|

市場調査レポート

商品コード

1910650

手術室機器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Operating Room Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 手術室機器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

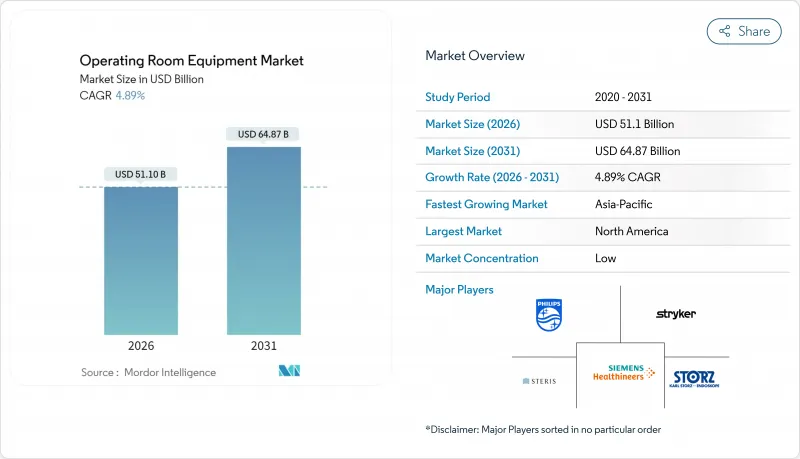

2026年の手術室機器市場の規模は511億米ドルと推定され、2025年の487億2,000万米ドルから成長し、2031年には648億7,000万米ドルに達すると予測されています。

2026年から2031年にかけての年間平均成長率(CAGR)は4.89%となる見込みです。

現在の支出傾向は、純粋な容量拡大よりも、手術時間の短縮、視覚化の向上、人工知能の組み込みといった技術に重点が置かれております。病院がパンデミック後の手術の遅れに対応する中、術中画像診断とAI駆動型ワークフローソフトウェアを備えたハイブリッド手術室は、引き続き予算優先事項となっております。資本支出は人口動態の変化にも連動しており、アジア太平洋地域の医療システムは新たな手術室への投資を進める一方、北米の医療提供者はサイバーセキュリティ対策が施され、アップグレード対応可能なプラットフォームで既存設備の更新を進めております。サプライヤー間の統合が進み、競合環境が再構築されています。大手ベンダーがニッチなイノベーターを買収し、統合ポートフォリオを拡充するとともに、複数年にわたるサービス契約を確保している状況です。

世界の手術室機器市場の動向と洞察

手術を必要とする慢性疾患の増加傾向

心血管疾患、腫瘍性疾患、筋骨格系疾患は、人口の高齢化と生活習慣リスクの増加に伴い、手術件数を押し上げています。整形外科用関節鏡検査だけでも、高スループット手術室プラットフォームへの持続的な需要を示すと予測されています。臨床医は、多段階介入を必要とする合併症患者に対応するため、多目的手術台、汎用性の高い画像診断装置、高度な麻酔ワークステーションを必要としています。支払機関が1回あたりの費用を精査する中、安全性を維持しながら手術室転換時間を短縮する相互運用可能なシステムをバンドルできるベンダーが最大の恩恵を受けます。

増加する病院数と政府資金

インド、インドネシア、中国本土における医療施設拡充計画は、天井吊り式手術灯、電気手術装置、基本患者モニターといった中核機器の継続的な調達案件につながっています。国内製造奨励策により輸入関税が引き下げられ価格帯が拡大したことで、世界の企業は現地のサービス環境に適した中級ラインの製品展開を加速させています。スウェーデン拠点のゲティンゲ社は、新興市場の予算に適合したモジュラー式滅菌処理システムと手術台パッケージを提供し、インド市場で45%のシェア獲得を目指しています。

手術室設備の高額な資本コストと維持費

遮蔽設備、空調設備のアップグレード、保守契約を含む包括的なハイブリッド設置費用は300万米ドルを超えます。そのため、コスト重視の購入者は、資産寿命を延長するモジュラー式天井柱や改修対応型イメージングレールを好みます。リースや設備サービスモデルは設備投資を予測可能な運用コストに変換しますが、ソフトウェアライセンス、サイバーセキュリティパッチ、トレーニングを考慮すると、総所有コストは依然として上昇します。

セグメント分析

2025年時点で麻酔ワークステーションが25.31%と最大の収益シェアを占めました。あらゆる処置に気道管理と生理学的モニタリングが必須であるため、需要は非弾力的です。麻酔機器の市場規模は急増ではなく、症例数に連動した着実な成長が見込まれます。一方、外科用イメージングシステムは、リアルタイムガイダンスを必要とするハイブリッド血管・神経手術室により、2031年までにCAGR11.05%で拡大する見込みです。イメージングソリューション向け手術室機器市場規模は、フラットパネル検出器、ナビゲーション、拡張現実オーバーレイを組み合わせたソリューションの提供により、2031年までに100億米ドル規模に達すると予測されます。

