|

市場調査レポート

商品コード

1850306

再生可能エネルギーにおける複合材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Composite Materials In Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 再生可能エネルギーにおける複合材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

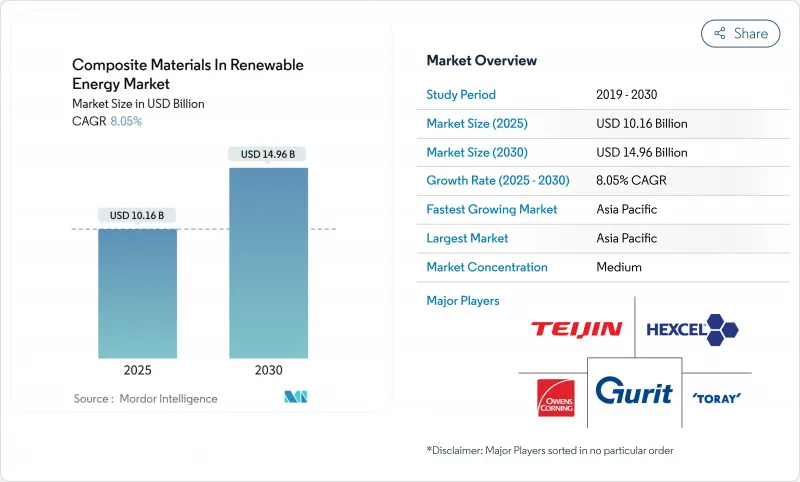

再生可能エネルギーにおける複合材料市場の2025年の市場規模は101億6,000万米ドルで、CAGR 8.05%で拡大し、2030年には149億6,000万米ドルに達すると予測されています。

風力、太陽光、水素プロジェクトにおける急速な設備増強は、部品の寿命を延ばしカーボンフットプリントを削減する、より軽量で強固な構造を要求しています。政府のクリーンエネルギー義務化、リサイクル可能な熱可塑性プラスチックプラットフォームの躍進、沖合や砂漠の過酷な気候に耐える軽量材料のニーズが相まって、調達サイクルが加速しています。繊維の自動配置、3Dプリンティング、その他のインダストリー4.0プロセスは、製造工程を短縮し、スクラップを削減しています。同時に、垂直統合型のサプライヤーは、サプライチェーンが緊張する中、重要なインプットを確保するために、繊維紡績、樹脂合成、部品製造を統合しています。こうした力が交錯することで、再生可能エネルギーにおける複合材料は、10年にわたる着実な技術革新主導型の成長を遂げることになります。

世界の再生可能エネルギーにおける複合材料市場の動向と洞察

金属構造に比べ軽量化

洋上風力発電、水素タンク、潮流発電装置では、複合材への置き換えによって構造物の質量が削減され、積載効率が向上し、輸送ロジスティクスが容易になります。潮流ブレードでは13.76%の軽量化により、鋼製代替品と比較して46.1%の出力向上が見られました。航空宇宙分野では、ライナーレスのV型炭素複合材タンクの開発が液体水素推進への移行をサポートし、間接的に再生可能グレード繊維の需要を増大させています。三菱化学のC/SiCセラミックマトリックス複合材は1,500℃に耐え、ヘリオスタット受信機や核融合炉ハードウェアへの道を開きます。これらの進歩は、再生可能エネルギーにおける複合材料が、高温で腐食性の高い環境においてアルミニウムやスチールに取って代わり続けている理由を明確に示しています。

風力タービンブレードの長尺化に対する需要の高まり

シーメンス・エナジー社のローター直径276mの21MWプロトタイプは、ブレードの長さが150m近くになると、グラスファイバーだけでは達成できない剛性対重量の目標のためにカーボンファイバーのスパーキャップが必要になることを示しています。高靭性エポキシ接合によって可能になるセグメント化されたブレード・アーキテクチャは、空力弾性的な完全性を維持しながら輸送を容易にします。ZEBRAコンソーシアムは、アルケマのElium樹脂を使用した世界最大の完全リサイクル可能な熱可塑性プラスチックブレードを完成させ、クローズドループプラットフォームへの産業的な準備を示しました。天然繊維と合成繊維を混合したハイブリッドレイアップは、耐衝撃性を向上させ、体積炭素量を削減します。

高い研究開発費と工具費

自動ファイバー配置ラインは1台500万~1,000万米ドルかかり、100mを超えるブレード用の金型は1セット200万米ドルを超え、投資回収までに何年も資本を拘束します。認証プログラムには5~7年かかることが多く、中堅イノベーターの運転資金ニーズを引き延ばしています。ヘクセルは2025年に3億米ドルの社債を発行するが、これはプロセス技術のリーダーシップを維持するために必要な資金力の例です。熱可塑性樹脂の採用は、オーブン、プレス、溶接設備が熱硬化性樹脂のラインと異なるため、コストがかさみます。

セグメント分析

2024年、再生可能エネルギーにおける複合材料市場において、GFRPは複合材料の55.25%を占め、このセグメントが最大の収益貢献をしています。炭素繊維のCAGR 8.62%は、剛性と疲労性能が5-10倍のコストプレミアムを正当化する、120mを超えるローター直径を反映しています。80mを超えるブレードに対するSGLカーボンの供給契約は、航空宇宙からエネルギーへの垂直的な動きを示しています。玄武岩と天然繊維を混合した繊維ハイブリッドレイアップは、体積炭素を削減しながらも必要な弾性率を維持し、中型タービンクラスの選択肢を広げています。ドイツで行われているバイオベースのリグニン繊維の研究は、商業的な量はまだ限られているもの、将来的なコスト削減のテコとなります。リサイクル炭素繊維は、メカニカルリサイクルにより元の引張強度を60~70%維持できるため、二次構造に着実に組み込まれつつあり、原料の多様化と原料価格変動の緩和が進んでいます。

