|

|

市場調査レポート

商品コード

1641870

コンプレッサ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| コンプレッサ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 243 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

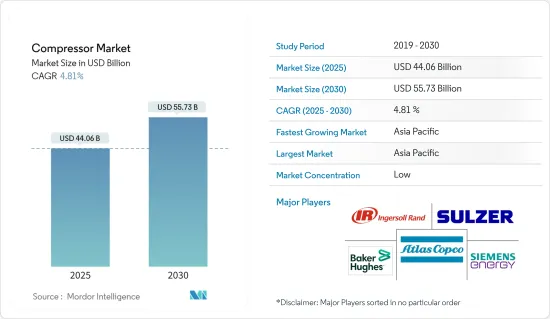

コンプレッサ市場規模は2025年に440億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.81%で、2030年には557億3,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、天然ガス需要の拡大がガスパイプラインネットワークの拡大につながるなどの要因が、コンプレッサ市場の最も大きな促進要因の1つになると予想されます。

- その一方で、太陽光発電や風力発電の導入が増加することで、石炭や天然ガスといった化石燃料を燃料とする発電への依存度が低下することが予想されます。これは、予測期間中のコンプレッサ市場に脅威をもたらします。

- エンドユーザーの需要が高まり、エネルギー効率基準が変化する中、コンプレッサメーカー数社は、よりエネルギー効率の高い製品の開発に邁進しています。この要因は、将来的に市場にいくつかの機会を生み出すと予想されます。

- アジア太平洋が市場を独占しており、予測期間中に最も高いCAGRで推移する可能性が高いです。中国とインドが市場を牽引しているのは、これらの国々の天然ガスインフラが成長しているためです。

コンプレッサ市場動向

石油・ガスセグメントが市場を独占する見込み

- 容積式コンプレッサとダイナミックコンプレッサは、石油・ガス産業で広く使用されており、上流、中流、下流の各セクターを網羅しています。コンプレッサは、ガス輸送、ガス注入のための圧縮、ガス収集、ガスリフトなど、石油・ガスセクターのさまざまな目的に使用されます。

- 貯留層の圧力は時間とともに低下する傾向があるため、ダイナミック・コンプレッサは、ガス田開発の後期段階で、パイプライン・ネットワークへのガス流量を維持または増加させるために利用されます。ガス再圧入は、油田の自然減産を相殺するために増進回収法(EOR)で採用されます。

- 過去10年間の環境意識の高まりを受けて、ほとんどの国が、石炭ベースの発電からガスベースの発電に切り替えることによって二酸化炭素排出量を削減することを計画しています。石油・ガス産業からのコンプレッサ需要は、天然ガスの生産量と発電用消費量が増加し続ける可能性に支えられていると予想されます。エネルギーラボ(EI)は、2022年の世界の天然ガス生産量は2015年比15.3%増の4兆438億立方メートルと予測しています。

- インドは需要の増加に対応するため、ガスパイプラインのインフラを拡大しています。インド政府は複数の州にまたがるパイプラインプロジェクトを発表しました。例えば、2024年1月、政府はIndian Oil Corporation Ltd(IOCL)の全長488kmの天然ガス・パイプラインとHindustan Petroleum Corporation Ltd(HPCL)の全長697kmの石油パイプライン(VDPL)を含む900億インドルピー(11億米ドル)のガス・パイプラインプロジェクトを開始しました。

- 同様に、中国政府は2060年までにネットゼロ排出という目標を掲げています。同国のエネルギー転換戦略では、天然ガスはCO2排出量削減の重要な役割を担うことになっており、今後10年以内に同国の主要エネルギー源になると予測されています。

- さらに、米国エネルギー情報局(EIA)は、国際的な天然ガス需要の増加が予想されるため、米国のLNG輸出量は2020~2029年の間に2倍以上になると予測しており、コンプレッサ市場にも好影響を与えそうです。

- 上記の要因の結果、石油・ガスセグメントが予測期間中にコンプレッサ市場を独占する可能性が高いです。

アジア太平洋が市場を独占する

- 世界有数の天然ガス輸入国と消費国は、アジア太平洋に位置しています。エネルギー需要のために、この地域はまだ主に石炭と石油に頼っています。しかし、大気汚染に対する懸念の高まりから、最近では天然ガスをより頻繁に使用する傾向にあります。

- この地域で天然ガスを最も多く使用しているのは、製造業と発電部門です。中国やインドなどの国々におけるエネルギー消費の増加が、天然ガス市場を促進すると予想されています。

- 住宅用ガス消費は、アジア太平洋諸国における都市化と中間層の拡大により増加すると予測されています。ガス消費量の増加により、ガス圧縮機のニーズは、電力部門や製造部門、ガス中流産業で増加すると予想されます。

