|

市場調査レポート

商品コード

1630183

硬質バルク包装:市場シェア分析、産業動向、統計、成長予測(2025~2030年)Rigid Bulk Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 硬質バルク包装:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

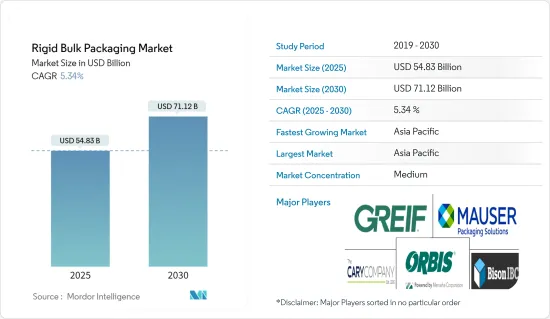

硬質バルク包装の市場規模は2025年に548億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.34%で、2030年には711億2,000万米ドルに達すると予測されます。

主要ハイライト

- 地域間で輸送される資源や製品の量が増加し続ける中、バルク包装の重要性が最も高まっています。硬質バルク包装市場は、バルク液体や粒状物質を保管・輸送するソリューションで構成されています。これには、食品原料、溶剤、化学品、医薬品、さらには大量に扱われる産業機器などが含まれます。

- 硬質バルク包装市場は、世界の輸出入活動と密接に結びついています。重工業は、ドラム缶やペール缶のような製品に対する強い需要を示しています。一方、ロジスティクスや短距離輸送では、マテリアルハンドリングコンテナや中間バルクコンテナ(IBC)に大きく依存しています。

- 多様なエンドユーザー産業で化学品や石油潤滑油の需要が増加し、サプライチェーン能力の強化が顕著に強調される中、産業用スチールドラムのニーズは急増する見込みです。InfralineEnergyの報告によると、インドは同地域で第2位の潤滑油消費国であり、世界でも米国と中国に次いで第3位です。

- 潤滑油は、加工産業において重要な役割を果たしており、自動車部品、特にブレーキやエンジンに不可欠で、その円滑な作動を保証しています。この市場は、ピストンエンジン用潤滑油の輸出入の増加と、自動車の性能を重視する消費者の増加によって成長を遂げています。化学、鉱業、非従来型エネルギーなどの産業が、工業用潤滑油の最大消費者になると予想されています。この動向は、工業用潤滑油の需要を強化し、市場における硬質包装の使用の高まりを示唆しています。

- プラスチック汚染は環境悪化に大きく寄与しており、多くの研究がその有害な影響を強調しています。これを受けて、欧州は他のいくつかの国々と並んで、プラスチックの使用量を世界的に抑制するための規制を制定しました。こうした世界の立法措置により、企業は産業用包装において持続可能で再利用可能な製品に焦点を当てた技術革新を余儀なくされています。

硬質バルク包装の市場動向

産業用コンテナドラムセグメントが大きなシェアを占める見込み

- 産業用ドラム缶は、危険物や非危険物の輸送や保管に頻繁に使用されます。化学、肥料、石油、石油産業で最も一般的に使用されています。産業用ドラム缶市場の成長を支えている要因の一つは、過去10年間におけるこれらのセグメントの継続的な拡大と国際貿易活動の活発化です。

- 従来の青いプラスチックドラムは、貯蔵施設、スーパーマーケット、倉庫などでおなじみです。多くの工業製品は青いプラスチックドラムに収まる。食品用プラスチックドラムは、食品を安全に保管・輸送するのに理想的です。さらに、食品ビジネスで使用されるプラスチックドラムは、長期間にわたって消耗品を輸送・保管する前に適切に除染され、安全であることが証明されなければならないです。

- さらに、同国では農業が拡大しており、特に化学品、食品穀物、肥料の用途でスチールドラムの需要がかなり高まると予想されます。2024年4月に発表された国際穀物協会(IGC)の報告書によると、世界の穀物生産量は2020/2021年度の22億2,700万トンから2023/2024年度には23億100万トンと一貫して増加しています。この需要増加傾向は予測期間中も続くとみられ、硬質バルク包装容器やドラム缶の需要増につながります。

