|

市場調査レポート

商品コード

1521712

プラスミドDNA受託製造:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Plasmid DNA Contract Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| プラスミドDNA受託製造:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

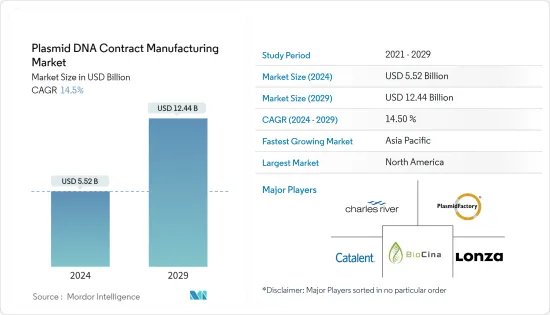

プラスミドDNA受託製造市場規模は2024年に55億2,000万米ドルと推定され、2029年には124億4,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは14.5%で成長すると予測されます。

疾患有病率の増加、調査研究への投資、遺伝子治療の人気が市場成長の主要要因です。遺伝子治療の人気がますます高まっているため、遺伝子治療プロセスにおけるプラスミドの重要な役割により、プラスミドDNA受託製造の需要が高まっています。プラスミドは治療遺伝子を標的細胞に導入するためのキャリアとしての役割を果たします。より多くの遺伝子治療が臨床試験を経て商業生産へと進むにつれ、プラスミドDNAの大規模かつ高品質な生産に対するニーズが高まっています。例えば、2023年8月、Charles Riverは、供給不足に対処し、細胞・遺伝子治療業界の高まる需要を満たすために、世界クラスのHQプラスミド製造センター・オブ・エクセレンスを設立しました。

慢性疾患から感染症の脅威まで、多様な健康課題を特徴とする疾病負担の増加は、プラスミドDNA受託製造サービスの需要を増大させています。英国心臓財団の2024年1月England Factsheetによると、2022年にはイングランドで約760万人が心血管疾患を患っていました。同じ情報源によると、2022年には世界中で約6億2,000万人が心臓・循環器疾患(心血管疾患)を患っています。この数は、ライフスタイルの変化、高齢化、人口増加により、その後も増加し続けています。このように、慢性疾患の有病率の上昇に伴い、新規治療や治療に対する需要も増加しています。プラスミドDNAの受託製造は、慢性疾患に対する高度な治療法を開発するバイオテクノロジー企業や製薬企業の要求に応えることで、この恩恵を受ける態勢を整えています。

WHOが2023年3月に発表した報告書によると、2022年末までに約3,900万人がHIV感染者となり、その中には150万人の幼児も含まれています。さらに、HIVとともに生きる2,980万人が、世界中で抗レトロウイルス療法を受けていました。プラスミドDNAは、遺伝子治療やワクチン開発において極めて重要であり、慢性疾患の治療において牽引役となっています。遺伝子治療は、治療遺伝子を細胞内に導入するためにプラスミドDNAを利用することが多く、慢性疾患に関連する遺伝的障害を対象としています。したがって、慢性疾患の負担の増大は、予測期間中の市場の成長を後押しすると予想されます。

この市場の参入企業は、プラスミドDNAの需要拡大に対応するため、継続的に事業を拡大しています。各社は、プロセス開発と最適化、プラスミド設計、プラスミド工学、プラスミド構築、GMPプラスミド製造を含む様々なプラスミドサービスを提供することで、完全に統合されたワンストップ・ショップとしての役割を果たすべく、精力的に能力を高めています。

例えば、Catalentは2023年1月、ベルギーのゴーセリーズにある同社の欧州細胞治療センター・オブ・エクセレンス内に、新しい商業グレードのプラスミドDNA(pDNA)生産施設を開設しました。この施設は、臨床と商業段階の供給用にCGMPグレードのpDNAを製造するための、複数のクリーンルームにまたがる1万2,000平方フィート(1,100平方メートル)の開発・製造スペースを有しています。

このように、細胞・遺伝子治療に対する需要の高まりと市場関係者の戦略的活動が、予測期間中の市場成長を後押しすると予想されます。しかし、特に新興諸国では製造のための高度なインフラが必要であり、受託製造に関連する品質問題が予測期間中の市場成長を抑制すると予想されます。

