|

市場調査レポート

商品コード

1694035

喘息治療薬の市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asthma Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 喘息治療薬の市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 196 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

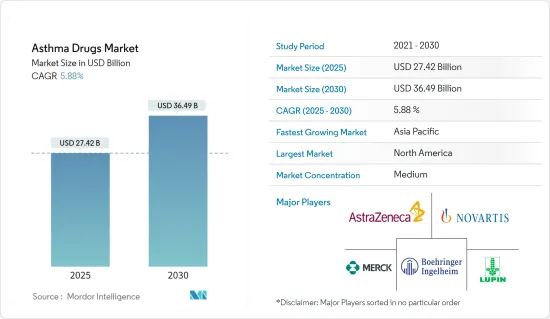

喘息治療薬市場規模は2025年に274億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.88%で、2030年には364億9,000万米ドルに達すると予測されます。

喘息の罹患率や有病率の増加、高齢者の増加、技術の進歩などの要因が、喘息治療薬市場の成長を後押ししています。

喘息の有病率は、大気汚染、職業上の化学品や粉塵、小児期に頻発する下気道感染症、タバコの喫煙、その他の環境要因など、さまざまな理由で世界的に増加しており、これが喘息治療薬市場の成長を後押ししています。世界保健機関(WHO)は、非感染性疾患(NCDs)の予防と制御のための世界行動計画に喘息を含めています。世界喘息デー2023の最新情報によると、喘息の有病率は世界的に増加しており、約3億3,900万人が罹患しています。このことは、世界的に喘息の負担が著しく高いことを示しており、喘息治療薬の需要を押し上げ、予測期間中の市場の成長を促進する可能性が高いです。

世界の喫煙者の増加は、人々の喘息リスクを高めています。例えば、BMC Pulmonary Medicineが2022年4月に発表した紙製によると、喫煙は様々な非伝染性疾患、特に肺がんや喘息などの慢性呼吸器疾患の重大な危険因子として広く認識されています。タバコの煙に含まれる有害な化学品は、呼吸器系に炎症や損傷を引き起こし、喘息を開発したり、既存の症状を悪化させたりする可能性を高めています。そのため、タバコを吸う患者の増加により、その治療のための喘息治療薬の需要が高まっています。

技術の絶え間ない進化、特にバイオマーカーの開発は、市場に大きな機会をもたらすと期待されています。治療効果の遅延や有効性の低下といった従来の治療に内在する限界が、市場を新たな標的治療の革新へと向かわせる。このシフトが市場成長を促進すると予想されます。例えば、2023年1月、AstraZenecaのテズスパイア(テゼペルマブ)は、自己投与用のプレフィルドペンでの使用について、ヒト用医薬品委員会(CHMP)から肯定的意見を得ました。この承認により、12歳以上の重症喘息患者が自己投与できるようになり、治療選択肢の柔軟性と利便性が高まりました。

そのため、喘息患者の増加と技術の進歩が喘息治療薬市場の成長を後押ししています。しかし、製品承認のための厳しい政府規制や薬剤に関連する副作用が市場の成長を抑制しています。

喘息治療薬市場の動向

短時間作用型β2作動薬セグメントは予測期間中に大幅な成長が見込まれる

短時間作用型β2作動薬は気管支拡大薬であり、気道平滑筋細胞を急速に弛緩させて気管支収縮を緩和し、気流を改善します。喘鳴、息切れ、胸部圧迫感、運動誘発性気管支収縮(EIB)などの急性喘息症状を管理するための第一選択治療です。短時間作用型β2アゴニストには、アルブテロール(サルブタモール)とテルブタリンがあり、主に定量吸入器(MDI)やネブライザーを用いて投与されます。

リリーバー療法は、突発的な喘息症状の管理と重症喘息発作の予防に効果的な薬剤療法として重要な役割を果たしています。短時間作用型β作動薬(SABA)は、その作用発現の速さから、迅速な喘息症状の緩和のための有力な選択肢です。定量吸入器(MDI)の携帯性と使いやすさは、その場での症状管理に理想的なソリューションです。この特性は、毎日の吸入コルチコステロイド(ICS)の規則的なレジメンを守るのに苦労している患者にとって特に魅力的です。

