|

市場調査レポート

商品コード

1550207

欧州の医薬品ガラス包装:市場シェア分析、産業動向、成長予測(2024~2029年)Europe Pharmaceutical Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の医薬品ガラス包装:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

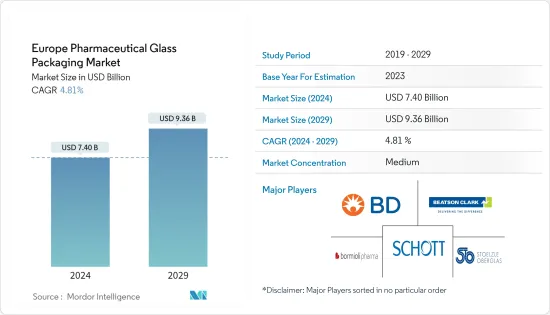

欧州の医薬品ガラス包装市場規模は2024年に74億米ドルと推定・予測され、2029年には93億6,000万米ドルに達し、予測期間中(2024-2029年)のCAGRは4.81%で成長すると予測されています。

同市場は、ヘルスケア製品に対する継続的な需要の増加など、主要な重要な要因により成長しています。同地域は医薬品の研究開発、生産、販売に注力しています。人口動態の変化、慢性疾患の増加、予防とセルフメディケーションへの関心の高まりが市場を牽引しています。

主なハイライト

- 平均寿命の伸びと高齢化により、一部の医薬品、特に変性疾患治療薬の需要が高まっています。過去10年間で、バイオテクノロジー業界は発展し、大学からスピンアウトした小規模なバイオテクノロジー新興企業や、業界関係者間の提携が増加しています。

- 高齢化社会では変性疾患の罹患率が高くなることが多く、医薬品に対する需要が高まっています。バイアルとアンプルは、特に高齢化に伴う症状に対する医薬品の包装と配送において極めて重要です。医薬品の需要が高まるにつれて、適切な包装ソリューションのニーズも高まり、バイアルおよびアンプル市場の成長に寄与しています。

- FEVEによると、2023年、欧州ガラス容器製造業者連盟の会員総数は年間2,000万トンを超えます。会員は60社で、ほぼ20のグループに分かれています。欧州の23の州に広がるこれらの製造工場には、世界の優良企業や、世界の主要消費者ブランド向けの重要な企業が含まれています。この地域の幅広いガラス容器製造部門は、医薬用ガラス包装市場を活用すると思われます。

- さらに、欧州製薬団体連合会(EFPIA)によると、2023年には欧州の医療費の平均18.4%が医薬品やその他の医療品に充てられます。がんや関節リウマチのような高額な疾患では、医薬品は総医療費の20%近くを占める。医薬品はまた、例えば入院や長期療養費など、ヘルスケアの他の分野でのコストを大幅に削減することによって、さらなる節約を生み出すことができます。

- 従来、医薬品の包装にはガラスが好んで使われてきました。しかし、原料価格やその他の要因により、これらの材料は時間の経過とともに高価になり、大量消費される製品を包装するための経済的に実行可能なソリューションを提供できなくなった。そのため、製薬業界ではプラスチックが選択肢として登場し、ガラス包装市場の成長を妨げる可能性があります。

欧州の医薬品ガラス包装市場の動向

ドイツが市場で大きなシェアを占める見込み

- ドイツは製薬とライフサイエンスにおける世界的リーダーの1つとして際立っています。欧州最大級の医薬品市場を誇り、数多くの業界トップランナーを抱え、急成長するバイオテクノロジーを育み、強固な公的ヘルスケアシステムを運営しています。個別化医療に対する世界の需要の高まりを受けて、ドイツは最先端のバイオ医薬品を生産する重要なプレーヤーとして台頭しました。

- ドイツの医薬品需要は、人口動態の変化と密接に結びついています。高齢化が進む中、医療介入、特に慢性疾患や運動関連の疾患の管理に対するニーズが高まっています。こうした人口動態の変化は、ニッチ医薬品メーカーやジェネリック医薬品メーカーにビジネスチャンスをもたらす一方で、ドイツの厳しい規制環境は、医薬品セクターに価格戦略の見直しを迫り、より幅広い市場へのアクセスを確保しています。

- ドイツ政府は、ドイツの製薬産業の条件を強化するためのいくつかの改革を盛り込んだ新しい製薬戦略を議論しています。最近では、戦略ペーパー4.0「ドイツにおける製薬セクターの一般的条件の改善」において、政府は市場アクセスと価格設定を強化するため、医薬品の研究と生産を強化しています。

