|

市場調査レポート

商品コード

1550325

中国の監視アナログカメラ市場:シェア分析、産業動向と統計、成長予測(2024年~2029年)China Surveillance Analog Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の監視アナログカメラ市場:シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

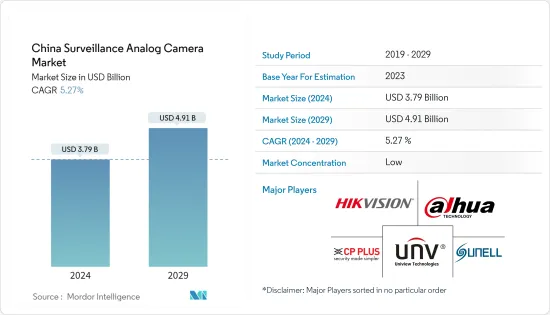

中国の監視アナログカメラ市場規模は2024年に37億9,000万米ドルと推定され、2029年には49億1,000万米ドルに達し、予測期間(2024-2029年)のCAGRは5.27%で成長すると予測されます。

主なハイライト

- 中国はアナログカメラのインフラが充実しており、さまざまな分野に数百万台のカメラが普及しています。企業や当局がこれらのアナログシステムを使い続けているため、互換性のあるアナログカメラへの需要が高まっています。アナログカメラからデジタルIPカメラへの移行には、新しい機器やインフラへの多額の投資が必要であり、特に中小企業セグメントの多くの組織にとって大きなハードルとなっています。

- アナログ監視カメラには、IPベースのデジタル・システムよりも簡単な設置プロセスなど、いくつかの利点があります。専門的な機器や労力が少なくて済むため、全体的な設置コストを削減できます。このため、特に予算が限られているプロジェクトでは、アナログカメラはより利用しやすく、費用対効果の高い選択肢となります。

- 中国の特定の業界や政府機関は、セキュリティや監視用のカメラを規定する規制を実施しています。このような規制は、主にデータ・プライバシーとセキュリティへの懸念が動機となっており、アナログ・カメラの需要を支えています。例えば、2024年2月、国家発展改革委員会(NDRC)は、政府出資の中国のデベロッパーがプロジェクトに監視装置を組み込むことを義務付けると発表しました。この規制は、最低3,000万人民元(~420万米ドル)の政府資金を持つ企業に適用されます。このようなイニシアチブは、予測期間中の研究市場の成長をサポートすると予想されます。

- しかし、アナログカメラは、デジタルIPベースのカメラと比較して、画質、解像度、高度な機能の面で固有の制限があります。より高品質でスマートな監視ソリューションへの需要が高まるにつれ、アナログカメラとIPカメラの間の技術的なギャップはより明白になります。このため、アナログカメラがより高度な機能を必要とする用途に特化し続けることは困難な課題となっています。

- 中国の監視カメラ産業は、マクロ経済要因、特に米国と中国の貿易戦争の影響を大きく受けています。米国政府によるハイエンド・チップやチップ技術の中国への輸出制限は、深刻な影響を及ぼしています。その結果、主要企業はこれらの高度なチップを調達する上でハードルに直面し、チップ輸入の減少と監視用アナログカメラ市場におけるハードウェア部品の直接的な改善につながった。しかし、半導体/電子デバイス製造の現地エコシステムが強化され、調査された市場の成長にとって将来は有望と思われます。

中国監視用アナログカメラ市場の動向

アナログカメラの費用対効果が予算制約のある中小企業やプロジェクトにアピールし、市場の成長を支える

- 小売店、飲食店、地域サービスなどの小規模企業では、セキュリティ予算が限られているため、支援が必要になることが多いです。アナログカメラは、初期費用が抑えられるため、こうした企業にとって実行可能で経済的な選択肢となります。この手頃な価格により、財政に負担をかけることなく基本的な監視システムを構築できるため、中国の中小企業におけるアナログ監視カメラの普及を後押ししています。

- 小売業は、中小企業の存在感が大きい主要部門のひとつです。小売セクター全体でセキュリティと監視システムの導入が増加しており、小売業界の規模拡大が調査市場の成長に有利なエコシステムを構築しています。例えば、中国国家統計局によると、中国の消費財小売売上高は2023年に急増し、小売総売上高は約47兆1,000億人民元(~6兆4,800億米ドル)に達します。都市部は前年比7.1%増の40兆7,000億人民元(約5兆6,000億米ドル)、農村部は前年比8%増の6兆4,000億人民元(約9,000億米ドル)となった。