プラスミドDNA受託製造市場動向

細胞・遺伝子治療セグメントは予測期間中に大幅な成長が見込まれる

細胞・遺伝子治療市場は、細胞・遺伝子ベースのプラスミドDNA製造サービスを追加する開発業務受託機関(CDO)の増加により拡大が見込まれます。例えば、2022年10月、Ray Therapeuticsと開発・製造受託機関(CDMO)のForge Biologicsは、臨床段階のプラスミドDNAを製造する契約を延長し、Ray Therapeuticsの画期的なオプトジェネティクス遺伝子治療プログラムをサポートしています。さらに2023年10月、BioCina Pty LtdはGenomeFrontier Therapeutics AU Pty Ltdとの新たな提携を発表し、CAR-T細胞療法製品をサポートするためのミニサークルDNAとプラスミドDNAのプロセス開発とGMP製造においてゲノムフロンティアをサポートすることになりました。

プラスミドDNAプラットフォームの技術的進歩や受託製造による先進技術の採用は、アウトソーシング需要を増加させ、同セグメントの成長を後押しすると予想されます。例えば、2023年1月、Charles River Laboratories International Inc.は、同社の開発製造受託(CDMO)と生物製剤試験の経験から確立されたeXpDNAプラスミドプラットフォームを発表しました。このプラットフォームは、プラスミドの開発・製造期間を大幅に短縮するとともに、細胞・遺伝子治療やワクチン開発者の開発期間を合理化し、製品の品質と一貫性に重点を置いたものです。

遺伝子治療開発企業は、遺伝子治療におけるプラスミドDNAの需要増に対応するため、専門知識、インフラ、規制コンプライアンスを活用するため、こうした専門製造施設と協力することが多いです。このようなアウトソーシングにより、遺伝子治療企業は、商業規模でのプラスミドDNAの効率的かつ信頼性の高い生産を確保しながら、治療の臨床面や規制面に集中することができます。2023年6月、INADcure財団とチャールズ・リバー・ラボラトリーズは、小児神経軸索性ジストロフィーを標的とした遺伝子治療の第I/II相臨床試験用の高品質プラスミドDNA(pDNA)の生産で協力しました。

したがって、細胞・遺伝子治療に対する需要の高まりと市場参入企業による戦略的活動が、予測期間中の同セグメントの成長に寄与すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米では、確立された研究施設、細胞治療のための研究開発投資の増加、慢性疾患の負担増などの要因により、プラスミドDNA受託製造市場の成長が見込まれています。プラスミドDNA受託製造市場の成長は、製品上市数の増加、進行中の臨床試験の多さ、自己免疫疾患、がん、感染症治療への細胞治療の応用の可能性などに起因しています。

細胞・遺伝子治療に対する需要の高まりは、予測期間中の市場成長を後押しすると予想されます。2023年10月現在、北米では細胞療法に焦点を当てた581件以上の臨床試験が実施され、さまざまな疾患の治療に対するこれらの療法の可能性が解釈されています。したがって、臨床開発における研究の増加は、予測期間にわたってプラスミドDNA受託製造市場を押し上げると予想されます。

市場参入企業によるアウトソーシングや戦略的活動の動向の高まりは、予測期間中の市場成長に寄与すると予想されます。例えば、2022年10月、Forge Biologicsは、9,000万米ドルのシリーズC資金調達ラウンドを完了した後、AAVクライアントをサポートするためにプラスミドDNA(pDNA)製造サービスを開始しました。同様に、2022年5月、AvantorはCytovance Biologics(プラスミドDNAに特化した研究開発・製造受託機関)と、ウイルスベクターとRNAベースのワクチンや治療用の研究グレードとGMPグレードのプラスミドを製造する契約を締結しました。

したがって、細胞治療や遺伝子治療のための臨床研究数の増加、プラスミドDNA製造施設の拡大、市場参入企業による戦略的提携は、予測期間にわたって市場を押し上げると予想されます。

プラスミドDNA受託製造業界概要

プラスミドDNA受託製造市場は適度な競合関係にあり、サービスの拡大、提携、共同研究、M&Aなどの戦略的活動に取り組む大企業と中小企業の両方が存在します。PlasmidFactory GmbH &Co.KG、Lonza、BioCina、Charles River Laboratories、Catalent Inc.などが、この市場における注目すべき主要企業です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 疾患有病率の増加

- 調査研究の投資拡大

- 遺伝子治療の人気の高まり

- 市場抑制要因

- 一部の新興諸国における製造のための高度なインフラの欠如

- 受託製造に伴う品質問題

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 用途別

- 細胞・遺伝子治療

- 免疫療法

- その他

- 治療領域別

- がん

- 感染症

- 自己免疫疾患

- 循環器疾患

- その他

- エンドユーザー別

- 製薬・バイオテクノロジー企業

- 研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- インド

- 日本

- 中国

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Charles River Laboratories

- VGXI Inc.

