|

市場調査レポート

商品コード

1521717

ペプチドおよびオリゴヌクレオチドCDMO:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Peptide And Oligonucleotide CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ペプチドおよびオリゴヌクレオチドCDMO:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

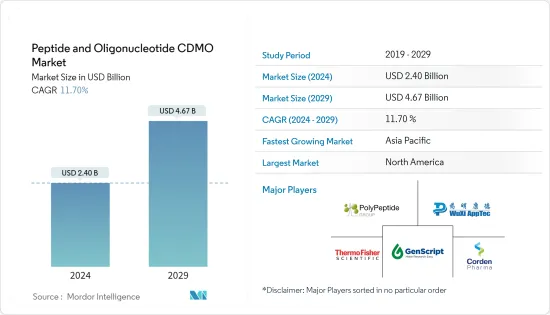

ペプチドおよびオリゴヌクレオチドCDMO市場規模は2024年に24億米ドルと推定・予測され、2029年には46億7,000万米ドルに達し、予測期間中(2024-2029年)のCAGRは11.70%で成長すると予測されます。

市場の動向は、ペプチドおよびオリゴヌクレオチドをベースとした治療薬に対する需要の高まり、ペプチド合成およびオリゴヌクレオチド製造技術の進歩、製薬業界におけるアウトソーシング傾向の高まりによる。ペプチドとオリゴヌクレオチドは、疾患治療により的を絞った個別化アプローチを提供します。ペプチドやオリゴヌクレオチドは、特定の分子標的と相互作用するように設計されており、治療介入の精度を高めています。これらの分子は、がん、遺伝性疾患、代謝性疾患など、さまざまな治療分野で研究されています。例えばオリゴヌクレオチドは、遺伝子変異に対処する可能性があるとして注目を集めています。CDMOは多くの場合、ペプチドやオリゴヌクレオチドを含む特定のタイプの分子の合成・製造に特化しています。彼らの専門知識により、効率的かつ高品質な生産が保証され、治療用分子が要求される基準を満たすことが保証されます。

製薬業界内でのコラボレーションやパートナーシップは、ペプチドおよびオリゴヌクレオチドCDMO市場を大きく押し上げる可能性があります。例えば、2023年5月、PolyPeptide社とNumaferm社は、ペプチドの開発と生産に関するPreferred Partner Collaboration Agreementを締結し、PolyPeptide社のcGMP製造能力、規制に関するノウハウ、市場アクセス、Numaferm社の生化学的生産プラットフォームと持続可能なペプチド製造に関する専門知識を活用しました。

同様に、2023年8月、EUROAPIとCDMOであるBianoGMPの株主は、EUROAPIがBianoの株式を100%取得する株式売買・譲渡契約を締結しました。この契約は、初期段階(前臨床およびフェーズ1)のオリゴヌクレオチドプロジェクトにおけるEUROAPIの魅力を高めるものです。

したがって、ペプチドやオリゴヌクレオチドをベースとした治療薬に対する需要の増加や戦略的提携は、予測期間中の市場成長に寄与すると予想されます。しかし、厳しい規制政策と治療に伴う高コストが、予測期間中の市場の抑制要因になると予想されます。

ペプチドおよびオリゴヌクレオチドCDMO市場の動向

治療薬セグメントが大きな市場シェアを占め、予測期間中も同様の状況が続く見込み

ペプチドおよびオリゴヌクレオチド治療薬は多面的な用途を有し、製造および規制上の共通点があり、製剤の進歩により製品の複雑性が増し、革新的なソリューションが必要となります。熟練した開発・製造受託機関との連携は、医薬品開発者の製造要件を容易にし、開発努力を優先させることを可能にします。

ペプチドとオリゴヌクレオチドの治療への応用は、医薬品開発活動を活発化させ、市場の成長に寄与すると予想されます。ペプチドは、標的を絞ったがん治療や糖尿病などの疾患管理のために研究されています。これらの疾患による負担の増大は、同分野の成長を促進すると予想されます。例えば、米国がん協会(ACS)が発表した2024年の統計によると、がんの罹患率は2021年の193万件から2023年には200万件に増加すると推定され、2年間で6万件以上増加しており、国内におけるがん罹患率の急速な伸びを示しています。ペプチドやオリゴヌクレオチドは、がん標的治療薬として研究されています。CDMOはペプチドベースの抗がん剤の開発と生産に貢献しています。

さらに、ペプチドやオリゴヌクレオチドの生産能力の立ち上げは、予測期間中に市場を押し上げると予想されています。例えば、2023年9月、CordenPharma社は、世界最大の固相ペプチド合成(SPPS)製造施設であるCordenPharma Colorado社において、新たにアップグレードされた設備による商業用ペプチド生産能力の増強を発表しました。

