|

|

市場調査レポート

商品コード

1549891

産業オートメーションの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Industrial Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業オートメーションの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 213 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

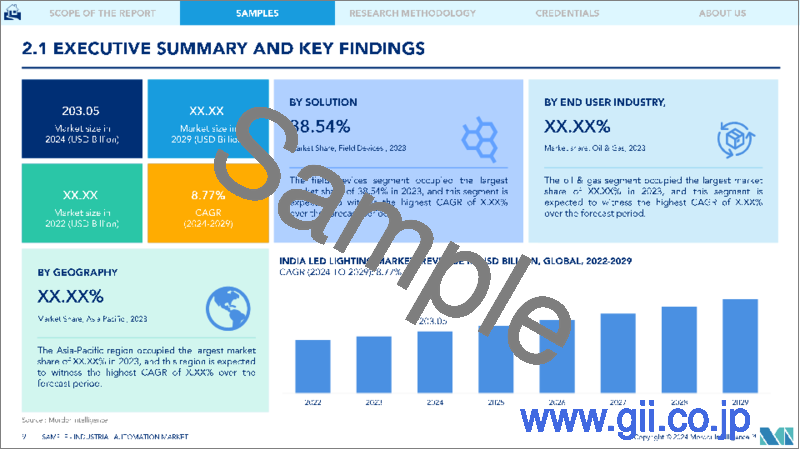

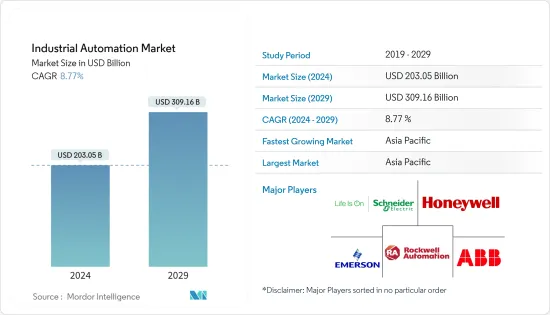

世界の産業オートメーションの市場規模は、2024年に2,030億5,000万米ドルと推定され、2029年には3,091億6,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR8.77%で成長すると予測されています。

主なハイライト

- 産業オートメーションは、発展途上国の輸出競争力を高める可能性があります。製造工程を自動化することで、これらの国々は、より迅速、効果的、安価に商品を作ることができ、世界市場での競争力を高めることができます。その結果、輸出レベルが向上し、外貨収入が改善され、新興国経済が改善される可能性があるため、新興経済諸国における産業オートメーション市場が活性化します。

- 産業オートメーションは、発展途上国の中小企業に大きな影響を与えます。オートメーションは、これらの企業の競争力を高め、持続的な成長を達成する可能性があります。中小企業が生産性を向上させ、業務を合理化し、大規模な顧客やサプライチェーンのニーズを満たすことを可能にします。例えば、産業オートメーションはリソースを最適化し、生産時間を短縮することで、人員を戦略的業務に振り向けることができます。国際ロボット連盟(IFR)によると、製造業では複数の工程を自動化することで、生産性が最大30%向上するといいます。

- 国際通貨基金(IMF)によると、新興市場および新興経済諸国の成長率は、2023年の4.3%に対し、2024年と2025年は4.2%と予測されています。インドのような多くの新興国では、インド市場におけるスクラップ政策、自動車ミッションプラン2026、生産連動型インセンティブ制度のようなインド政府によるいくつかの取り組みが、インドを二輪車・四輪車市場における重要なプレーヤーにすることが期待されています。このような政策には、オートメーション技術を採用し、市場調査に有利な環境を育成することが含まれます。

- オートメーション設備は、スマート製造のための高額な設備投資を義務付けています(オートメーションシステムの設置、設計、製作には数百万米ドルかかる場合があります)。ロボットシステム、コンベアベルト、センサー、制御システムなど、機器の購入コストは相当なものになります。ファクトリーオートメーション機器はまた、既存の生産システムへのカスタマイズと統合を必要とします。このプロセスには、特定の製造要件を満たすための機器の設計、エンジニアリング、プログラミングが含まれます。これは、調査対象市場の成長にとって大きな障害となります。

