|

市場調査レポート

商品コード

1850137

データセンターオートメーション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Data Center Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンターオートメーション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

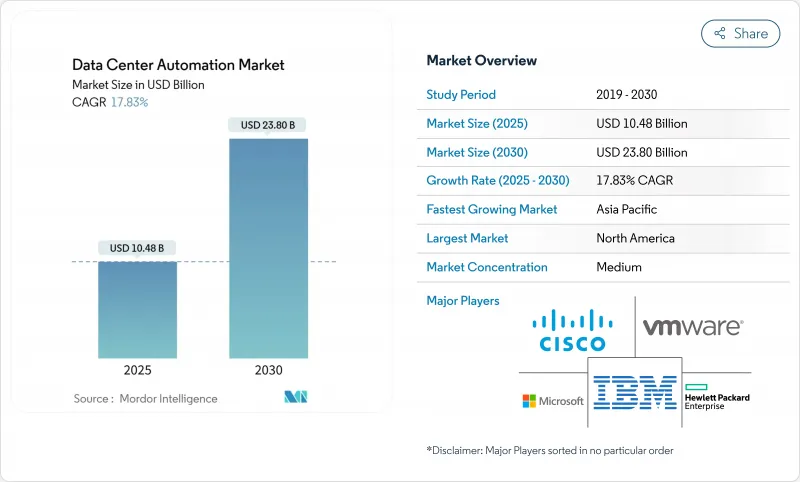

データセンターオートメーション市場規模は2025年に104億8,000万米ドルと推定・予測され、2030年には238億米ドルに達し、期間中のCAGRは17.83%を記録すると予測されます。

クラウドプラットフォームへの依存の高まり、AIワークロードの急増、エネルギーフットプリントの削減への圧力の高まりにより、自動化は運用上の利便性から取締役会レベルの義務へと移行しつつあります。ハイパースケールの構築により、電力コストを削減しながらサービス品質を維持するソフトウェア定義のオーケストレーションの必要性が高まっています。これと並行して、モジュール設計や液冷システムの展開では、自動化システムだけが実現できるきめ細かなリアルタイム制御が求められています。ベンダーは、インフラを自己調整し、ハードウェアの故障を予測するAIエンジンを組み込むことで、労働力、エネルギー、ダウンタイムの測定可能な節約を実現し、競争激化が加速しています。さらに、米国エネルギー省の報告によると、データセンターの電力需要は2028年までに2倍または3倍に増加する可能性があり、AIアプリケーションがこの成長の大部分を牽引しているため、エネルギー使用を最適化できる自動化ソリューションに対する緊急の圧力が高まっています。さらに、負荷のシフトを行い、エネルギーの柔軟性を収益源に変えることで事業者に報酬を支払う、成熟しつつあるグリッド・インタラクティブ・プログラムによって、その採用はさらに強化されます。

世界のデータセンターオートメーション市場の動向と洞察

クラウドとハイパースケール構築の急増

2025年に予定されているハイパースケールキャンパスの投資額は2,500億米ドルを超え、容量計画、熱管理、ワークロードのライブマイグレーションにまたがる自動化の必要性が生じています。オペレーターは、コンピュート、電力、冷却リソースを瞬時に割り当て、オペレーターの介入を最小限に抑えながら、サービスレベルの需要に対応できるAI主導のコントローラーを中心に施設を設計しています。資本集約的な拡張は現在、配線済みでテスト済みのモジュラー・ブロックと組み合わされているため、オーケストレーション・ソフトウェアは各ブロックを即座に発見し、ベースライン化し、統合する必要があります。グローバルベンダーは、何千もの資産にポリシーを適用するインテントベースのプラットフォームで対応し、構築速度を競争力のある武器に変えています。