- PlasmidFactory GmbH & Co. KG

- Boehringer Ingelheim

- BioCina

- TriLink Biotechnologies

- Esco Aster PTE. LTD

- Thermo Fisher Scientific Inc.

- VIVE biotech

- Lonza

第7章 市場機会と今後の動向

The Plasmid DNA Contract Manufacturing Market size is estimated at USD 5.52 billion in 2024, and is expected to reach USD 12.44 billion by 2029, growing at a CAGR of 14.5% during the forecast period (2024-2029).

The growing disease prevalence, investment in research studies, and popularity of gene therapy are the key factors driving the growth of the market. The ever-increasing popularity of gene therapy drives the demand for plasmid DNA contract manufacturing due to the essential role of plasmids in the gene therapy process. Plasmids serve as carriers for introducing therapeutic genes into target cells. As more gene therapy treatments advance through clinical trials and into commercial production, there is an increasing need for large-scale, high-quality production of plasmid DNA. For instance, in August 2023, Charles River established a world-class HQ plasmid manufacturing center of excellence to combat supply scarcity and fulfill the escalating demands of the cell and gene therapy industry.

The increasing disease burden, characterized by diverse health challenges ranging from chronic diseases to infectious threats, increases the demand for plasmid DNA contract manufacturing services. According to the British Heart Foundation's January 2024 England Factsheet, approximately 7.6 million individuals in England had cardiovascular diseases in 2022. As per the same source, around 620 million people live with heart and circulatory diseases (cardiovascular diseases) across the world in 2022; this number has been rising since then due to changing lifestyles, aging, and the growing population. Thus, with the rise in the prevalence of chronic diseases, there is a corresponding increase in demand for novel therapeutics and treatments. Plasmid DNA contract manufacturing is poised to benefit from this by meeting the requirements of biotech and pharmaceutical companies that are developing advanced therapies for chronic conditions.

As per the report published by WHO in March 2023, approximately 39.0 million people were living with HIV by the end of 2022, including 1.5 million children. Moreover, 29.8 million people living with HIV were receiving antiretroviral therapy globally. Plasmid DNA is crucial in gene therapy and vaccine development, gaining traction in treating chronic diseases. Gene therapies often utilize plasmid DNA to deliver therapeutic genes into cells, targeting genetic disorders associated with chronic conditions. Hence, the growing burden of chronic diseases is expected to boost the market's growth over the forecast period.

The players in this market are continuously expanding their operations to accommodate the growing demand for plasmid DNA. They are vigorously advancing their capabilities to serve as a fully integrated one-stop-shop by offering various plasmid services, including process development and optimization, plasmid design, plasmid engineering, plasmid construction, and GMP plasmid manufacturing.

For instance, in January 2023, Catalent inaugurated a novel commercial-grade plasmid DNA (pDNA) production facility within its European Center of Excellence for Cell Therapies in Gosselies, Belgium. The facility has 12,000 square feet (1,100 m2) of development and manufacturing space across multiple cleanrooms for CGMP-grade pDNA production for clinical and commercial-phase supply.

Thus, the growing demand for cell and gene therapy and strategic activities from the market players is expected to boost the market's growth over the forecast period. However, the need for advanced infrastructure for manufacturing in particular developing countries and quality issues associated with contract manufacturing are anticipated to restrain the market growth over the forecast period.

Plasmid DNA Contract Manufacturing Market Trends

The Cell & Gene Therapy Segment is Expected to Grow Significantly Over the Forecast Period

The cell & gene therapy market is anticipated to expand due to the growing number of contract development organizations (CDOs) adding cell and gene-based plasmid DNA manufacturing services to their offerings. For instance, in October 2022, Ray Therapeutics and contract development and manufacturing organization (CDMO) Forge Biologics extended their agreement to manufacture clinical-stage plasmid DNA, supporting Ray Therapeutics' groundbreaking optogenetics gene therapy program. Moreover, in October 2023, BioCina Pty Ltd announced a new partnership with GenomeFrontier Therapeutics AU Pty Ltd to support GenomeFrontier with process development and GMP manufacturing for Minicircle DNA and Plasmid DNA to support the CAR-T cell therapy product.

