|

市場調査レポート

商品コード

1549829

アフリカのデータセンター冷却:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Africa Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのデータセンター冷却:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

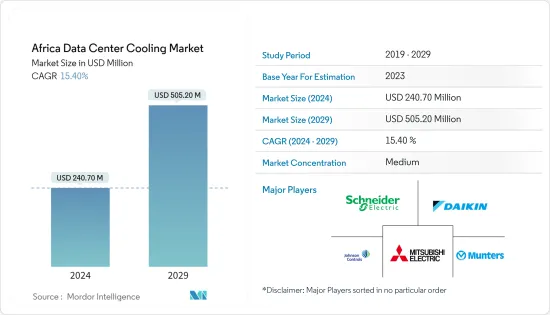

アフリカのデータセンター冷却市場規模は、2024年に2億4,070万米ドルと推定され、2029年には5億520万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは15.40%で成長する見込みです。

中小企業におけるクラウドコンピューティング需要の増加、地域のデータセキュリティに関する政府規制、国内企業による投資の拡大などが、アフリカにおけるデータセンター需要を促進する主要要因となっています。

建設中のIT負荷容量:アフリカのデータセンター建設市場における今後のIT負荷容量は、2029年までに1,226MWに達すると予想されます。

建設中の高床スペース:同地域の床面積は2029年までに520万平方フィート増加すると予想されます。

計画中のラック:当地域で設置が予定されているラックの総数は、2029年までに26万個に達すると予想されます。2029年までに最大数のラックが設置されるのは南アフリカです。

アフリカの平均気温は、夏は15℃~36℃、冬は-2℃~26℃です。アフリカは天水農業に大きく依存しているため、気候の変動や変化に非常に脆弱です。冷却技術の選択は通常、データセンターの地理的位置に基づいて行われます。

計画中の海底ケーブルアフリカを結ぶ海底ケーブルは70近くあり、その多くが建設中です。2024年にサービス開始が予定されている海底ケーブルのひとつがAfrica-1で、エジプトのポートサイドとラス・ガレブに陸揚げされ、1万キロメートル以上に及びます。

アフリカのデータセンター冷却市場動向

情報技術産業が高成長を遂げる

- アフリカは潜在的なデータセンター市場として浮上しています。Liquid Telecomの子会社であるAfrica Data Centersは、ケニアのナイロビにある同社施設に160ラックを収容するフロアを増設しました。新たに開設されたフロアは、アフリカにおけるコロケーションとホスティングサービスに対する莫大な需要に直接応えるものです。これにより、同地域でのデータセンター冷却設備のさらなる設置が可能になります。

- 南アフリカ、ナイジェリア、エジプトでは、それぞれ約8,900万台、1億6,300万台、7,560万台のスマートフォン接続があります。ナイジェリアでは約60%、南アフリカでは約21%のユーザーがM-Pesaなどのデジタルウォレットを利用しています。Netflix、Disney+、Amazon Primeはこの地域の主要なOTT参入企業で、Netflixは2022年のアフリカ市場の加入者ベースで約640万人をリードしています。これらのサービスは、ナイジェリア、南アフリカ、ボツワナ、ケニア、モーリシャス、マダガスカル、セイシェル、タンザニア、トーゴ、ジンバブエ、ザンビアなどの特定の国で利用できます。こうした動きとともに、データを処理するデータセンターの増加により、同地域では冷却装置の需要が高まっている

- アフリカ43カ国で5Gサービスが展開され、帯域幅の高速化がデータ消費の増加につながります。こうした動きに伴い、データを処理するデータセンターの数が増加しているため、同地域では冷却装置の需要が高まっている

- アフリカの人々は、ブロードバンドよりもモバイルサービスを好む傾向があります。例えば、ブロードバンドを利用する人の割合は、2016年の19%から2020年には29%に増加し、2029年には51%に達する可能性があります。4Gから5Gへの移行と、より多くの光ファイバーケーブルの採用より、同地域ではティア3とティア4データセンターの需要が増加する可能性が高いです。これらのデータセンターは、大陸全域で自動化と開発を実施するために必要な多様なデジタルサービスとIoT環境に対応する必要がある可能性があります。こうした市場開拓により、同地域の市場需要は拡大すると考えられます。

- データのローカライゼーションの必要性は、クラウドアグリゲーターがこの地域にクラウドデータセンターを設置する原動力となっています。このことは、クラウドなどのセグメントの成長を促進し、地域投資の需要と魅力の高まりを裏付けています。これはまた、同地域における冷凍機器の使用増加に対応するものです。