- さらに、アジア太平洋の精製部門は過去10年間で著しく増加しており、遠心式コンプレッサのようなコンプレッサは精製プロセスで不可欠に使用されています。Statistical Review of World Energy Dataによると、2022年のアジア太平洋の製油所能力は日量3,618万9,000バレルで、2013年と比較して8.9%増加しました。この数字は、今後数年間で多くのプロジェクトが開始されるため、予測期間中に大幅に増加すると予想されます。

- 中国は今後10年間、天然ガス・石油パイプライン網を強化することで、エネルギーミックスにおけるクリーン燃料の比率を高める意向です。国家開発改革委員会によると、中国の石油・ガスパイプライン網は2025年までに24万kmに拡大すると予想されています。天然ガスパイプラインは、24万kmのうち12万3,000kmをカバーすると予想されています。コンプレッサは、長距離天然ガスパイプラインの動力源として最も頻繁に使用される機械のひとつであるため、パイプライン網の拡大に伴い、コンプレッサの需要は予測期間を通じて増加すると予想されます。

- 同様に、インドは石油化学部門に大規模な投資を行っており、コンプレッサの需要増加が見込まれています。例えば、2023年12月、インド政府は、グジャラート州で開催されたVibrant Gujarat Global Summitの前イベントで、化学・石油化学産業向けに6,700億インドルピー(83億米ドル)相当の11件のMoUに調印しました。石油化学セクターへの投資は、予測期間中にこの地域で急激に増加し、産業全体のコンプレッサ需要を大幅に引き上げると予想されています。

- これらの要因から、予測期間中、アジア太平洋がコンプレッサ市場を独占すると予想されています。

コンプレッサ産業概要

コンプレッサ市場はセグメント化されています。この市場の主要企業(順不同)には、Atlas Copco AB、Baker Hughes Co.、Ingersoll-Rand Inc.、Siemens Energy AG、Sulzer Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 市場促進要因

- 天然ガス需要の増大

- 世界のパイプラインインフラの増加

- 市場抑制要因

- 太陽エネルギーと風力エネルギーの採用増加

- 市場促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- エンドユーザー別

- 石油・ガス産業

- 電力セクター

- 製造業

- 化学・石油化学産業

- その他

- タイプ別

- 容積式

- ダイナミック

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- ノルウェー

- トルコ

- ロシア

- ノルディック

- その他の欧州

- アジア太平洋

- 中国

- インド

- マレーシア

- タイ

- オーストラリア

- インドネシア

- ベトナム

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Aerzener Maschinenfabrik GmbH

- Ariel Corporation

- Atlas Copco AB

- Baker Hughes Co.

- Bauer Compressors Inc.

- Burckhardt Compression Holding AG

- Ebara Corporation

- Ingersoll Rand Inc

- Siemens Energy AG

- Sulzer Ltd

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 複数のコンプレッサメーカーがよりエネルギー効率の高い製品の開発に邁進

目次

Product Code: 61051

The Compressor Market size is estimated at USD 44.06 billion in 2025, and is expected to reach USD 55.73 billion by 2030, at a CAGR of 4.81% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as growing demand for natural gas, which, in turn, is leading to a growing gas pipeline network, are expected to be one of the most significant drivers for the compressor market.

- On the other hand, increasing solar and wind power installation is expected to decrease the countries' dependency on fossil fuel-fired power generation, such as coal and natural gas. This poses a threat to the compressor market during the forecast period.

- Nevertheless, several compressor manufacturers are making strides to develop more energy-efficient products amid rising end-user demands and changing energy efficiency standards. This factor is expected to create several opportunities for the market in the future.

- The Asia-Pacific region dominates the market and will likely register the highest CAGR during the forecast period. China and India drive it due to these countries' growing natural gas infrastructure.

Compressor Market Trends

Oil and Gas Segment Expected to Dominate the Market

- Positive displacement and dynamic compressors are widely used in the oil and gas industry, encompassing upstream, midstream, and downstream sectors. Compressors are used for various purposes in the oil and gas sector, including gas transportation, compression for gas injection, gas collection, and gas lift.

- As reservoir pressure tends to drop with time, dynamic compressors are utilized in later stages of gas field development to sustain or boost gas flow into pipeline networks. Gas reinjection is employed in enhanced oil recovery (EOR) to offset the oil fields' natural reduction in production.

- Most nations plan to reduce carbon emissions by switching from coal-based to gas-based electricity generation in response to the growing environmental consciousness during the past ten years. The demand for compressors from the oil and gas industry is anticipated to be supported by the potential for natural gas output and consumption for power generation to keep growing. The Energy Institute (EI) estimates that the world produced 4043.8 billion cubic meters of natural gas in 2022, an increase of 15.3% compared to 2015.

