|

市場調査レポート

商品コード

1550153

欧州の電子試験および計測:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Europe Electronic Test And Measurement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の電子試験および計測:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

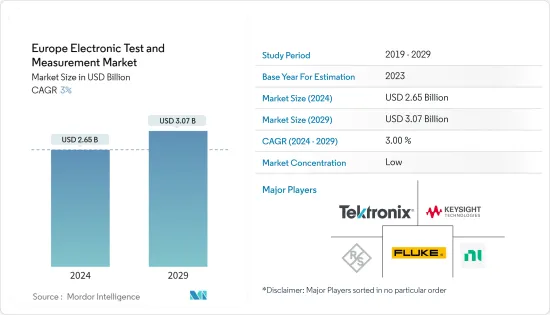

欧州の電子試験および計測市場規模は2024年に26億5,000万米ドルと推定・予測され、2029年には30億7,000万米ドルに達し、市場推計・予測期間中(2024-2029年)にCAGR 3%で成長すると予測されます。

主なハイライト

- 技術の進歩が試験および計測機器の需要に拍車をかけ、電気自動車やハイブリッド車の台頭が重要な動向となっています。欧州委員会は、EUが世界有数の自動車生産国であり、自動車産業が民間の研究開発投資をリードしていることを強調しています。

- EVに対する世界の需要が急増するにつれ、販売状況にも顕著な変化が見られ、中国が重要な役割を果たすようになっています。2024年までには、EUで販売される電気自動車の4分の1が中国で生産されるようになると予測されており、中国の新参企業が現地の競合他社を圧倒していることを物語っています。欧州諸国によるこのような国内EV生産投資の急増は、電子試験および計測機器市場を顕著に押し上げました。

- また、電子機器が小型化するにつれて、最新のT&M技術はモノのインターネット、5G、M2Mのような新しい技術の評価に適応しています。特に、ドイツのような国では、DT、Telefonica、Vodafoneなどの大手通信事業者が5Gネットワークを展開しており、カバー率はドイツの人口の94%と75%に及んでいます。

- 機械学習(ML)や人工知能(AI)などの高度なデジタル技術の採用は、リアルタイムの作業監視に革命をもたらします。例えば、Keysight Technologies Inc.は、Nemo Device Application Test Suiteを発表しました。このソフトウェア・ソリューションは、自動化とAIを活用して、モバイル・ユーザーとネイティブ・アプリとのインタラクションの評価を合理化し、無線サービス・プロバイダーとアプリ開発者の双方に利益をもたらします。

- 一方、市場は価格への敏感さとレンタルサービスへの嗜好の高まりによる課題に直面しています。多くの企業、特に資本が限られている企業は、所有に伴う初期コストが高いことから、試験・測定機器のレンタルを選択しています。

欧州の電子試験および計測市場動向

電気自動車セグメントが著しい成長を遂げる見込み

- 自動車産業は欧州経済の要であり、同地域の国内総生産(GDP)に約7%貢献しています。長年にわたり、この産業は経済成長の推進と技術革新の促進に役立ってきました。現在進行中の都市化の動向は、英国、フランス、ドイツなどの主要市場におけるシェアード・モビリティ・サービスの人気の高まりと相まって、消費者の嗜好、ひいては自動車需要に大きな影響を与えています。

- 2022年から2023年にかけて、欧州では、特に新たなCO2基準の導入など、大幅な政策展開が見られました。これらの規制措置は、ゼロ・エミッションの道路交通への移行を加速させ、電気自動車(EV)の需要を大幅に押し上げる上で極めて重要であると予想されます。

- 国際エネルギー機関(IEA)のデータによると、欧州は2022年に、中国に次ぐ世界第2位の電気自動車市場の地位を確保しました。同地域は世界の電気自動車販売台数の25%を占め、世界在庫の30%を占めています。この分野の主要国には、ドイツ、英国、フランス、ノルウェー、オランダ、スウェーデン、イタリアが含まれ、欧州における電気自動車導入の最前線にあります。

- 2019年に小型車のCO2規制が実施されて以来、排出量の削減と気候変動への対応に新たな焦点が当てられています。欧州連合(EU)は、「Fit for 55」パッケージで示された2030年目標に合わせ、自動車とバンの厳しいCO2新基準を採択しました。欧州自動車工業会(ACEA)によると、EUの自動車市場は2023年に前年比13.9%の力強い成長を遂げ、年間総販売台数は1,050万台に達しました。

