|

市場調査レポート

商品コード

1684793

高速データコンバータの市場機会、成長促進要因、産業動向分析、2025年~2034年予測High-speed Data Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 高速データコンバータの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

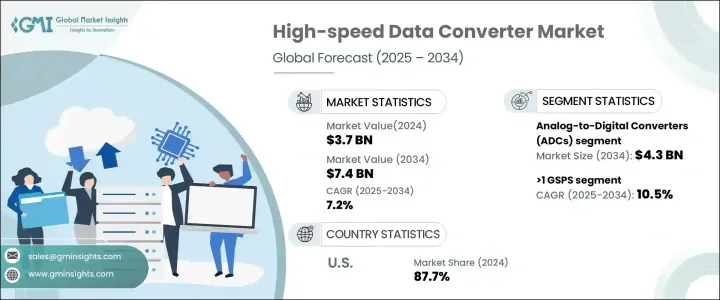

高速データコンバータの世界市場は、2024年に37億米ドルと評価され、2025年から2034年にかけてCAGR7.2%で成長すると予測されています。

この成長の原動力となっているのは、5G技術と次世代通信ネットワークの急速な進化であり、これが高速データコンバータの需要に拍車をかけています。これらのデバイスは、効率的な信号トランスミッションと処理に不可欠であり、現代の通信インフラに欠かせないものとなっています。高速データコンバータは、シームレスな接続性と最適なパフォーマンスを確保する上で極めて重要な役割を果たしています。

また、通信、産業オートメーション、自動車など、リアルタイムのデータ処理とシステム効率が最重要視される分野でも、高速データコンバータの採用が進んでいます。さらに、エネルギー効率の高い高解像度コンポーネントへのシフトが、ハイテクアプリケーションにおけるスピードと精度に対する需要の高まりに対応する高度なデータコンバータの開発を加速させています。IoTデバイスの統合が進み、人工知能や機械学習の進歩も相まって、高速データコンバータの必要性がさらに高まっています。これらの技術は、正確で効率的なデータ処理に大きく依存しているためです。市場の成長軌道は、より小型でエネルギー効率に優れた高性能コンバータの製造を可能にする半導体技術の継続的な革新によっても支えられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 37億米ドル |

| 予測金額 | 74億米ドル |

| CAGR | 7.2% |

市場はタイプ別に区分され、アナログデジタルコンバータ(ADC)とデジタルアナログコンバータ(DAC)が主要なカテゴリーです。ADCは、アナログ信号を正確にデジタル化する需要の高まりにより、2034年には43億米ドルに達すると予測されています。リアルタイムのデータ変換を必要とする産業は、低消費電力と高分解能を提供する高性能ADCの開発を推進しています。これらのコンバータは、高速データ処理を必要とするアプリケーションに不可欠であり、進化するデジタルエコシステムの要となっています。DACの需要も、産業界がさまざまなアプリケーションにおける信号変換の品質と効率の向上を求めていることから高まっています。

周波数帯域によって、市場は125MSPS、125 MSPS~1 GSPS、1 GSPS以上に分けられます。1 GSPS超セグメントは最も速い速度で成長し、予測期間中のCAGRは10.5%と予測されます。この成長の背景には、先端アプリケーションにおける高速データ処理のニーズの高まりがあります。一方、125 MSPS~1 GSPSのセグメントは、性能と電力効率のバランスの良さから依然として人気が高いです。自動車、衛星通信、ミッドレンジ通信などの業界は、ネットワーク機能を強化し、適度なビットレートをサポートすることから、これらのコンバータの採用を促進しています。

米国は2024年の高速データコンバータ市場で87.7%のシェアを占め、5Gインフラの急速な拡大、半導体分野の旺盛な需要、IoTサービスの普及がその原動力となっています。防衛・航空宇宙用途への注目の高まりも、高性能データコンバータの需要拡大に寄与しています。業界大手間の戦略的提携が技術革新と研究を促進し、市場の成長をさらに後押ししています。技術とインフラ開拓の進展が高速データコンバータの新たな機会を生み出すため、米国市場の優位は今後も続くと予想されます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 高速通信ネットワークに対する需要の増加

- データ中心アプリケーションの成長

- コンシューマーエレクトロニクス市場の拡大

- カーエレクトロニクスの進歩

- ソフトウェア無線(SDR)の採用増加

- 業界の潜在的リスク・課題

- 設計の複雑さと製造コストの高さ

- 急速な技術進化と短い製品ライフサイクル

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- アナログ/デジタルコンバータ(ADC)

- デジタル/アナログコンバータ(DAC)

第6章 市場推計・予測:解像度別、2021年~2034年

- 主要動向

- 8ビット

- 10ビット

- 12ビット

- 16ビット

- 24ビット以上

第7章 市場推計・予測:周波数帯別、2021年~2034年

- 主要動向

- 125 MSPS以下

- 125 MSPS~1 GSPS

- 1 GSPS以上

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自動車

- 通信

- 産業用

- テスト・マネジメント

- ヘルスケア

- コンシューマーエレクトロニクス

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- IQ-ANALOG

- Advanced Micro Devices, Inc.

- Analog Devices, Inc.

