自動車エンジン管理システム:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Automotive Engine Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日

- 商品コード

- 1523308

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

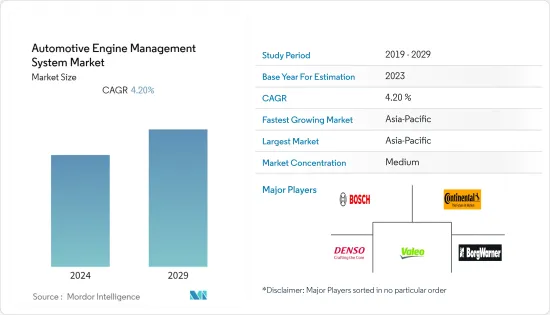

自動車エンジン管理システム市場規模は、2024年に662億米ドルと推定され、2029年には848億米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは4.20%で成長すると予測されます。

長期的には、低燃費車を求める消費者動向の高まりが、エンジン動作を制御する先進コンポーネントの開発をメーカーに促しています。世界の温室効果ガス濃度の上昇により、厳しい排ガス規制の制定が大幅に増加する可能性が高いです。

乗用車の販売と生産の増加に伴い、世界の自動車セクターは年々急激な成長を遂げています。例えば、インドにおける2022-23年度の乗用車販売台数は前年度比14,67,039台から17,47,376台に、実用車は14,89,219台から20,03,718台に、バンは1,13,265台から1,39,020台に増加しています。

自動車需要の増加に伴い、エンジンマネジメント企業は、高い需要に対応するため、製品投入、生産能力拡大、合併などの戦略的な動きを採用しています。

主なハイライト

- 2023年7月、ヴァレオはSanand工場で超音波センサーの生産能力を700万ユニットに拡大しました。サナンドでの最初の生産ラインは2021年11月に開始されました。この追加ラインにより、総生産能力は年間300万ユニットから700万ユニットに増加しました。

- 2023年1月、センサータは自動車および大型車両オフロード(HVOR)アプリケーション向けの幅広いミッションクリティカルなセンサと電気保護ソリューションを展示しました。

北米は世界で最も急速に成長している自動車用エンジンマネジメントシステム市場です。しかし、特に中国とインドでの自動車販売台数が多いため、アジア太平洋地域の自動車エンジンマネジメントシステムが大きな市場シェアを占めています。インドと中国の顧客は、自動車の性能向上に対する意識が高まっており、これが自動車エンジンマネジメントシステム市場を押し上げると予想されます。

自動車エンジンマネジメントシステム市場動向

乗用車が最も高い市場シェアを占める

乗用車は、そのスタイリッシュでコンパクトなデザインと経済的価値などの特徴から、消費者の間で非常に人気があります。乗用車の需要増加は、中流階級の人口増加や新興国における生活水準の向上も影響しています。

スポーツ用多目的車(SUV)の需要増加は、インドにおける乗用車販売の50%以上をスポーツ用多目的車の販売が占めているため、市場プレーヤーにとって収益機会を生み出しています。インドや中国のような国々では、地上高の高い大型車を好むなど、さまざまな要因からスポーツ用多目的車の需要が急増しました。

さらに、税制補助金や充電器インフラの拡充による電気自動車需要の増加も、市場の成長をもたらしました。インドにおける2023年第1四半期の電気自動車販売台数は、2022年同時期の2倍に達しました。

国際クリーン交通評議会によると、米国における電気自動車の販売台数は100万台を超えました。特に、2023年第1~3四半期までの販売台数は、2022年同期比で約58%増加しました。

乗用車セグメントの成長に伴い、電子制御ユニットやエンジンセンサーなどの各種エンジン管理システムの需要は今後も飛躍的に伸びると予想されます。安全性と利便性に関連する先進的な機能の動向の進行に伴い、自動車の機能搭載が進んでいます。さらに、自律走行車や電気自動車に対する需要の高まりは、エンジンマネジメントシステムに新たな機会をもたらすと予想されます。

企業もまた、市場の高い需要に対応するため、技術的に高度な製品を生み出し、生産能力を拡大することに注力しています。例えば、2023年6月、MEMSベースのソリッドステート車載ライダーとADAS(先進運転支援システム)ソリューションのリーダーであるMicroVision Inc.は、ソリッドステートフラッシュベースのMOVIAライダーセンサーを発売しました。MOVIAセンサーは小型で軽量であるため、さまざまな用途に適しています。

