|

市場調査レポート

商品コード

1521702

牛血漿誘導体:市場シェア分析、産業動向、成長予測(2024年~2029年)Bovine Blood Plasma Derivatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 牛血漿誘導体:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

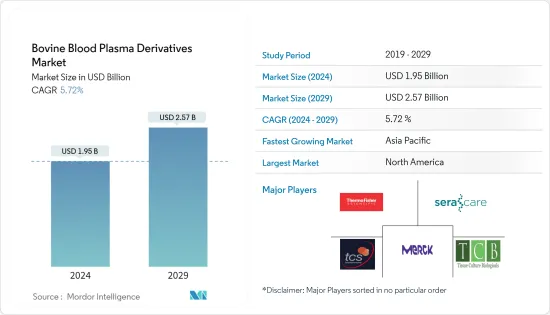

牛血漿誘導体の市場規模は2024年に19億5,000万米ドルと推定され、2029年には25億7,000万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは5.72%で成長する見込みです。

牛血漿誘導体とは、牛の血漿から得られる物質を指します。血漿とは、血液中の血球が分離した後に残る液体部分です。免疫グロブリン(抗体)、アルブミン、凝固因子、その他の生理活性成分など、さまざまなタンパク質で構成されています。牛血漿誘導体は、クロマトグラフィー技術によって処理され、医薬品、バイオテクノロジー、動物栄養などの産業における様々な用途のために、特定のタンパク質や成分を抽出します。

より良い成果を得るための研究開発における牛血漿誘導体の使用の開拓や、動物飼料産業における噴霧乾燥牛血漿の使用の増加は、市場成長を促進すると予想されるいくつかの要因です。例えば、2023年2月、Scientific Reports誌が発表した研究によると、細胞培養に使用される牛胎児血清の品質を均一に標準化することで、科学研究における実験結果の再現性が向上すると述べられています。

ウシの血液由来のタンパク質は、消化性の高い動物性タンパク質源である血漿粉末の製造に利用されます。この粉末は一般的に、飼料の嗜好性を高め、動物の腸の健康を促進し、動物の肉質を向上させるために使用されます。2023年6月の国連食糧農業機関(FAO)によると、2050年までに動物性タンパク質の生産量は年間約1.7%増加し、食肉生産量は70%近く増加すると予測されています。動物性タンパク質と食肉生産に対する需要の増加は、牛血漿誘導体に対する需要を増加させ、それによって市場の成長を促進します。

さらに、血漿由来の治療に対する需要が増加し続ける中、企業は、世界中の患者の増加する要求に応えるため、革新、効率性の向上、最高級の血漿製品の提供を保証することを目指しているため、競争の激化に直面しています。例えば、2023年8月、Dyadic International Inc.は、動物実験を行わない組換え血清アルブミンの試験で良好な結果が得られたと発表しました。同社独自の真菌ベースの微生物タンパク質生産プラットフォームを通じて、同社は、さまざまな疾患を治療するための医薬品用途に供給するために、動物を使わない組換えウシ血清アルブミンを生産する安定した細胞株の開発に成功しました。

このように、さまざまな臨床用途における牛血液形質誘導体の要件を満たす牛血清アルブミンの開発におけるこのような技術革新は、今後5年間の市場成長を促進すると予測されます。

反対に、牛血漿誘導体から感染する人獣共通感染症の可能性や、他の供給源からの代替血漿誘導体が入手可能であることが、予測期間中の市場成長の妨げになると予想されます。

牛血漿誘導体市場の動向

予測期間中、トロンビンセグメントが牛血漿誘導体市場を独占する見込み

- 牛血漿由来のトロンビンは、医療セグメントで重要性を増しています。トロンビンは、心臓血管、整形外科、一般外科などの手術中の出血抑制に役立っています。ウシのトロンビンは止血を促進し、創傷治癒を促進する効果を示しています。そのため、局所止血剤として外科手術中にトロンビンを使用するケースが増加していることが、このセグメントの拡大につながっています。

- WHOのデータ2023によると、世界では毎年3億件以上の手術が行われており、世界中で行われる外科手術の件数は時間の経過とともに劇的に増加しています。手術件数の増加に伴い、牛由来トロンビンの使用需要も予測期間中に増加する可能性があります。