南アフリカが最大の市場シェアを占める

- 南アフリカ市場では、さまざまなエンドユーザー産業のデータ消費が徐々に増加しています。特にeコマースや小売業におけるeコマースの導入増加は、同国におけるコロケーションサービスの需要拡大を支える主要要因の1つであり、ファッション、スポーツ、健康、美容製品がこれに続きます。これは、データセンターの冷却装置の増加に相当します。

- 経済特区(SEZ)や自由貿易区(FTZ)の設立、スマートシティへの投資が南アフリカのデータセンター建設産業を後押ししています。データセンター数の増加に伴い、同国では冷却装置の使用が増加しています。

- クラウドの利用、データのローカライズ、5GやIoTなどの新技術が増加しています。先進的なITインフラの導入が進み、オンプレミスからコロケーションやマネージドサービスへの移行が進んでいることから、今後数年間、国内でのデータセンター施設開発に向けた投資家の動きが活発化すると予想されます。データセンターの増加は、国内の冷却設備使用量の増加に対応しています。

- 南アフリカ市場ではスマートフォンの普及が進んでおり、データセンターの容量はデータの増加に対応できるよう拡大する必要があります。スマートフォンは、リアルタイムの処理と分析を必要とする大量のデータを生成します。データセンターは膨大な量のデータを処理しなければならないです。そのため、スマートフォンの利用者が増えれば増えるほど、南アフリカのデータセンターではラック/サーバーを増設する必要性が高まると考えられます。これはデータセンター数の増加に対応したもので、同国における冷却装置の需要増を意味します。

アフリカのデータセンター冷却産業概要

アフリカのデータセンター冷却市場は競争が激しく、多くの大手企業が参入しています。Schneider Electric SE、Daikin Industries Ltd、Johnson Controls International PLC、Mitsubishi Electric Corporation、Munters Group ABなどの大手企業が既存市場で存在感を示し、市場への浸透が進んでいます。技術革新への注目の高まりに伴い、液体ベースの冷却技術やポータブル冷却技術などの新技術への需要も伸びており、それがこの地域でのさらなる開発のための投資を後押ししています。

2024年5月、Rittalは複数のハイパースケールデータセンター事業者と共同でモジュール型冷却システムを開発しました。このソリューションは、直接水冷により1MWを超える冷却能力を誇ります。AI用途の高電力密度に対応するよう特別に調整されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 欧州における高性能コンピューティングの動向の高まり

- 増大するラックの電力密度

- 市場抑制要因

- 高額な初期投資

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 冷却技術

- 空冷

- CRAH

- チラーとエコノマイザー

- 冷却塔

- その他の空気式冷却

- 液体冷却

- 液浸冷却

- チップ間直接冷却

- 空冷

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他

- 国名

- 南アフリカ

- ナイジェリア

第6章 競合情勢

- 企業プロファイル

- Stulz GmbH

- Rittal GMBH & Co.KG

- Schneider Electric SE

- Vertiv Group Corp.

- Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- Asetek A/S

- Johnson Controls International PLC

- Fujitsu General Limited

- Airedale International Air Conditioning

- Emerson Electric Co.

第7章 投資分析

第8章 市場機会と今後の動向

The Africa Data Center Cooling Market size is estimated at USD 240.70 million in 2024, and is expected to reach USD 505.20 million by 2029, growing at a CAGR of 15.40% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in Africa.

Under Construction IT Load Capacity: The upcoming IT load capacity of the African data center construction market is expected to reach 1,226 MW by 2029.

Under Construction Raised Floor Space: The region's construction of raised floor area is expected to increase 5.2 million sq. ft by 2029.

Planned Racks: The region's total number of racks to be installed is expected to reach 260K units by 2029. South Africa is expected to house the maximum number of racks by 2029.

Average temperatures in Africa range from 15°C to 36°C in summer and -2°C to 26°C in winter. Africa's heavy reliance on rain-fed agriculture makes it highly vulnerable to climate variability and change. The choice of cooling technology is typically based on the geographic location of the data center.

Planned Submarine Cables: Close to 70 submarine cable systems connect Africa; many are under construction. One submarine cable expected to begin service in 2024 is Africa-1, spanning over 10,000 kilometers with a landing point in Port Said, Egypt, and Ras Ghareb, Egypt.

Africa Data Center Cooling Market Trends

Information Technology Industry to Witness Highest Growth

- Africa is emerging as a potential data center market. Africa Data Centers, a subsidiary of Liquid Telecom, has installed an additional floor to accommodate 160 racks at its facility in Nairobi, Kenya. The newly opened floor directly responds to the enormous demand for colocation and hosting services in Africa. This will enable further data center cooling equipment installations in the region.

