|

|

市場調査レポート

商品コード

1689806

超純水:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Ultra-pure Water - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 超純水:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

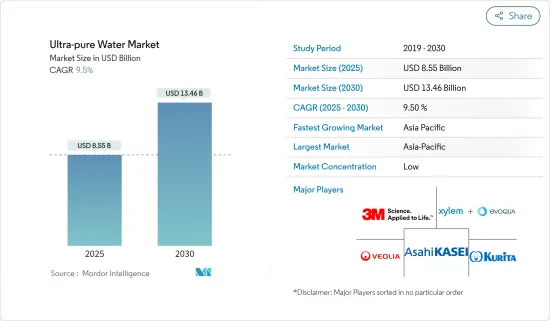

超純水市場規模は2025年に85億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.5%で、2030年には134億6,000万米ドルに達すると予測されています。

COVID-19の大流行により、超純水の需要は一部の産業で減少しました。しかし、製薬産業では超純水の用途が増加しています。パンデミック後は、半導体、医薬品、発電など様々な産業で超純水の需要が大幅に増加しています。

主要ハイライト

- 短期的には、半導体産業と製薬産業の需要増加が市場成長の原動力になりそうです。

- 限られた汚染された水資源しか利用できないことが、市場成長の妨げになると予想されます。

- グリーン水素製造における超純水の需要は、2024~2029年にかけて有利な成長機会を生み出す可能性が高いです。

- アジア太平洋が市場を独占し、2024~2029年にかけて最も高いCAGRで推移すると予想されます。

超純水市場動向

半導体セグメントが市場を独占する見込み

- 超純水(UPW)は半導体産業で重要な役割を果たしています。水中のわずかな不純物でも半導体部品の性能や信頼性に影響を与えるからです。ウエハーの初期洗浄から半導体・マイクロエレクトロニクス部品の最終製造まで使用されます。

- 半導体産業は、様々なエンドユーザー産業からの高い需要により、近年活況を呈しています。半導体産業協会(SIA)によると、半導体製造能力に対する世界需要は2030年までに56%増加すると予想されています。

- 半導体産業協会(SIA)によると、2024年1月の半導体売上高は前年同期比で15%近く増加しました。

- さまざまな用途からの半導体需要の増加を考慮し、数カ国の政府は需要を満たし、世界の競争の最前線に立ち続けるために、さまざまな施策を発表しています。

- 北米では、米国が2022年8月にCHIPS and Science Actを立ち上げ、半導体産業の国内生産と技術革新を支援しています。

- 同政府は、チップ製造インセンティブと研究投資に520億米ドルを投資すると発表しました。これには半導体・装置製造に対する投資税額控除も含まれます。

- さらにアジア太平洋では、インド政府が2024~25年予算でディスプレイと半導体の製造に690億3,000万インドルピー(約8億3,256万米ドル)を割り当てました。

- さらに2023年、中国は米国を含む他の半導体生産国に追いつくため、半導体セクタのために約400億米ドルを調達する新たな国営投資ファンドを計画していると発表しました。

- しかし、半導体産業協会によると、2023年の世界の半導体産業売上高は5,268億米ドルで、2022年の5,741億米ドルに比べ8.2%減少しました。

- さまざまな政府が半導体産業を支援しているが、売上高の減少は市場の成長にマイナスの影響を与えそうです。

アジア太平洋が市場を独占する見込み

- 2024~2030年にかけて、アジア太平洋が超純水市場を独占すると予想されます。中国、インド、日本などの国々の需要が高いため、超純水市場は拡大しています。

- 中国は半導体チップの純輸入国であり、使用される半導体の20%以下しか製造していないです。広範な需要シナリオから利益を得るため、中国は「メイドイン・チャイナ2025」計画のような戦略的イニシアチブに着手しています。この計画の下、中国政府は2030年までに生産高3,050億米ドルを達成し、国内需要の80%を満たすという目標を発表しています。