- 産業オートメーションソリューションのサプライチェーンや生産に見られる直接的な影響とは別に、パンデミックの後遺症も調査対象市場の成長に影響を与えています。例えば、北米を含む様々な地域に迫りつつある景気後退の脅威は、経済の先行き不透明感から消費者や企業が自動車などの高額製品や拡張プロジェクトに支出を増やせなくなり、調査対象市場の成長に悪影響を及ぼす可能性があります。

産業オートメーション市場の動向

石油・ガス産業が著しい成長を遂げる見通し

- 石油・ガス産業は、産業オートメーションソリューションの導入において圧倒的なセグメントとなっています。しかし、この産業における産業オートメーションの成長見込みは、他の発展途上産業と比較して限定的であるため、この産業の成長率は鈍化すると予想されます。

- 石油・ガスオートメーション(油田オートメーションとも呼ばれる)は、世界市場におけるエネルギー生産者の競争力強化を目的とした、デジタル技術を活用した一連のプロセスです。業界内の特定のセクターがオートメーションをより促進する一方、主要分野には掘削、生産業務、物流、安全、小売業務などが含まれます。石油・ガスのオートメーションは、主にIoTベースのセンサー、予測システム、AI駆動のエキスパート・システムに依存し、生産性を高め、労働力不足から生じるスキルギャップを埋めます。

- 石油・ガス業界の危険な環境は、オートメーションによってますます改善されつつあります。ロボットやオートメーションシステムが掘削、検査、メンテナンスなどの作業を処理し、人間がリスクにさらされる機会を大幅に減らしています。

- 業界は、緊急停止システムなどのオートメーション機能によって安全性を強化し、困難な状況への迅速な対応を保証しています。センサーやオートメーションツールを導入することで、企業は規制へのコンプライアンスを確保し、環境への影響を抑制しています。

- 石油・ガス産業は世界経済の重要な構成要素です。IEAによると、2024年の世界の液体燃料生産量は、OPEC+の自主的減産がOPEC+以外の供給増加によって相殺されるため、2023年の180万b/dの増加から鈍化し、80万b/d以上増加します。2024年のOPEC+の原油生産量は前年比で90万b/d減少するものの、OPEC+以外の生産量は米国、ガイアナ、ブラジル、カナダが牽引し、180万b/d増加すると予想されます。石油生産量の大幅な増加とデジタル化の進展に伴い、石油・ガス企業はデジタル技術とオートメーションへの依存度を高めています。

アジア太平洋が最速の成長を記録する見込み

- アジア太平洋には、中国、日本、韓国、台湾など、世界最大の製造業経済圏があります。自動車、エレクトロニクス、航空宇宙、医療機器などの製造業の拡大が続いており、産業オートメーションに対する大きな需要が生まれています。

- インドのような新興国が製造業を拡大し、自立を目指す取り組みは、市場の成長をさらに後押ししています。インドでは、製造業が高成長分野のひとつに浮上しています。メイク・イン・インディア」プログラムは、インドを製造業のハブとして世界地図に掲載し、インド経済を世界的に認知させています。IBEFによると、インドは2030年までに1兆米ドル相当の商品を輸出することが可能であり、世界の重要な製造ハブになる道を歩んでいます。

- インド政府は2025年までに5兆ドルの経済規模を目指しており、そのうち製造業は1兆ドルの価値があります。この目標を達成するためには、Make in IndiaやSkill India、Digital Indiaといったフラッグシッププログラムの融合が不可欠であり、それによってこの地域の市場成長が促進されます。