- 同地域で電気自動車が普及するにつれて、包括的な試験・認証サービスへの需要が大幅に増加すると予想されます。これらのサービスには、バッテリー性能と安全性試験、電気モーター評価、車両性能評価、充電器試験、および全体的な認証プロセスが含まれます。これらのサービスは、電気自動車の信頼性、安全性、効率性を保証し、欧州市場への普及と統合を支援します。

ドイツが大きな市場シェアを占める

- 世界的リーダーであるドイツの自動車産業は、国の基幹産業です。ドイツはハイテク自動車製品のフロントランナーとして台頭し、特に電気自動車(EV)と充電インフラの拡大に力を入れています。政府のコミットメントは明らかで、連邦経済・気候変動対策省は2022年に12億米ドルをバッテリーセル生産の強化に充て、世界のリーダーシップを目指しています。

- インセンティブと資金援助に裏打ちされたこのEVへの熱心な取り組みは、ドイツのバッテリー式電気自動車(BEV)の普及と市場シェアを大幅に押し上げました。その結果、BEVに対する需要の高まりは、EV産業における電子試験および計測機器の必要性の高まりを裏付けています。このような機器は、電流・電圧測定や充電通信などの重要な測定基準に関する洞察を提供する極めて重要なものです。

- 焦点を移すと、ドイツは欧州第3位の航空宇宙・防衛産業を誇り、軍事・航空宇宙費の世界シェアは注目に値します。2021年、国防省(MOD)は469億ユーロという多額の資金援助を受けました。この支援は2022年に増加し、国防省の配分は503億ユーロに上昇し、2026年まで一貫して年間501億ユーロのコミットメントが約束されました。国の野心的な2%目標が達成されれば、軍事費は2026年までに856億ユーロに急増する可能性があります。このような国防支出の増加は、航空宇宙・防衛産業における電子試験および計測機器のニーズの増加を示しています。

- 最後に、ドイツではネットワーク消費が急速に進化し、より高速なデータ・トランスミッションへのニーズが高まっているため、ファイバー・ネットワークが急増しています。この需要の主な原動力は、5G技術の要件であり、5G技術の高度な機能をサポートするためにより高密度のネットワーク・インフラが必要となります。帯域幅の利用が増加し、最先端技術のイントロダクションが導入されるにつれて、通信テスト・管理機器の需要は急増します。

欧州の電子試験および計測産業の概要

欧州の電子試験および計測市場は競争が激しく、複数のプレーヤーで構成されています。各社は、新製品の投入、事業の拡大、戦略的M&A、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主なプレーヤーには、Tektronix Inc.、Keysight Technologies、Teledyne LeCroy Inc.などがあります。

2023年9月Keysight Technologies Inc.は、業界をリードするInfiniiumオシロスコープのポートフォリオを拡張し、ハードウェア・アクセラレーションを搭載したInfiniium MXR Bシリーズを発表しました。

2023年9月NIは、第3世代のPXIベクトル信号トランシーバ(VST)であるPXIe-5842の新しいオプションと拡張機能を発表しました。PXIe-5842は、NIのソフトウェア・エコシステムと組み合わせることで、航空宇宙および防衛アプリケーションにおける製品のテストと検証が可能な多用途ツールです。信号解析、スペクトラム解析、信号生成などの従来のRF機能をサポートします。

2023年8月アドバンテスト・コーポレーションは、MPT3000ソリッド・ステート・ドライブ(SSD)テスト・プラットフォームに2つの機能を追加することを発表しました。独立熱制御(ITC)デバイス・インタフェース・ボード(DIB)とエンジニアリング・サーマル・チャンバ(ETC)は、効率的な少量生産エンジニアリング、早期テスト開発、SSDデバイスの品質保証を可能にすることで、MPT3000の早期エンジニアリング導入をターゲットとしています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因が電子試験および計測市場に与える影響

第5章 市場力学

- 市場促進要因

- 試験および計測機器の必要性につながる技術の進歩

- 電気自動車とハイブリッド車の新興動向

- 市場の課題

- 価格への敏感さとレンタルサービスへの嗜好の高まり

第6章 市場セグメンテーション

- タイプ別

- 半導体自動試験装置(ATE)

- 無線周波数(RF)試験機器

- デジタル試験機器

- 電気・環境試験

- データ収集(DAQ)

- 用途別

- 通信機器

- 半導体・コンピューティング

- 航空宇宙・防衛

- コンシューマーエレクトロニクス

- 電気自動車

- 国別

- 英国

- ドイツ

- フランス

第7章 競合情勢

- 企業プロファイル

- Tektronix Inc.