- 牛血漿由来のトロンビンは再生医療用途にも使用されます。血小板豊富血漿(PRP)や他の成長因子と組み合わせてトロンビンゲルマトリックスを作ることができます。このマトリックスは、細胞の移動、増殖、組織再生をサポートする足場として機能します。Rohto Pharmaceuticalは2022年9月、自己多血小板血漿(PRP)ゲル調製キット「オートロゲルシステム」の日本での使用承認を取得しました。これは生物製剤であり、従来の治療に反応しなかった創傷の治癒や被覆を促進するために使用されます。オートロジェルは誘導体としてトロンビンを含んでおり、患者の予後を効果的に改善するのに役立ちます。

- したがって、新製品の開発とトロンビンを使用する手術の増加は、今後数年間でトロンビンセグメントの著しい成長を示すことになると予想されます。

北米が牛血漿誘導体市場を独占する見込み

- 北米は、手術症例の増加、医療インフラの整備、新製品の上市、同地域における既存企業の存在などの要因により、市場を独占すると予想されます。

- トロンビンのような牛血漿の誘導体は、術中出血の管理に役立ちます。したがって、手術件数が増加するにつれて、牛血漿誘導体の使用はこの地域で拡大する可能性が高いです。全米保健統計センターによると、米国では2022年、出産の32.1%が帝王切開分娩でした。さらに、2023年4月にNCBIで発表された研究の1つによると、米国では年間120万件以上の胆嚢摘出手術が行われています。米国では外科手術の件数が多いため、この地域ではトロンビンのような牛血漿誘導体の需要が高まると予想されます。

- 米国飼料産業協会が発表したデータによると、2023年6月、動物栄養産業は2022年に米国経済に2,600億米ドル以上を貢献しました。米国の動物飼料とペットフード製造業界もまた、北米における牛血漿誘導体の牽引役です。Feed Additiveが発表したデータによると、2023年9月、この地域のペットフード生産量は2021年の1,060万トンから2022年には1,120万トンに増加しました。したがって、ペットフード生産量の増加に伴い、牛血漿誘導体の需要も増加します。ペットフード製造会社は、ペットフードをより健康的なものにするため、さまざまな牛血漿誘導体を飼料配合物として添加しました。このように、牛血漿誘導体の市場は、北米におけるこの産業の商業的実行可能性を後押ししています。

- さらに、ペットの人間化という動向の高まりにより、カナダでは高品質の原材料を使用したプレミアム・ペットフードへの嗜好が高まっています。データによると、カナダではペットフードの需要が増加しています。米国農務省が発表したデータによると、2022年12月、カナダは2021年に80万トンのペットフードを生産しました。また、同ソースによると、2022年半ばから、カナダが米国から輸入したペットフードの金額は、2021年の同時期と比較して19.6%増加しました。したがって、このペットフード需要の増加が市場成長に寄与しています。

- 結論として、動物飼料需要の増加、市場参入企業の存在、米国における手術件数の多さは、同国における牛血漿誘導体市場の成長を促進する要因の一部です。したがって、前述の要因により、北米で調査された市場は成長すると予想されます。

牛血漿誘導体産業概要

牛血漿誘導体市場は、世界的と地域的に事業を展開する複数の企業が存在するため、その性質上セグメント化されています。競合情勢には、LAMPIRE Biological Labs Inc.、Merck KGaA、SeraCare、MP Biomedicals、Thermo Fisher Scientific、TCS Biosciences、ROCKY MOUNTAIN BIOLOGICALS、Bovogen Biologicals、Kraeber &Co GmbH、Auckland BioSciences Ltd、Tissue Culture Biologicalsなど、市場シェアを持ち、知名度の高い国際企業や地元企業の分析が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 製薬とバイオテクノロジー産業における研究開発活動の活発化

- 動物飼料業界における血漿粉末の製造における牛血漿誘導体の使用の増加

- 牛血漿誘導体の加工技術の進歩

- 市場抑制要因

- 牛血漿誘導体から人獣共通感染症が感染する可能性の高さ

- 牛血漿誘導体の代替品の利用可能性

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額ベース市場規模-米ドル)

- 誘導体別

- 免疫グロブリン

- フィブリノゲン

- ウシ血清アルブミン

- ウシ胎児血清

- 新生仔牛血清

- トロンビン

- その他の誘導体

- エンドユーザー産業別

- 製薬会社とバイオテクノロジー企業

- 学術・研究機関

- 食品産業

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- LAMPIRE Biological Labs Inc.