- 電気自動車をより早く普及させるため、バッテリー製造工場を建設する構想が進行中であることも、市場の成長をさらに後押ししています。例えば、リチャージ・インダストリーズは2023年8月、およそ30万台のEVにバッテリーを供給するため、年間生産能力30ギガワット時の工場を建設する計画を発表しました。2024年5月頃に着工し、2025年に生産を開始する予定です。

- この地域は、台湾セミコンダクター・マニュファクチャリング・カンパニーなどの企業の存在により、最大の半導体・電子製品メーカーとなっています。台湾は世界の半導体の60%以上、最先端の半導体の90%以上を生産しています。半導体のほとんどはTSMCが製造しています。

産業オートメーション産業の概要

産業オートメーション市場は、中小企業やグローバル企業が存在するため、非常に断片化されています。同市場の主要企業には、シュナイダーエレクトリックSE、ロックウェルオートメーション、ハネウェルインターナショナル、エマソン・エレクトリック、ABBリミテッドなどがあります。市場の主要企業は、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、買収やパートナーシップなどの戦略を採用しています。

- 2024年6月- ロックウェルオートメーションは、より安全でスマートな産業用AIモバイルロボットの開発を促進するため、エヌビディアとの提携を発表しました。この提携により、自律移動ロボット(AMR)におけるAIの利用が促進され、その性能と効率が向上すると予想されます。

- 2024年2月- シュナイダーエレクトリックは、技術大手のインテルおよびレッドハットと提携し、新しいソフトウェアフレームワークである分散制御ノード(DCN)を発表しました。シュナイダーエレクトリックのEcoStruxure Automation Expertをベースに構築されたこの革新的なフレームワークは、産業企業がソフトウェア定義のプラグアンドプレイモデルに移行することを支援します。この移行により、業務効率と品質が向上し、プロセスが合理化されるため、最終的にコスト削減につながります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 技術動向/進歩

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 業界バリューチェーン分析

- 市場のマクロ動向分析

第5章 市場力学

- 市場促進要因

- 新興経済諸国における産業活動の成長

- エネルギー効率とコスト削減への関心の高まり

- 市場の抑制要因

- 据付・再築コストの高さ

第6章 市場セグメンテーション

- ソリューション別

- 産業用制御システム

- 分散型制御システム(DCS)

- 監視制御・データ収集(SCADA)

- プログラマブル・ロジック・コントローラー(PLC)

- ヒューマン・マシン・インターフェース(HMI)

- その他の制御システム

- フィールド機器

- センサーとトランスミッター

- バルブとアクチュエーター

- モーターとドライブ

- ロボット

- その他のフィールド機器

- ソフトウェア

- 製品ライフサイクル管理(PLM)

- エンタープライズ・リソース・プランニング(ERP)

- 製造実行システム(MES)

- その他ソフトウェア

- 産業用制御システム

- エンドユーザー産業別

- 石油・ガス

- 製薬

- 自動車・運輸

- 飲食品

- 電力・公益事業

- 化学・石油化学

- その他エンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Limited

- Mitsubishi Electric Corporation

- Siemens AG

- Omron Corporation

- Yokogawa Electric Corporation

- Yaskawa Electric Corporation

- Kuka Aktiengesellschaft

- Fanuc Corporation

- Regal Rexnord Corporation

- Nidec Corporation

- Basler AG

第8章 投資分析

第9章 市場の将来

The Industrial Automation Market size is estimated at USD 203.05 billion in 2024, and is expected to reach USD 309.16 billion by 2029, growing at a CAGR of 8.77% during the forecast period (2024-2029).

Key Highlights

- Industrial automation may potentially and considerably increase export competitiveness in developing nations. By automating their manufacturing processes, these nations can create items more quickly, effectively, and affordably, which boosts their ability to compete in the global market. This may result in higher levels of exports, better foreign currency revenues, and an improvement in the emerging economy, hence driving the market for industrial automation in developing countries.