- Keysight Technologies

- Rohde & Schwarz GmbH & Co. KG

- National Instruments Corporation

- Fluke Corporation

- Teledyne LeCroy Inc.

- Yokogawa Test & Measurement Corporation

- Teradyne Inc.

- Chauvin Arnoux Group

- Advantest Corporation

第8章 投資分析

第9章 市場の将来

The Europe Electronic Test And Measurement Market size is estimated at USD 2.65 billion in 2024, and is expected to reach USD 3.07 billion by 2029, growing at a CAGR of 3% during the forecast period (2024-2029).

Key Highlights

- Technological advancements fuel the demand for test and measurement equipment, with the rise of electric and hybrid vehicles emerging as a significant trend. The European Commission highlights the EU as one of the globe's major motor vehicle producers, with its automotive industry leading in private R&D investments.

- As the global appetite for EVs surges, a notable shift is seen in the sales landscape, with China stepping into a prominent role. By 2024, projections suggest that a quarter of electric vehicles sold in the EU will originate from China, underscoring the traction Chinese newcomers are gaining over local competitors. This surge in domestic EV production investments by European nations notably bolstered the electronic test and measurement equipment market.

- Also, as electronic devices shrink, the latest T&M technologies adapt to assess newer technologies like the Internet of Things, 5G, and M2M. Notably, major telecom players in countries like Germany, including DT, Telefonica, and Vodafone, are rolling out 5G networks, with coverage extending to 94% and 75% of Germany's population.

- Adopting advanced digital technologies, such as machine learning (ML) and artificial intelligence (AI), revolutionizes real-time work monitoring. For example, Keysight Technologies Inc. unveiled the Nemo Device Application Test Suite. This software solution leverages automation and AI to streamline the assessment of mobile users' interactions with native apps, benefiting both wireless service providers and app developers.

- Conversely, the market faces challenges due to price sensitivity and a growing preference for rental services. Many companies, especially those with limited capital, opt to rent test and measurement equipment, given the high initial costs associated with ownership.

Europe Electronic Test And Measurement Market Trends

The Electric Vehicles Segment is Expected to Witness Significant Growth

- The automotive industry is a cornerstone of the European economy, contributing approximately 7% to the region's gross domestic product (GDP). Over the years, this industry has been instrumental in driving economic growth and fostering innovation. The ongoing trend toward urbanization, coupled with the rising popularity of shared mobility services in key markets such as the United Kingdom, France, and Germany, significantly influences consumer preferences and, consequently, the demand for automobiles.

- During the 2022-2023 period, Europe witnessed substantial policy developments, particularly the introduction of new CO2 standards. These regulatory measures are anticipated to be crucial in accelerating the transition toward zero-emission road transport, thereby significantly boosting the demand for electric vehicles (EVs).

- According to data from the International Energy Agency (IEA), Europe secured its position as the world's second-largest market for electric cars in 2022, second only to China. The region accounted for 25% of global electric car sales and held 30% of the global stock. Leading countries in this sector include Germany, the United Kingdom, France, Norway, the Netherlands, Sweden, and Italy, which are at the forefront of electric vehicle adoption in Europe.

- Since implementing the light-duty vehicle CO2 regulation in 2019, a renewed focus has been on reducing emissions and addressing climate change. The European Union has adopted stringent new CO2 standards for cars and vans, aligned with the 2030 targets outlined in the 'Fit for 55' package. According to the European Automobile Manufacturers' Association (ACEA), the EU car market experienced a robust 13.9% growth in 2023 compared to the previous year, reaching a total annual volume of 10.5 million.

- As electric vehicles become more prevalent across the region, the demand for comprehensive testing and certification services is expected to rise significantly. These services include battery performance and security testing, electrical motor assessments, vehicle performance evaluations, charger tests, and overall certification processes. These services ensure electric vehicles' reliability, safety, and efficiency, supporting their widespread adoption and integration into the European market.

