|

市場調査レポート

商品コード

1849887

北米のカーボンブラック:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)North America Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のカーボンブラック:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月16日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

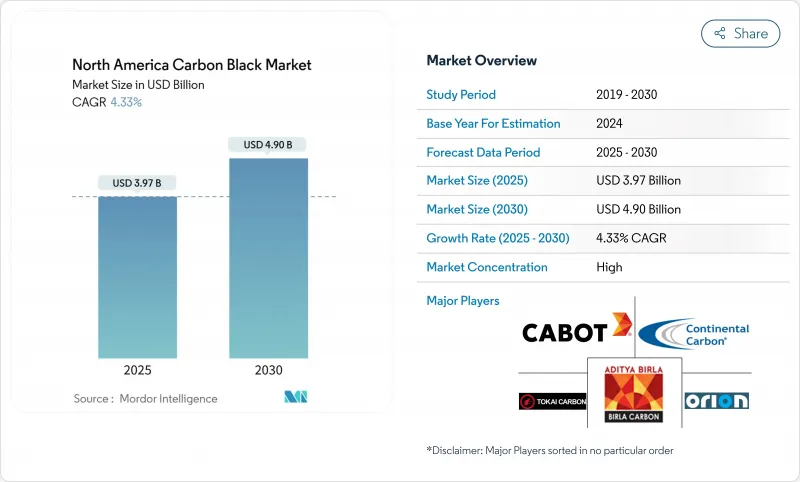

北米のカーボンブラック市場は、2025年に39億7,000万米ドルに達し、CAGR 4.33%で成長し、2030年には49億米ドルに達すると予測されています。

この成長軌道は、タイヤ業界の電動モビリティへの継続的なシフト、安定したプラスチック需要、地域の継続的なインフラ投資から恩恵を受ける、成熟しているが回復力のあるセクターを反映しています。米国メキシコ湾岸沿いの堅調な原料供給力と、エネルギー集約度を下げるプロセス改善により、生産者のマージンが強化され、特殊グレードへの的を絞った投資が可能になっています。一方、カナダでは規制の追い風が、メキシコでは建設主導の需要が、それぞれプレミアム化と最終用途の多様化を促進しています。競争戦略の中心は、回収カーボンブラックのスケールアップ、独自の表面改質、タイヤメーカーやバッテリーメーカーとの統合供給契約となってきており、北米のカーボンブラック市場は2030年までバランスの取れた成長を遂げることができます。

北米のカーボンブラック市場の動向と洞察

高表面積ファーネスブラックを必要とするワイドベースEV用タイヤの需要急増

ワイドベースの電気自動車用タイヤは、標準的な乗用車用タイヤよりも1本当たりのカーボンブラック使用量が多いです。タイヤメーカーは、耐久性を維持しながら転がり抵抗を下げる高表面積ファーネスブラックを採用しています。持続可能なカーボンブラック前駆体を配合したグッドイヤーの実証タイヤは、グリップを犠牲にすることなく転がり抵抗の低減を達成し、この材料戦略を検証しています。EV専用タイヤのOEM装着目標は、スペシャルティブラックの普及を加速させ、北米のカーボンブラック市場全体の平均販売価格を高めると予測されます。そのため、先進的な粒度制御技術を持つサプライヤーは、大手EVタイヤメーカーとの長期供給契約を確保できる立場にあります。EVの性能基準によって創出されたプレミアムセグメントは、従来のタイヤの販売量が頭打ちになったとしても、粗利率を引き上げると予想されます。

米国メキシコ湾岸の製油所から低コストでデカントオイルが供給され、生産者のマージンが向上

2025年の原油生産量は1,350万b/dまで増加し、ファーネスブラック製造の主要原料であるデカントオイルの安定供給が確保されます。メキシコ湾岸の製油所近隣の生産者は、欧州やアジアの同業他社よりも低い配送原料コストを享受しており、持続的なコスト優位性を生み出しています。この差は、北米の供給業者に、短期的な収益性を損なうことなく、反応炉をエネルギー回収システムで改修し、回収カーボンブラックのパイロットラインに資金を供給するための資本の柔軟性を与えています。その結果、生産能力の合理化圧力は依然として低く、北米のカーボンブラック市場は、効率的な事業者に有利な、競争的だが安定した価格設定環境の恩恵を受け続けています。また、このコスト・クッションは、バイオベース原料や循環型原料の調査を後押しし、地域の生産者を持続可能性革新の最前線に立たせています。