- Industrial automation significantly impacts small and medium-sized firms (SMEs) in developing nations. Automation may boost these companies' competitiveness and achieve sustained growth. It enables SMEs to improve productivity, streamline operations, and satisfy the needs of larger customers and supply chains. For instance, Industrial automation optimizes resources and reduces production times, freeing personnel for strategic tasks. According to the International Federation of Robotics (IFR), productivity increases by up to 30% in manufacturing with automation in multiple processes.

- According to the International Monetary Fund (IMF), growth rates for emerging markets and developing economies are projected to be 4.2% in 2024 and 2025 compared to 4.3% in 2023. In many developing countries such as India, several initiatives by the Government of India, like the scrappage policy, Automotive Mission Plan 2026, and production-linked incentive scheme in the Indian market, are expected to make India a significant player in the two-wheeler and four-wheeler market. Such policies include adopting automation technologies and fostering a favorable environment for the market studied.

- Automation equipment mandates high capital investment to fund smart manufacturing (an automated system may cost millions of dollars to install, design, and fabricate). The cost of purchasing the equipment, including robotic systems, conveyor belts, sensors, and control systems, can be substantial. The factory automation equipment also necessitates the customization and integration into existing production systems. This process involves designing, engineering, and programming the equipment to meet specific manufacturing requirements. This poses a significant hindrance to the growth of the market studied.

- Apart from the direct impact evident in the supply chains and production of industrial automation solutions, the aftereffects of the pandemic are also impacting the growth of the studied market. For instance, the ongoing threat of recession looming over various regions, including North America, may negatively influence the studied market's growth as the economic uncertainty will prevent consumers and businesses from spending more on high-value products such as automobiles and expansion projects, which may impact the growth of the market studied.

Industrial Automation Market Trends

Oil and Gas Industry to Witness Significant Growth

- The oil and gas industry has been a dominating segment in adopting industrial automation solutions. However, the growth prospects for industrial automation in this industry are limited compared to other developing industries, and therefore, the growth rate is expected to slow in this industry.

- Oil and gas automation, also known as oilfield automation, is a set of processes, many leveraging digital technologies, aimed at enhancing the competitiveness of energy producers in global markets. While certain sectors within the industry are more primed for automation, key areas include drilling, production operations, logistics, safety, and retail operations. Oil and gas automation predominantly relies on IoT-based sensors, predictive systems, and AI-driven expert systems to boost productivity and bridge skill gaps arising from labor shortages.

- The oil and gas industry's hazardous environments are increasingly being navigated through automation. Robots and automated systems handle tasks like drilling, inspection, and maintenance, significantly reducing human exposure to risks.

- The industry is bolstering safety with automated features like emergency shutdown systems, guaranteeing swift responses to difficult situations. By deploying sensors and automated tools, companies are ensuring compliance with regulations and curbing their environmental footprint.

- The oil and gas industry is a vital component of the global economy. As per IEA, global production of liquid fuels will increase by more than 0.8 million b/d in 2024, slowing from the 1.8 million b/d increase in 2023, as OPEC+ voluntary production cuts are offset by supply growth outside of OPEC+. Although OPEC+ crude oil production in 2024 decreases by 0.9 million b/d compared with last year, forecast production outside of OPEC+ increased by 1.8 million b/d, led by the United States, Guyana, Brazil, and Canada. With significant surge in oil production and surging digitization, oil and gas companies have increasingly relied on digital technology and automation.

Asia-Pacific is Expected to Register the Fastest Growth

- Asia-Pacific is home to some of the world's largest manufacturing economies, including China, Japan, South Korea, and Taiwan. The ongoing expansion of manufacturing industries in automotive, electronics, aerospace, and medical devices creates a significant demand for industrial automation.

- Initiatives by emerging countries like India to expand their manufacturing footprint and become self-reliant further propel the market growth. Manufacturing emerged as one of the high-growth sectors in India. The 'Make in India' program places India on the global map as a manufacturing hub and globally recognizes the Indian economy. According to IBEF, India can export goods worth USD 1 trillion by 2030 and is on the road to becoming a significant global manufacturing hub.