2023年10月にWorld Allergy Organization Journalが発表した報告によると、喘息患者における短時間作用型β2作動薬の過剰配合は、即時的な症状緩和のためにこれらの薬にかなり依存していることを示唆しています。このパターンは好ましくない臨床転帰と関連しており、患者の26.7%が過去1年間に少なくとも3本の短時間作用型β2作動薬を投与されており、より重症の喘息や頻繁な増悪と相関しています。

病院、臨床現場、薬局で使用される短時間作用型β2アゴニスト製剤の数は増加しており、予測期間中に大きく成長すると予想されます。より多くの病院やクリニックがこれらの製品を採用するにつれて、このセグメントは今後数年間でかなりの急成長を遂げる可能性が高いです。例えば、2024年1月、AstraZenecaは米国でAIRSUPRA(アルブテロール/ブデソニド)を発売しました。エアスプラは、喘息症状の必要に応じての治療または予防、18歳以上の突然の激しい呼吸障害(喘息発作)の予防を目的として、2023年1月にFDAの承認を取得しました。エアスプラには、気道の平滑筋を弛緩させる短時間作用型β2アゴニストと、肺の炎症を抑える吸入コルチコステロイド(ICS)が含まれています。エアスプラは2つの第III相検査の結果に基づいて承認された:MANDALAとDENALIです。MANDALA検査において、エアスプラは中等症から重症の喘息患者における重症の喘息増悪リスクの減少においてアルブテロールより優れていました。DENALIでは、軽度から中等度の喘息患者において、AIRSUPRAはアルブテロールと比較して気管支拡大の発現が同等でした。

2022年5月、Teva Pharmaceutical Industries Ltd.の米国関連会社であるTeva Pharmaceuticals USA Inc.は、2022年米国胸部学会(ATS)2022年次総会において、プロエアデジヘイラー(アルブテロール硫酸塩)吸入粉末の客観的な患者データに対する独立系専門家のコンセンサスによって確立された短時間作用型β2作動薬の使用に関する新たな知見を発表しました。貯蓄プログラムの拡大、新薬の発売、FDAの承認、発表された臨床所見は、短時間作用型β2アゴニストの利用しやすさと採用の拡大に寄与し、この市場の成長を促進します。

短時間作用型β2作動薬の市場成長は、喘息有病率の増加、これらの薬への過度の依存、費用対効果、併用療法の動向、最近の製品の発売や承認などの要因によって促進され、アクセシビリティと市場導入が強化されています。

北米は喘息治療薬市場全体において大きな成長と市場シェアを維持する見込み

北米の喘息治療薬市場は、喘息の有病率の増加や、臨床検査や製品承認などの喘息治療薬に対する取り組みの増加に伴う喘息治療薬の助成金により成長が見込まれています。強固な医療インフラ、より良い償還施策、資金調達の増加、先進的な喘息治療薬の入手可能性などが北米市場の成長を後押ししています。

北米では、喘息は低所得者、高齢者、黒人、ヒスパニック系、アラスカ先住民に偏って広がっています。これらのグループは喘息罹患率、死亡率、入院率が最も高いです。例えば、米国喘息・アレルギー財団が2023年9月に発表したデータによると、米国では2,700万人以上が喘息でした。これは米国の12人に1人、2,200万人以上に相当します。18歳以上の成人が喘息であり、2022年には18歳以下の約450万人の幼児が喘息でした。喘息の罹患率は、米国の黒人とアメリカ先住民の成人の間で特に高いです。2023年に喘息と診断された成人女性は10.8%、成人男性は6.5%でした。同国では喘息の有病率が高まっており、喘息患者の増加によって効果的な治療・管理ソリューションに対する需要が高まっているため、予測期間中に市場が牽引されるとみられます。同市場は、こうしたハイリスクグループのニーズを満たすため、対象を絞った喘息治療薬の開発と提供に一層注力することで、この動向に対応していくとみられます。

製品の承認や上市など、市場参入企業が採用する戦略は、製品の入手可能性の向上に寄与しており、これが同地域における市場の成長を促進すると予想されます。例えば、Pulmatrixは2023年2月、アレルギー性気管支肺アスペルギルス症(ABPA)と喘息を対象に、最初の患者にPUR1900を投与する第2b相検査を開始しました。この国際共同治験は、喘息患者に革新的な治療法を提供するためのパルマトリックス社とシプラ社との提携の一環として、16週間にわたって薬剤の安全性、忍容性、有効性を評価することを目的としたものです。この検査の概念実証データは2024年半ばまでに得られる予定です。

