乳製品パッケージング:市場シェア分析、産業動向、成長予測(2025年~2030年)

Dairy Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1628730

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

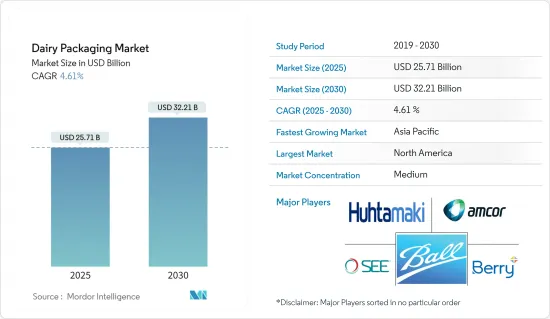

乳製品パッケージング市場規模は2025年に257億1,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは4.61%で、2030年には322億1,000万米ドルに達すると予測されます。

主なハイライト

- ヘルシーな間食へのシフト、調理済み食品の消費の増加、オンラインショッピングとモバイルショッピングの台頭により、食品の購買と消費のパターンが変化しています。こうした動向は、健康志向の高まりと相まって、乳製品市場に大きな影響を与えると予想されます。

- 人口増加と食生活の変化により、様々な小売チャネルを通じてパッケージ入り乳製品が入手可能になりつつあることが、市場の成長を後押しすると思われます。さらに、タンパク質ベースの製品に対する消費者の嗜好の高まりは、世界的に乳製品ベースのアイテムの採用を促進すると予想されます。

- 乳製品業界の世界の動向から、メーカーが製品を際立たせるためにパッケージにますます力を入れるようになっていることがわかる。今日の乳製品パッケージは、人目を引くデザインと無菌機能を誇ることが多いです。日本、アジア太平洋地域、西欧、北米などの主要市場における激しい競争のため、エンドユーザーは乳製品の革新的なパッケージ戦略を採用しています。

- 乳製品メーカーは、国際的な輸出能力の向上と現地生産を通じて、世界の乳製品貿易でより大きなシェアを獲得することにますます重点を置くようになっています。この動向は、より先進的な乳製品パッケージング・ソリューションの需要に拍車をかけています。

- 包装タイプの多様化は、乳製品販売の拡大における重要な要因です。例えば、かつては主にゲーブルトップカートンで販売されていた牛乳は、現在では持ち運び可能でブランドに適したペットボトルで販売されることが多く、時間に制約のある消費者にアピールしています。

- しかし、乳製品パッケージング市場は課題に直面しています。食品価格に影響される包装資材の価格変動は、市場の成長を妨げる可能性があります。さらに、がんや生殖に関する健康問題につながる毒素の懸念など、プラスチック包装に関連する潜在的な健康リスクに対する懸念が、市場拡大の障害となっています。

乳製品パッケージング市場の動向

牛乳が最大の市場シェアを占める

- 牛乳は世界で最も消費されている乳製品です。水分とミネラルを多く含むため、ベンダーにとっては保管に大きな課題があり、そのため粉ミルクや加工乳が広く流通しています。このような特性から生乳は非常に腐りやすく、品質を維持し賞味期限を延ばすために先進の保存・パッケージング技術が必要とされています。

- 現在の牛乳加工技術では、液体牛乳を瓶詰めして4~8℃で保存し、10~21日の賞味期限を保つことができます。超高温(UHT)処理などの先進的なプロセスにより、冷蔵なしでパッケージングされた牛乳の賞味期限は1年まで延びた。この技術的進歩は牛乳の流通に革命をもたらし、より幅広い市場への参入と無駄の削減を可能にしました。

- 近年、特にアジアでは地産地消の傾向が強まっています。このシフトは輸入への依存を減らし、国内の酪農産業を支援することを目的としています。インドのような国が世界の生乳生産量の約16%を占めているにもかかわらず、顕著な需給ギャップが続いています。この食い違いは、新興国市場におけるインフラと流通網の改善の必要性を浮き彫りにしています。