- South Africa, Nigeria, and Egypt have approximately 89 million, 163 million, and 75.6 million smartphone connections in the region, respectively. Around 60% of users in Nigeria and 21% in South Africa use digital wallets such as M-Pesa to process transactions. Netflix, Disney+, and Amazon Prime are major OTT players in the region, with Netflix leading the African market subscriber base of around 6.4 million in 2022. These services are available in selected countries such as Nigeria, South Africa, Botswana, Kenya, Mauritius, Madagascar, Seychelles, Tanzania, Togo, Zimbabwe, and Zambia. Along with these developments, the growing number of data centers processing data has increased the demand for cooling equipment in the region.

- 5G service rolls out in 43 African countries, and improving bandwidth speeds will lead to higher data consumption. Along with these developments, the growing number of data centers processing data has increased the demand for cooling equipment in the region.

- Africans tend to prefer mobile services over broadband. For example, the percentage of people using broadband could increase from 19% in 2016 to 29% in 2020 and reach 51% by 2029. The transition from 4G to 5G and the introduction of more fiber optic cables will likely increase the demand for Tier 3 and Tier 4 data centers in the region. These data centers may need to accommodate the diverse digital services and IoT environments required to implement automation and development across the continent. These developments will increase the market demand in this region.

- The need for data localization is driving cloud aggregators to set up cloud data centers in the region. This confirms the growing demand and attractiveness of regional investment, driving the growth of sectors such as cloud. This will also accommodate the increased use of refrigeration equipment in the region.

South Africa Accounts for the Largest Market Share

- The data consumption of various end-user industries in the South African market is gradually increasing. Increasing adoption of e-commerce, especially in e-commerce and retail, is one of the main drivers underpinning the growing demand for colocation services in the country, followed by fashion, sports, health, and beauty products. This equates to an increase in data center cooling equipment.

- The establishment of special economic zones (SEZs), free trade zones (FTZs), and investments in smart cities are boosting the South African data center construction industry. With the increase in the number of data centers, the use of cooling equipment is increasing in the country.

- Cloud usage, data localization, and new technologies such as 5G and IoT are rising. The increasing adoption of advanced IT infrastructure and the shift from on-premises to colocation and managed services are expected to drive investors to develop data center facilities in the country in the coming years. The increase in data centers corresponds to the increase in domestic cooling equipment usage.

- With the South African market favoring smartphones, data center capacity must expand to keep up with the growing data. Smartphones generate large amounts of data that require real-time processing and analysis. Data centers have to deal with huge amounts of data. Therefore, as smartphone users grow, the need for additional racks/servers in South African data centers will likely increase. This is in response to an increase in the number of data centers, which means increased demand for cooling equipment in the country.

Africa Data Center Cooling Industry Overview

The African data center cooling market is highly competitive and consists of many significant players, some of which currently dominate. Market penetration is growing with a strong presence of major players, such as Schneider Electric SE, Daikin Industries Ltd, Johnson Controls International PLC, Mitsubishi Electric Corporation, and Munters Group AB in established markets. With the increasing focus on innovation, the demand for new technologies, such as liquid-based cooling and portable cooling technologies, is also growing, which, in turn, is driving investments for further developments in the region.

In May 2024, Rittal developed a modular cooling system in collaboration with multiple hyperscale data center operators. This solution boasts a cooling capacity exceeding 1 MW, achieved through direct water cooling. It's specifically tailored to cater to the high-power densities of AI applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Trend of High-Performance Computing across Europe

- 4.2.2 Growing Rack Power Density

- 4.3 Market Restraints

- 4.3.1 High Initial Investments

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Cooling Technology

- 5.1.1 Air-based Cooling

- 5.1.1.1 CRAH

- 5.1.1.2 Chiller and Economizer

- 5.1.1.3 Cooling Tower

- 5.1.1.4 Other Air-based Cooling

- 5.1.2 Liquid-based Cooling

- 5.1.2.1 Immersion Cooling

- 5.1.2.2 Direct-to-chip Cooling

- 5.1.1 Air-based Cooling

- 5.2 End User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End Users

- 5.3 Country

- 5.3.1 South Africa

- 5.3.2 Nigeria

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Stulz GmbH

- 6.1.2 Rittal GMBH & Co.KG

- 6.1.3 Schneider Electric SE

- 6.1.4 Vertiv Group Corp.

- 6.1.5 Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- 6.1.6 Asetek A/S

- 6.1.7 Johnson Controls International PLC

- 6.1.8 Fujitsu General Limited

- 6.1.9 Airedale International Air Conditioning

- 6.1.10 Emerson Electric Co.