- これらのイニシアチブはライフサイエンス・セクター全体に波及し、臨床試験の迅速な承認、最先端医薬品への迅速なアクセス、デジタル化の促進、供給セキュリティの強化、投資しやすい環境、官僚制の合理化などを約束しています。また、Statistisches Bundesamtによると、ドイツにおける医薬品卸売の売上高は2024年には2,203億4,000万米ドルに達すると予想されており、2021年の2,092億米ドルから増加しています。医薬品による収益の増加は、ガラス包装にテコ入れをもたらすと思われます。

- さらに、バイエルはドイツのレバークーゼンで固形医薬品を製造するSolida-1製薬施設を開発しています。同社はこの施設に2億7,500万ユーロ(2億8,698万米ドル)を投資しました。施設の建設は2020年に始まり、2022年5月に上棟式が行われました。施設は2024年に操業を開始する予定です。Solida-1施設は世界で最も近代的な製薬工場となり、がんや心血管疾患の治療薬の生産に注力します。

製薬用ガラス包装の成長

- 欧州の製薬用ガラス産業は、その技術革新と研究で知られており、同地域の成長の重要な原動力となっています。研究開発には数十億米ドルもの資金が投入され、そのために多くの労働力が割かれているため、英国は医薬品パイプラインを積極的に強化しています。このことは、ガラス瓶・アンプルのベンダーにとって有利な機会となります。

- さらに、医薬品市場が拡大するにつれ、医薬品用ガラス包装に対する需要も拡大しています。各社はアンプル、バイアル、シリンジを含む様々なガラス包装製品を導入し、製造能力と製品ポートフォリオを拡大しています。

- 政府が革新的な医薬品へのアクセスを確保することに注力していることから、医薬品セクターにおける研究開発活動が活発化する可能性があります。その結果、業界の進化するニーズに対応するために機能を改善したガラスバイアルやアンプルなど、新しく先進的な医薬品パッケージングソリューションが開発される可能性があります。

- 医薬品や医療機器を含む幅広い製品へのアクセスを確保するための幅広い取り組みの一環として、フランス政府が必須医薬品の生産を回復させる計画を立てていることは、フランスの医薬品用ガラス包装市場にいくつかの影響を与える可能性があります。

- 2023年6月、フランス政府は重要医薬品の生産を再構築するリショアリング計画を発表しました。リショアリングは、新薬や医療機器を含む全ての医療製品への患者のアクセスを確保するための、より重要な努力の一環であり、将来的な供給不足によって悪影響を受ける可能性のある「確立された、または古い製品」でもあります。必要不可欠な医薬品の生産を再調達することは、国内生産に重点を置くことを意味します。このことは、医薬品の増産に対応するため、医薬用ガラスバイアルやアンプルなどの包装資材の需要増につながる可能性があります。

- さらに、新薬の開発に注力することで、市場の拡大が見込まれます。EFPIAによると、EMAによって承認された医薬品の数は、2023年にはドイツが147品目で首位に立ち、イタリア、オーストリアなどがこれに続く。医薬品の増加は、この地域の医薬品セクターにおけるガラス包装を促進するかもしれないです。

欧州の医薬品ガラス包装業界の概要

欧州の医薬品ガラス包装市場は、Bormioli Pharma SpA Inc.、SGD SA、Schott AG、Stolzle Oberglas GmbHのような企業の存在により断片化されています。

- 2024年1月- 医薬品の封じ込めソリューションとデリバリーシステムを提供するショット・ファーマが、深冷保存に最適なガラス製バイアルを発売。ショットファーマのEVERICフリーズバイアルは、ガラス管、バイアルの形状、製造工程を最大限に活用するために強度を高めています。同社の科学的強度試験により、新しいバイアルは標準的なバイアルを凌駕することが明らかになっており、疾患、がん、中枢神経系疾患の治療に使用される凍結薬剤のための信頼できるソリューションとなっています。

- 2024年1月- イタリアに本社を置くボルミオリ・ファーマ社は、北米での売上高が47%増と大幅に急増したことを報告しました。この成長は、同社のインフラと生産能力の戦略的強化、特にガラスバイアルへの需要の高まりによるものです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- 市場促進要因

