|

市場調査レポート

商品コード

1521890

産業用金属包装:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Industrial Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用金属包装:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

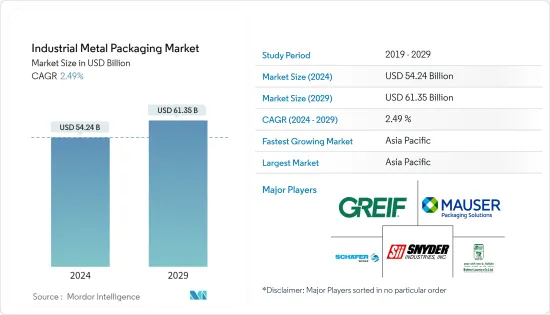

産業用金属包装市場規模は2024年に542億4,000万米ドルと推定され、2029年には613億5,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは2.49%で成長します。

主要ハイライト

- 金属製バルクコンテナ、特にスチールとアルミニウムで構成されたコンテナは、卓越した耐久性と保護を提供するため、製品の完全性を最優先する産業に好まれるコンテナとなっています。また、新興経済諸国を中心とした世界の景気拡大と産業化の継続は、産業用潤滑油と流体の需要を刺激すると予想されます。その結果、頑丈な包装ソリューションに対する需要が増加し、金属包装が大幅な成長を遂げることになります。

- 製品出荷中、包装は定期的にトルク力、外圧・内圧、極端な温度、その他の悪条件にさらされることを考慮することが重要です。スチールの機械的性能には、高い強度と耐高圧性が含まれ、簡単に損傷することはありません。そのため、包装された製品の安全性が確保され、保管、輸送、取り扱い、使用が容易になります。

- スチールドラムは、石油産業で使用される低粘度の液体やその他の危険な化学物質を保管する安全な方法であり、プラスチックドラムはスチールドラムに劣る。効率的な消火システムとともに使用される場合、回収タイプのスチールドラムは高温火災に対して最高の防御力を発揮します。このようなユニークな特性は、石油・潤滑油セクターの産業用ドラム缶を牽引すると予想されます。

- 加えて、生産性の上昇、輸入、石油輸出は国際貿易の成長をもたらし、産業用金属包装の需要を潜在的に増加させる。様々なエンドユーザー産業からの化学品と石油潤滑油の市場の上昇と、サプライチェーン能力の強化への大きな焦点は、産業用金属包装のニーズを促進すると予想されます。

- 産業用包装の情勢は、持続可能性への配慮に煽られた輸送と出荷において大きな変貌を遂げつつあり、スチール製中間バルクコンテナ(IBC)が重要な位置を占めています。スチール製IBCは、堅牢性や再利用性といった固有の特性により、その寿命を通じて環境への影響を大幅に削減するため、環境に責任のある包装を示しています。

産業用金属包装市場の動向

液体輸送用バルク容器包装ソリューションへの需要の高まり

- IBCとドラム缶は、産業用と非産業用製品のバルク包装ソリューションまたは輸送容器です。これらのソリューションは、危険物や非危険物の液体・半液体製品を大量に保管・輸送するために設計されています。IBCのようなバルク包装ソリューションは、梱包された製品に最適な衛生環境を提供し、流出の可能性を減らすことができるため、広く普及しています。

- 化学、製薬、食品、飲料の各企業は、製品輸送用に高品質で信頼性の高いバルク容器を求めており、ドラム缶やIBCなどの産業用金属製包装ソリューションに新たな機会が生まれています。ドラム缶メーカーやIBCメーカーは、国境を越えた輸送が持続可能性と環境に優しい包装に焦点を当て、バルク容器への需要が高まるにつれて変化する市場に遭遇しています。

- ITP包装が実施した調査によると、スチールドラムは汎用性が高く、長持ちし、コスト効率の高い産業用ドラム缶の形態で、多くの産業で複数の用途に使用されています。スチールドラムは輸送・物流業界の主力です。また、スチールドラムには、物流業界の燃料となるガソリンやディーゼルが保管され、業界を動かしています。

- 中間バルクコンテナ(IBC)は、その耐久性、汎用性、費用対効果の高さから、産業用化学品の梱包や輸送によく利用されています。IBCは、輸送や取り扱いの際に遭遇する過酷な条件にも耐えられるように設計されています。米国化学産業協会(American Chemistry Council)によると、2021~2022年の化学品出荷額は5兆655億米ドル、2022~2023年には5兆7,214億米ドルに達し、世界の化学品出荷額は大幅に急増しました。化学品生産高の前年比成長率は、2023年が0.6%だったのに対し、2024年は3.5%になると予測されています。このような化学品出荷の増加は、予測期間中のドラム缶とIBCの市場を牽引すると考えられます。

