|

市場調査レポート

商品コード

1773320

手術室機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Operating Room Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 手術室機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

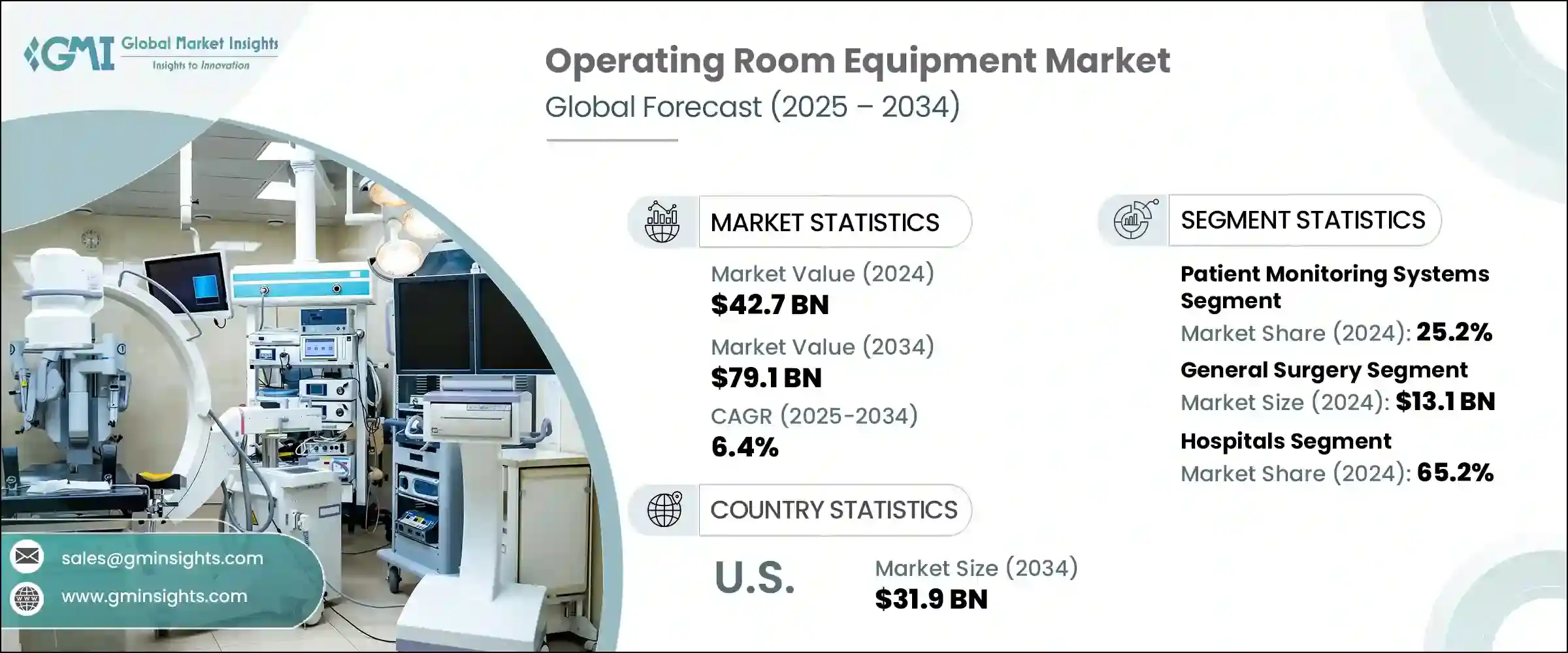

世界の手術室機器市場は、2024年に427億米ドルと評価され、CAGR6.4%で成長し、2034年までには791億米ドルに達すると推定されています。

この市場には、安全で効果的な外科手術を促進するために不可欠なツール、機械、システム、インフラが幅広く含まれています。整形外科疾患、がん、心臓病などの慢性疾患の世界の負担に煽られた外科手術の着実な増加が、市場の拡大を大幅に加速しています。ヘルスケアインフラの近代化に対する注目の高まりと、より技術的に高度な手術手技へのシフトは、主要な成長要因です。病院は、特に複雑な症例に対する手術の精度、安全性、効率性を高めるため、次世代ソリューションに投資しています。最新の手術室には、ロボットシステム、統合された手術室プラットフォーム、画像技術が組み込まれ、侵襲を最小限に抑え、治療成績を向上させています。