- The government of India aims for a USD 5 trillion economy by 2025, of which manufacturing would be worth USD 1 trillion. The convergence of flagship programs, such as Make in India with Skill India and Digital India, would be vital to achieving this goal, thereby driving the region's market growth.

- The ongoing initiatives to build a battery manufacturing plant for faster adoption of electric vehicles are further driving the market growth. For instance, in August 2023, Recharge Industries announced its plans to build a factory with an annual capacity of 30 gigawatt-hours to supply batteries for roughly 300,000 EVs. Construction is expected to begin around May 2024, with production slated to start in 2025.

- The region is the biggest semiconductor and electronics product manufacturer due to the presence of companies like Taiwan Semiconductor Manufacturing Company. Taiwan produces over 60% of the world's semiconductors and over 90% of the most advanced ones. Most of the semiconductors are manufactured by TSMC.

Industrial Automation Industry Overview

The industrial automation market is highly fragmented due to the presence of small and medium-sized enterprises and global players. Some of the major players in the market are Schneider Electric SE, Rockwell Automation Inc., Honeywell International Inc., Emerson Electric Co., and ABB Limited. Key players in the market are adopting strategies such as acquisitions and partnerships to enhance their product offerings and gain sustainable competitive advantage.

- June 2024 - Rockwell Automation announced a partnership with NVIDIA to expedite the development of safer and smarter industrial AI mobile robots. The collaboration is anticipated to drive the use of AI in autonomous mobile robots (AMRs), improving their performance and efficiency.

- February 2024 - Schneider Electric, in partnership with tech giants Intel and Red Hat, unveiled a new software framework, the Distributed Control Node (DCN). Building upon Schneider Electric's EcoStruxure Automation Expert, this innovative framework empowers industrial firms to transition to a software-defined, plug-and-play model. This shift boosts operational efficiency and quality and streamlines processes, ultimately leading to cost savings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends/Advancements

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Industry Value Chain Analysis

- 4.5 Analysis of the Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Industrial Activities in Developing Economies

- 5.1.2 Growing Emphasis on Energy Efficiency and Cost Reduction

- 5.2 Market Restrains

- 5.2.1 High Cost of Installation and Re-building

6 MARKET SEGMENTATION

- 6.1 By Solution

- 6.1.1 Industrial Control Systems

- 6.1.1.1 Distributed Control System (DCS)

- 6.1.1.2 Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.3 Programmable Logic Controller (PLC)

- 6.1.1.4 Human-machine Interface (HMI)

- 6.1.1.5 Other Control Systems

- 6.1.2 Field Devices

- 6.1.2.1 Sensors and Transmitters

- 6.1.2.2 Valves and Actuators

- 6.1.2.3 Motors and Drives

- 6.1.2.4 Robotics

- 6.1.2.5 Other Field Devices

- 6.1.3 Software

- 6.1.3.1 Product Lifecycle Management (PLM)

- 6.1.3.2 Enterprise Resource and Planning (ERP)

- 6.1.3.3 Manufacturing Execution System (MES)

- 6.1.3.4 Other Software

- 6.1.1 Industrial Control Systems

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Pharmaceuticals

- 6.2.3 Automotive and Transportation

- 6.2.4 Food and Beverage

- 6.2.5 Power and Utilities

- 6.2.6 Chemical and Petrochemical

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Rockwell Automation Inc.

- 7.1.3 Honeywell International Inc.

- 7.1.4 Emerson Electric Co.

- 7.1.5 ABB Limited

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Siemens AG

- 7.1.8 Omron Corporation

- 7.1.9 Yokogawa Electric Corporation

- 7.1.10 Yaskawa Electric Corporation

- 7.1.11 Kuka Aktiengesellschaft

- 7.1.12 Fanuc Corporation

- 7.1.13 Regal Rexnord Corporation

- 7.1.14 Nidec Corporation

- 7.1.15 Basler AG