- 工業用貯蔵の最も一般的な種類のひとつがプラスチックドラムです。大量の工業製品の長期保管と輸送は複数の機能を果たし、多くの利点を記載しています。ほとんどのプラスチックドラムは青色で、HDPE(高密度ポリエチレン)でできています。プラスチック・ドラムには様々なサイズがあり、30リットルから220リットルまでのものが多いです。

- さらに、ファイバードラムは、生産性を向上させ、経費を削減できるため、化学・肥料産業で目立つようになってきています。様々な国の間で肥料や化学品の輸送が拡大し、様々な産業用ドラム缶の成長が加速すると予測されています。

- さらに、様々なエンドユーザー産業からの化学品と石油潤滑油の需要の増加と、サプライチェーン能力の強化への重要な焦点は、産業用スチールドラムのニーズを促進すると予想されます。InfralineEnergy社によると、インドは同地域で第2位、世界では米国と中国に次いで第3位の潤滑油消費国です。

アジア太平洋が最大の市場シェアを占める

- アジア太平洋の産業・製造業は急速に発展しており、中国、インド、インドネシアなどの新興経済圏に製造拠点を拡大し続けているため、硬質バルク包装の使用量が増加すると予想されます。中国はファイバードラムの生産において楽観的な成長を見せています。金額ベースでは、マレーシアやシンガポールといった他の国々を圧倒しています。

- 地元企業や有名企業による洗練された製品包装ソリューションへの関心の高まりが、より高品質のファイバードラムを生み出しています。小売産業の成長と、リサイクル可能なファイバードラムのような軽量バルクコンテナへの嗜好の高まりは、ファイバードラム市場に影響を与える主要要因です。ファイバードラムを利用する主要利点はリサイクル可能であることで、アジア太平洋の硬質バルク市場の展望は明るいです。

- 中国経済は高い成長速度を維持しており、これは20年以上にわたって消費者消費と設備投資、工業生産高、輸出入の連続的な増加によって刺激されてきました。中国における工業用包装の需要は、過去数十年間同様の傾向をたどってきました。また、今後10年間は生産と需要の両方が伸び続けると予想されており、同国の工業用包装市場の成長を支えるものと期待されています。

- Indian Brand Equity Federationによると、インドはジェネリック医薬品の世界トップサプライヤーです。インドの製薬産業は、世界のワクチン需要の半分以上、米国のジェネリック需要の40%、英国の全医薬品の25%を供給しています。世界的に見て、インドの医薬品生産量は第3位、金額では第14位です。医薬品産業の成長とともに同国の医薬品包装事業も成長し、同地域の硬質バルク包装市場を牽引していくと考えられます。

- また、アジア諸国からの化学・関連産業輸出の伸びが、ドラム缶、コンテナ、ドラム缶、ペール缶などの硬質バルク包装製品の需要を牽引しています。インド準備銀行とDirectorate General of Commercial Intelligenceのデータによると、2023会計年度にインドは2兆4,353億6,000万インドルピー(290億2,000万米ドル)以上の有機・無機化学品を輸出しました。これは前会計年度の評価額2兆1,890億7,000万インドルピー(260億8,000万米ドル)から上昇しました。その結果、この化学品輸出の急増は、予測期間中の市場の強化につながると考えられます。

硬質バルク包装産業概要

硬質バルク包装市場はセグメント化されており、Greif Inc.、FDL Packaging Group、Mondi PLC、BWAY Corporationなど多くの大手企業が参入しています。さらに、包装市場の他の主要企業は、市場に参入し、提供を成長させるために買収やパートナーシップ戦略を採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場力学

- 市場促進要因

- 持続可能でリサイクル可能な包装材料の出現

- 化学・製薬産業の生産量の増加

- 市場抑制要因

- 環境規制が市場成長の課題

- 市場促進要因

第5章 市場セグメンテーション

- 材料別

- プラスチック

- 金属

- 木材

- その他

- 製品別

- 工業用バルク容器

- ドラム缶

- ペール缶

- ボックス

- その他バルク容器

- エンドユーザー産業別

- 食品

- 飲料

- 工業用

- 製薬・化学

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア

- インド

- 中国

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

- 北米

第6章 競合情勢

- 企業プロファイル

- ORBIS Corporation

- FDL Packaging Group Ltd

- Bison IBC Ltd

- Wadpack Pvt Ltd

- Greif Inc.