- さらに、革新的で環境に優しい牛乳パッケージの台頭が、市場のトップラインを押し上げています。この動向はボトル、カートン、パウチなど複数の包装形態に及んでいます。例えば、Delamere Dairy社は2024年7月、外出の多い消費者をターゲットにしたCartoCanフレーバーミルクシリーズを発表しました。完全にリサイクル可能なCartoCanは、プラスチック廃棄物を削減し、従来の500mlガラス瓶に代わる手軽な代替品を提供します。

- 米国農務省海外農業局によると、世界の牛乳生産量は着実に増加しています。世界の牛乳生産量は2017年の5億1,160万トンから2023年には約5億4,948万トンに増加します。この成長は、乳製品に対する世界の需要の増加と、酪農の実践と技術の向上を反映しています。

- 酪農業界では無菌包装の需要が急増しています。世界の生乳生産量の増加は、新たな市場機会を解き放つと思われます。また、UHT牛乳の消費量の急増に象徴されるように、消費者の行動には著しい変化が見られます。消費者が買い物に行く回数を減らそうとしているため、賞味期限が長いUHT牛乳の需要が急増しています。特筆すべきは、乳製品ソリューションにおける消費者の嗜好に明らかな変化が見られることで、バラ売り牛乳から大手ブランド、特に大量に供給しているブランドのパック入り牛乳へと移行しています。

北米が最大の市場シェアを占める

- 北米は、牛乳、チーズ、ヨーグルトなどの乳製品の生産と販売の増加により、世界の乳製品パッケージング市場で最大のシェアを占めています。米国では、特にパルメザン、プロヴォローネ、モッツァレラなどのチーズを中心に乳製品の消費量が増加しており、これが乳製品パッケージング市場を押し上げると期待されています。この地域の先進的な酪農産業インフラ、厳格な食品安全規制、便利で革新的なパッケージングソリューションに対する消費者の需要は、この地域の優位性をさらに強化しています。

- 米国の乳製品パッケージング市場は、包装食品に対する消費者の嗜好の急速な変化と経済状況の影響を大きく受けています。乳製品ポートフォリオの大幅な拡大、特にスポーツ栄養、カジュアルユーザーの増加により、市場はさらに成長すると予想されます。

- 健康志向、持続可能性への懸念、eコマースの台頭といった要因も、乳製品業界のパッケージング動向を形成しています。消費者がタンパク質の豊富な製品を求めるようになり、パッケージ化された乳製品が多様な小売チャネルを通じて入手しやすくなるにつれて、乳製品の全国的な受け入れが増加し、市場が前進します。

- 米国農務省によると、米国における食用生乳生産量は2017年の2,154億英ポンド(2,679億1,000万米ドル)から2023年には2,266億英ポンド(2,818億4,000万米ドル)に増加します。このような生乳生産量の増加により、増加した量を処理し流通させるために、小売、バルク、流通目的により大きなパッケージングソリューションが必要となります。生乳生産量の増加は、製品の鮮度を確保し、貯蔵期間を延長し、様々な流通チャネルで多様な消費者の嗜好に対応する包装技術への投資に拍車をかけています。

- 北米市場での乳製品の絶え間ない発売も、包装メーカーにとってこの地域での存在感を強める大きなチャンスとなると思われます。2023年9月、北米オルヌア食品は、利便性と間食のしやすさを追求した、すぐに食べられるチーズスティックを特徴とする最新製品「Kerrygold Cheese Snacks」を発表しました。このような絶え間ないイノベーションが、市場における乳製品パッケージオプションの需要を押し上げると思われます。

乳製品パッケージング業界の概要

乳製品パッケージング市場は、複数の大手企業によって半固体化しています。革新的で持続可能なパッケージングにより、多くの企業が新たな契約を獲得し、新たな市場を開拓することで市場での存在感を高めています。市場の主要企業には、Amcor Group GmbH、Sealed Air Corporation、Berry Global Inc.、Ball Corporationなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- プロテインベースの製品に対する消費者の嗜好の高まり

- 小分けパッケージの採用増加

- 市場の課題

- 原材料コストの上昇が包装製品メーカーの成長を妨げる可能性

第6章 市場セグメンテーション

- 材料別

- プラスチック

- 紙・板紙

- ガラス

- 金属

- 製品別

- 牛乳

- チーズ

- 冷凍食品

- ヨーグルト

- 培養製品

- パッケージタイプ別

- ボトル

- パウチ

- カートン・箱

- 袋とラップ

- その他のパッケージタイプ

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- アジア

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 北米

第7章 競合情勢

- 企業プロファイル

- Huhtamaki Group

- Berry Global Inc.