Germany To Hold Significant Market Share

- Germany's automotive industry, a global leader, stands as the backbone of the nation's industry. Germany has emerged as a frontrunner in high-tech automotive products, with a particular focus on expanding its electric vehicle (EV) and charging infrastructure. The government's commitment is evident, with the Federal Ministry for Economic Affairs and Climate Action allocating a substantial USD 1.2 billion in 2022 to bolster the nation's battery cell production, aiming for global leadership.

- This dedication to EVs, backed by incentives and funding, has significantly boosted Germany's adoption and market share of battery electric vehicles (BEVs). Consequently, the rising demand for BEVs underscores a growing necessity for electronic test and measurement equipment in the EV industry. Such equipment is pivotal, offering insights into critical metrics like current and voltage measurements and charging communication.

- Shifting focus, Germany boasts Europe's third-largest aerospace and defense industry, with a notable global military and aerospace expenditure share. In 2021, the Ministry of Defense (MOD) received a substantial EUR 46.9 billion in funding. This support increased in 2022, with the MOD's allocation rising to EUR 50.3 billion and a consistent annual commitment of EUR 50.1 billion until 2026. If the nation's ambitious 2% target is met, military expenditure could soar to EUR 85.6 billion by 2026. This increase in defense spending indicates an increased need for electronic test and measurement equipment in the aerospace and defense industries.

- Lastly, as Germany witnesses a rapid evolution in network consumption and an increasing need for faster data transmission, the country is seeing a surge in fiber networks. This demand is largely driven by the requirements of 5G technology, which necessitates a denser network infrastructure to support its advanced features. With bandwidth usage on the rise and the introduction of cutting-edge technologies, the demand for communications test and management equipment is set to soar.

Europe Electronic Test And Measurement Industry Overview

The European electronic test and measurement market is highly competitive and consists of several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Tektronix Inc., Keysight Technologies, and Teledyne LeCroy Inc.

September 2023: Keysight Technologies Inc. expanded its industry-leading portfolio of Infiniium oscilloscopes with hardware-accelerated Infiniium MXR B-Series, which offers automated analysis tools that enable engineers to shorten time to market by finding anomalies quickly.

September 2023: NI announced new options and extended capabilities for its third-generation PXI Vector Signal Transceiver (VST), the PXIe-5842. Combined with NI's software ecosystem, the PXIe-5842 is a versatile tool that can test and validate products in aerospace and defense applications. This supports traditional RF capabilities such as signal analysis, spectrum analysis, and signal generation.

August 2023: Advantest Corporation announced two additions to its MPT3000 solid-state drive (SSD) test platform. The independent thermal control (ITC) device interface boards (DIBs) and engineering thermal chamber (ETC) target early engineering adoption of the MPT3000 by enabling efficient, small-batch engineering, early test development, and quality assurance for SSD devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macroeconomic Factors on the Electronic Test and Measurement Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technological Advancements Leading to the Need for Test and Measurement Equipment

- 5.1.2 Emerging Trend of Electric and Hybrid Vehicle

- 5.2 Market Challenges

- 5.2.1 Price Sensitivity and Increasing Preference for Rental Services

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Semiconductor Automatic Test Equipment (ATE)

- 6.1.2 Radio Frequency (RF) Test Equipment

- 6.1.3 Digital Test Equipment

- 6.1.4 Electrical and Environmental Test

- 6.1.5 Data Acquisition (DAQ)

- 6.2 By Application

- 6.2.1 Communications

- 6.2.2 Semiconductors and Computing

- 6.2.3 Aerospace and Defense

- 6.2.4 Consumer Electronics

- 6.2.5 Electric Vehicles

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tektronix Inc.

- 7.1.2 Keysight Technologies

- 7.1.3 Rohde & Schwarz GmbH & Co. KG

- 7.1.4 National Instruments Corporation

- 7.1.5 Fluke Corporation

- 7.1.6 Teledyne LeCroy Inc.

- 7.1.7 Yokogawa Test & Measurement Corporation

- 7.1.8 Teradyne Inc.

- 7.1.9 Chauvin Arnoux Group

- 7.1.10 Advantest Corporation