- Merck KGaA

- SeraCare

- MP BIOMEDICALS

- Thermo Fisher Scientific

- TCS Biosciences

- ROCKY MOUNTAIN BIOLOGICALS

- Bovogen Biologicals

- Tissue Culture Biologicals

- Kraeber & Co GmbH

- Lake Immunogenics Inc.

- Auckland BioSciences Ltd

第7章 市場機会と今後の動向

The Bovine Blood Plasma Derivatives Market size is estimated at USD 1.95 billion in 2024, and is expected to reach USD 2.57 billion by 2029, growing at a CAGR of 5.72% during the forecast period (2024-2029).

Bovine blood plasma derivatives refer to substances obtained from the blood plasma of cattle. Blood plasma is the liquid part of blood that remains once the blood cells have been separated. It consists of different proteins, such as immunoglobulins (antibodies), albumin, coagulation factors, and other bioactive elements. Bovine blood plasma derivatives undergo processing through chromatographic techniques to extract specific proteins or components for various applications in industries such as pharmaceuticals, biotechnology, and animal nutrition.

The growing use of bovine plasma derivatives in research and development to achieve better outcomes and the increasing use of spray-dried bovine plasma in the animal feed industry are some factors that are expected to drive market growth. For instance, in February 2023, a study published by Scientific Reports stated that a uniform standard quality of fetal bovine serum used in cell cultures improves the repeatability of experimental results in scientific studies.

Proteins derived from bovine blood are utilized in creating plasma powder, which is a highly digestible animal protein source. This powder is commonly used to enhance feed palatability, promote animal gut health, and promote animal meat quality. According to the United Nations Food and Agriculture Organization (FAO) in June 2023, by 2050, production of animal proteins is expected to grow by around 1.7% per year, with meat production projected to rise by nearly 70%. An increasing demand for animal proteins and meat production increases the demand for bovine blood plasma derivatives, thereby driving market growth.

Furthermore, as the demand for plasma-derived therapies continues to rise, companies face heightened competition as they aim to innovate, enhance efficiency, and guarantee the provision of top-notch plasma products to cater to the increasing requirements of patients worldwide. For instance, in August 2023, Dyadic International Inc. announced positive results in the company's animal-free recombinant serum albumin trail. Through the company's proprietary fungal-based microbial protein production platforms, the company successfully developed stable cell lines to produce animal-free recombinant bovine serum albumin to supply in pharmaceutical applications to treat different diseases.

Thus, such innovation in developing bovine serum albumin to meet the requirement of bovine blood plasm derivatives in different clinical applications is projected to drive market growth over the next five years.

On the contrary, the chances of zoonotic diseases transmitted from bovine blood plasma derivatives and the availability of alternative plasma derivatives from other sources are expected to hinder market growth during the forecast period.

Bovine Blood Plasma Derivatives Market Trends

Thrombin Segment is Expected to Dominate the Bovine Blood Plasma Derivatives Market During the Forecast Period

- Thrombin, derived from bovine blood plasma, has been growing in importance in the medical field. It helps control bleeding during surgeries, including cardiovascular, orthopedic, and general surgical procedures. Bovine thrombin has shown effectiveness in promoting hemostasis and facilitating wound healing. Thus, the rise in the utilization of thrombin during surgical procedures as a topical hemostatic agent is responsible for the expansion of the segment.

- According to WHO data 2023, globally, more than 300 million surgeries are performed each year, and the number of surgical procedures performed around the world has increased dramatically over time. As the number of surgical procedures increases, the demand for the use of bovine derivatives thrombin may also increase during the forecast period.