- 中国の地方自治体や市町村は、公共の安全とセキュリティのために厳しい予算内で運営されることが多いです。アナログ監視カメラは、このような事業体にとって費用対効果の高いソリューションであり、予算をかけずに監視ネットワークを構築・維持することができます。ハードウェア、設置、メンテナンスにかかる費用を削減できるアナログ・システムは、財政的な制約のある地域でセキュリティ・インフラを強化するための現実的な選択肢です。

- さらに、アナログカメラは一般的に、デジタルIPベースの監視ソリューションよりもメンテナンスやサポートのコストが低くなります。よりシンプルなテクノロジーと確立されたサービス・エコシステムにより、メンテナンスやトラブルシューティングがより身近で、コスト効率に優れています。これは、技術リソースやメンテナンス予算が限られている組織にとって重要な考慮事項であり、アナログカメラの費用対効果をさらに高めます。

政府部門が大きな市場シェアを占める

- 中国政府は、国家レベルから地方レベルまで、公共の安全とセキュリティの強化を優先しています。政府機関や自治体は、犯罪防止、交通監視、緊急対応のための包括的な監視システムを確立するために、アナログカメラを幅広く導入しています。このように政府機関がアナログカメラを広く採用していることが、中国の監視用アナログカメラ市場の需要を大きく支えています。

- さらに、公共スペースや政府ビルなどの犯罪多発地域に設置された目に見えるアナログカメラは抑止力として機能し、犯罪行為の可能性を低下させる。監視され記録されているという意識は、個人が違法行為に手を染めることを抑制し、犯罪率の低下につながります。ChinaDaily』に掲載された調査によると、2023年に重大な暴力犯罪で起訴された人の数は61,000人と、1999年に報告された162,000人から大幅に減少しました。

- さらに、犯罪司法政策研究所(ICPR)が提供したデータによると、2023年、中国は米国に次いで受刑者数第2位の国となった。このような動向は、政府が公共の安全とセキュリティをより重視していることを示しており、これが中国における調査市場の成長を支える重要な要因の一つとなっています。

- 政府機関、特にセキュリティとインフラに重点を置く機関は、厳しい予算制限を満たすために多くの時間を必要とすることが多いです。アナログ監視カメラは、デジタルIPカメラに代わるコスト効率の高い選択肢として登場しました。この手頃な価格により、政府機関は予算の範囲内でカメラネットワークを拡大することができます。

- さらに、アナログ監視カメラは、特にデジタルIPベースのものと比較した場合、設置、操作、メンテナンスが簡単であることも評価されています。したがって、政府が公共監視機能の拡大に引き続き注力することで、予測期間中に新たな機会が創出されると予想されます。

中国監視アナログカメラ産業概要

中国の監視用アナログカメラ市場は、国内外のブランドが市場シェアを競っているため、もともと断片化されています。重要な企業は、イノベーションを継続するための研究開発投資や、競争力を維持するための提携、合併、買収などの戦略的イニシアティブを重視しています。主な市場プレイヤーは、Hangzhou Hikvision Digital Technology、Dahua Technology、CP PLUS、Zhejiang Uniview Technologies、Shenzhen Sunell Technology Corporationなどです。

- 2024年6月- 中国政府は、いじめや校内暴力に対抗するため、すべての小中学校の廊下、倉庫、屋上などの主要エリアに監視カメラを設置する計画を発表しました。このような取り組みが、調査対象市場の機会を促進すると予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- 市場のマクロ経済動向の評価

第5章 市場力学

- 市場促進要因

- アナログカメラの費用対効果が中小企業、地方自治体、予算制約のあるプロジェクトにアピールし、市場の成長を支える

- アナログカメラはよりシンプルな技術とユーザー・インターフェースを誇り、設置が容易です。

- 市場抑制要因

- 技術的限界と代替品の存在

第6章 市場セグメンテーション

- エンドユーザー産業別

- 政府機関

- 銀行

- ヘルスケア

- 運輸・物流

- 産業

- その他(教育機関、小売業、企業)

第7章 競合情勢

- 企業プロファイル

- Zhuhai RaySharp Technology Co., Ltd.