- 成長する石油化学産業は、製品を保護するために安全な包装ソリューションを必要としています。また、新興市場における塗料や潤滑油の生産量の増加や、製品の安全なサプライチェーンと輸送に対する需要の高まりも、需要を牽引すると予想されます。エンドユーザー産業の生産への投資の増加は、産業用スチールドラム市場に大きな成長機会をもたらすと考えられます。そのため、金属製ドラム缶は、その相対的な再利用可能性と危険物輸送の安全性に対する評判により、引き続き広く使用されるであろう。

危険物の国内生産の増加と原材料の入手可能性がアジア太平洋の市場成長を助ける

- 金属製包装は、その耐久性と外力に対する耐性により、危険物貯蔵に理想的なソリューションです。金属ドラムは衝撃による穴あけから優れた保護を提供し、紫外線(UV)放射にも耐性があるため、屋外保管に適しています。マテリアルハンドリングは、注意深く管理・取り扱いを行わないと脅威をもたらす可能性があります。

- 化学製品を効果的に封入することで、流出、爆発、腐食のリスクを軽減することができます。危険物包装は、化学と製薬産業で広く使用されている化学物質の保護ソリューションを記載しています。

- インドの化学産業は、需要の増加と政府の有利な政策により繁栄しています。インドは化学生産国として独自の地位を誇っています。インド政府は、国内製造と輸出を促進するため、化学・石油化学部門に生産連動奨励金(PLI)制度を設立しました。この制度は、国内での製品販売の増加に基づいて企業にインセンティブを与えるものです。

- 2023~2024年度連邦予算において、中央政府は化学・石油化学省に2,093万米ドルを割り当てた。この配分は、化学部門を支援し、さらに発展させるという政府のコミットメントを浮き彫りにしています。化学産業からのこのような需要の増加は、予測期間中に危険物の産業用金属包装市場を牽引すると考えられます。

- 同地域では鉄鋼などの原材料が入手可能なため、包装メーカーにメリットがあります。India Brand Equity Foundationによると、インドの鉄鋼セクターは大きく成長しています。23年度の粗鋼生産量は125.32トン、完成鋼生産量は121.29トンでした。

- 危険物の輸送は、資産の損失を最小限に抑え、すべての法的コンテナ遵守要件を監視するために、綿密に管理する必要があります。IBCの電子タグ付けは、産業用物質のトレーサビリティーを容易にすると予測されており、メーカーはIBCの紛失や破損によるコストを削減する必要があります。IBCは、ドラム缶に比べて保管コストが低く、大量に液体を輸送するために使用されます。ドラム缶の丸い形態は十分な未使用スペースを形成するが、IBCは効率的なスペース利用を保証します。また、金属包装の使い勝手は何度も使用できるため、市場の成長を促進します。

産業用金属包装業界概要

産業用金属包装市場は、様々な世界企業やローカル企業が様々なエンドユーザー産業向けに様々な製品ポートフォリオを提供しているため、セグメント化されています。同市場で事業を展開する主要企業には、Greif Inc.、Mauser Packaging Solutions、Balmer Lawrie &、Snyder Industries Inc.、SCHAFER Werke GmbH、Time Mauser Industries Pvt. Ltd.などがあります。参入企業は、市場での足跡を拡大し、能力を強化するために戦略的買収に参入しています。

2024年5月、Mauser Packaging Solutionsは、スチールペール缶、錫鋼製一般ライン、衛生缶、エアゾール缶を製造するメキシコの会社Taenza SA de CVの買収を発表しました。この買収により、同社はメキシコにおける製造能力とプレゼンスを強化することになります。

2023年5月、ENVASES OHRINGEN GMBHは、スペインとオランダで食品と産業製品の金属包装を製造するDomiberia Groupの買収を発表しました。これにより、ENVASES OHRINGEN GMBHは欧州における地理的範囲を拡大します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 地政学的シナリオが市場に与える影響

第5章 市場力学

- 市場促進要因

- 液体輸送用バルク容器包装ソリューションの需要拡大

- 危険物貯蔵用金属包装の技術革新

- 市場抑制要因

- プラスチックドラムなどの代替包装ソリューションの存在

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- 製品タイプ別

- IBC類

- 輸送用バレルとドラム

- バルク容器(ペール缶、樽など)

- エンドユーザー産業別

- 飲食品

- 化学・医薬品

- 石油・石油化学

- 建築・建設

- 自動車

- 地域*別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- アジア

- 中国

- インド

- 日本

- タイ

- ベトナム

- オーストラリアとニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- エジプト

- アラブ首長国連邦

- 北米

第7章 競合情勢

- 企業プロファイル

- Greif Inc.