電気外科用ジェネレーターは低侵襲技術が普及する中で依然として重要性を保ちますが、現在では組織インピーダンスに適応するインテリジェントなエネルギー変調技術が革新の中心となっています。天井設置型医療ペンダントは、電力・ガス・データを提供するネットワークハブへと進化し、接続型手術室エコシステムに不可欠な存在となっています。複数の米国州が使用を義務付けたことを受け、煙排出装置の導入が加速しています。ミズーリ州では2026年1月から順守が実施されます。LGなどのディスプレイメーカーは、繊細な顕微手術における奥行き認識と色再現性を高める4KミニLEDモニターを導入しています。

地域別分析

北米は収益の37.55%を占めております。これは、AI対応ワークフローツールやサイバーセキュリティネットワークの早期導入を支援する償還制度によるものです。米国の病院では、待機手術の解消と旧式設備の近代化に向け、2026年までに設備投資を9%増加させる計画です。カナダの州保健当局は患者移送削減のためハイブリッド手術室の共同出資を進め、メキシコの民間チェーンは医療観光客誘致に向け高級キャンパスを整備しています。手術室機器市場では、施設がプラットフォームを混在させつつFDAサイバーセキュリティ指令に準拠できるよう、ベンダー中立の統合レイヤーが引き続き重視されています。

アジア太平洋地域は6.54%という最速のCAGRを記録しており、インドと中国が公的・民間セクター双方で外科インフラを拡充しているためです。国際的なサプライヤーは、スタッフのスキル向上と投資対効果の証明を目的としてトレーニングアカデミーを開設しており、東南アジアにおけるメドトロニックの「ロボティクス・エクスペリエンス・スタジオ」がその戦略の好例です。日本と韓国は高齢化関連専門分野に注力し、ロボット内視鏡やスマート麻酔システムへ投資することで入院期間の短縮を図っています。インドネシア、ベトナム、フィリピンの価格感応度の高いセグメントでは、包括的な手術室構築への入り口として、モジュラー式ペンダントや耐久性の高い診断用画像装置が好まれています。

欧州では、ドイツ、フランス、英国が主導して、炭素削減のための改造やヘリウム効率の高いMRIスイートの共同出資を行い、緩やかな拡大を維持しています。フィリップスと画像診断プロバイダーのEvidiaが、持続可能なスキャナーを導入するために提携したことは、気候変動対策が調達に影響を与えていることを示しています。中東およびアフリカの成長は、湾岸協力会議(GCC)加盟国に集中しており、主要な大学病院は、海外からの医療観光客を獲得するために、フルハイブリッドパッケージを購入しています。ブラジルが先導する南米は、通貨変動の中で徐々に近代化が進んでおり、基本的なテーブルや照明は現地の組立業者に依存しながら、高級な血管イメージング機器を輸入しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3か月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 手術を必要とする慢性疾患の増加傾向

- 増加する病院数と政府資金

- 低侵襲手術および画像誘導手術の導入拡大

- 高度な術中画像診断機能を備えたハイブリッド手術室への急速な移行

- 手術室効率化のためのAI駆動型ワークフロー分析の導入

- パンデミック後の選択的手術のバックログが手術室のアップグレードを促進

- 市場抑制要因

- 手術室設備の高額な資本コストと維持管理費

- 熟練した周術期スタッフの不足

- 統合手術室プラットフォームにおけるサイバーセキュリティリスク

- AI搭載手術機器の規制遅延

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額は米ドル建て)

- 製品別

- 麻酔装置

- 外科用画像システム

- 電気外科用機器

- 手術台

- 手術用照明・診察用照明

- 患者モニター

- 医療用ペンダント及びブーム

- 煙排出システム

- その他の手術室機器

- モビリティ別

- 固定式/内蔵式

- モジュラー/レトロフィット

- モバイル/ポータブル

- エンドユーザー別

- 病院

- 外来手術センター

- 外来施設/専門クリニック

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Koninklijke Philips NV

- STERIS

- Stryker Corporation

- Karl Storz SE & Co. KG

- Siemens Healthineers AG

- Baxter International

- Getinge AB

- Medtronic plc

- GE HealthCare

- Mizuho OSI

- Dragerwerk AG & Co. KGaA

- Olympus Corporation

- Hill-Rom Holdings Inc.

- Skytron LLC

- Conmed Corporation

- Zimmer Biomet Holdings Inc.

- Leica Microsystems GmbH

- Sony Medical Systems

- EIZO Corp.

- Trumpf Medical