したがって、ペプチドとオリゴヌクレオチドの治療用途と市場プレイヤーの戦略的イニシアティブが、予測期間中にこのセグメントの成長を促進すると予想されます。

北米が予測期間中に大きな市場シェアを占める見込み

北米では、ペプチドおよびオリゴヌクレオチドCDMO市場は、確立された研究施設、ペプチド・オリゴヌクレオチドをベースとした治療薬の研究開発への高い投資、慢性疾患の負担の増加によって成長すると予想されます。ペプチドやオリゴヌクレオチドを含むバイオ医薬品の需要は高まっています。北米のCDMOは、このような複雑な分子の開発・製造に特化したサービスを提供することで、この需要に対応できる体制を整えています。

製薬会社やバイオテクノロジー企業による研究開発活動への継続的な投資は、ペプチドおよびオリゴヌクレオチドCDMO市場の拡大に貢献しています。こうした投資は、専門的な専門知識やインフラを利用するためにCDMOとの提携を伴うことが多いです。例えば、2023年1月、アジレント・テクノロジー社は、市場の急成長を受けて、治療用核酸の製造能力を倍増させるために約7億2,500万米ドルを投資しました。この投資は、治療用オリゴヌクレオチドに対する旺盛な需要と、治療用オリゴヌクレオチド受託開発・製造組織の比類ない品質とサービスを反映しています。

さらに2022年12月、CDMOのアシムケムラボラトリーズ(天津)はマサチューセッツ州ウォバーンに新拠点を開設すると発表しました。最新のボストン拠点は、低分子、ペプチド、オリゴヌクレオチドを含む初期段階の研究開発サービスを提供します。

従って、北米のペプチドおよびオリゴヌクレオチドCDMO市場は、需要の増加、治療薬の進歩、アウトソーシング動向、規制支援、R&D投資により盛り上がると予想されます。

ペプチドおよびオリゴヌクレオチドCDMO産業の概要

ペプチド・オリゴヌクレオチド受託開発・製造市場の競争は緩やかで、大小のプレーヤーがサービスの拡大、提携、共同研究、合併、買収などの戦略的活動に取り組んでいます。主なプレーヤーは、Thermo Fisher Scientific Inc.、Polypeptide Group、Wuxi Apptec、Genscript Biotech Corporation、CordenPharma Internationalです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ペプチドおよびオリゴヌクレオチドベースの治療薬に対する需要の増加

- ペプチド合成およびオリゴヌクレオチド製造技術の進歩

- 製薬業界におけるアウトソーシング動向の高まり

- 市場抑制要因

- 規制上の課題

- 製造能力の制約と知的財産に関する懸念

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-金額)

- 製品別

- ペプチドCDMO

- オリゴヌクレオチドCDMO

- 用途別

- 治療

- 研究用途

- 診断

- その他の用途

- エンドユーザー別

- 製薬・バイオテクノロジー企業

- 研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- インド

- 日本

- 中国

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Catalent, Inc.

- Genscript Biotech Corporation

- Polypeptide Group

- Bachem Holding AG

- Ajinomoto Co. Inc.

- Wuxi Apptec Co. Ltd

- Rentschler Biopharma SE

- CordenPharma International

- Senn Chemicals AG

- PolyPeptide Group

- Almac Group

- Lonza

第7章 市場機会と今後の動向

The Peptide And Oligonucleotide CDMO Market size is estimated at USD 2.40 billion in 2024, and is expected to reach USD 4.67 billion by 2029, growing at a CAGR of 11.70% during the forecast period (2024-2029).

The market increases due to the rising demand for peptide and oligonucleotide-based therapeutics, advancements in peptide synthesis and oligonucleotide manufacturing technologies, and the growing outsourcing trend in the pharmaceutical industry. Peptides and oligonucleotides offer a more targeted and personalized approach to treating diseases. They are designed to interact with specific molecular targets, providing precision in therapeutic interventions. These molecules are being explored for various therapeutic areas, including cancer, genetic disorders, and metabolic diseases. Oligonucleotides, for instance, are gaining attention for their potential in addressing genetic mutations. CDMOs often specialize in synthesizing and manufacturing specific types of molecules, including peptides and oligonucleotides. Their expertise ensures efficient and high-quality production, ensuring the therapeutic molecules meet the required standards.

Collaboration and partnerships within the pharmaceutical industry can significantly boost the peptide and oligonucleotide CDMO market. For instance, in May 2023, PolyPeptide and Numaferm signed a Preferred Partner Collaboration Agreement for peptide development and production, leveraging PolyPeptide's cGMP manufacturing capacities, regulatory know-how, and market access and Numaferm's biochemical production platform and expertise in sustainable peptide manufacturing.

Similarly, in August 2023, EUROAPI and the shareholders of BianoGMP, a CDMO, signed a share purchase and transfer agreement under which EUROAPI will acquire 100% of Biano shares. The deal enhances EUROAPI's attractiveness for early-phase (preclinical and Phase 1) oligonucleotide projects.

Hence, increasing demand for peptide and oligonucleotide-based therapeutics and strategic partnerships is expected to contribute to the market growth during the forecast period. However, stringent regulatory policies and the high cost associated with the therapy are expected to restrain the market during the forecast period.