The technological advancement of the plasmid DNA platform and the introduction of advanced technologies by contract manufacturing are expected to increase the outsourcing demand, thereby boosting the segment's growth. For instance, in January 2023, Charles River Laboratories International Inc. launched its eXpDNA plasmid platform, established from the company's contract development and manufacturing (CDMO) and biologics testing experience. The platform significantly reduces plasmid development and production timelines while streamlining the development journey for cell and gene therapy and vaccine developers, focusing on product quality and consistency.

Gene therapy developers often collaborate with these specialized manufacturing facilities to leverage their expertise, infrastructure, and regulatory compliance to meet the increasing demand for plasmid DNA in gene therapy treatments. This outsourcing allows gene therapy companies to focus on the clinical and regulatory aspects of their treatments while ensuring the efficient and reliable production of plasmid DNA at a commercial scale. In June 2023, INADcure Foundation and Charles River Laboratories collaborated on the production of high-quality plasmid DNA (pDNA) for Phase I/II clinical trials of a gene therapy targeting Infantile Neuroaxonal Dystrophy.

Hence, the growing demand for cell and gene therapy and strategic activities by the market players are expected to contribute to the segment's growth over the forecast period.

North America is Expected to Hold a Significant Share of the Market Over the Forecast Period

In North America, the plasmid DNA contract manufacturing market is expected to grow owing to factors such as established research facilities, increasing investment in R&D for cell therapy, and the growing burden of chronic diseases. The growth of the plasmid DNA contract manufacturing market can be attributed to the increasing number of product launches, the high number of ongoing clinical trials, and the potential application of cell therapies in the treatment of autoimmune diseases, cancer, and infectious diseases.

The growing demand for cell and gene therapy is expected to boost the market's growth over the forecast period. As of October 2023, more than 581 clinical trials focusing on cell therapies were conducted to interpret the potential of these therapies for treating various disease indications in North America. Therefore, the increasing research in clinical development is expected to boost the plasmid DNA contract manufacturing market over the forecast period.

The growing trend of outsourcing and strategic activities by the market players is expected to contribute to the market's growth over the forecast period. For instance, in October 2022, Forge Biologics launched plasmid DNA (pDNA) manufacturing services to support its AAV clients after closing a USD 90 million Series C funding round. Similarly, in May 2022, Avantor signed an agreement with Cytovance Biologics (a contract development and manufacturing organization specializing in plasmid DNA) in order to manufacture research-grade and GMP-grade plasmids for viral vectors and m RNA-based vaccines and therapeutics.

Hence, the increase in the number of clinical research for cell and gene therapy, expansion of plasmid DNA manufacturing facilities, and strategic collaboration by the market players are expected to boost the market over the forecast period.

Plasmid DNA Contract Manufacturing Industry Overview

The plasmid DNA contract manufacturing market is moderately competitive, with the presence of both small and large players who are involved in strategic activities such as the expansion of services, partnerships, collaborations, and mergers and acquisitions. PlasmidFactory GmbH & Co. KG, Lonza, BioCina, Charles River Laboratories, and Catalent Inc. are among the notable key players in this market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Disease Prevalence

- 4.2.2 Growing Investments in Research Studies

- 4.2.3 Growing Popularity of Gene Therapy

- 4.3 Market Restraints

- 4.3.1 Lack of Advanced Infrastructure For Manufacturing in Certain Developing Countries

- 4.3.2 Quality Issues Associated With Contract Manufacturing

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Application

- 5.1.1 Cell & Gene Therapy

- 5.1.2 Immunotherapy

- 5.1.3 Others

- 5.2 By Therapeutic Area

- 5.2.1 Cancer

- 5.2.2 Infectious Diseases

- 5.2.3 Autoimmune Diseases

- 5.2.4 Cardiovascular Diseases

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Pharmaceutical and Biotechnology Companies

- 5.3.2 Research Institutes

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 Japan

- 5.4.3.3 China

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of the Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Charles River Laboratories

- 6.1.2 VGXI Inc.

- 6.1.3 PlasmidFactory GmbH & Co. KG

- 6.1.4 Boehringer Ingelheim

- 6.1.5 BioCina

- 6.1.6 TriLink Biotechnologies

- 6.1.7 Esco Aster PTE. LTD

- 6.1.8 Thermo Fisher Scientific Inc.

- 6.1.9 VIVE biotech

- 6.1.10 Lonza