|

市場調査レポート

商品コード

1644892

インドのPOS端末:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India POS Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのPOS端末:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

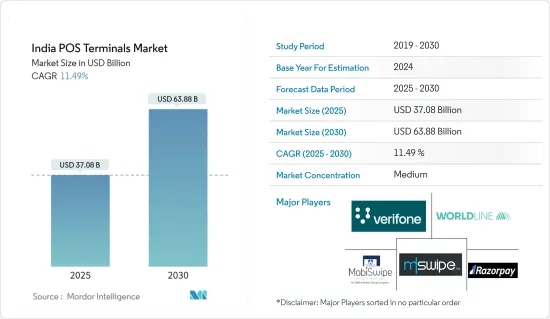

インドのPOS端末の市場規模は2025年に370億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.49%で、2030年には638億8,000万米ドルに達すると予測されています。

モバイルPOS端末の需要急増、モバイルウォレットの普及拡大、支援的規制、eコマースの成長、新規企業の流入、都市化、技術進歩など、いくつかの要因がインドのPOS端末市場を後押ししています。

主なハイライト

- 決済の世界は、消費者の嗜好の変化、技術の進歩、規制のシフトによって劇的な変化を遂げつつあります。デジタル取引の急増に後押しされ、著しい成長を遂げているインドでは、決済環境が再構築されつつあります。

- インドの小売セクターは、小売店舗の急増と消費支出の増加に牽引され、急成長を遂げています。その結果、決済処理機の需要が高まっています。インドの消費者の間で現金よりもデジタル取引への嗜好が高まる中、これらの機械は小売業者にとって不可欠な要素となっています。

- インドでは、POS端末の市場が堅調です。これらの端末はキャッシュレス取引を促進するもので、消費者は携帯電話やカードで支払いを済ませることができます。POS端末のインド市場は、現金よりもデジタル決済の普及が進んでいることから拡大しています。このシフトに伴い、専用のPOS端末に対する企業や店舗からの需要が高まっています。ここ数年、インドではカード決済機の導入が急増しており、企業がデジタル決済に対応できるようになっています。

- インド準備銀行(RBI)は、政府やその他の省庁に加え、デジタル決済の大幅な急増につながる取り組みを熱心に主導してきました。これらの取り組みのいくつかは国際的な評価を得ています。カード決済は、Aadhaar-enabled Payment System(AePS)、Unified Payments Interface(UPI)、Immediate Payment Service(IMPS)、QRベースの決済、National Electronic Toll Collection(NETC)と並んで、現金中心の経済からデジタル取引への依存度が高まる経済への段階的な移行において極めて重要な役割を果たしてきました。

- 2023年10月、フィンテック業界のプレーヤーであるPaytmは、最新のイノベーションであるPaytmカード・サウンドボックスを発表しました。この先進的なデバイスは、UPI取引の音声アラートを提供するだけでなく、Visa、Mastercard、Amex、RuPayなどの主要ネットワークをカバーする「タップ・アンド・ペイ」カード取引を容易にします。パインラボはまた、「Mini」と名付けられた従来のPOS(販売時点情報管理)端末のコスト効率に優れたイテレーションを発表しました。Mini'端末は、UPIトランザクションと幅広いネットワークの「タップ・アンド・ペイ」カード決済を処理する機能を備えています。

- しかし、POS端末の不足が業界の成長を妨げています。同市場は、高額な設置費用やメンテナンス費用、セキュリティ上の懸念、関連費用といった課題に直面しており、これらすべてが市場拡大の妨げとなっています。

インドのPOS端末市場動向

小売セグメントが大きな市場シェアを占める見込み

- インドの小売セクターにおけるいくつかの重要な要因がPOS端末市場の成長を促進しています。組織化された小売チェーンの拡大や独立系店舗の増加が、インドにおける効率的なトランザクション処理システムへの需要を押し上げています。小売業者は顧客体験と業務効率の向上を目指しており、POS端末の導入は不可欠となっています。

- さらに、Digital Indiaなどの政府のイニシアチブは、小売業者をデジタル決済ソリューションへと向かわせています。この勢いは、デーモンエタニゼーションとGST導入の両方によって強化され、企業が正式なデジタル取引を取り入れることに拍車をかけています。

- インド電気通信規制庁によると、2023年12月現在、リライアンス・ジオ・インフォコム(Reliance Jio Infocomm Limited)がインターネット加入者の最も多いサービス・プロバイダーであり、4億7,000万人以上の加入者を誇り、50%を超える圧倒的な市場シェアを誇っています。