- Zhejiang Uniview Technologies Co.,Ltd.

- Shenzhen TVT Digital Technology Co., Ltd.

- Shenzhen Sunell Technology Corporation

- JER TECHNOLOGY CO., LTD.

- Hanwha Vision Co., Ltd.

- Shenzhen MVTEAM Technology Co,Ltd

- Shenzhen LOYALTY-SECU Technology Co., LTD

- Jovision Technology Co., Ltd

- CP PLUS

- Dahua Technology Co., Ltd.

- Hangzhou Hikvision Digital Technology Co., Ltd.

第8章 投資分析

第9章 市場の将来

The China Surveillance Analog Camera Market size is estimated at USD 3.79 billion in 2024, and is expected to reach USD 4.91 billion by 2029, growing at a CAGR of 5.27% during the forecast period (2024-2029).

Key Highlights

- China boasts an extensive analog camera infrastructure, with millions of cameras spread across diverse sectors. Businesses and authorities continue to use these analog systems, fueling a sustained demand for compatible analog cameras. Transitioning from analog to digital IP cameras necessitates substantial investments in new equipment and infrastructure, posing a significant hurdle for numerous organizations, especially in the SME segment.

- Analog surveillance cameras offer several advantages, e.g., a more straightforward installation process than IP-based digital systems. They require less specialized equipment and labor, which reduces overall installation costs. This makes analog cameras a more accessible and cost-effective option, especially for projects with limited budgets.

- Specific industries and governmental bodies in China enforce regulations stipulating cameras for security and surveillance. These mandates, primarily motivated by data privacy and security apprehensions, sustain the demand for analog cameras. For instance, in February 2024, the National Development and Reform Commission (NDRC) announced that government-funded Chinese developers would be required to incorporate monitoring equipment into their projects. This regulation applies to companies with a minimum of CNY 30 million (~USD 4.2 million) in government funding. Such initiatives are anticipated to support the studied market's growth during the forecast period.

- However, analog cameras have inherent limitations in terms of image quality, resolution, and advanced features compared to digital IP-based cameras. As the demand for higher-quality and smart surveillance solutions grows, the technological gap between analog and IP cameras becomes more apparent. This can make it challenging for analog cameras to remain specific to applications that require more advanced capabilities.

- The Chinese Surveillance industry has been significantly affected by macroeconomic factors, notably the US-China trade war. The US government's restrictions on exporting high-end chips and chip technology to China have had profound implications. Consequently, Chinese companies are encountering hurdles in sourcing these sophisticated chips, leading to a decline in chip imports and a direct improvement of hardware components in the surveillance analog camera market. However, with the local ecosystem for semiconductor/electronic device manufacturing bolstering, the future appears promising for the studied market's growth.

China Surveillance Analog Camera Market Trends

Cost-Effectiveness of Analog Cameras' Appeals to Smaller Businesses and Projects with Budget Constraints, thereby Supporting the Market's Growth

- Small enterprises, like retail outlets, eateries, and local services, frequently need help with constrained security budgets. Analog cameras, with their modest initial costs, emerge as a viable and economical choice for these businesses. This affordability enables them to set up fundamental surveillance systems without straining their finances, bolstering analog surveillance cameras' prevalence in China's small and medium enterprises.

- Retail is among the major sectors wherein the prominence of SMEs is significant. With the adoption of security and surveillance systems increasing across the retail sector, the expanding size of the retail industry is creating a favorable ecosystem for the studied market's growth. For instance, according to the National Bureau of Statistics of China, China's retail sales of consumer goods witnessed a surge in 2023, with total retail sales hitting around CNY 47.1 trillion (~USD 6.48 trillion). Urban regions accounted for a significant CNY 40.7 trillion (~USD 5.60 trillion), up 7.1% year-on-year, while rural areas contributed CNY 6.4 trillion (~USD 0.9 trillion), up 8% year-on-year.

- Local governments and municipalities in China frequently operate within tight budgets for public safety and security. Analog surveillance cameras present a cost-effective solution for these entities, enabling them to establish and maintain surveillance networks without breaking the bank. Given their reduced hardware, installation, and maintenance expenses, analog systems are the pragmatic choice for bolstering security infrastructure in financially constrained areas.