エネルギー効率の高い持続可能な運用への要求

データセンターは現在、世界の電力使用量の1~3%を占めているが、AIの普及が加速すれば、その割合は2030年までに5%に上昇すると予測されています。欧州のClimate Neutral Data Centre Pact(気候中立データセンター協定)のような厳格なイニシアチブは、新設のPUE上限を1.3に設定しており、オペレータはエアフロー、ファン速度、ワークロード配置を継続的に調整する自動化を採用するよう促しています。AIを活用した制御により、初期の導入ではすでに冷却電力が最大40%削減されており、検証可能な二酸化炭素削減を示す事業者は、独自のESG目標を達成しなければならないハイパースケールのテナントを引き付けています。自動化された持続可能性報告は、コンプライアンスのオーバーヘッドをさらに削減し、規制当局との透明性を向上させています。

レガシーシステムの相互運用性のハードル

多くの事業者は、まだ限られたAPIで独自のハードウェアを運用しており、最新のオーケストレーションが定着する前に、コストのかかるカスタムコネクタを余儀なくされています。ネットワークチームは、設定ミスによるスクリプトの停止を恐れて、ミッションクリティカルなトラフィックを処理するコアスイッチの自動化を躊躇することが多いです。あるサイト用に構築されたテンプレートが他のサイトにきれいに移植されることはほとんどないため、レガシーな施設全体で設計が標準化されていないことが、ロールアウトをさらに複雑にしています。ベンダーは、広範なプラグインマーケットプレースや、デバイス構成をリバースエンジニアリングするAIベースのディスカバリーツールで対応しているが、技術的負債が深い組織では、移行スケジュールは依然として長期化しています。

セグメント分析

2024年のデータセンターオートメーション市場シェアでは、サーバーオートメーションが51.8%を占めるが、2030年までのCAGRは19.20%と予測され、ネットワークオートメーションが最も急成長しています。ネットワークに特化したプラットフォームの成長は、マイクロサービス、コンテナクラスタ、東西トラフィックパターンの普及により、手作業によるコマンドラインの変更が圧倒的に多いことを反映しています。企業は、ビジネスの意図をデバイスのコンフィギュレーションに変換し、クローズドループのテレメトリを通じて結果を検証するコントローラにシフトしています。このシフトは、ダウンタイムインシデントを削減するプログラマブルQoS、マイクロセグメンテーション、自動ロールバック機能を解き放ちます。

中期的には、オーケストレーション・スイートは、構成管理、パフォーマンス分析、コンプライアンス・チェックなど、以前は別々だった機能を、役割ベースのアクセスによって管理される統合ツールチェーンに収束させる。AIを活用した診断は、レイテンシの根源を特定し、改善策を提案することで、解決までの平均時間を短縮します。その結果、経営幹部はネットワークの自動化をコストセンターとしてではなく、戦略的投資として捉えるようになりました。企業の30%が2026年までにネットワーク活動の少なくとも半分を自動化することを目指しており、インテントベースネットワーキングの普及に向けた基盤が整いつつあります。

2024年のデータセンターオートメーション市場規模は、ティア3施設が45.20%を占めるが、ティア4施設は99.995%のアップタイムが期待されているため、CAGRは18.34%になります。ティア4キャンパスのオペレータは、オーケストレーションされたフェイルオーバー・プロセス、リアルタイムの健全性スコアリング、自己修復メッシュ・アーキテクチャに依存しています。自動化された診断機能により、冗長パスや環境センサーが1分間に何千回も検査され、先手を打ったパーツの交換や負荷の移動が行われます。

逆に、ティア1やティア2のサイトでは、予算の制限から、バックアップのスケジューリングやパッチ管理に重点を置き、選択的な自動化を追求しています。しかし、ソフトウェア・コストの低下とモジュラー・コントローラーの設計により、参入障壁は低くなっています。ディザスタリカバリのオーケストレーションは、普遍的な優先事項になりつつある:現在では、自動化されたランブックが人手を介さずに毎月フェイルオーバー・シークエンスをテストし、収益を守りながら監査要件を満たしています。これらの機能により、ティアレベル間の運用格差は徐々に縮小し、業界全体の基本的な期待が高まっています。