これらのシステムによる視覚化と正確なデータの向上は、より良い臨床判断と迅速な回復をサポートし、質の高い医療への普遍的なアクセスを拡大するという広範な目標に沿うものです。これらの高度な技術により、外科医や医療スタッフはバイタルサインや内部構造をリアルタイムでモニターすることができ、手技の結果を大幅に改善し、合併症の可能性を減らすことができます。高精細画像、統合されたソフトウェアプラットフォーム、AIを駆使した解析は、より正確な診断と手術計画の立案に貢献します。このレベルの洞察力は、手技の侵襲性を低減するだけでなく、入院期間の短縮、再入院率の最小化、術後のオーダーメイド医療をサポートします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 427億米ドル |

| 予測金額 | 791億米ドル |

| CAGR | 6.4% |

様々な製品カテゴリーの中で、患者モニタリングシステム分野は2024年に25.2%のシェアを占めました。外科医や麻酔科医は、外科手術中の酸素飽和度、心電図、血圧などのバイタルサインをリアルタイムで追跡するこれらのシステムに大きく依存しています。心臓、神経、臓器移植のようなリスクの高い手術では、正確さと継続的なフィードバックが重要であり、需要は高いです。アラーム設定やデータトレンド機能を備えた高度なモニタリング装置は、患者の安全を確保し、一刻を争う環境での臨床的意思決定をサポートするために広く採用されています。手術手技が複雑化するにつれ、信頼性の高い術中モニタリングは合併症の軽減と手術成績の向上に役立つため、高性能モニタリングソリューションの需要が高まっています。

一般外科分野は2024年に131億米ドルを生み出し、引き続き機器需要の主要な牽引役となっています。ヘルニア修復、胆嚢摘出、盲腸切除などの日常的な処置は、世界市場全体で一貫した処置量に貢献しています。この安定した需要が、麻酔システム、手術台、電気手術ユニット、手術用照明など、手術室に不可欠な機器への定期的な投資を促進します。病院が症例の遅延を減らし、手術スケジュールを最適化することを目指しているため、手術室の生産性向上に対するプレッシャーが高まっています。一般外科は、様々な期間の手術を大量に扱うため、特に、古くなったインフラを交換し、症例の迅速なターンアラウンドとリソースの有効利用を促進するシステムを採用することに重点を置いています。

米国の手術室機器の市場規模は2024年に174億米ドルとなり、2034年には319億米ドルに達すると推定されています。同国の外科手術率の高さは、主に高齢化社会と肥満、がん、心血管疾患などの慢性疾患の蔓延によるものです。手術需要の高まりにより、病院システムや手術センターは先進的な手術室技術への投資を余儀なくされています。学術医療センターから大規模な医療ネットワークに至るまで、ヘルスケア機関は外科インフラのアップグレードや拡張に多額の資本予算を割いています。これにより、医療の質を向上させ、手術の待ち時間を短縮し、進化する臨床基準に対応することができます。OR環境の一貫した近代化は、米国市場全体の力強い成長を牽引し続けています。

この業界の発展に貢献している主要企業は、Getinge、Stryker、Olympus、Medtronic、GE HealthCare、Philips、Karl Storz、Smith &Nephew、Siemens Healthineers、Dragerwerk、Zimmer Biomet、B. Braun、Johnson &Johnson、Baxter International、Mindrayなどです。強力な競争力を維持するため、OR機器市場で事業を展開する企業はさまざまな標的戦略を採用しています。これには、画像技術、統合技術、ロボット技術の革新による製品ポートフォリオの拡大が含まれます。多くの企業は、病院や手術センターとの提携に注力し、一括ソリューションやターンキー手術室設置を提供しています。また、低侵襲ツールやAI搭載システムの研究開発への投資も、スマートな手術環境に対するニーズの高まりに対応する一助となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術の需要の高まり

- 外科用画像診断とロボットシステムにおける技術的進歩

- 慢性疾患の有病率の増加

- 特に新興国におけるヘルスケアインフラの拡大

- 業界の潜在的リスク・課題

- 高度な手術室技術に関連する高い資本コスト

- 熟練した専門家の不足

- 市場機会

- 外来手術センターの拡大

- スマートORと接続技術の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 特許分析

- 価格分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 手術器具

- 麻酔器具

- 手術台

- 手術室の照明

- 電気外科ユニット

- 患者モニタリングシステム

- 内視鏡機器

- その他の製品タイプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 一般外科

- 整形外科

- 心臓血管外科

- 脳神経外科

- 婦人科手術

- 耳鼻咽喉科手術

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- 学術研究機関

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- B. Braun

- Baxter International

- Dragerwerk

- GE HealthCare

- Getinge

- Johnson &Johnson

- Karl Storz

- Medtronic

- Mindray

- Olympus

- Philips

- Siemens Healthineers

- Smith &Nephew

- Stryker

- Zimmer Biomet

The Global Operating Room Equipment Market was valued at USD 42.7 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 79.1 billion by 2034. This market encompasses a broad range of essential tools, machines, systems, and infrastructure used to facilitate safe and effective surgical procedures. A steady rise in surgeries fueled by the global burden of chronic illnesses-such as orthopedic conditions, cancers, and heart diseases-is significantly accelerating market expansion. The increasing focus on healthcare infrastructure modernization and a shift toward more technologically advanced surgical techniques are key growth contributors. Hospitals are investing in next-generation solutions to enhance surgical precision, safety, and efficiency, particularly for complex cases. Modern surgical suites now incorporate robotic systems, integrated OR platforms, and imaging technologies to minimize invasiveness and improve outcomes.