アジア太平洋地域が最も高い市場シェアを占める

予測期間中、アジア太平洋地域が主要な市場シェアを占めると予想されます。この地域の成長は、主にインド、中国、日本などの自動車生産上位国が牽引しています。

その他の促進要因としては、運転体験の向上、快適性、安全性を提供する自動車に対する需要の増加、低燃費エンジンに対する需要の増加などが挙げられます。インドのような国では、厳しい規制、補助金、税額控除、その他の優遇措置を通じてエンジン管理システムの採用を推進しているため、電気自動車の販売が増加していることが、エンジン管理システムの使用をさらに後押ししています。

- インドの道路交通高速道路省(MoRTH)は、自動車の燃費効率を高めるため、2023年から燃費基準への適合を義務化しました。フレックス燃料車に関する新ガイドラインは、内燃機関車の成長に寄与しています。

- 中国は、燃料ポンプとインジェクターを供給するエンジンマネージメントシステム(EMS)分野で世界市場シェアをリードしています。ディーゼルエンジンの新しい排ガス規制は、中国のエンジン管理会社にとってさらなるビジネスチャンスを意味する可能性があります。

従来のICエンジン車とは別に、電気自動車の需要が市場の成長を後押しすると予想されます。各地域で排ガス規制が厳しくなっているため、予測期間中に電気自動車の需要が増加する可能性が高いです。International Council of Clean Transportationによると、中国は世界最大のEV市場であり続け、2023年上半期には約300万台のEVが販売されました。

- 2024年1月現在、中国メーカーは自律走行技術のライダー革新で主導権を握り続けており、2000年以降、ライダー関連の特許出願件数は25,957件と驚異的で、米国企業や日本企業を上回っています。

自動車用エンジンマネジメントシステム産業の概要

自動車エンジンマネジメントシステム市場は、世界的および地域的に確立されたプレーヤーによって統合され、主導されています。各社は、新製品投入、提携、合併などの戦略を採用し、市場での地位を維持しています。

- 例えば、TTTech Autoは2023年4月、高度なネットワーク機能を備えた高性能ECU、N4 Network Controllerを発売しました。N4は、最新の自動車E/Eアーキテクチャで中心的な役割を果たすよう設計されており、ソフトウェア定義の自動車への道を開く。

同市場の主要企業には、コンチネンタルAG、株式会社デンソー、株式会社ヴァレオ、ロバート・ボッシュGmbHなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 乗用車販売の増加

- 市場抑制要因

- 安全装備の追加による車両コストの上昇

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 自動車タイプ別

- 乗用車

- 商用車

- コンポーネントタイプ別

- エンジン制御ユニット(ECU)

- エンジンセンサー

- 燃料ポンプ

- その他のコンポーネントタイプ

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Robert Bosch GmbH

- Continental AG

- BorgWarner Inc.

- DENSO Corporation

- Hella KGaA Hueck & Co.

- Infineon Technologies AG

- Sensata Technologies

- Mobiletron Electronics Co. Ltd

- NGK Spark Plugs Pvt Ltd.

- Hitachi Automotive Systems Ltd

- Dover Corporation

第7章 市場機会と今後の動向

目次

The Automotive Engine Management System Market size is estimated at USD 66.20 billion in 2024, and is expected to reach USD 84.80 billion by 2029, growing at a CAGR of 4.20% during the forecast period (2024-2029).

Over the long term, the growing consumer trend toward fuel-efficient vehicles has encouraged manufacturers to develop advanced components that control engine operation. The enactment of stringent emission norms is likely to increase significantly due to the rise in greenhouse gas levels globally.

With the growth in sales and production of passenger cars, the global automotive sector has been witnessing exponential growth year on year. For instance, the sales of passenger cars in India increased from 14,67,039 to 17,47,376, utility vehicles from 14,89,219 to 20,03,718, and vans from 1,13,265 to 1,39,020 units in FY 2022-23, compared to the previous year.

With the growth in demand for vehicles, engine management companies are adopting strategic moves such as product launches, capacity expansion, and mergers to cater to the high demand.

Key Highlights

- In July 2023, Valeo expanded its ultrasonic sensor manufacturing capacity to 7 million units at the Sanand plant. The first production line at Sanand was started in November 2021. With this additional line, the total production capacity increased from 3 million to 7 million units annually.

- In January 2023, Sensata showcased its broad range of mission-critical sensors and electrical protection solutions for automotive and heavy vehicle off-road (HVOR) applications.

North America is the fastest automotive engine management systems market in the world. However, due to the more significant automotive sales, especially in China and India, the automotive engine management systems in Asia-Pacific hold the major market share. Customers in India and China are becoming more aware of enhancing their vehicles' performance, which is expected to boost the automotive engine management system market.