エポキシは、成熟したサプライチェーンと高い耐疲労性により、2024年の売上高シェアは45.86%を維持します。しかし、バイオ樹脂と再生樹脂は、OEMが循環型経済への要求を満たすために競争しているため、CAGR 8.04%で拡大しています。ダウとヴェスタスは、層間靭性を高めながら迅速な引抜成形を可能にするポリウレタンスパーキャップ化学物質を認定しました。シコミンのバイオエポキシゲルコートSGi 128は、再生可能成分を35%含む火災安全ソリューションを実証しています。Eliumのような熱可塑性マトリックスは、修理可能性とメルトリサイクルという付加的な利点を提供し、再生可能エネルギーにおける複合材料をクローズドループ経済性へと向かわせる。

地域分析

アジア太平洋地域は、2024年の再生可能エネルギーにおける複合材料市場規模の44.68%を占め、2030年までのCAGRは8.12%です。中国はエンド・ツー・エンドのサプライチェーンでこの地域を支えているが、2024年のリサイクル基準ではコンプライアンス・コストが上昇するため、地元の総合企業が有利となります。インドの24億米ドルの水素ミッションと国防部門の炭素繊維推進は、国内生産のインセンティブを強化します。日本のペロブスカイト・ロードマップは、フレキシブルな複合基板を使って2040年までに3,830万kWを目指すもので、これは世界の太陽電池モジュール・アーキテクチャーを再調整する軸となるかもしれないです。韓国は造船のノウハウを活用して洋上風力複合材料に参入し、オーストラリアは内陸の貯水池で浮体式ソーラーをテストしており、最終用途事例における地域の多様性を示しています。

北米は、インフレ削減法(Inflation Reduction Act)による3,690億米ドルの資金調達の恩恵を受け、テキサス州、ニューヨーク州、オンタリオ州では国産化ボーナスが工場拡張の起爆剤となりました。GEヴァーノヴァの6億米ドルの製造設備増強は、太平洋横断ロジスティクス・リスクを削減するリショアリングの一例です。カナダの航空宇宙複合材クラスターは、オートクレーブから潮流タービンシェルへの移行を支援し、メキシコのコスト競争力のある労働力プールは、ソーラーラック輸出のためのプルトルーダーを引き寄せています。この地域の課題は、輸入品への過度な依存を防ぐために繊維製品の生産を拡大することだが、このギャップはいくつかの合弁企業が2027年までに解消することを目指しています。

欧州は規制の影響力を行使し、リサイクル可能性と体積炭素に関する世界的な規範の舵取りを行っています。ZEBRAプロジェクトの熱可塑性ブレードの成功は、欧州大陸を技術のフロントランナーとして位置づけています。ドイツのリグニン繊維パイロット・ラインは研究開発のリーダーシップを象徴しており、フランスは航空宇宙産業の伝統を活用して高弾性プリプレグを改良しています。英国国立複合材料センターのSusWINDプログラムは、複数のリサイクルルートを検証し、OEMに設計の柔軟性を与えています。北海とバルト海における洋上風力発電の建設は、持続的なファイバー需要の原動力となっているが、エネルギーコストの高騰により、オートメーションはマージンを守る必要に迫られています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 金属構造に比べて軽量

- 風力タービンブレードの長寿命化の需要増加

- 再生可能エネルギー導入に対する政府の意向

- 熱可塑性リサイクル可能ブレードプラットフォームの商業化

- 浮体式太陽光発電・潮力発電装置における3Dプリント複合部品の採用増加

- 市場抑制要因

- 研究開発およびツール投資額が高め

- リサイクルおよび埋め立て禁止遵守コスト

- 一部の複合材料の耐久性と耐火性に関する懸念

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 繊維タイプ別

- ガラス繊維強化プラスチック(GFRP)

- 炭素繊維強化プラスチック(CFRP)

- 繊維強化ポリマー(FRP)

- その他の繊維タイプ(ハイブリッド繊維やその他の繊維など)

- 樹脂基体別

- エポキシ

- ポリエステル

- ポリウレタン

- 熱可塑性

- バイオ樹脂とリサイクル樹脂

- 製造工程別

- 真空注入

- プリプレグ/オートクレーブ

- プルトルージョン

- 自動繊維配置/3Dプリント

- 圧縮成形(SMC、BMC)

- 用途別

- 風力

- 太陽光発電

- 水力発電

- その他の用途(グリーン水素およびエネルギー貯蔵容器)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Changzhou Tiansheng New Materials Co. Ltd

- EPSILON Composite SAS

- EURO-COMPOSITES

- Evonik Industries AG

- Exel Composites

- GE Vernova

- Gurit Services AG

- Jiangsu Hengshen Co.,Ltd

- Hexcel Corporation

- HS HYOSUNG ADVANCED MATERIALS

- LM WIND POWER

- Mitsubishi Chemical Group Corporation

- Norco Composites & GRP

- Owens Corning

- Plastic Reinforcement Fabrics Ltd

- SGL Carbon

- Siemens Gamesa Renewable Energy, S.A.U

- Solvay

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.