- さらに、マイクロチップ技術は2023年7月、インドでの事業拡大に約3億米ドルを投資する複数年計画を発表しました。この投資は、同国の半導体生産能力の向上に貢献すると考えられます。

- さらに、中国の製薬産業は世界最大級の規模を誇っています。同国はジェネリック医薬品、治療、原薬、漢方薬の生産に携わっています。

- 2024年3月、デンマークの製薬会社Novo Nordiskは、中国の天津にある施設の無菌製剤拡大プロジェクトに5億5,600万米ドルを投資すると発表しました。このプロジェクトは2027年までに完了する予定で、同社の生産能力を高めると同時に、医薬品の現地生産をサポートします。

- さらに、インド政府は、生産連動奨励金制度を通じて、インドの医薬品部門への投資と生産を増加させ、2022~2023~2027~2028年までの6年間で2兆9,400億インドルピー(約373億3,800万米ドル)の売上増を見込んでいます。

- 日本は、2030年までに電力の20~22%を原子力から供給することを目標としており、稼働可能な原子炉は33基です。2013年以降、再稼働のための新規制要件を満たした原子炉は10基のみで、高浜原発は12年の中断を経て2023年7月に再稼働しました。

- したがって、半導体産業や製薬産業への投資の増加に伴い、超純水の需要は2024~2029年にかけて増加する可能性が高いです。

超純水産業概要

超純水市場は細分化されています。同市場の主要企業は、(順不同)ヴェオリア、Evoqua Water Technologies LLC、Kurita Water Industries Ltd、Asahi Kasei Corp.、3Mです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 半導体産業からの需要増加

- 製薬産業の成長

- 抑制要因

- 限られた汚染された水資源の利用可能性

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途

- 洗浄

- エッチング

- 成分

- その他の用途(高速液体クロマトグラフィー(HPLC)と免疫化学)

- エンドユーザー産業

- 半導体

- 医薬品

- 発電

- その他のエンドユーザー産業(飲食品、石油・ガス、パーソナルケア産業)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Applied Membranes Inc.

- Asahi Kasei Corporation

- Dupont

- ECOLAB

- Evoqua Water Technologies LLC

- Komal Industries

- Kurita Water Industries Ltd

- Organo Corporation

- Ovivo

- Pentair

- Rodi Systems Corporation

- Veolia

第7章 市場機会と今後の動向

- グリーン水素製造における超純水の必要性

The Ultra-pure Water Market size is estimated at USD 8.55 billion in 2025, and is expected to reach USD 13.46 billion by 2030, at a CAGR of 9.5% during the forecast period (2025-2030).

The demand for ultrapure water decreased in a few industries due to the COVID-19 pandemic. However, the application of ultrapure water has increased in the pharmaceutical industry. Post-pandemic, the demand for ultrapure water has increased significantly in various industries, including semiconductors, pharmaceuticals, and power generation.

Key Highlights

- In the short term, growing demand from the semiconductor industry and the rising pharmaceutical industry are likely to drive market growth.

- The availability of limited and polluted water resources is expected to hinder the market's growth.

- Nevertheless, the requirement for ultrapure water in green hydrogen production is likely to create lucrative growth opportunities between 2024 and 2029.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR from 2024 to 2029.

Ultra-pure Water Market Trends

The Semiconductor Segment is Expected to Dominate the Market

- Ultrapure water (UPW) plays a crucial role in the semiconductor industry, as even the smallest impurity in the water can affect the performance and reliability of these components. It is used from the initial cleaning of wafers to the final fabrication of semiconductor and microelectronics components.

- The semiconductor industry has been witnessing a boom in recent years due to high demand from various end-user industries. According to the Semiconductor Industry Association (SIA), the global demand for semiconductor manufacturing capacity is expected to increase by 56% by 2030.

- According to the Semiconductor Industry Association (SIA), the sales of semiconductors in January 2024 increased by almost 15% compared to the same period last year.

- Considering the increasing demand for semiconductors from various applications, governments across several countries have announced various policies to meet the demand and stay at the forefront of the global competition.