- さらに、eコマースとオムニチャネル小売の急増により、オンラインとオフラインの両方の取引をスムーズに管理できる統合POSシステムへの需要が高まっています。小売企業は現在、競争力を維持するため、在庫管理、顧客関係管理(CRM)、データ分析などの機能を重視し、洗練されたPOSソリューションを優先しています。

- 可処分所得の増加に支えられた中間層の拡大が、個人消費の増加に拍車をかけています。この急増は小売売上高の急増に直結しており、合理化された決済システムの必要性が浮き彫りになっています。

- 2024年2月、Zoho Corporationはインドでの最新ベンチャーを発表し、Zakyaブランドを導入しました。Zakyaの主な焦点は、小売店向けにカスタマイズされた最新のPOS(販売時点情報管理)ソリューションを提供することです。これらのソリューションは、日常業務を簡素化し、集中監視機能を提供することを目的としています。特に、クラウド上で動作するZakyaのPOSシステムは、迅速な導入プロセスとユーザーフレンドリーなインターフェイスを誇っています。この機能セットは、中小規模の小売業者がセットアップから1時間以内に迅速に移行、稼動、課金を開始できるように設計されています。

著しい成長が見込まれるモバイルPOS

- カード決済やモバイル決済は、ATMでの引き出しを凌ぐ勢いで普及しています。この変化の背景には、デジタル決済への嗜好の高まりがあります。この変化のきっかけとなったのはCOVID-19の大流行で、現金の取り扱いに対する懸念が高まり、デジタル取引に軸足を移すようになった。この流れは今後も続くとみられ、これは店舗カード決済の導入が増加していることからも明らかです。

- インドでは、スマートフォンによる店舗での買い物に統一決済インターフェイス(UPI)を活用する動きが加速しています。このプロセスをさらに合理化するために、近距離無線通信技術をUPIに統合する動きがあります。この進歩は、取引中の物理的接触を最小限に抑えるだけでなく、加盟店におけるUPIの普及を促します。さらに、UPIの普及がこれまで限定的であった小売業者にとっても、デジタル決済の環境が強化されることになります。

- 2024年4月、インドのフィンテック分野のプレーヤーであるBharatPeは、インドのオールインワン決済ソリューションである「BharatPe One」を発表しました。この革新的な製品は、POS、QR、スピーカーの機能を1つのデバイスに統合したものです。この革新的な製品は、加盟店の取引を簡素化することを目的としています。動的・静的QRコード、タップ・アンド・ペイ、従来のカード決済など、さまざまな決済オプションを提供します。これらのオプションは、膨大な種類のデビットカードやクレジットカードに対応しています。

- さらに、インドのmPOSの状況は、POS企業のイニシアチブによって拍車がかかり、進化しています。RapiPayは、モバイルPOS(mPOS)機として機能するハイブリッド型マイクロATMを提供しています。このイノベーションにより、顧客はRapiPayステーションでデビットカードと一緒にクレジットカードを利用することができます。従来のATMとは異なり、RapiPayのマイクロATMは利便性を高めており、ユーザーは現金を引き出すだけでなく、RapiPay Direct Business Outletで様々な銀行業務を行うことができます。

インドPOS端末産業の概要

インドのPOS端末市場は競争が激しく、かなりの数の地域プレーヤーが存在します。市場の主要企業には、VeriFone Inc.、Worldline、Ezetap(Razorpay)、MobiSwipe Technologies Private Limited、Mswipe Technologies Pvt Ltd.などがあります。各社は市場シェアと収益性を高めるため、戦略的な提携や企業買収を行っています。

- 2024年6月QueueBusterとOtipyが戦略的パートナーシップを締結。キューバスターの先進的なPOSテクノロジーとOtipyの先駆的な青果物小売における電動カートの活用を融合。キューバスターの高度なPOSテクノロジーは、Otipy社が最近導入した物理的な電動カートにシームレスに統合され、業務効率を強化し、顧客満足度を向上させる。

- 2024年2月インドに本社を置くCSB銀行は、フィンテック企業Bijlipayとの戦略的提携を発表しました。この提携は、包括的なPOSソリューションを提供することで、銀行の決済エコシステムを強化することを目的としています。この提携は、Bijlipayのシームレスに統合されたソリューションを銀行のネットワーク全体で活用することで、顧客満足度を高め、サービス提供を合理化することを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 急速なデジタル化がインドのPOS端末の成長を促進

- 市場成長を向上させる様々な政府イニシアチブの実施

- モバイルPOSシステムへの需要の高まり

- 市場抑制要因

- データ・セキュリティに対する懸念が経済成長を阻害する可能性

- デバイスあたりのコンプライアンス・コストと認証更新コストの高さ

- 市場機会

- 非接触型決済の普及

- POS端末に関する主な規制と苦情基準

- 非接触決済の普及と業界への影響に関する解説

- 主要事例の分析

第6章 市場セグメンテーション

- 決済手段別

- 接触型

- 非接触型

- タイプ別

- 固定POSシステム

- モバイル/ポータブルPOSシステム

- エンドユーザー産業別

- 小売

- ホスピタリティ

- ヘルスケア

- その他のエンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- VeriFone Inc.