湾岸地域の供給混乱に伴う原料価格の変動

ハリケーン活動や製油所のメンテナンス停止は、定期的にデカントオイルの流量を制限し、スポット価格の高騰を引き起こして、非統合型カーボンブラック生産者のマージンを侵食しています。米国エネルギー情報局は、メキシコ湾岸の短時間の混乱でさえ、地域の原料市場に急速に波及し、一部のプラントは稼働率の低下を余儀なくされると指摘しています。供給業者は貯蔵タンクを拡張し、商品ヘッジプログラムを採用して変動を緩衝しているが、在庫の積み増しは運転資金の必要性を高める。バランスシート能力を欠く小規模企業は、操業コストの分散に直面し、北米のカーボンブラック市場の統合を加速させる可能性があります。長期的には、代替スラリー油の使用を可能にするマルチ原料の柔軟性への投資が価格の変動を和らげるはずだが、短期的には、予測不可能性が依然として逆風となっています。

セグメント分析

ファーネスブラックは2024年の北米のカーボンブラック市場で85%のシェアを維持し、多様な原料に対応する柔軟なリアクター構成を活用し、大量生産用途で一貫した品質を実現しています。このセグメントのシェア85%はCAGR見通し4.71%に相当し、北米のカーボンブラック市場全体の成長率を上回り、ユニットコストと排出量を削減するエネルギー回収アップグレードに支えられています。サーマルブラック、ガスブラック、ランプブラックは総じてニッチセグメントを占め、特殊なプラスチック、インク、電池部品など、独自の粒子径や純度が不可欠なものに供給されます。能力拡張は、タイヤおよび機械ゴム製品メーカーからの旺盛な需要に支えられ、引き続きファーネス技術に集中しています。

継続的な炉の技術革新により、粒度分布の厳格化と表面化学のカスタム化が可能になり、生産者は高度なバッテリーや軽量複合部品向けのグレードをオーダーメイドできるようになります。タイヤ熱分解油のような循環型原料は、処理能力を犠牲にすることなく炉の運用を脱炭素化するために試験的に使用されています。これらの進歩は、ファーネスブラックの構造的優位性を強化し、業界が持続可能性の要請と性能要件を統合する中で、このプロセスがリーダーシップを維持することを確実にします。

標準グレードは2024年の販売量の78%を占めたが、特殊グレードはベースラインの市場成長を上回る5.22%のCAGR予測に助けられ、利益の不均衡なシェアを生み出しました。導電性グレードと静電散逸性グレードは、導電性が充電速度とサイクル寿命を決定するリチウムイオン電池において重要な役割を果たすため、まだ小さいながらも急速に拡大しています。

Journal of Power Sources誌に掲載された調査では、最適な導電性カーボンブラックの微細構造が、より高い電池エネルギー密度と関連しており、電池メーカーが長期供給契約を結ぶよう促しています。このような技術的な依存関係は、スイッチングの障壁を高め、価格設定の弾力性を強化します。OEMがより高いリサイクル率を追求する中、rCBとバージンのスペシャルティブラックをブレンドしたハイブリッド配合は、北米のカーボンブラック業界全体の価値創造を拡大する態勢を整えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高表面積のファーネスブラックを必要とするワイドベースEVタイヤの需要急増

- 米国湾岸の製油所からの低コストのデカントオイル供給が生産者の利益率を向上

- カナダのタイヤラベル規制により特殊グレードの採用が増加

- OEMのESG目標達成により回収カーボンブラック(rCB)の需要が増加

- メキシコのインフラ建設業の回復がプラスチックとコーティングの需要を刺激

- 市場抑制要因

- メキシコ湾岸の供給途絶による原料価格の変動

- 乗用車トレッドコンパウンドにおけるシリカ-シラン置換

- タイヤ熱分解由来フィラーとの競合

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

第5章 市場規模と成長予測(価値と量)

- プロセスタイプ別

- ファーネスブラック

- ガスブラック

- ランプブラック

- サーマルブラック

- グレード別

- 標準グレードカーボンブラック

- 特殊カーボンブラック

- 導電性およびESDカーボンブラック

- 用途別

- タイヤおよび工業用ゴム製品

- プラスチック

- トナーと印刷インク

- コーティング

- 繊維

- その他の用途

- エンドユーザー業界別

- 自動車・輸送

- パッケージ

- 建築・建設

- 電気・電子工学

- 繊維・アパレル

- その他

- 地域別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cabot Corporation

- Birla Carbon

- Orion Engineered Carbons S.A.

- Continental Carbon Company

- Tokai Carbon Co., Ltd.(incl. Cancarb)

- Mitsubishi Chemical Corporation

- OMSK Carbon Group

- PCBL Limited

- Imerys

- Monolith Inc.

- Pyrolyx AG

- Koppers Inc.

- Sid Richardson Carbon & Energy Co.

- International China Rubber Investment Holding Co., Ltd.