- In North America, the United States launched the CHIPS and Science Act in August 2022 to support domestic production and innovation in the semiconductor industry.

- The government announced an investment of USD 52 billion in chip manufacturing incentives and research investments. This also includes an investment tax credit for semiconductor and equipment manufacturing.

- Further, in Asia-Pacific, the government of India has allocated INR 6,903 crore (~USD 832.56 million) in Budget 2024-25 for the manufacturing of displays and semiconductors.

- Additionally, in 2023, China announced that to catch up with other semiconductor-producing countries, including the United States, a new state-backed investment fund is planned to raise about USD 40 billion for its semiconductor sector.

- However, according to the Semiconductor Industry Association, in 2023, the global semiconductor industry sales totaled USD 526.8 billion, with a decline of 8.2% compared to the total of USD 574.1 billion in 2022.

- Although various governments support the semiconductor industry, the decrease in sales is likely to impact the market's growth negatively.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the ultrapure water market between 2024 and 2030. Due to the high demand from countries like China, India, and Japan, the market for ultrapure water has been growing.

- China is the net importer of semiconductor chips, with China manufacturing less than 20% of semiconductors used. To benefit from the extensive demand scenario, China has embarked on strategic initiatives, like the Made in China 2025 plan, under which the Chinese government has announced its goal to reach an output of USD 305 billion by 2030 and, therefore, meet 80% of its domestic demand.

- Additionally, in July 2023, Microchip Technology announced a multi-year plan to invest approximately USD 300 million in expanding its operations in India. The investment is likely to help to increase the country's production capacity of semiconductors.

- Further, the pharmaceutical industry in China is one of the largest in the world. The country is involved in producing generics, therapeutic medicines, active pharmaceutical ingredients, and traditional Chinese medicine.

- In March 2024, Novo Nordisk, a Danish pharmaceutical company, announced a USD 556 million investment in a sterile preparation expansion project at its facility in Tianjin, China. The project is expected to be completed by 2027 and will support localized drug production while boosting the company's production capacity.

- In addition, through the Production Linked Incentive scheme, the Government of India hopes to increase investment and production in the Indian pharmaceutical sector, expecting to generate incremental sales of INR 2,94,000 crore (~USD 37,338 million) in 6 years from 2022-2023 to 2027-2028.

- Japan targets supplying 20-22% of electricity by 2030 from nuclear power, with 33 operable reactors. Since 2013, only ten reactors have met new regulatory requirements for restart, with Takahama Nuclear Power Plant resuming operations in July 2023 after a 12-year hiatus.

- Therefore, with the increasing investments in the semiconductor and pharmaceutical industry, the demand for ultrapure water is likely to increase between 2024 and 2029.

Ultra-pure Water Industry Overview

The ultrapure water market is fragmented in nature. Major players in the market are (not in any particular order) Veolia, Evoqua Water Technologies LLC, Kurita Water Industries Ltd, Asahi Kasei Corporation, and 3M.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Semiconductor Industry

- 4.1.2 The Growing Pharmaceutical Industry

- 4.2 Restraints

- 4.2.1 Availability of Limited and Polluted Water Resources

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Cleaning

- 5.1.2 Etching

- 5.1.3 Ingredient

- 5.1.4 Other Applications (High-performance Liquid Chromatography (HPLC) and Immune Chemistry)

- 5.2 End-user Industry

- 5.2.1 Semiconductor

- 5.2.2 Pharmaceuticals

- 5.2.3 Power Generation

- 5.2.4 Other End-user Industries (Food and Beverage, Oil and Gas, and Personal Care Industries)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Applied Membranes Inc.

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Dupont

- 6.4.5 ECOLAB

- 6.4.6 Evoqua Water Technologies LLC

- 6.4.7 Komal Industries

- 6.4.8 Kurita Water Industries Ltd

- 6.4.9 Organo Corporation

- 6.4.10 Ovivo

- 6.4.11 Pentair

- 6.4.12 Rodi Systems Corporation

- 6.4.13 Veolia

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Requirement of Ultrapure Water in Green Hydrogen Production