|

市場調査レポート

商品コード

1692510

北米の空調機器:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Air Conditioning Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の空調機器:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

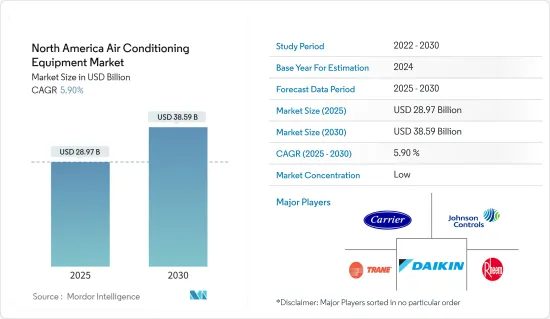

北米の空調機器市場規模は2025年に289億7,000万米ドルと推定・予測され、2030年には385億9,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは5.9%です。

エアコンは、熱を取り出し外部に伝えることで空間を冷却するシステムです。この冷却された空気は、換気によって建物全体に分配されます。HVACシステムの重要な一部として、エアコンは家庭の温度を調節し、快適性と居住性を高める。

主なハイライト

- 米国の不動産市場は、住宅、商業、工業の各分野で建設支出が増加し、建築許可件数が急増したことで、力強い上昇を目の当たりにしています。特筆すべきは、米国の建設セクターが、連邦政府による多額のインフラ投資に後押しされて、さらに拡大する態勢を整えていることです。この勢いは公的な取り組みにとどまらず、民間の商業建設事業も牽引力を増しています。

- これらの相互接続されたスマートAC機器には、数多くの利点があります。スマートACシステムは、ユーザーの好みを学習し、それに応じて冷房スケジュールを調整することで、エネルギー使用を最適化するのに役立ちます。これは快適さを提供するだけでなく、エネルギー消費とコストを削減します。スマートフォンのアプリや音声コマンドでACシステムを遠隔操作できる機能は、消費者の標準的な期待になりつつあります。先進的なスマートACシステムは、自身の性能を監視し、大きな問題になる前に潜在的な問題をユーザーに警告することができます。これにより、ユニットの寿命を延ばし、効率的に作動させることができます。

- 1970年代のオイルショック以降、家庭におけるエネルギー効率向上の取り組みは大きな変動を経験し、エネルギー消費削減に対する経済的インセンティブが高まりました。現在、エネルギー効率は住宅改修の主要な推進力であり、北米全域の様々な政策によって支えられています。これらの政策には、エネルギー監査、エネルギー性能証明書、および補助金、助成金、税額控除、低金利ローン、第三者融資などの金銭的インセンティブが含まれます。

- 北米のHVAC業界は、厳格な安全規制と基準に従うことを求められています。ガス検知・監視システムの活用は、コンプライアンスと安全ガイドラインへの従順さを示すものです。これらのシステムを取り入れることで、HVAC企業は規制基準を満たし、安全な職場を作り、罰則や法的結果に直面する可能性を減らすことができます。

- IoT対応のスマート空調機器は、スマートフォンやデスクトップで空調を操作・管理できるため、消費者の間で人気を集めました。2024年4月、著名な世界IoTコネクティビティ・プロバイダーであるソラコム株式会社は、三菱電機欧州BVとの協業を発表しました。この提携は、ソラコムのセルラー接続を三菱電機のクラウドベースの遠隔管理システムであるMELCloudに統合することを目的としています。MELCloudは特に三菱電機の空調、暖房、熱回収/換気製品に対応し、遠隔制御と管理機能の新時代を切り開きます。

北米の空調機器市場動向

住宅部門が市場を独占する

- 同地域の住宅用空調機器の需要は、夏季の暑さを和らげ、快適さを提供するために極めて重要であることから増加しています。住宅環境で一般的に使用される空調システムの種類は、気候、建物の設計、エネルギーの利用可能性、文化的嗜好などの要因によって異なります。

- エネルギー情報局(EIA)によると、セントラル・エアコンは、北米の人々が自宅を冷やす主な方法として広く採用しています。EIAは、この地域の家庭がセントラル空調システムを選ぶ傾向が強まっていると報告しています。もうひとつの人気オプションは、ダクトレス・ミニスプリット・システムです。ダクトレス・ミニスプリット・システムはゾーン冷房が可能で、住宅所有者は家のさまざまなエリアの温度を個別にコントロールできます。

