。

再生可能エネルギーの設備増強、新興経済国におけるインフラ投資の同時多発的拡大、ユーラシア横断鉄道回廊の成熟化により、サービス範囲が拡大するとともに、輸送1件あたりの価値も向上しております。中規模LNGターミナル、水素パイプライン転換、モジュール式建設プロジェクトにより平均部品サイズが拡大し、特殊船舶、自走式モジュール輸送機、温度管理型貯蔵施設への需要が高まっています。同時に、AIを活用したルート最適化プラットフォームによりエンドツーエンドコストが10~15%削減され、納期が短縮されることで、事業者は限られた資産をより迅速に再配置できるようになりました。地域専門業者や技術主導の新規参入企業による競合激化が中堅企業の統合を加速させていますが、単独事業者のシェアが8%を超えないため、市場集中度は依然として低い水準です。貨物運賃の変動、重荷役認定作業員の不足、慢性的な港湾混雑といった持続的な逆風により、運送事業者はデジタル可視化ツール、マルチモーダルハブ、シミュレーション訓練プログラムへの投資を推進しています。

世界のプロジェクト物流市場の動向と洞察

再生可能エネルギー大型プロジェクトが専門物流需要を牽引

洋上風力発電所とグリーン水素回廊が輸送の青写真を書き換えています。タービンブレードは現在100メートルを超え、15~20MWタービン用に設計されたジャッキアップ船が必要となっています。ベンチャー・世界の社によるプラクミンズLNG第3段階拡張プロジェクト(総額180億米ドル)は、構成部品の規模拡大を象徴する一方、ドイツにおける400キロメートルの天然ガスパイプラインを水素輸送用に転換する動きは、-253℃以下に保たねばならない新たな極低温貨物の登場を示しています。こうした変化に対応するため、事業者はルート計画、船舶選定、在庫配置の見直しを迫られています。

新興経済国におけるインフラ・スーパーサイクルが長期成長を支える

中国の「一帯一路」構想は、100億米ドル規模の東アフリカ港湾計画と、輸送時間を最大50%短縮する鉄道網の整備を促しました。同時に、トランスカスピ国際輸送ルートは2024年に27,000 TEUを輸送し、前年比25倍の飛躍的成長を遂げました。プロジェクト物流市場は、この予測可能な数十年にわたる資本パイプラインの恩恵を受け、船隊の拡大や地域デポの拡張を正当化する基盤となっています。

多額の先行投資が市場参入を阻む

1,000トンのクローラークレーンは5,000万~1億米ドル、風力発電設備設置船は2億米ドルを超える費用がかかります。こうした巨額投資が新規参入を阻み、地域の専門業者に高コストでの機材リースを強いるため、プロジェクト量が増加しても利益率の向上が抑制されています。

セグメント分析

2025年時点でプロジェクト物流市場の60.45%を占めた輸送部門は、特大貨物における航路設計、重量物運搬船、護衛船の不可欠な役割を反映しています。倉庫保管・流通・在庫管理は規模こそ小さいもの、CAGR5.18%で最も急速に拡大している分野です。この伸びは、温度管理された仮置き場と同期化されたステージングを必要とするモジュール式建設の増加を反映しています。倉庫保管サービスのプロジェクト物流市場規模は、統合プロバイダーが保管とラストマイル組立をセット化するにつれ、拡大が見込まれます。自動在庫管理システムを導入する事業者は、部品の滞留時間を可視化でき、遊休資本や遅延違約金を抑制できます。

サービス内容の多様化に伴い、現地物流調整、通関業務、リスクアドバイザリーへの需要も高まっています。ハイランド・フェアビュー社の物流メガセンターはこのワンストップモデルを体現し、複雑な貨物フローに対応した4,000万平方フィートの施設を提供しています。資産所有者が製造から設置までの責任を外部委託する中、プロジェクト物流業界は輸送中心の契約から成果重視のパートナーシップへと転換し、顧客定着率と手数料収入の可能性を高めています。