- Amcor PLC

- Ball Corporation

- Altium Packaging

- Saudi Basic Industries Corporation

- International Paper Company

- Winpak Ltd

- Sealed Air Corporation

- Stora Enso Oyj

- Greiner Packaging international GmbH

第8章 投資分析

第9章 市場の将来

目次

The Dairy Packaging Market size is estimated at USD 25.71 billion in 2025, and is expected to reach USD 32.21 billion by 2030, at a CAGR of 4.61% during the forecast period (2025-2030).

Key Highlights

- The shift toward healthy snacking, increased consumption of ready-to-eat foods, and the rise of online and mobile shopping are transforming food purchasing and consumption patterns. These trends, combined with a growing focus on health-conscious eating, are expected to impact the dairy market significantly.

- The expanding availability of packaged dairy products through various retail channels, driven by population growth and changing diets, will likely boost market growth. Additionally, increasing consumer preference for protein-based products is expected to enhance the adoption of dairy-based items globally.

- Global trends in the dairy industry reveal that manufacturers are increasingly focusing on packaging to set their products apart. Today's dairy product packaging often boasts eye-catching designs and aseptic features. End users are adopting innovative packaging strategies for dairy products due to intense competition in key markets such as Japan, the broader Asia-Pacific region, Western Europe, and North America.

- Dairy manufacturers increasingly focus on capturing a larger share of the global dairy trade through improved international export capabilities and local production. This trend has fueled the demand for more advanced dairy packaging solutions.

- The diversification of packaging types has been a key factor in the expansion of dairy product sales. For example, milk, once available primarily in gable-topped cartons, is now often sold in portable, brand-friendly PET bottles, appealing to time-constrained consumers.

- However, the dairy packaging market faces challenges. Price fluctuations in packaging materials, influenced by food prices, may hinder market growth. Additionally, concerns about the potential health risks associated with plastic packaging, including fears of toxins linked to cancer or reproductive health issues, pose obstacles to market expansion.

Dairy Packaging Market Trends

Milk Occupies the Largest Market Share

- Milk is the most consumed dairy product globally. Its high moisture and mineral content pose significant storage challenges for vendors, leading to the prevalence of milk powder and processed milk in the trade. These characteristics make fresh milk highly perishable, necessitating advanced preservation and packaging techniques to maintain quality and extend shelf life.

- Current milk processing technology allows liquid milk to be bottled and stored at 4-8°C to maintain a shelf life of 10 to 21 days. Advanced processes like ultra-high temperature (UHT) treatment have extended packaged milk's shelf life up to a year without refrigeration. This technological advancement has revolutionized milk distribution, allowing for broader market reach and reduced waste.

- There has been a trend toward encouraging local production in recent years, particularly in Asia. This shift aims to reduce dependency on imports and support domestic dairy industries. A notable supply-demand gap persists despite countries like India contributing approximately 16% of global milk production. This discrepancy highlights the need for improved infrastructure and distribution networks in developing markets.

- Moreover, the rise of innovative and eco-friendly milk packaging is boosting the market's top line. This trend spans multiple packaging formats, such as bottles, cartons, and pouches. For example, in July 2024, Delamere Dairy unveiled its CartoCan Flavoured Milk range, targeting on-the-go consumers. The fully recyclable CartoCan reduces plastic waste and offers a handy alternative to the conventional 500 ml glass bottle.