2022年10月、AstraZenecaとアムジェンは、重症喘息の成人と12歳以上の青少年に対する追加維持療法を適応とするテズスパイア(テゼペルマブ注射剤)のカナダでの発売を発表しました。テズスパイアの承認は、PATHWAY第IIb相検査とNAVIGATOR第III相検査に基づいており、プラセボと併用した場合、重症喘息患者の主要評価項目と主要な副次評価項目において、標準治療と比較して有意な改善が認められました。重症喘息治療薬におけるテズスパイアの有効性が証明されたことから、喘息治療薬に対する需要は増加し、予測期間中の市場の成長を牽引すると予想されます。

喘息の負担と有病率の上昇、喘息治療薬の発売、臨床検査、投資に注力するメーカーなどの要因が、予測期間中の北米の喘息治療薬市場の成長を後押しすると予想されます。

喘息治療薬産業概要

喘息治療薬市場は適度に細分化されています。成長機会のため、喘息治療薬市場には多くの新規参入企業が現れています。今後、主要医薬品の特許切れが予定されており、競争が激化し、特にジェネリック医薬品市場がさらに活性化すると予想されます。市場は大きく成長すると予想され、市場では複数のジェネリック医薬品メーカーが大きなシェアを占めています。市場参入企業の中には、AstraZeneca PLC、Boehringer Ingelheim GmbH、Novartis AG、Sanofi SA、Merck & Co.Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 喘息の発生率と有病率の増加

- 技術の進歩

- 高齢者の増加

- 市場抑制要因

- 製品承認のための厳しい政府規制

- 医薬品に伴う副作用

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 薬剤クラス別

- 気管支拡大薬

- 短時間作用型β2アゴニスト

- 長時間作用型β2アゴニスト

- 抗コリン薬

- 抗炎症薬

- 経口と吸入副腎皮質ステロイド薬

- 抗ロイコトリエン薬

- ホスホジエステラーゼ4型阻害剤

- その他の抗炎症薬

- モノクローナル抗体

- 配合剤

- 気管支拡大薬

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 企業プロファイルと競合情勢

- 企業プロファイル

- AstraZeneca

- Boehringer Ingelheim International GmbH

- Lupin Ltd

- Covis Pharma GmbH

- GSK Plc

- Merck & Co. Inc.

- Viatris Inc.(Mylan NV)

- Novartis AG

- Pfizer Inc.

- Sanofi

- Sumitomo Dainippon Pharma Co. Ltd

- Teva Pharmaceutical Industries Ltd

第7章 市場機会と今後の動向

The Asthma Drugs Market size is estimated at USD 27.42 billion in 2025, and is expected to reach USD 36.49 billion by 2030, at a CAGR of 5.88% during the forecast period (2025-2030).

Factors such as an increase in the incidence and prevalence of asthma, the growing geriatric population, and technological advancements are boosting the growth of the asthma drug market.

The prevalence of asthma is increasing globally due to various reasons, such as air pollution, occupational chemicals and dust, frequent lower respiratory infections during childhood, tobacco smoking, and other environmental factors, which boost the growth of the asthma drug market. World Health Organization (WHO) included asthma in the Global Action Plan for the Prevention and Control of Noncommunicable Diseases (NCDs). As per the latest update on World Asthma Day 2023, the prevalence of asthma is increasing globally, affecting approximately 339 million people. This showed a significantly high burden of asthma globally, likely to boost the demand for asthma drugs and propel the market's growth over the forecast period.

Rising cases of smoking worldwide are increasing the risk of asthma in people. For instance, according to an article published by BMC Pulmonary Medicine in April 2022, smoking was widely recognized as a significant risk factor for various noncommunicable diseases, notably lung cancer and chronic respiratory conditions such as asthma. The harmful chemicals in tobacco smoke can cause inflammation and damage to the respiratory system, increasing the likelihood of developing asthma or exacerbating existing symptoms. Thus, the increasing number of cases of tobacco smoking is raising the demand for asthma drugs for their treatment.