Peptide And Oligonucleotide CDMO Market Trends

The Therapeutics Segment Holds a Significant Market Share and is Expected to Continue the Same During the Forecast Period

Peptide and oligonucleotide therapeutics possess multifaceted applications and share manufacturing and regulatory similarities, with advancements in formulation increasing product complexity and necessitating innovative solutions. Collaboration with a proficient contract development and manufacturing organization facilitates drug developers' manufacturing requirements, enabling them to prioritize their development efforts.

The therapeutic application of peptides and oligonucleotides is expected to increase drug development activities and contribute to market growth. Peptides are being explored for targeted cancer therapies and managing conditions like diabetes. The growing burden of these diseases is expected to propel the segment's growth. For instance, according to 2024 statistics published by the American Cancer Society (ACS), the incidence of cancer cases was estimated to increase from 1.93 million in 2021 to 2.00 million in 2023, a rise of more than 60 thousand cases in two years, demonstrating a rapid growth in the incidence of cancer cases in the country. Peptides and oligonucleotides are being explored for targeted cancer therapies. CDMOs contribute to the development and production of peptide-based anticancer drugs.

Moreover, the launch of peptides and oligonucleotides production capacity is expected to boost the market during the forecast period. For instance, in September 2023, CordenPharma announced the inauguration of increased commercial peptide production capacity with newly upgraded facilities at CordenPharma Colorado, the largest solid-phase peptide synthesis (SPPS) manufacturing facility worldwide.

Hence, the therapeutic applications of peptides and oligonucleotides, along with the strategic initiatives taken by market players, are expected to drive the growth of this segment during the forecast period.

North America is Expected to Hold a Significant Market Share During the Forecast Period

In North America, the peptide and oligonucleotide CDMO market is expected to grow owing to established research facilities, high investment in R&D for peptide and oligonucleotide-based therapeutics, and the growing burden of chronic diseases. The demand for biopharmaceuticals, including peptides and oligonucleotides, has been rising. CDMOs in North America are well-positioned to cater to this demand by offering specialized services in developing and manufacturing these complex molecules.

Continuous investments in research and development activities by pharmaceutical and biotech companies contribute to expanding the peptides and oligonucleotide CDMO market. These investments often involve collaborations with CDMOs to access specialized expertise and infrastructure. For instance, in January 2023, Agilent Technologies Inc. invested approximately USD 725 million to double the manufacturing capacity of therapeutic nucleic acids in response to the market's rapid growth. This investment reflects the strong demand for therapeutic oligonucleotide and the unmatched quality and service of therapeutic oligonucleotide contract development and manufacturing organization.

Additionally, in December 2022, Asymchem Laboratories (Tianjin) Co. Ltd, a CDMO, announced the opening of a new site in Woburn, Massachusetts. The latest Boston site provides early-stage R&D services, including small molecules, peptides, and oligonucleotides.

Hence, the North American peptides and oligonucleotide CDMO market is expected to boost due to increasing demand, advancements in therapeutics, outsourcing trends, regulatory support, and R&D investments.

Peptide And Oligonucleotide CDMO Industry Overview

The market for peptide and oligonucleotide contract development and manufacturing organizations is moderately competitive, with both small and large players involved in strategic activities such as the expansion of services, partnerships, collaborations, as well as mergers, and acquisitions. Key players are Thermo Fisher Scientific Inc., Polypeptide Group, Wuxi Apptec Co. Ltd, Genscript Biotech Corporation, and CordenPharma International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Peptide And Oligonucleotide-Based Therapeutics

- 4.2.2 Advancements In Peptide Synthesis And Oligonucleotide Manufacturing Technologies

- 4.2.3 Increasing Outsourcing Trend In The Pharmaceutical Industry

- 4.3 Market Restraints

- 4.3.1 Regulatory Challenges

- 4.3.2 Manufacturing Capacity Constraints and Intellectual Property Concerns

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Peptide CDMO

- 5.1.2 Oligonucleotide CDMO

- 5.2 By Application

- 5.2.1 Therapeutics

- 5.2.2 Research Applications

- 5.2.3 Diagnostics

- 5.2.4 Other Application

- 5.3 End User

- 5.3.1 Pharmaceutical and Biotechnology Companies

- 5.3.2 Research Organization

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 Japan

- 5.4.3.3 China

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of the Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Thermo Fisher Scientific Inc.

- 6.1.2 Merck KGaA

- 6.1.3 Catalent, Inc.

- 6.1.4 Genscript Biotech Corporation

- 6.1.5 Polypeptide Group

- 6.1.6 Bachem Holding AG

- 6.1.7 Ajinomoto Co. Inc.

- 6.1.8 Wuxi Apptec Co. Ltd

- 6.1.9 Rentschler Biopharma SE

- 6.1.10 CordenPharma International

- 6.1.11 Senn Chemicals AG

- 6.1.12 PolyPeptide Group

- 6.1.13 Almac Group

- 6.1.14 Lonza