- Worldline

- Ezetap(Razorpay)

- MobiSwipe Technologies Private Limited

- Mswipe Technologies Pvt Ltd

- ePaisa

- NGX Technologies

- PayU

- Payswiff

- PAX Technologies Pvt. Ltd

第8章 投資分析

第9章 市場の将来展望

The India POS Terminals Market size is estimated at USD 37.08 billion in 2025, and is expected to reach USD 63.88 billion by 2030, at a CAGR of 11.49% during the forecast period (2025-2030).

Several factors are propelling India's POS terminal market, such as the surging demand for mobile POS terminals, increasing adoption of mobile wallets, supportive regulations, the growth of e-commerce, the influx of new enterprises, urbanization, and technological advancements.

Key Highlights

- The world of payments is undergoing dramatic changes, driven by evolving consumer preferences, technological advancements, and regulatory shifts. India, propelled by the surge in digital transactions, is witnessing remarkable growth, reshaping its payment landscape.

- The Indian retail sector is witnessing a surge, driven by a proliferation of retail outlets and heightened consumer spending. Consequently, there is a growing demand for payment processing machines. With a rising preference for digital transactions over cash among Indian consumers, these machines have become an essential element for retailers.

- India boasts a robust market for point-of-sale (POS) terminals. These devices facilitate cashless transactions, allowing consumers to make payments via their phones or cards. The Indian market for these machines is expanding due to the extended adoption of digital payments over cash. With this shift, there's a growing demand from businesses and stores for specialized POS terminals. Over the last few years, India has witnessed a significant surge in the adoption of card payment machines, enabling businesses to accept digital payments.

- The Reserve Bank of India (RBI), in addition to the government and other ministries, has diligently spearheaded efforts that have led to a significant surge in digital payments. Several of these initiatives have garnered international recognition. Card payments, alongside the Aadhaar-enabled Payment System (AePS), Unified Payments Interface (UPI), Immediate Payment Service (IMPS), QR-based payments, and National Electronic Toll Collection (NETC), have played pivotal roles in the gradual shift from a cash-centric economy to one that is increasingly reliant on digital transactions.

- In October 2023, Paytm, a player in the fintech industry, unveiled its latest innovation: the Paytm Card Soundbox. This advanced device not only offers audio alerts for UPI transactions but also facilitates 'tap-and-pay' card transactions, covering major networks like Visa, Mastercard, Amex, and RuPay. Pine Labs also introduced a cost-effective iteration of its traditional point-of-sale (PoS) terminal, dubbed 'Mini'. The 'Mini' terminal is equipped to process UPI transactions and 'tap-and-pay' card payments across a wide array of networks.

- However, the industry's growth is hampered by a scarcity of PoS terminals. The market faces challenges such as steep installation and maintenance costs, security concerns, and related expenses, all hindering its expansion.

India POS Terminals Market Trends

Retail Segment Expected to Hold Significant Market Share

- Several key factors in India's retail sector are propelling the growth of the POS terminals market. The expansion of organized retail chains and a rising number of independent stores are boosting the demand for efficient transaction processing systems in India. As retailers aim to elevate customer experiences and operational efficiency, the adoption of POS terminals is becoming essential.

- Moreover, the government's initiatives, such as Digital India, are propelling retailers toward digital payment solutions. This momentum is reinforced by both demonetization and the GST implementation, which have spurred businesses to embrace formalized digital transactions.

- As per the Telecom Regulatory Authority of India, as of December 2023, Reliance Jio Infocomm Limited held the most significant service provider of internet subscribers, boasting more than 470 million subscribers, equating to a dominant market share exceeding 50%.

- Furthermore, the surge in e-commerce and omnichannel retailing is driving demand for unified POS systems capable of managing both online and offline transactions effortlessly. Retailers are now prioritizing sophisticated POS solutions, emphasizing features like inventory management, customer relationship management (CRM), and data analytics to maintain their competitive edge.

- The expanding middle class, bolstered by rising disposable incomes, is fuelling the rising consumer spending. This surge is directly translating into a spike in retail sales, underscoring the necessity for streamlined payment systems.