The continuous evolution of technology, particularly in the development of biomarkers, is expected to create significant opportunities for the market. The inherent limitations of conventional treatments, such as delayed therapeutic effects and reduced effectiveness, drive the market toward the innovation of new targeted therapies. This shift is anticipated to fuel market growth. For instance, in January 2023, AstraZeneca's Tezspire (tezepelumab) received a positive opinion from the Committee for Medicinal Products for Human Use (CHMP) for its use in a prefilled pen for self-administration. This approval, which allows patients with severe asthma aged 12 years and older to self-administer the drug, enhances the flexibility and convenience of treatment options.

Therefore, increasing cases of asthma and technological advancements are propelling the growth of the asthma drug market. However, stringent government regulations for product approval and side effects associated with drugs are restraining the market growth.

Asthma Drugs Market Trends

The Short-acting Beta-2 Agonists Segment is Expected to Witness Significant Growth Over the Forecast Period

Short-acting beta-2 agonists are bronchodilators, rapidly relaxing airway smooth muscle cells to relieve bronchoconstriction and improve airflow. They are the first-line treatments for managing acute asthma symptoms such as wheezing, shortness of breath, chest tightness, and exercise-induced bronchoconstriction (EIB). Most used short-acting beta-2 agonists include albuterol (salbutamol) and terbutaline, primarily delivered via metered-dose inhalers (MDIs) or nebulizers.

Reliever therapy plays a critical role in effective medications in managing sudden asthma symptoms and preventing severe asthma attacks. Short-acting beta-agonists (SABAs) are a prominent choice for quick relief due to their rapid onset of action. The portability and user-friendliness of metered-dose inhalers (MDIs) make them an ideal solution for on-the-spot symptom management. This characteristic is especially attractive to patients who struggle to adhere to the regular regimen of daily inhaled corticosteroids (ICS).

According to a report published by the World Allergy Organization Journal in October 2023, the overprescription of short-acting beta-2 agonists among asthma patients suggests a considerable dependency on these medications for immediate symptom relief. This pattern is linked to unfavorable clinical outcomes, with 26.7% of patients receiving at least three canisters of short-acting beta-2 agonists over the past year, correlating with more severe asthma and frequent exacerbations.

The rising number of short-acting beta-2 agonist products used in hospitals, clinical settings, and pharmacies is expected to grow significantly during the forecast period. As more hospitals and clinics adopt these products, the segment will likely experience a considerable growth surge over the coming years. For instance, in January 2024, AstraZeneca launched AIRSUPRA (albuterol/budesonide) in the United States. AIRSUPRA received FDA approval in January 2023 for the as-needed treatment or prevention of asthma symptoms and to help prevent sudden severe breathing problems (asthma attacks) in people aged 18 years and older. Airsupra contains a short-acting beta2-agonist to help relax the smooth muscles of the airways and an inhaled corticosteroid (ICS) to help decrease lung inflammation. Airsupra was approved based on the results from two Phase III trials: MANDALA and DENALI. In MANDALA, AIRSUPRA was superior to albuterol in reducing the risk of severe asthma exacerbations in patients with moderate to severe asthma. In DENALI, AIRSUPRA had a similar onset of bronchodilation compared to albuterol in patients with mild to moderate asthma.

In May 2022, Teva Pharmaceuticals USA Inc., a US affiliate of Teva Pharmaceutical Industries Ltd, published new findings at the 2022 American Thoracic Society (ATS) 2022 Annual Meeting for short-acting beta-2 agonist use established by independent expert consensus to objective patient data from ProAir Digihaler (albuterol sulfate) Inhalation Powder. Expanded savings programs, new medication launches, FDA approvals, and published clinical findings contribute to greater accessibility and adoption of short-acting beta-2 agonists, driving the growth of this market.

The growing market for short-acting beta-2 agonists is driven by factors such as increasing asthma prevalence, over-reliance on these medications, cost-effectiveness, combination therapy trends, and recent product launches and approvals, enhancing accessibility and market adoption.

North America is Expected to Hold Significant Growth and Market Share in the Overall Asthma Drugs Market

The asthma drug market in North America is expected to grow due to the increasing prevalence of asthma and grants of asthma drugs with the increasing number of initiatives for them, such as clinical trials and product approvals. Robust healthcare infrastructure, better reimbursement policies, increased funding, and availability of advanced asthma drugs in the country are boosting the market's growth in North America.