- The Cary Company

- Hoover Container Solutions

- ITP Packaging

- Mauser Packaging Solutions

- Mondi PLC

第7章 投資分析

第8章 市場機会と今後の動向

目次

Product Code: 60379

The Rigid Bulk Packaging Market size is estimated at USD 54.83 billion in 2025, and is expected to reach USD 71.12 billion by 2030, at a CAGR of 5.34% during the forecast period (2025-2030).

Key Highlights

- As the volume of resources and products transported across regions continues to rise, the significance of bulk packaging has become paramount. The rigid bulk packaging market comprises solutions for storing and transporting bulk liquids and granulated substances. These include food ingredients, solvents, chemicals, pharmaceuticals, and even industrial equipment, all handled in large quantities.

- The rigid bulk packaging market is closely tied to global import and export activities. Heavy manufacturing industries show a strong demand for products like drums and pails. In contrast, logistics and short-distance transportation of goods heavily rely on materials handling containers and intermediate bulk containers (IBCs).

- With a growing demand for chemicals and petroleum lubricants across diverse end-user industries and a pronounced emphasis on bolstering supply chain capabilities, the need for industrial steel drums is set to surge. As reported by InfralineEnergy, India ranks as the second-largest lubricant consumer in its region and holds the third position globally, trailing only the United States and China.

- Lubricants play a crucial role in processing industries and are vital for automobile parts, especially brakes and engines, ensuring their smooth operation. The market is witnessing growth, fueled by rising imports and exports of piston engine lubricants and an increasing consumer emphasis on vehicle performance. Industries such as chemicals, mining, and unconventional energy are anticipated to be the largest consumers of industrial lubricants. This trend bolsters the demand for industrial lubricants and hints at a heightened use of rigid packaging in the market.

- Plastic pollution has significantly contributed to environmental degradation, with numerous studies highlighting its detrimental effects. In response, European regions, alongside several other nations, have enacted regulations to curb plastic usage globally. These worldwide legislative measures have forced companies to innovate, focusing on sustainable and reusable products in industrial packaging.

Rigid Bulk Packaging Market Trends

The Industrial Containers and Drums Segment is Expected to Hold a Significant Share

- Industrial drums are frequently used for transporting and storing hazardous and non-hazardous commodities. They are most commonly used in the chemical, fertilizer, oil, and petroleum industries. One factor supporting the growth of the industrial drum market is the continued expansion of these segments and rising international trade activities over the past 10 years.

- Traditional blue plastic drums are familiar in storage facilities, supermarkets, and warehouses. Many industrial objects fit in blue plastic drums. Food-grade plastic drums are ideal for securely storing and transporting food. Additionally, plastic drums used in the food business should be properly decontaminated and certified as safe before transporting and storing consumables over an extended period.

- Further, the expanding agricultural industry in the country is anticipated to generate considerable demand for steel drums, particularly in chemicals, food grains, and fertilizer applications within the region. According to the International Grains Council (IGC) report published in April 2024, global grain production has consistently increased from 2,227 million metric tons in FY 2020/2021 to 2,301 million metric tons in FY 2023/2024. This rising demand trend is expected to continue during the forecast period, leading to an increased demand for rigid bulk packaging containers and drums.

- One of the most common types of industrial storage is plastic drums. The long-term storage and transportation of large quantities of industrial commodities serve multiple functions and offer numerous advantages. Most plastic drums are blue and made of HDPE (high-density polyethylene), a robust type of plastic that can be molded easily and lasts for many years. Plastic drums come in a variety of sizes, often ranging from 30 to 220 liters.

- Moreover, fiber drums are becoming more prominent in the chemical and fertilizers industry because they improve productivity and reduce expenses. The expansion of fertilizer and chemical traffic between various countries is predicted to accelerate the growth of different industrial drums.