- 気候変動に起因する地域の気温上昇により、多くの州で空調システムの必要性が贅沢品から必需品へと高まっています。その結果、この地域では、自宅にエアコンを装備することを選択する個人が増えています。地球の気温が上昇の一途をたどっているため、この採用動向はさらにエスカレートするものと思われます。気候力学の変化を考えると、住宅用エアコン市場は予測期間中に大きく成長するものと思われます。

- また、米国国勢調査局によると、2024年4月の住宅ビルと住宅の建設は、2023年4月に比べて8%増加しました。2024年4月の住宅建設支出は推定年間9,022億9,000万米ドルに達しました。このような要因が市場の成長を促進すると予想されます。さらに、この地域全体で住宅建設が増加していることから、今後数年間で新たな市場機会が創出されると予想されます。

著しい成長を遂げるカナダ

- 同国では、高級住宅インフラプロジェクトの増加により、空調需要が急増しています。市場関係者は、都市化の進展や一人当たり所得の増加などの要因により、予測期間中に数多くのビジネスチャンスが得られると期待しています。カナダではセントラル・エアコン・システムが非常に好まれており、中・大家族住宅や複数階建ての住宅に最適です。

- CREAによると、2023年の住宅販売件数は443,511件で、2025年にはほぼ525,500件に達すると予想されています。変わりやすい気候と厳しい冬のため、カナダの大半の家庭ではエアコンが不可欠となっています。カナダの多くの地域では、気温の上昇と湿度の高さを特徴とする異常な暑さや熱波が発生しています。BC州検視局が公表した初期データによると、ブリティッシュコロンビア州では夏の猛暑が長引き、合計619人が猛暑のために命を落としました。

- こうした事態を避けるため、政府は空調設備の無料提供に力を入れています。例えば2024年5月、BC州政府は2,000万カナダドル(1,453万米ドル)を追加し、経済的支援が必要な人や暑さに弱い人に数千台のエアコンを無料で提供すると発表しました。

- BC Hydroが管理するこのプログラムでは、この時点までに6,000台のエアコンが無料で配布されており、追加資金により合計約2万8,000台のエアコンが配布される見込みです。

北米の空調機器産業の概要

北米の空調機器市場は、多くのバルブ市場企業によって断片化されています。空調機器業界は最大市場の1つであるため、市場シェアを損なうことなく、このような多数の大手ベンダーが存在することは持続可能であり、企業としては、Daikin Industries Ltd、Carrier Corporation、Rheem Manufacturing Company、Tran Inc.(Trane Technologies PLC)、Johnson Controls International PLCなどが挙げられます。

- 2024年3月Carrier Corporationは、データセンター向けの高性能チラーの先進的で革新的な製品ラインを発表しました。これらのチラーは、エネルギー消費と二酸化炭素排出量を削減し、データセンター事業者の運用コストを削減するよう設計されています。486.4 kWから1,464 kWまでのこれらのユニットは、信頼性の高いキャリアのスクリューコンプレッサーを活用しており、効率性と長寿命が保証されています。

- 2024年2月ダイキン工業は、重要な要素に重点を置いてエアコンを強化。地球温暖化係数の低いR32冷媒であるHFC-32を採用し、環境性と省エネ性を重視。さらに、エアコンの基本性能も強化しました。重要な動きとして、ダイキンはビル用マルチエアコン「VRV 7」シリーズを2024年11月に発売します。このシリーズは業界トップのエネルギー効率を誇り、環境フットプリントと運用負荷の軽減に極めて重要です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の後遺症とその他のマクロ経済要因が市場に与える影響

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 既存機器の性能向上と空調機器減税の復活

- ホームオートメーションとビルオートメーションシステムの採用拡大

- 市場抑制要因

- 厳しい規制遵守と安全基準

第6章 市場セグメンテーション

- タイプ別

- ユニットエアコン

- ダクト付きスプリット

- ダクトレス・ミニスプリット

- 室内パッケージ型およびルーフトップ型

- ルームエアコン

- パッケージ・ターミナル・エアコン

- チラー

- 可変冷媒フロー(VRF)

- ユニットエアコン

- エンドユーザー別

- 住宅用

- 商業用および産業用

- 国別

- 米国

- カナダ

- 効率別

- 低効率(13 SEER)

- 高効率(>13 SEER)

第7章 競合情勢

- 企業プロファイル

- Daikin Industries Ltd

- Carrier Corporation

- Rheem Manufacturing Company

- Trane Inc.(Trane Technologies PLC)

- Johnson Controls International PLC

- Mitsubishi Electric Corporation

- Lennox International Inc.