- Mauser Packaging Solutions

- Balmer Lawrie & Co. Ltd

- ENVASES OHRINGEN GMBH

- SCHAFER Werke GmbH

- Sicagen India Limited

- Time Mauser Industries Pvt. Ltd

- THIELMANN PORTINOX SPAIN SA

- Snyder Industries Inc.

- American Keg Company(BLEFA BEVERAGE SYSTEMS)

- Lancaster Container Inc.

- P. Wilkinson Containers Ltd

- Bison IBC Ltd

- Colep Packaging(RAR Group Company)

- Peninsula Drums

第8章 投資分析

第9章 市場の将来

The Industrial Metal Packaging Market size is estimated at USD 54.24 billion in 2024, and is expected to reach USD 61.35 billion by 2029, growing at a CAGR of 2.49% during the forecast period (2024-2029).

Key Highlights

- Metal bulk containers, particularly those composed of steel and aluminum, provide exceptional durability and protection, making them the preferred container for industries that prioritize product integrity. Also, the continued global expansion and industrialization, especially in developing economies, are expected to stimulate the demand for industrial lubricants and fluids. As a result, there will be an increased demand for sturdy packaging solutions, positioning metal packaging for substantial growth.

- Throughout product shipment, it is important to consider that the package is regularly exposed to torque forces, external and internal pressure, extreme temperatures, and other unfavorable conditions. Steel's mechanical performance includes high strength and high-pressure resistance and cannot be damaged easily. This ensures the safety of packaged products and facilitates storage, transportation, handling, and use.

- The steel drums are a safe way to store low-viscosity fluids and other hazardous chemicals used in the oil industry; plastic drums are inferior to steel drums. When employed with an efficient fire suppression system, steel drums of the retrieving type provide the best protection against high-temperature fires. Such unique properties are expected to drive industrial drums in the petroleum and lubricant sector.

- In addition, the rising productivity, imports, and oil exports result in the growth of international trade, potentially increasing demand for industrial metal packaging. The rise in the market for chemicals and petroleum lubricants from varied end-user industries and a significant focus on strengthening the supply chain capability is expected to drive the need for industrial metal packaging.

- The landscape of industrial packaging is undergoing a profound transformation in transportation and shipping fueled by sustainability considerations, and steel intermediate bulk containers (IBCs) occupy a prominent position. Steel IBCs illustrate environmentally responsible packaging due to their inherent characteristics, such as robustness and reusability, which significantly reduce environmental impact throughout their lifespan.

Industrial Metal Packaging Market Trends

Growing Demand for Bulk Container Packaging Solutions for Liquid Transportation

- IBCs and drums are bulk-packaging solutions or shipping containers for industrial and non-industrial products. These solutions are designed to store and transport large quantities of hazardous and non-hazardous liquid and semi-liquid products. Bulk packaging solutions such as IBCs are gaining wider popularity due to their ability to provide an optimal hygienic environment for packed products and reduce the possibilities of spillage.

- Chemical, pharmaceutical, food, and drink companies seek high-quality and reliable bulk containers for product transportation, creating new opportunities for industrial metal packaging solutions such as drums and IBCs. Drum and IBC manufacturers are encountering a changing market as the demand for bulk containers grows, with cross-border transportation focusing on sustainability and eco-friendly packaging.

- According to a study conducted by ITP Packaging, steel drums are a versatile, long-lasting, cost-effective form of industrial drums with multiple uses across many industries. Steel drums are the mainstay of the transportation and logistics industry. Steel drums also store the petrol and diesel that fuel the logistics industry and keep the industry running in steel drums.

- Intermediate bulk containers (IBCs) are often utilized for packaging and transporting industrial chemicals due to their durability, versatility, and cost-effectiveness. IBCs are designed to withstand harsh conditions encountered during shipping and handling. According to the American Chemistry Council, the value of chemical shipments in 2021-2022 was USD 5,065.5 billion and reached USD 5,721.4 billion in 2022-2023; global chemical shipments experienced a significant surge. The Y-o-Y growth of chemical output is projected to be 3.5% in 2024 compared to 2023, which was 0.6%. Such an increase in chemical shipments would drive the market for drums and IBCs during the forecast period.

- The growing petrochemical industry requires safe packaging solutions to protect its products. Also, the rising production of paints and lubricants in emerging markets and the ever-increasing demand for a secure supply chain and transportation of products are anticipated to drive the demand. Increased investment in end-user industries' production will provide significant growth opportunities for the industrial steel drums market. Therefore, metal drums will remain widely used due to their relative reusability and reputation for safety in transporting hazardous materials.