プロジェクト・ロジスティクス市場レポートは、サービス別(輸送、倉庫保管、流通・在庫管理、その他サービス)、貨物タイプ別(特大貨物、重量物、バラ積み貨物、その他)、エンドユーザー別(石油・ガス、発電・送電、建設・インフラその他)、地域別(北米、南米、アジア太平洋、欧州、中東・アフリカ)に分類されています。市場予測は金額ベース(米ドル)で提供されます。

地域別分析

アジア太平洋地域は、中国の「一帯一路」沿いの港湾、インドの高速道路網、オーストラリアの再生可能鉱物資源の急増に支えられ、世界収益の38.60%を占めております。トランスカスピアン航路の取扱量が2024年に27,000TEUと25倍に急増したことは、スエズ運河への依存度を低減する代替回廊の重要性を浮き彫りにしています。地域政府は内陸デポやデジタル通関窓口への資金提供を行い、運送業者が資産の回転を加速させ、滞船料を削減することを可能にしています。

北米は第2位で、メキシコ湾岸のLNG設備拡充、40GW規模の再生可能エネルギーパイプライン、2025年末開通予定の64億米ドル規模ゴーディ・ハウ国際橋梁など回廊整備が牽引しています。カナダ北極貿易回廊はハドソン湾鉄道の改修により輸送時間を短縮し、重要鉱物輸出の鍵を開きます。許可手続きの改革によりスケジュール確実性が向上し、物流企業が長期チャーター契約を締結する後押しとなっています。

欧州、中東・アフリカは成熟した輸送ルートと新興ルートのモザイク状に構成されています。ドイツにおける400キロの水素パイプライン転換は新たな貨物カテゴリーを開拓し、エジプトの港湾拡張やサウジアラビアのランドブリッジ計画は沿岸重機クレーンの需要を加速させております。タンザニアのバガモヨ港を含む中国支援の東アフリカ港湾は貿易ルートの再編を促し、地域専門業者によるフィーダーサービス設立を誘致しております。南米の鉱業回廊と再生可能エネルギー計画は、リスク対応能力のある事業者に報いるフロンティア機会を開拓しております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 再生可能エネルギー大型プロジェクト(洋上風力、グリーン水素回廊)

- 新興経済国におけるインフラ・スーパーサイクル

- モジュール式建設およびプレハブプラントの規模拡大

- 中規模LNG輸出ターミナルの急増(米国メキシコ湾岸、西アフリカ)

- 一帯一路によるユーラシア横断鉄道回廊の成熟化

- AIを活用した航路・リスク最適化プラットフォーム

- 市場抑制要因

- 重量物運搬資産に対する高額な初期設備投資

- 変動する運賃と燃料費が利益率を圧迫しております

- 重荷役オペレーターの深刻な不足

- 港湾許可および混雑による遅延

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19および地政学的イベントの影響

第5章 市場規模と成長予測

- サービス別

- 輸送

- 道路

- 鉄道

- 航空

- 海

- 倉庫管理、物流、在庫管理

- 付加価値サービスおよびその他

- 輸送

- 貨物タイプ別

- 特大貨物(規格外貨物)

- 重量貨物

- バラ積み貨物

- その他

- エンドユーザー産業別

- 石油・ガス、鉱業・採石業

- エネルギー発電・送電

- 建設・インフラ

- 製造および工業プラント

- 航空宇宙・防衛

- その他(海事・造船、通信など)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- ペルー

- チリ

- アルゼンチン

- その他南米

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- 韓国

- 東南アジア(シンガポール、マレーシア、タイ、インドネシア、ベトナム、フィリピン)

- その他アジア太平洋

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ベネルクス(ベルギー、オランダ、ルクセンブルク)

- 北欧諸国(デンマーク、フィンランド、アイスランド、ノルウェー、スウェーデン)

- その他欧州

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Deutsche Post DHL

- Rhenus Logistics

- CEVA Logistics

- Kuehne+Nagel

- EMO Trans

- Hellmann Worldwide Logistics

- C.H. Robinson

- NMT Global Project Logistics

- Rohlig Logistics

- Expeditors International

- Kerry Logistics

- DSV A/S

- Fagioli group

- FLS Transportation

- Megalift

- Express Global Logistics(EXG)

- Yusen Logistics

- Geodis

- Crane Worldwide Logistics

- Transworld