- In February 2024, Zoho Corporation unveiled its latest venture in India, introducing the Zakya brand. Zakya's primary focus is on providing modern Point of Sale (POS) solutions tailored for retail establishments. These solutions aim to simplify daily operations and offer centralized monitoring capabilities. Notably, Zakya's POS system, operating on the cloud, boasts a swift implementation process and a user-friendly interface. This feature set is designed to enable small- and medium-sized retailers to swiftly transition, go live, and initiate billing within an hour of setup.

Mobile Point-of-Sale Anticipated to Register Significant Growth

- Card and mobile payments are surpassing ATM withdrawals in popularity. The shift is driven by a growing preference for digital payment methods. The impetus for this change was the COVID-19 pandemic, which heightened concerns about cash handling, prompting a pivot toward digital transactions. This trajectory is poised to persist, which is evident in the rising adoption of store card payments.

- In India, the trend of utilizing the Unified Payment Interface (UPI) for in-store purchases via smartphones is gaining momentum. To further streamline this process, there is a push toward integrating near-field communication technology with UPI. This advancement not only minimizes physical contact during transactions but also encourages wider UPI adoption among merchants. Additionally, it enhances the digital payment landscape for retailers, an area where UPI has historically seen limited penetration.

- In April 2024, BharatPe, a player in India's fintech sector, unveiled 'BharatPe One,' marking India's all-in-one payment solution. This innovative product combines POS, QR, and speaker functionalities into a single device. This innovative product aims to simplify merchant transactions. It provides a variety of payment acceptance options, such as dynamic and static QR codes, tap-and-pay, and traditional card payments. These options cater to a vast spectrum of debit and credit cards.

- Moreover, India's mPOS landscape is evolving, spurred by initiatives from POS companies. RapiPay stands out, offering hybrid micro-ATMs that function as mobile point-of-sale (mPOS) machines. This innovation enables customers to use credit cards alongside debit cards at RapiPay stations. Unlike conventional ATMs, RapiPay's Micro ATMs offer enhanced convenience, allowing users to not only withdraw cash but also conduct a range of banking operations at any RapiPay Direct Business Outlet.

India POS Terminals Industry Overview

The Indian POS terminal market is moderately competitive, with a considerable number of regional players. Some of the major players in the market are VeriFone Inc., Worldline, Ezetap (Razorpay), MobiSwipe Technologies Private Limited, and Mswipe Technologies Pvt Ltd. Companies are strategically collaborating and acquiring businesses to boost their market share and profitability.

- June 2024: QueueBuster and Otipy entered a strategic partnership. The alliance merges QueueBuster's advanced POS technology with Otipy's pioneering use of Electric Carts in fresh produce retailing. QueueBuster's advanced POS technology would be seamlessly integrated into Otipy's recently introduced physical electric carts, bolstering operational efficiency and elevating customer satisfaction.

- February 2024: CSB Bank, headquartered in India, unveiled a strategic collaboration with fintech firm Bijlipay. This partnership is designed to bolster the bank's payment ecosystem by offering comprehensive POS solutions. Beyond this, the alliance is set to enhance customer satisfaction and streamline service delivery, leveraging Bijlipay's seamlessly integrated solutions across the bank's network.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Digitization Drives the Growth of POS Terminals in India

- 5.1.2 Implementation of Various Government Initiatives to Improve Market Growth

- 5.1.3 Growing Demand for Mobile Point-of-Sale Systems

- 5.2 Market Restraints

- 5.2.1 Concerns Over Data Security Might Restrict Economic Growth

- 5.2.2 High Compliance Costs per Device and Certification Renewal Costs

- 5.3 Market Opportunities

- 5.3.1 Rise in Contactless Payment Adoption

- 5.4 Key Regulations and Complaince Standards of PoS Terminals

- 5.5 Commentary on the Rising Use of Contactless Payment and its Impact on the Industry

- 5.6 Analysis of Major Case Studies

6 MARKET SEGMENTATION

- 6.1 By Mode of Payment Acceptance

- 6.1.1 Contact-based

- 6.1.2 Contactless

- 6.2 By Type

- 6.2.1 Fixed Point-of-sale Systems

- 6.2.2 Mobile/Portable Point-of-sale Systems

- 6.3 By End-User Industry

- 6.3.1 Retail

- 6.3.2 Hospitality

- 6.3.3 Healthcare

- 6.3.4 Other End-User Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 VeriFone Inc.

- 7.1.2 Worldline

- 7.1.3 Ezetap (Razorpay)

- 7.1.4 MobiSwipe Technologies Private Limited

- 7.1.5 Mswipe Technologies Pvt Ltd

- 7.1.6 ePaisa

- 7.1.7 NGX Technologies

- 7.1.8 PayU

- 7.1.9 Payswiff

- 7.1.10 PAX Technologies Pvt. Ltd