- Systemair AB

- Robert Bosch GmbH

- Electrolux AB

- LG Electronics Inc.

- Midea Group

- Schneider Electric SE

- GE Appliances

- Whirlpool Corporation

第8章 冷房機器流通チャネル分析セントラル空調、ルーム空調

- 直接販売

- 小売業者

- 卸売業者/販売業者/請負業者

第9章 投資分析

第10章 市場の将来

The North America Air Conditioning Equipment Market size is estimated at USD 28.97 billion in 2025, and is expected to reach USD 38.59 billion by 2030, at a CAGR of 5.9% during the forecast period (2025-2030).

An air conditioner is a system that cools a space by extracting heat and transferring it outside. This cooled air is then distributed throughout a building via ventilation. As an essential part of the HVAC system, air conditioners regulate home temperatures to enhance comfort and livability.

Key Highlights

- The US real estate market is witnessing a robust upswing, buoyed by escalating construction outlays and a surge in building permits across residential, commercial, and industrial segments. Notably, the US construction sector is poised for further expansion, fueled by substantial federal investments in infrastructure. This momentum extends beyond public initiatives, with private commercial construction endeavors also gaining traction.

- These interconnected and smart AC equipment offer numerous benefits. Smart AC systems help optimize energy usage by learning user preferences and adjusting cooling schedules accordingly. This not only provides comfort but also reduces energy consumption and costs. The ability to control AC systems remotely via smartphone apps or voice commands is becoming a standard consumer expectation. Advanced smart AC systems can monitor their own performance and alert users to potential issues before they become major problems. This can extend the life of the unit and ensure it operates efficiently.

- Efforts to promote energy efficiency in homes have experienced significant fluctuations since the oil shocks of the 1970s, which increased the financial incentives for reducing energy consumption. Currently, energy efficiency is a primary driver for home renovations, supported by various policies across North America. These policies include energy audits, energy performance certificates, and financial incentives like grants, subsidies, tax credits, low-interest loans, and third-party financing.

- The North American HVAC industry is required to follow strict safety regulations and standards. Utilizing gas detection and monitoring systems shows dedication to compliance and following safety guidelines. By incorporating these systems, HVAC companies can meet regulatory standards, create a safe workplace, and reduce the likelihood of facing penalties or legal consequences.

- IoT-enabled smart air conditioning equipment gained traction among consumers as these systems enable users to operate and manage ACs using smartphones and desktops. In April 2024, Soracom Inc., a prominent global IoT connectivity provider, announced its collaboration with Mitsubishi Electric Europe BV. The partnership aims to integrate Soracom's cellular connectivity into MELCloud, Mitsubishi Electric's cloud-based remote management system. MELCloud specifically caters to Mitsubishi Electric's air conditioning, heating, and heat recovery/ventilation products, ushering in a new era of remote control and management capabilities.

North America Air Conditioning Equipment Market Trends

Residential Sector to Dominate the Market

- The demand for residential air conditioning units in the region is increasing as they are crucial for providing comfort and relief from hot temperatures during the summer months. The types of air conditioning systems commonly used in residential settings vary depending on factors such as climate, building design, energy availability, and cultural preferences.

- According to the Energy Information Administration (EIA), central air conditioning is widely adopted by North Americans as the primary method of cooling their homes. The EIA reports a growing trend of households in the region opting for central air conditioning systems, which are significantly more favored than window or wall units. Another popular option is ductless mini-split systems. They provide zoned cooling, allowing homeowners to control the temperatures of different areas of the house independently.

- The rising temperatures in the region, attributed to climate change, have elevated the need for air conditioning systems from a luxury to a necessity in many states. Consequently, a growing number of individuals in the region are choosing to equip their homes with air conditioning. This adoption trend is poised to escalate further as the planet's temperature continues its upward trajectory. Given the shifting climate dynamics, the residential air conditioning market is set for significant growth over the forecast period.

- In addition, according to the US Census Bureau, construction of residential buildings and homes increased by 8% in April 2024 compared to April 2023. In April 2024, construction spending in residential reached an estimated annual rate of USD 902.29 billion. Such factors are anticipated to drive the market's growth. Furthermore, the growing residential construction across the region is expected to create new market opportunities in the coming years.