- 医薬品研究開発への支出の増加が市場開拓の原動力となる見通し

- 持続可能な包装に対する需要の増加

- 市場抑制要因

- ガラスの破損と剥離が市場成長を制限する可能性

第5章 市場セグメンテーション

- 製品別

- ボトル

- バイアル

- アンプル

- カートリッジとシリンジ

- その他の製品

- 国別

- ドイツ

- 英国

- フランス

- イタリア

第6章 競合情勢

- 企業プロファイル

- Bormioli Pharma SpA

- Stolzle Oberglas GmbH

- Beatson Clark

- Becton, Dickinson, and Company

- SGD Pharma

- Ardagh Group SA

- Gaasch Packaging

- Piramal Enterprises Ltd

- PGP Glass Private Limited

第7章 投資分析

第8章 市場機会と今後の動向

The Europe Pharmaceutical Glass Packaging Market size is estimated at USD 7.40 billion in 2024, and is expected to reach USD 9.36 billion by 2029, growing at a CAGR of 4.81% during the forecast period (2024-2029).

The market is growing due to major vital factors, such as the continuously increasing demand for healthcare products. The region is focused on pharmaceutical R&D, production, and sales of medicines. The market is driven by demographic change, a rise in chronic diseases, and an increasing focus on prevention and self-medication.

Key Highlights

- Rising life expectancy and an aging population have boosted the demand for some drugs, particularly those for degenerative diseases. Over the past decade, the industry has evolved, with small biotech start-ups being spun out of universities and a growing number of collaborations between industry players.

- The aging population often experiences a higher prevalence of degenerative diseases, leading to an increased demand for pharmaceuticals. Vials and ampoules are crucial in packaging and delivering medications, especially for conditions associated with aging. As the demand for drugs rises, so does the need for suitable packaging solutions, contributing to the vial and ampoules market growth.

- According to FEVE, in 2023, the Federation of European Manufacturers of Glass containers has a membership that collectively churns out over 20 million tonnes of glass annually. With 60 corporate members, they are part of nearly 20 distinct groups. Spread across 23 European States, these manufacturing plants include global blue-chip giants and significant players catering to the world's leading consumer brands. The region's wide glass container manufacturing sector would leverage the pharmaceutical glass packaging market.

- Further, according to the European Federation of Pharmaceutical Industries and Associations (EFPIA), in 2023, medicines constitute, on average, 18.4% of health expenditures in Europe on pharmaceuticals and other medical goods. For costly diseases such as cancer and rheumatoid arthritis, medicines account for close to 20% of the total disease costs. Medicines can also generate additional savings, for instance, by substantially reducing costs in other areas of healthcare, including hospital stays and long-term care costs.

- Traditionally, glass was the preferred material for pharmaceutical packaging. However, due to raw material prices and other factors, these materials became expensive over time and could not provide economically viable solutions for packaging products for mass consumption. That marked the advent of plastics as an option in the pharmaceutical industry, which might hinder the market's growth in glass packaging.

Europe Pharmaceutical Glass Packaging Market Trends

Germany is Expected to Have a Significant Share in the Market

- Germany stands out as one of the global leaders in pharmaceutical and life sciences. It boasts one of Europe's largest pharmaceutical markets, hosts numerous industry frontrunners, nurtures a burgeoning biotech landscape, and operates a robust public healthcare system. Responding to the surging global demand for personalized medicine, Germany emerged as a critical player in producing cutting-edge biopharmaceuticals.

- The demand for pharmaceuticals in Germany is intricately tied to its shifting demographics. With a progressively aging population, there's a heightened need for medical interventions, especially in managing chronic and mobility-related ailments. While these demographic shifts present opportunities for niche and generic drug manufacturers, the stringent regulatory environment in Germany is compelling the pharmaceutical sector to recalibrate pricing strategies, ensuring broader market accessibility.

- The German government is discussing a new Pharma Strategy with several reforms to enhance the conditions for the pharmaceutical industry in Germany. Recently, in Strategy Paper 4.0 - Improving the General Conditions for the Pharmaceutical Sector in Germany, the government is strengthening pharmaceutical research and production to enhance market access and pricing.

- These initiatives are poised to resonate across the life sciences sector, vowing faster clinical trial approvals, swifter access to cutting-edge medicines, heightened digitalization, bolstered supply security, an environment more conducive to investments, and a streamlined bureaucracy. Also, according to Statistisches Bundesamt, the revenue of wholesale pharmaceutical goods in Germany is expected to reach USD 220.34 billion in 2024, and it has increased from USD 209.2 billion in 2021. An increase in revenue from pharmaceutical goods would leverage the glass packaging.