In North America, asthma is spread disproportionately among people with low income, senior adults, and Black, Hispanic, and Alaska Native people. These groups have the highest asthma rates, deaths, and hospitalizations. For instance, as per the data published by the Asthma and Allergy Foundation of America in September 2023, more than 27 million people in the United States had asthma. This corresponded to 1 in 12 people, or more than 22 million people, in the United States. Adults aged 18 and older had asthma; about 4.5 million children under the age of 18 had asthma in 2022. Asthma rates are particularly high among Black and Indigenous American adults in the United States. Additionally, the condition is more prevalent among female adults than male adults; about 10.8% of female adults and 6.5% of male adults were diagnosed with asthma in 2023. The growing prevalence of asthma in the country is expected to drive the market during the forecast period, as the increasing number of individuals with asthma creates a higher demand for effective treatment and management solutions. The market is likely to respond to this trend with a greater focus on developing and delivering targeted asthma treatments to meet the needs of these high-risk groups.

The strategies employed by market players, such as product approvals and launches, are contributing to increased product availability, which is expected to drive the market's growth in the region. For instance, in February 2023, Pulmatrix initiated a Phase 2b trial, with the first patient dosed with PUR1900, targeting Allergic Bronchopulmonary Aspergillosis (ABPA) and asthma. This global trial was intended to evaluate the safety, tolerability, and efficacy of the drug over a 16-week period, forming part of Pulmatrix's partnership with Cipla to deliver innovative therapies for asthma patients. The proof-of-concept data from this study is anticipated by mid-2024.

In October 2022, AstraZeneca and Amgen announced the Canadian availability of Tezspire (tezepelumab injection), which was indicated as an add-on maintenance treatment for adults and adolescents aged 12 and older with severe asthma. The approval of Tezspire was based on the PATHWAY Phase IIb and NAVIGATOR Phase III trials, which showed significant improvements in primary and key secondary endpoints in patients with severe asthma, compared to a placebo, when used alongside standard therapy. Due to Tezspire's proven efficacy in treating severe asthma, the demand for asthma treatments is expected to increase, driving the market's growth over the forecast period.

Factors such as the rising burden and prevalence of asthma, manufacturers focusing on launches, clinical trials, and investments in asthma drugs are expected to boost the growth of the asthma drug market in North America during the forecast period.

Asthma Drugs Industry Overview

The asthma drugs market is moderately fragmented. Due to the growth opportunities, many new players are emerging in the asthma drug market. Forthcoming patent expiries of major drugs are expected to increase competition, further driving the market, especially in the generic sector. The market is expected to grow significantly, with several generic players controlling significant market shares in the developing regions. Some of the market players include AstraZeneca PLC, Boehringer Ingelheim GmbH, Novartis AG, Sanofi SA, and Merck & Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Incidence and Prevalence of Asthma

- 4.2.2 Technological Advancements

- 4.2.3 Growing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Stringent Government Regulations for the Product Approval

- 4.3.2 Side Effects Associated with Drugs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Drug Class

- 5.1.1 Bronchodilators

- 5.1.1.1 Short-acting Beta-2 Agonists

- 5.1.1.2 Long-acting Beta-2 Agonists

- 5.1.1.3 Anticholinergic Agents

- 5.1.2 Anti-inflammatory Drugs

- 5.1.2.1 Oral and Inhaled Corticosteroids

- 5.1.2.2 Anti-leukotrienes

- 5.1.2.3 Phosphodiesterase Type-4 Inhibitors

- 5.1.2.4 Other Anti-inflammatory Drugs

- 5.1.3 Monoclonal Antibodies

- 5.1.4 Combination Drugs

- 5.1.1 Bronchodilators

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPANY PROFILES AND COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AstraZeneca

- 6.1.2 Boehringer Ingelheim International GmbH

- 6.1.3 Lupin Ltd

- 6.1.4 Covis Pharma GmbH

- 6.1.5 GSK Plc

- 6.1.6 Merck & Co. Inc.

- 6.1.7 Viatris Inc. (Mylan NV)

- 6.1.8 Novartis AG

- 6.1.9 Pfizer Inc.

- 6.1.10 Sanofi

- 6.1.11 Sumitomo Dainippon Pharma Co. Ltd

- 6.1.12 Teva Pharmaceutical Industries Ltd