- According to the USDA Foreign Agricultural Service, global cow milk production has steadily increased. Worldwide cow milk production rose from 511.6 million metric tonnes in 2017 to approximately 549.48 million metric tonnes in 2023. This growth reflects increasing global demand for dairy products and improvements in dairy farming practices and technologies.

- The dairy industry is witnessing a surging demand for aseptic packaging. Rising global milk output is set to unlock new market opportunities. Also, there has been a remarkable shift in consumer behavior, highlighted by the soaring consumption of UHT milk. As consumers aim to reduce their trips to the store, the demand for UHT milk boasting an extended shelf life has surged. Notably, there has been a discernible shift in consumer preference within dairy solutions, moving from loose milk to packaged offerings from major brands, especially those supplying in bulk.

North America Occupies the Largest Market Share

- North America holds the largest share of the global dairy packaging market, driven by increased production and sales of dairy products such as milk, cheese, and yogurt. In the United States, dairy product consumption has risen, particularly for cheese varieties like parmesan, provolone, and mozzarella, which is expected to boost the dairy packaging market. The region's advanced dairy industry infrastructure, stringent food safety regulations, and consumer demand for convenient and innovative packaging solutions further reinforce its dominance.

- The US dairy packaging market is significantly affected by rapidly changing consumer preferences toward packaged food and economic conditions. The market is expected to grow further due to the substantial expansion of the dairy product portfolio, especially in sports nutrition, and increasing casual users.

- Factors such as health consciousness, sustainability concerns, and the rise of e-commerce also shape packaging trends in the dairy industry. As consumers increasingly seek protein-rich products and packaged dairy goods become more accessible through diverse retail channels, the nationwide acceptance of dairy products is set to rise, driving the market forward.

- According to the US Department of Agriculture, milk production for human consumption in the United States rose from GBP 215.4 billion (USD 267.91 billion) in 2017 to GBP 226.6 billion (USD 281.84 billion) in 2023. This higher milk production necessitates greater packaging solutions for retail, bulk, and distribution purposes to handle and distribute the increased volume. The growth in milk production has spurred investments in packaging technologies that ensure product freshness, extend shelf life, and meet diverse consumer preferences across various distribution channels.

- Constant launches of dairy products in the North American market would also create a huge opportunity for packaging manufacturers to strengthen their presence in the region. In September 2023, Ornua Foods North America unveiled its latest offering, Kerrygold Cheese Snacks, featuring ready-to-eat cheese sticks designed for convenience and snacking ease. Constant innovations like this will drive up demand for dairy product packaging options in the market.

Dairy Packaging Industry Overview

The dairy packaging market is semi-consolidated, owing to several significant players. With innovative and sustainable packaging, many companies are increasing their market presence by securing new contracts and tapping new markets. Some of the major players in the market are Amcor Group GmbH, Sealed Air Corporation, Berry Global Inc., and Ball Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGTHS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Product

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Consumer Preference Towards Protein-based Products

- 5.1.2 Increasing Adoption of Packages Incorporating Small Portion Size

- 5.2 Market Challenges

- 5.2.1 Rising Raw Material Costs Could Hinder Growth for Packaging Product Manufacturers

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.2 Paper and Paperboard

- 6.1.3 Glass

- 6.1.4 Metal

- 6.2 By Product

- 6.2.1 Milk

- 6.2.2 Cheese

- 6.2.3 Frozen Foods

- 6.2.4 Yogurt

- 6.2.5 Cultured Products

- 6.3 By Package Type

- 6.3.1 Bottles

- 6.3.2 Pouches

- 6.3.3 Cartons and Boxes

- 6.3.4 Bags and Wraps

- 6.3.5 Other Package Types

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Huhtamaki Group

- 7.1.2 Berry Global Inc.

- 7.1.3 Amcor PLC

- 7.1.4 Ball Corporation

- 7.1.5 Altium Packaging

- 7.1.6 Saudi Basic Industries Corporation

- 7.1.7 International Paper Company

- 7.1.8 Winpak Ltd

- 7.1.9 Sealed Air Corporation

- 7.1.10 Stora Enso Oyj

- 7.1.11 Greiner Packaging international GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日