Increasing Domestic Production of Hazardous Materials and Availability of Raw Materials Aids the Market Growth in the APAC Region

- Metal packaging is an ideal solution for hazardous material storage due to its durability and resistance against external forces. Metal drums provide superior protection from impact puncture and are resistant to ultraviolet (UV) radiation, making them suitable for outdoor storage. Hazardous materials could pose a threat if not managed or handled carefully.

- Effective encapsulation of chemical products reduces the risk of spillage, explosion, and corrosion. Hazardous material packaging offers a protective solution to chemicals extensively used in the chemical and pharmaceutical industries.

- India's chemical industry thrives due to increasing demand and favorable government policies. India boasts a unique position as a chemical producer. The Government of India established a Production Linked Incentive (PLI) scheme for the chemical and petrochemical sector to boost domestic manufacturing and exports. This scheme incentivizes businesses based on increased product sales within the country.

- In the Union Budget 2023-2024, the central government allotted USD 20.93 million to the Department of Chemicals and Petrochemicals. This allocation highlights the government's commitment to support and further develop the chemical sector. Such increased demand from the chemical industry would drive the industrial metal packaging of hazardous materials market during the forecast period.

- The availability of raw materials such as steel in the region benefits the packaging manufacturers. According to the India Brand Equity Foundation, India's steel sector has grown significantly. In FY23, crude and finished steel production stood at 125.32 metric tons and 121.29 metric tons, respectively.

- Shipping hazardous materials must be managed closely to minimize asset loss and monitor all legal container compliance requirements. Electronic tagging of IBCs is forecast to facilitate traceability of industrial substances, which manufacturers need to reduce the cost of lost or damaged IBCs. IBCs are used for the low storage cost and transportation of fluids in bulk quantity compared to drums. The round shape of drums forms ample unused space, while IBCs ensure efficient space utilization. Also, the usability of metal packaging can be used multiple times to drive market growth.

Industrial Metal Packaging Industry Overview

The industrial metal packaging market is fragmented due to various global and local players offering various product portfolios for different end-user industries. The key players operating in the market include Greif Inc., Mauser Packaging Solutions, Balmer Lawrie & Co. Ltd, Snyder Industries Inc., SCHAFER Werke GmbH, and Time Mauser Industries Pvt. Ltd. The players are entering into strategic acquisitions to expand their footprint in the market and strengthen their capabilities.

In May 2024, Mauser Packaging Solutions announced the acquisition of Taenza SA de CV, a company in Mexico that manufactures steel pails, tin-steel general line, sanitary, and aerosol cans. The acquisition would help the company strengthen its manufacturing capability and presence in Mexico.

In May 2023, ENVASES OHRINGEN GMBH announced the acquisition of Domiberia Group, a manufacturer of metal packaging for food and industrial products in Spain and the Netherlands. This will help the company broaden its geographical reach in Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Geopolitical Scenario on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Bulk Container Packaging Solutions for Liquid Transportation

- 5.1.2 Innovation in Metal Packaging for Storage of Hazardous Materials

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions such as Plastic Drums and Others

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminium

- 6.1.2 Steel

- 6.2 By Product Type

- 6.2.1 IBCs

- 6.2.2 Shipping Barrels and Drums

- 6.2.3 Bulk Containers (Pails, Kegs, etc.)

- 6.3 By End-user Industry

- 6.3.1 Food & Beverage

- 6.3.2 Chemicals and Pharmaceuticals

- 6.3.3 Oil and Petrochemicals

- 6.3.4 Building and Construction

- 6.3.5 Automotive

- 6.4 By Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Italy

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Thailand

- 6.4.3.5 Vietnam

- 6.4.3.6 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Argentina

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 South Africa

- 6.4.5.3 Egypt

- 6.4.5.4 United Arab Emirates

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Greif Inc.

- 7.1.2 Mauser Packaging Solutions

- 7.1.3 Balmer Lawrie & Co. Ltd

- 7.1.4 ENVASES OHRINGEN GMBH

- 7.1.5 SCHAFER Werke GmbH

- 7.1.6 Sicagen India Limited

- 7.1.7 Time Mauser Industries Pvt. Ltd

- 7.1.8 THIELMANN PORTINOX SPAIN SA

- 7.1.9 Snyder Industries Inc.

- 7.1.10 American Keg Company (BLEFA BEVERAGE SYSTEMS)

- 7.1.11 Lancaster Container Inc.

- 7.1.12 P. Wilkinson Containers Ltd

- 7.1.13 Bison IBC Ltd

- 7.1.14 Colep Packaging (RAR Group Company)

- 7.1.15 Peninsula Drums