- Asahi Kasei Microdevices Corporation

- Avia Semiconductor Ltd.

- Broadcom Inc.

- Datel, Inc.

- Faraday Technology Corporation

- GlobalSpec

- Infineon Technologies AG

- Microchip Technology Inc.

- Monolithic Power Systems, Inc.

- Mouser Electronics, Inc.

- NXP Semiconductors

- ON Semiconductor

- Qualcomm Technologies, Inc.

- Renesas Electronics Corporation

- ROHM Semiconductor

- STMicroelectronics

- Texas Instruments

The Global High-Speed Data Converter Market, valued at USD 3.7 billion in 2024, is expected to grow at a CAGR of 7.2% from 2025 to 2034. This growth is driven by the rapid evolution of 5G technology and next-generation communication networks, which are fueling the demand for high-speed data converters. These devices are critical for efficient signal transmission and processing, making them indispensable in modern telecommunications infrastructure. As industries strive to meet the increasing need for higher data rates and lower latency, high-speed data converters are playing a pivotal role in ensuring seamless connectivity and optimal performance.

The market is also benefiting from the growing adoption of these converters in sectors such as telecommunications, industrial automation, and automotive, where real-time data processing and system efficiency are paramount. Additionally, the shift toward energy-efficient and high-resolution components is accelerating the development of advanced data converters, which cater to the rising demand for speed and accuracy in high-tech applications. The increasing integration of IoT devices, coupled with advancements in artificial intelligence and machine learning, is further amplifying the need for high-speed data converters, as these technologies rely heavily on precise and efficient data processing. The market's growth trajectory is also supported by ongoing innovations in semiconductor technology, which are enabling the production of more compact, energy-efficient, and high-performance converters.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 7.2% |

The market is segmented by type, with Analog-to-Digital Converters (ADCs) and Digital-to-Analog Converters (DACs) being the primary categories. ADCs are projected to reach USD 4.3 billion by 2034, driven by the increasing demand for accurate digitalization of analog signals. Industries requiring real-time data conversion are pushing the development of high-performance ADCs that offer lower power consumption and enhanced resolution. These converters are essential for applications that demand high-speed data processing, making them a cornerstone of the evolving digital ecosystem. The demand for DACs is also rising as industries seek to improve the quality and efficiency of signal conversion in various applications.

Based on frequency bands, the market is divided into 125 MSPS, 125 MSPS to 1 GSPS, and >1 GSPS. The >1 GSPS segment is expected to grow at the fastest rate, with a projected CAGR of 10.5% during the forecast period. This growth is attributed to the increasing need for high-speed data processing in advanced applications. Meanwhile, the 125 MSPS to 1 GSPS segment remains a popular choice due to its balance of performance and power efficiency. Industries such as automotive, satellite communications, and mid-range telecommunications are driving the adoption of these converters as they enhance network capabilities and support moderate bit rates.

The United States held an 87.7% share of the high-speed data converter market in 2024, driven by the rapid expansion of 5G infrastructure, strong demand in the semiconductor sector, and the widespread adoption of IoT services. The growing focus on defense and aerospace applications is also contributing to the rising demand for high-performance data converters. Strategic collaborations among leading industry players are fostering innovation and research, further propelling the market's growth. The US market's dominance is expected to continue as advancements in technology and infrastructure development create new opportunities for high-speed data converters.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for high-speed communication networks

- 3.6.1.2 Growth in data-centric applications

- 3.6.1.3 Expanding consumer electronics market

- 3.6.1.4 Advancements in automotive electronics

- 3.6.1.5 Rising adoption of Software-Defined Radios (SDRs)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High design complexity and manufacturing costs

- 3.6.2.2 Rapid technological evolution and short product lifecycles

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Analog-to-Digital Converters (ADCs)

- 5.3 Digital-to-Analog Converters (DACs)

Chapter 6 Market Estimates & Forecast, By Resolution, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 8-bit

- 6.3 10-bit

- 6.4 12-bit

- 6.5 16-bit

- 6.6 24-bit and above

Chapter 7 Market Estimates & Forecast, By Frequency Band, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 <125 MSPS

- 7.3 125 MSPS TO 1 GSPS

- 7.4 >1 GSPS

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Telecommunications

- 8.4 Industrial

- 8.5 Test & management

- 8.6 Healthcare

- 8.7 Consumer Electronics

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 IQ-ANALOG

- 10.2 Advanced Micro Devices, Inc.

- 10.3 Analog Devices, Inc.

- 10.4 Asahi Kasei Microdevices Corporation

- 10.5 Avia Semiconductor Ltd.

- 10.6 Broadcom Inc.

- 10.7 Datel, Inc.

- 10.8 Faraday Technology Corporation

- 10.9 GlobalSpec

- 10.10 Infineon Technologies AG

- 10.11 Microchip Technology Inc.

- 10.12 Monolithic Power Systems, Inc.

- 10.13 Mouser Electronics, Inc.

- 10.14 NXP Semiconductors

- 10.15 ON Semiconductor

- 10.16 Qualcomm Technologies, Inc.

- 10.17 Renesas Electronics Corporation

- 10.18 ROHM Semiconductor

- 10.19 STMicroelectronics

- 10.20 Texas Instruments