- Further, the rise in the demand for chemicals and petroleum lubricants from various end-user industries and a significant focus on strengthening the supply chain capability is expected to drive the need for industrial steel drums. According to InfralineEnergy, India is the second-largest lubricant consumer in the region and the third-largest globally, after the United States and China.

Asia-Pacific to Hold the Largest Market Share

- The rapidly evolving industrial and manufacturing industry in Asia-Pacific is expected to increase the usage of rigid bulk packaging as manufacturers continue expanding their manufacturing bases to emerging economies like China, India, and Indonesia. China has shown optimistic growth in the production of fiber drums. In terms of value, it has a strong hold over other countries such as Malaysia and Singapore.

- The rising concerns for sophisticated product packaging solutions by local and renowned players have translated into better quality fiber drums. The growing retail industry and the increasing preference for lightweight bulk containers such as recyclable fiber drums are key factors affecting the fiber drums market. The primary benefit of utilizing fiber drums is their recyclability, leading to a positive outlook for the rigid bulk market in Asia-Pacific.

- The Chinese economy maintains a high speed of growth, which has been stimulated by consecutive increases in consumer consumption and capital investment, industrial output, and import and export for over two decades. The demand for industrial packaging in China has followed a similar trend in the past few decades. Also, both production and demand are expected to continue to grow in the next decade, which is expected to support the growth of the industrial packaging market in the country.

- India is the world's top supplier of generic pharmaceuticals, according to the Indian Brand Equity Federation. The Indian pharmaceutical industry supplies more than half of the global demand for vaccines, 40% of the generic demand in the United States, and 25% of all pharmaceuticals in the United Kingdom. Globally, India ranks third in terms of pharmaceutical production by volume and 14th by value. The country's pharmaceutical packaging business will grow as the pharmaceutical industry grows, driving the rigid bulk packaging market in the region.

- Also, the growth of chemical and allied industry exports from Asian countries is driving the demand for rigid bulk packaging products like drums, containers, drums, and pails. Data from the Reserve Bank of India and the Directorate General of Commercial Intelligence reveal that in fiscal year 2023, India exported organic and inorganic chemicals worth over INR 2435.36 billion (USD 29.02 billion). This marked an uptick from the prior fiscal year's valuation of INR 2189.07 billion (USD 26.08 billion). As a result, this surge in chemical exports is poised to strengthen the market during the forecast period.

Rigid Bulk Packaging Industry Overview

The rigid bulk packaging market is fragmented, with many major players like Greif Inc., FDL Packaging Group, Mondi PLC, and BWAY Corporation. Additionally, the other major players in the packaging market are adopting acquisition and partnership strategies to enter the market and grow offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Dynamics

- 4.4.1 Market Drivers

- 4.4.1.1 Emergence of Sustainable and Recyclable Packaging Materials

- 4.4.1.2 Growing Production Volume of Chemical and Pharmaceutical Industries

- 4.4.2 Market Restraint

- 4.4.2.1 Environmental Legislations Challenge the Market Growth

- 4.4.1 Market Drivers

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Pastic

- 5.1.2 Metal

- 5.1.3 Wood

- 5.1.4 Other Materials

- 5.2 By Product

- 5.2.1 Industrial Bulk Containers

- 5.2.2 Drums

- 5.2.3 Pails

- 5.2.4 Boxes

- 5.2.5 Other Bulk Containers

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Industrial

- 5.3.4 Pharmaceutical and Chemical

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.3 Asia

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia and New Zealand

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Mexico

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Saudi Arabia

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ORBIS Corporation

- 6.1.2 FDL Packaging Group Ltd

- 6.1.3 Bison IBC Ltd

- 6.1.4 Wadpack Pvt Ltd

- 6.1.5 Greif Inc.

- 6.1.6 The Cary Company

- 6.1.7 Hoover Container Solutions

- 6.1.8 ITP Packaging

- 6.1.9 Mauser Packaging Solutions

- 6.1.10 Mondi PLC