Enhanced visualization and accurate data through these systems support better clinical decisions and faster recovery, aligning with the broader goal of expanding universal access to quality care. These advanced technologies allow surgeons and medical staff to monitor vital signs and internal structures in real time, significantly improving procedural outcomes and reducing the likelihood of complications. High-definition imaging, integrated software platforms, and AI-powered analytics contribute to more precise diagnostics and surgical planning. This level of insight not only reduces the invasiveness of procedures but also shortens hospital stays, minimizes readmission rates, and supports tailored post-operative care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $42.7 Billion |

| Forecast Value | $79.1 Billion |

| CAGR | 6.4% |

Among various product categories, patient monitoring systems segment held a 25.2% share in 2024. Surgeons and anesthesiologists rely heavily on these systems for real-time tracking of vital signs like oxygen saturation, ECG, and blood pressure during surgical procedures. The demand is strong for high-risk surgeries such as cardiac, neurological, and organ transplants, where accuracy and continuous feedback are critical. Advanced monitoring devices equipped with alarm settings and data trend capabilities are being widely adopted to ensure patient safety and support clinical decision-making in time-sensitive environments. As surgical procedures become more complex, reliable intraoperative monitoring helps in reducing complications and improving surgical outcomes, thus boosting the demand for high-performance monitoring solutions.

The general surgery segment generated USD 13.1 billion in 2024 and continues to be a major driver of equipment demand. Routine procedures such as hernia repairs, gallbladder removals, and appendectomies contribute to a consistent procedural volume across global markets. This steady demand fuels recurring investments in essential operating room tools including anesthesia systems, surgical tables, electrosurgical units, and surgical lighting. As hospitals aim to reduce case delays and optimize surgical scheduling, there is greater pressure to enhance operating room productivity. General surgery departments, which handle a high volume of procedures with varying durations, are particularly focused on replacing outdated infrastructure and adopting systems that facilitate rapid case turnaround and better resource utilization.

U.S. Operating Room Equipment Market generated USD 17.4 billion in 2024 and is estimated to reach USD 31.9 billion by 2034. The country's high surgical procedure rate is primarily driven by its aging population and widespread chronic diseases such as obesity, cancer, and cardiovascular issues. The growing procedural demand has compelled hospital systems and surgical centers to invest in advanced operating room technologies. Institutions ranging from academic medical centers to large healthcare networks allocate significant capital budgets to upgrade or expand their surgical infrastructure. This enables them to improve care quality, reduce surgical wait times, and keep pace with evolving clinical standards. The consistent modernization of OR environments continues to drive robust growth across the U.S. market landscape.

Leading players contributing to the development of this industry include Getinge, Stryker, Olympus, Medtronic, GE HealthCare, Philips, Karl Storz, Smith & Nephew, Siemens Healthineers, Dragerwerk, Zimmer Biomet, B. Braun, Johnson & Johnson, Baxter International, and Mindray. To maintain a strong competitive edge, companies operating in the OR equipment market are adopting a range of targeted strategies. These include expanding product portfolios through innovation in imaging, integration, and robotic technologies. Many are focusing on partnerships with hospitals and surgical centers to offer bundled solutions or turnkey operating room installations. Investments in R&D for minimally invasive tools and AI-powered systems are also helping players meet the growing need for smart surgical environments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By product type

- 2.2.3 By application

- 2.2.4 By end use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for minimally invasive surgeries

- 3.2.1.2 Technological advancements in surgical imaging and robotic systems

- 3.2.1.3 Growth in chronic disease prevalence

- 3.2.1.4 Expanding healthcare infrastructure, especially in emerging economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital costs associated with advanced operating room technologies

- 3.2.2.2 Lack of skilled professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Growing expansion of outpatient surgery centers

- 3.2.3.2 Integration of smart OR and connected technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical instruments

- 5.3 Anesthesia equipment

- 5.4 Operating tables

- 5.5 Operating room lights

- 5.6 Electrosurgical units

- 5.7 Patient monitoring systems

- 5.8 Endoscopy equipment

- 5.9 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Orthopedic surgery

- 6.4 Cardiovascular surgery

- 6.5 Neurosurgery

- 6.6 Gynecological surgery

- 6.7 ENT surgery

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B. Braun

- 9.2 Baxter International

- 9.3 Dragerwerk

- 9.4 GE HealthCare

- 9.5 Getinge

- 9.6 Johnson & Johnson

- 9.7 Karl Storz

- 9.8 Medtronic

- 9.9 Mindray

- 9.10 Olympus

- 9.11 Philips

- 9.12 Siemens Healthineers

- 9.13 Smith & Nephew

- 9.14 Stryker

- 9.15 Zimmer Biomet