- Additionally, Bayer is developing the Solida-1 pharmaceutical facility in Leverkusen, Germany, to produce solid pharmaceutical products. The company invested EUR 275 million (USD 286.98 million) in the facility. Construction of the facility began in 2020, and a topping-up ceremony was held in May 2022. The facility is expected to start operations in 2024. The Solida-1 facility will be the world's most modern pharmaceutical plant, focusing on producing drugs for cancer and cardiovascular diseases.

Growing Traction of Pharmaceutical Glass Packaging in the Region

- The European pharmaceutical glass industry is known for its innovation and research and is a crucial driver of growth in the region. With billions allocated to R&D and a substantial workforce dedicated to these endeavors, the UK is actively bolstering its pharmaceutical pipeline. This presents a lucrative opportunity for glass vial and ampoule vendors.

- Moreover, as the pharmaceutical market expands, so does the region's demand for pharmaceutical glass packaging. Players introduce a variety of glass packaging products, including ampoules, vials, and syringes, and they scale up their manufacturing capabilities and product portfolios.

- The government's focus on ensuring access to innovative medicines may lead to increased research and development activities in the pharmaceutical sector. This could result in the development of new and advanced pharmaceutical packaging solutions, including glass vials and ampoules with improved features to meet the industry's evolving needs.

- The French government's plan to restore the production of essential medicines as part of its broader effort to ensure access to a wide range of products, including pharmaceuticals and medical devices, can have several implications for the pharmaceutical glass packaging market in France.

- In June 2023, the French government announced its reshoring plan to restructure the production of critical medicines. Reshoring is part of a more significant effort to ensure patient access to all medical products, including new drugs and equipment, and the 'established or older products that may be adversely affected by future shortages. Reshoring the production of essential medicines implies an increased focus on domestic manufacturing. This could lead to a rise in demand for packaging materials, including pharmaceutical glass vials and ampoules, to accommodate the increased production of medicines.

- Moreover, the market is expected to grow with a focus on developing new medicines. According to EFPIA, the number of drugs approved by the EMA available to patients, Germany took the top position with 147 approved medicines in 2023, followed by Italy, Austria, and other countries. An increase in medications might propel glass packaging in the pharmaceutical sector across the region.

Europe Pharmaceutical Glass Packaging Industry Overview

The European pharmaceutical glass packaging market is fragmented due to the presence of players like Bormioli Pharma SpA Inc., SGD SA, Schott AG, and Stolzle Oberglas GmbH, upscaling the market with substantial R&D investments, driving toward sustainability and digitization of the packaging industry in Europe.

- January 2024 - SCHOTT Pharma, a pharmaceutical drug containment solutions and delivery systems company, launched glass vials optimized for deep-cold drug storage. SCHOTT Pharma's EVERIC freeze vials feature increased strength to maximize glass tubing, vial geometry, and the production process. The company's scientific strength tests have revealed that the new vials outperform standard vials, making them a reliable solution for frozen medications used to treat diseases, cancer, and central nervous system disorders.

- January 2024 - Bormioli Pharma, headquartered in Italy, reported a substantial 47% surge in its North American sales. This growth is attributed to the company's strategic enhancements in infrastructure and production capacity, notably the rising demand for glass vials.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Market Drivers

- 4.4.1 Increasing Spending on Pharmaceutical Research and Development is Expected to Drive the Market's Growth

- 4.4.2 Increasing Demand for Sustainable Packaging

- 4.5 Market Restraints

- 4.5.1 Glass Breakage and Delamination May Restrict the Market's Growth

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Bottles

- 5.1.2 Vials

- 5.1.3 Ampoules

- 5.1.4 Cartridges and Syringes

- 5.1.5 Other Products

- 5.2 By Country

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 France

- 5.2.4 Italy

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bormioli Pharma SpA

- 6.1.2 Stolzle Oberglas GmbH

- 6.1.3 Beatson Clark

- 6.1.4 Becton, Dickinson, and Company

- 6.1.5 SGD Pharma

- 6.1.6 Ardagh Group SA

- 6.1.7 Gaasch Packaging

- 6.1.8 Piramal Enterprises Ltd

- 6.1.9 PGP Glass Private Limited