Canada to Witness Significant Growth

- The country is experiencing a surge in air conditioning demand due to the rise in luxury residential infrastructure projects. Market players can expect numerous opportunities over the forecast period, thanks to factors such as increased urbanization and higher per capita income. Central air conditioning systems are highly favored in Canada and are ideal for mid-to-large family homes, as well as for homes with multiple stories.

- According to CREA, the number of home sales in 2023 was recorded at 443,511, and it is expected to reach almost 525,500 by 2025. Due to the variable climate and severe winters, air conditioner equipment has become essential in the majority of Canadian households. Numerous regions in Canada experience extreme heat events or heat waves characterized by soaring temperatures and high levels of humidity. According to the initial data disclosed by the BC Coroners Service, a total of 619 individuals lost their lives due to the intense heat during the prolonged summer heat wave in British Columbia.

- To avoid such circumstances, the government is focusing on providing free air conditioning equipment. For instance, in May 2024, the BC government announced an additional CAD 20 million (USD 14.53 million) to provide thousands of free air conditioning units to those who need financial assistance and people vulnerable to heat.

- The program managed by BC Hydro has distributed 6,000 complimentary AC units up to this point, with additional funding anticipated to result in a total of approximately 28,000 AC units being distributed.

North America Air Conditioning Equipment Industry Overview

The North American air conditioning equipment market is fragmented due to many valve market players. Since the AC equipment industry is one of the largest markets, the existence of such a sheer number of major vendors without compromising their market shares is sustainable, and some of the players include Daikin Industries Ltd, Carrier Corporation, Rheem Manufacturing Company, Trane Inc. (Trane Technologies PLC), and Johnson Controls International PLC.

- March 2024: Carrier Corporation introduced an advanced, innovative line of high-performance chillers for data centers. These chillers are engineered to slash energy consumption and carbon footprints and lower operational expenses for data center operators. Ranging from 486.4 kW to 1,464 kW, these units leverage Carrier's trusted screw compressors, guaranteeing efficiency and longevity in operation.

- February 2024: Daikin Industries Ltd enhanced its air conditioners by focusing on critical elements. This includes shifting to HFC-32, an R32 refrigerant with low global warming potential, emphasizing its eco-friendliness and energy efficiency. Additionally, Daikin has bolstered the fundamental performance of its air conditioning units. In a significant move, Daikin is set to launch the VRV 7 multi-air conditioner series for buildings in November 2024. This series boasts the industry's top energy efficiency and is pivotal in lessening environmental footprints and operational burdens.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Replace Existing Equipment With Better Performance Equipment and Reinstate Tax Credits for Air Conditioning Equipment

- 5.1.2 Growing Adoption of Home and Building Automation Systems

- 5.2 Market Restraint

- 5.2.1 Stringent Regulatory Compliance and Safety Standards

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Unitary Air Conditioners

- 6.1.1.1 Ducted Splits

- 6.1.1.2 Ductless Mini-splits

- 6.1.1.3 Indoor Packaged and Roof Tops

- 6.1.2 Room Air Conditioners

- 6.1.3 Packaged Terminal Air Conditioners

- 6.1.4 Chillers

- 6.1.5 Variable Refrigerant Flow (VRF)

- 6.1.1 Unitary Air Conditioners

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Commercial and Industrial

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

- 6.4 By Efficiency

- 6.4.1 Low Efficiency (13 SEER)

- 6.4.2 High Efficiency (>13 SEER)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daikin Industries Ltd

- 7.1.2 Carrier Corporation

- 7.1.3 Rheem Manufacturing Company

- 7.1.4 Trane Inc. (Trane Technologies PLC)

- 7.1.5 Johnson Controls International PLC

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Lennox International Inc.

- 7.1.8 Systemair AB

- 7.1.9 Robert Bosch GmbH

- 7.1.10 Electrolux AB

- 7.1.11 LG Electronics Inc.

- 7.1.12 Midea Group

- 7.1.13 Schneider Electric SE

- 7.1.14 GE Appliances

- 7.1.15 Whirlpool Corporation

8 ANALYSIS OF COOLING EQUIPMENT DISTRIBUTION CHANNEL CENTRAL AIR CONDITIONING, ROOM AIR CONDITIONING

- 8.1 Direct

- 8.2 Retailers

- 8.3 Wholesalers/Dealers/Contractors