- India is expanding its gas pipeline infrastructure to accommodate rising demand. The Indian government announced a pipeline project across several states. For instance, in January 2024, the government launched a gas pipeline project of INR 9,000 crore (USD 1.1 billion) that includes Indian Oil Corporation Ltd's (IOCL) 488-km-long natural gas pipeline and Hindustan Petroleum Corporation Ltd's (HPCL) 697-km-long Petroleum Pipeline (VDPL).

- Similarly, China's government has set a target of net-zero emissions by 2060. Under the country's energy transition strategy, natural gas is intended to play a critical part in lowering CO2 emissions, and it is projected to be the country's major energy source within the next decade.

- Furthermore, the United States Energy Information Administration (EIA) predicts that due to anticipated rises in international demand for natural gas, the US LNG exports are expected to more than double between 2020 and 2029, which is likely to have a positive impact on the compressor market.

- As a result of the factors mentioned above, the oil and gas segment is likely to dominate the compressor market over the forecast period.

Asia-Pacific to Dominate the Market

- Some of the world's top importers and consumers of natural gas are located in the Asia-Pacific region. For energy needs, this region still primarily relies on coal and oil. However, due to increasing concerns about air pollution, there has been a recent trend toward using natural gas more frequently.

- The most significant users of natural gas in the region are the manufacturing and power generation sectors. It is anticipated that rising energy consumption in nations like China and India will propel the market for natural gas.

- Residential gas consumption is predicted to rise due to urbanization and the expansion of the middle class in Asia-Pacific nations. The need for gas compressors is anticipated to increase in the electricity and manufacturing sectors, as well as in the midstream gas industry, due to the rising gas consumption.

- Furthermore, the refinery sector of Asia-Pacific has risen significantly over the last ten years, and compressors like centrifugal compressors are vitally used during the refinery process. According to Statistical Review of World Energy Data, in 2022, the refinery capacity of the Asia-Pacific region was 36,189 thousand barrels daily, increased by 8.9% compared to 2013. The number is expected to rise significantly over the forecast period as serval projects are going to start in the upcoming years.

- China intends to increase the proportion of clean fuel in its energy mix by strengthening its network of natural gas and oil pipelines over the next ten years. The nation's network of gas and oil pipelines is anticipated to grow to 240,000 km by 2025, according to the National Development and Reform Commission. The natural gas pipes are anticipated to cover 123,000 km of the 240,000 km. Since compressors are among the most frequently utilized pieces of machinery that power long-distance natural gas pipelines, the demand for compressors is anticipated to rise throughout the projected period as the pipeline network expands

- Similarly, India is investing significantly in the petrochemical sector, which is anticipated to create a rising demand for compressors. For instance, in December 2023, the government of India signed 11 MoUs worth INR 67,000 crore (USD 8.3 billion) at a pre-Vibrant Gujarat Global Summit event in the state of Gujarat for the Chemical and Petrochemicals Industry. Investments in the petrochemical sector is anticipated to rise exponentially over the region during the forecast period and significantly raise the demand for compressors across the industry.

- Due to these factors, Asia-Pacific is expected to dominate the compressor market during the forecast period.

Compressor Industry Overview

The compressor market is fragmented. Some key players in this market (in no particular order) include Atlas Copco AB, Baker Hughes Co., Ingersoll-Rand Inc., Siemens Energy AG, and Sulzer Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Market Drivers

- 4.5.1.1 The Growing Demand for Natural Gas

- 4.5.1.2 Rising Pipeline Infrastructure across Globe

- 4.5.2 Market Restraints

- 4.5.2.1 Increasing Adoption of Solar and Wind Energies

- 4.5.1 Market Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By End-User

- 5.1.1 Oil and Gas Industry

- 5.1.2 Power Sector

- 5.1.3 Manufacturing Sector

- 5.1.4 Chemicals and Petrochemical Industry

- 5.1.5 Other End-Users

- 5.2 By Type

- 5.2.1 Positive Displacement

- 5.2.2 Dynamic

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 Norway

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 NORDIC

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Thailand

- 5.3.3.5 Australia

- 5.3.3.6 Indonesia

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Aerzener Maschinenfabrik GmbH

- 6.3.2 Ariel Corporation

- 6.3.3 Atlas Copco AB

- 6.3.4 Baker Hughes Co.

- 6.3.5 Bauer Compressors Inc.

- 6.3.6 Burckhardt Compression Holding AG

- 6.3.7 Ebara Corporation

- 6.3.8 Ingersoll Rand Inc

- 6.3.9 Siemens Energy AG

- 6.3.10 Sulzer Ltd

- 6.4 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Several Compressor Manufacturers are Making Strides to Develop More Energy-Efficient Products