データセンターオートメーション市場は、ソリューション別(サーバー自動化、ネットワーク自動化など)、データセンター階層タイプ別(階層1および2、階層3、階層4)、導入形態別(オンプレミス、クラウド)、データセンタータイプ別(ハイパースケーラ/クラウドサービスプロバイダ、コロケーションプロバイダなど)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は、クラウドの普及と大規模資本プールへのアクセスにより、2024年のデータセンターオートメーション市場シェアの46.30%を維持。バージニア北部のようなコア回廊では電力制約があり、利用可能なメガワットを最大限に活用するグリッド・インタラクティブ・オートメーションに注目が集まっています。データセンターの電力需要が2028年までに倍増する可能性を示す連邦政府の調査は、アイドル消費を最小限に抑え、デマンドレスポンスプログラムを通じて柔軟性を収益化するプラットフォームへの関心を高めています。企業の持続可能性に関するシナリオは、AIガイドによる冷却と容量計画ツールの積極的な導入をさらに後押ししています。

アジア太平洋は、2025~2030年のCAGRが19.45%と予想される最も急成長している地域です。中国、日本、インドの国家的イニシアチブは、ローカル・クラウド・ゾーンとエッジの増築を奨励し、労働力不足を補う自動化の必要性を高めています。タイとインドネシアにおける数十億米ドル規模の投資を含む大規模プロジェクトでは、液体冷却と再生可能電源がバンドルされ、初日から異種のテクノロジーを調和させるオーケストレーション層が求められます。

欧州は、成熟したコロケーション拠点と厳しい環境規制を併せ持ち、高度なサステナビリティ自動化の坩堝となっています。2030年までに気候変動に左右されない施設を実現するというコミットメントは、1.3以下のPUE目標を維持し、再生可能エネルギーの使用を検証する継続的最適化エンジンを導入するようオペレーターを後押ししています。デマンドレスポンスへの参加と熱再利用スキームへのインセンティブは、ビジネスケースを強化します。サウジアラビア、アラブ首長国連邦、南アフリカの主要プロジェクトでは、遠隔地での人員配置の制限を克服するため、ネット・ゼロの実証ポイントと自律運転が必要とされており、自動化は融資とテナント確保の必須条件となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- クラウドとハイパースケールの構築の急増

- エネルギー効率と持続可能な運用の需要

- AI/MLワークロード自動化のニーズの高まり

- ハイブリッドおよびマルチクラウドアーキテクチャの複雑さ

- データセンター向けグリッドインタラクティブインセンティブプログラム

- 新興経済におけるエッジローカリゼーション

- 市場抑制要因

- レガシーシステムの相互運用性のハードル

- サイバーセキュリティとコンプライアンスリスクの高まり

- NetOps/自動化の人材不足

- 主要拠点における電力と水の不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場におけるマクロ経済動向の評価

- 持続可能性とカーボンニュートラルの取り組み

- 容量と電力需要分析

第5章 市場規模と成長予測

- ソリューション別

- サーバー自動化

- ネットワーク自動化

- ストレージ/データベース自動化

- オーケストレーションと構成管理

- パフォーマンスとコンプライアンスの管理

- データセンター階層タイプ別

- ティア1とティア2

- ティア3

- ティア4

- 展開モード別

- オンプレミス

- クラウド

- データセンタータイプ別

- ハイパースケーラー/クラウドサーバープロバイダー

- コロケーションプロバイダー

- エンタープライズとエッジ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- シンガポール

- オーストラリア

- マレーシア

- その他アジア太平洋地域

- 南米

- ブラジル

- チリ

- アルゼンチン

- その他南米

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cisco Systems Inc.

- VMware Inc.

- Microsoft Corporation

- IBM Corporation

- Hewlett Packard Enterprise(HPE)

- Dell Technologies Inc.

- BMC Software Inc.

- ServiceNow Inc.

- Oracle Corporation

- Fujitsu Ltd.

- Juniper Networks Inc.

- ABB Ltd.

- Citrix Systems Inc.

- Chef Software Inc.(Progress Software)

- Brocade Communications Systems

- HashiCorp Inc.

- Puppet Labs LLC

- Micro Focus Intl. plc

- Huawei Technologies Co. Ltd.

- Schneider Electric SE

- NetApp Inc.