Automotive Engine Management System Market Trends

Passenger Cars Holds Highest Market Share

Passenger cars have become exceptionally popular among consumers due to features like their stylish and compact design and economic value. The rise in the demand for passenger cars is also influenced by the increasing middle-class population and the enhanced standard of living in emerging countries.

The rise in demand for sports utility vehicles (SUVs) creates profitable opportunities for market players as the sale of sports utility vehicles accounts for more than 50% of passenger car sales in India. The demand for sports utility vehicles in countries like India and China surged due to various factors, such as buying preference for bigger cars with high ground clearance.

Furthermore, the increase in demand for electric vehicles due to tax subsidies and expansion in charger infrastructure also resulted in the growth of the market. Electric car sales in India in the first quarter of 2023 were double what they were in the same period in 2022.

According to the International Council of Clean Transportation, the sales of electric vehicles in the United States crossed 1 million. Notably, the sales through the first three quarters of 2023 were about 58% higher than the same period in 2022.

With the growth in the passenger car segment, demand for various engine management systems, such as electronic control units and engine sensors, is expected to continue to grow exponentially in the future. With the ongoing trend of advanced features related to safety and convenience, cars are becoming more feature-loaded. Moreover, the rise in demand for autonomous and electric vehicles is anticipated to create new opportunities for engine management systems.

Companies are also focusing on creating technologically advanced products and expanding their capacity to cater to the high demand in the market. For example, in June 2023, MicroVision Inc., a leader in MEMS-based solid-state automotive lidar and advanced driver-assistance systems (ADAS) solutions, launched its solid-state flash-based MOVIA lidar sensor. The small form factor and light weight of the MOVIA sensor make it appealing for a wide variety of applications.

Asia-Pacific Holds the Highest Market Share

Asia-Pacific is expected to hold a major market share during the forecast period. The regional growth is mainly driven by the top-producing automotive countries like India, China, and Japan.

Other driving factors include the increase in demand for automobiles that provide enhanced driving experiences, comfort, and safety and an increase in demand for fuel-efficient engines. The rise in the sale of electric vehicles has further boosted the use of engine management systems, as countries like India are promoting their adoption through strict regulations, subsidies, tax credits, and other incentives.

- The Ministry of Road Transport and Highways (MoRTH) in India made it mandatory for vehicles to comply with fuel consumption standards from 2023 to make vehicles fuel efficient. The new guidelines on flex-fuel vehicles contribute to the growth of ICE engines.

- China is leading the global market share in the engine management system (EMS) segment, supplying fuel pumps and injectors. New emission norms for diesel engines could mean additional opportunities for Chinese engine management companies.

Apart from conventional IC engine vehicles, the demand for electric vehicles is anticipated to boost the growth of the market. With stringent emission regulations across every region, the demand for electric vehicles is likely to increase during the forecast period. According to the International Council of Clean Transportation, China remained the world's largest EV market, with approximately 3 million EVs sold in 2023 H1.

- As of January 2024, Chinese manufacturers continue to lead the charge in lidar innovation of autonomous driving technology and have filed a staggering 25,957 patent applications related to lidar since 2000, surpassing American and Japanese companies.

Automotive Engine Management System Industry Overview

The automotive engine management system market is consolidated and led by globally and regionally established players. The companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions.

- For instance, in April 2023, TTTech Auto launched the N4 Network Controller, a high-performance ECU with advanced networking capabilities. The N4 is designed to play a central role in modern automotive E/E architectures, paving the way to software-defined vehicles.

Some of the major players in the market include Continental AG, DENSO Corporation, DENSO Corporation, Valeo, and Robert Bosch GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Increase in Sales of Passenger Cars

- 4.3 Market Restraints

- 4.4 Increased Cost of Vehicles Due to Additional Safety Features

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Billion)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Commercial Vehicle

- 5.2 By Component Type

- 5.2.1 Engine Control Unit (ECU)

- 5.2.2 Engine Sensors

- 5.2.3 Fuel Pump

- 5.2.4 Other Component Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Robert Bosch GmbH

- 6.2.2 Continental AG

- 6.2.3 BorgWarner Inc.

- 6.2.4 DENSO Corporation

- 6.2.5 Hella KGaA Hueck & Co.

- 6.2.6 Infineon Technologies AG

- 6.2.7 Sensata Technologies

- 6.2.8 Mobiletron Electronics Co. Ltd

- 6.2.9 NGK Spark Plugs Pvt Ltd.

- 6.2.10 Hitachi Automotive Systems Ltd

- 6.2.11 Dover Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日