- Further, analog cameras generally incur lower maintenance and support costs than digital IP-based surveillance solutions. Their simpler technology and well-established service ecosystem make them more accessible and cost-effective to maintain and troubleshoot. This is a crucial consideration for organizations with limited technical resources or maintenance budgets, further enhancing the cost-effectiveness of analog cameras.

Government Segment to Hold a Significant Market Share

- The Chinese government prioritizes enhancing public safety and security from national to local levels. Government agencies and municipalities extensively deploy analog cameras to establish comprehensive surveillance systems for crime prevention, traffic monitoring, and emergency response. This widespread adoption of analog cameras by governmental bodies significantly sustains demand in China's surveillance analog camera market.

- In addition, visible analog cameras in public spaces and high-crime areas such as government buildings serve as a deterrent, reducing the likelihood of criminal activities. The awareness of being monitored and recorded discourages individuals from engaging in unlawful behavior, leading to a decrease in crime rates. According to a study published in ChinaDaily, in 2023, the number of individuals charged with serious violent crimes dropped significantly to 61,000, a stark decline from the 162,000 reported in 1999.

- Furthermore, according to the data provided by the Institute of Crime and Justice Policy Research (ICPR), in 2023, China was the 2nd leading country in terms of the number of prisoners after the United States. Such trends shows the higher emphasis of the government on public safety and security, which is among the key factor supporting the studied market's growth in China.

- Government agencies, especially those focusing on security and infrastructure, frequently need more time to meet stringent budget limitations. Analog surveillance cameras have emerged as a cost-efficient alternative to their digital IP counterparts. This affordability enables government bodies to expand their camera networks within their financial confines.

- Furthermore, analog surveillance cameras are also lauded for their straightforward installation, operation, and maintenance, especially when contrasted with their digital IP-based counterparts. Hence, with the government continue to focus on expanding its public surveillance capabilities, new opportunities are anticipated to be created, during the forecast period.

China Surveillance Analog Camera Industry Overview

The China surveillance analog camera market is fragmented by nature, as domestic and international brands compete for their slice of the market share. Significant companies are emphasizing R&D investments to continue innovations and strategic initiatives like partnerships, mergers, and acquisitions to remain competitive. Some key market players are Hangzhou Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd., CP PLUS, Zhejiang Uniview Technologies Co., Ltd., and Shenzhen Sunell Technology Corporation.

- June 2024 - The Chinese government announced its plans to install surveillance cameras in key areas of all primary and secondary schools, including corridors, store rooms, and rooftops, to combat bullying and campus violence. Such initiatives are anticipated to drive opportunities in the studied market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Cost-Effectiveness of Analog Cameras' Appeals to Smaller Businesses, Local Governments, and Projects with Budget Constraints, Thereby Supporting the Market's Growth

- 5.1.2 Analog Cameras Boast Simpler Technology and User Interfaces, Rendering them Easier to Install

- 5.2 Market Restraint

- 5.2.1 Technological Limitations and Availability of Substitutes

6 MARKET SEGMENTATION

- 6.1 By End-User Industry

- 6.1.1 Government

- 6.1.2 Banking

- 6.1.3 Healthcare

- 6.1.4 Transportation and Logistics

- 6.1.5 Industrial

- 6.1.6 Others (Education Institutions, Retail, and Enterprises)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Zhuhai RaySharp Technology Co., Ltd.

- 7.1.2 Zhejiang Uniview Technologies Co.,Ltd.

- 7.1.3 Shenzhen TVT Digital Technology Co., Ltd.

- 7.1.4 Shenzhen Sunell Technology Corporation

- 7.1.5 JER TECHNOLOGY CO., LTD.

- 7.1.6 Hanwha Vision Co., Ltd.

- 7.1.7 Shenzhen MVTEAM Technology Co,Ltd

- 7.1.8 Shenzhen LOYALTY-SECU Technology Co., LTD

- 7.1.9 Jovision Technology Co., Ltd

- 7.1.10 CP PLUS

- 7.1.11 Dahua Technology Co., Ltd.

- 7.1.12 Hangzhou Hikvision Digital Technology Co., Ltd.