- Thrombin derived from bovine blood plasma is also used in regenerative medicine applications. It can be combined with platelet-rich plasma (PRP) or other growth factors to create a thrombin gel matrix. This matrix acts as a scaffold to support cell migration, proliferation, and tissue regeneration. In September 2022, Rohto Pharmaceutical Co. Ltd got approval to use in Japan for AutoloGel System, a preparation kit for autologous platelet-rich plasma (PRP) gel. It is a biological product and is used to promote the healing or dressing of wounds that have not responded to conventional treatment. The Autologel contains thrombin as a derivative, which helps improve patients' outcomes effectively.

- Hence, new product development and an increasing number of surgeries that use thrombin are expected to witness significant growth of the thrombin segment in the coming years.

North America is Expected to Dominate the Bovine Blood Plasma Derivatives Market

- North America is expected to dominate the market owing to factors such as increasing cases of surgeries, developed healthcare infrastructure, new product launches, and the presence of established players in the region.

- The derivatives of bovine blood plasma, like thrombin, help in managing interoperative bleeding. Thus, as the number of surgeries increases, the use of bovine blood plasma derivatives is likely to grow in the region. According to the National Center for Health Statistics, in the United States, in 2022, 32.1% of births were cesarean deliveries. Additionally, one of the published studies in the NCBI in April 2023 stated that in the United States, more than 1.2 million cholecystectomies are done annually. The high volume of surgical procedures in the United States is expected to drive the demand for bovine blood plasma derivatives like thrombin in the region.

- According to data published by the American Feed Industry Association, in June 2023, the animal nutrition industry contributed more than USD 260 billion to the US economy in 2022. The US animal feed and pet food manufacturing industry is another driver of bovine blood plasma derivatives in North America. According to data published by Feed Additive, in September 2023, the pet food production of the region increased from 10.6 million tons in 2021 to 11.2 million tons in 2022. Thus, as pet food production increases, the demand for bovine blood plasma derivatives also increases. Pet food manufacturing companies added different bovine blood plasma derivatives as feed formulations to make pet food healthier. Thus, the market for bovine blood plasma derivatives drives the commercial viability of this industry in North America.

- Further, the rising trend of humanizing pets has led to an increased preference for premium pet food made with high-quality ingredients in Canada. Data show that the demand for pet food in Canada has increased. According to the Data published by the United States Department of Agriculture, in December 2022, Canada produced 0.80 million tons of pet food in the year 2021. The same source also stated that from mid-year 2022, the value of pet food imported by Canada from the United States increased by 19.6% compared to the same period in 2021. Hence, this increasing demand for pet food contributes to market growth.

- In conclusion, the growing demand for animal feed, the presence of market players, and the high volume of surgeries in the United States are some of the factors driving the growth of the bovine blood plasma derivatives market in the country. Therefore, owing to the aforementioned factors, the market studied is anticipated to grow in North America.

Bovine Blood Plasma Derivatives Industry Overview

The bovine blood plasma derivatives market is fragmented in nature due to the presence of several companies operating globally and regionally. The competitive landscape includes an analysis of a few international and local companies that hold the market shares and are well known, including LAMPIRE Biological Labs Inc., Merck KGaA, SeraCare, MP Biomedicals, Thermo Fisher Scientific, TCS Biosciences, ROCKY MOUNTAIN BIOLOGICALS, Bovogen Biologicals, Kraeber & Co GmbH, Auckland BioSciences Ltd, and Tissue Culture Biologicals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Reserach and Develpment Activity in Pharmaceutical and Biotechnology Industries

- 4.2.2 Increasing Use of Bovine Plasma Derivatives in the Production of Plasma Powder in Animal Feed Insustry.

- 4.2.3 Technological Advancements in Processing Techniques of Bovin Plasma Derivatives

- 4.3 Market Restraints

- 4.3.1 High Chances of Zoonotic Diseases Transmit From Bovine Blood Plasma Derivatives

- 4.3.2 Alternative Available for Bovine Plasma Derivatives

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Derivative

- 5.1.1 Immunoglobulin

- 5.1.2 Fibrinogen

- 5.1.3 Bovin Serum Albumin

- 5.1.4 Fetal Bovin Serum

- 5.1.5 Newborn Calf Serum

- 5.1.6 Thrombin

- 5.1.7 Other Derivatives

- 5.2 By End-user Industries

- 5.2.1 Pharmaceutical and Biotechnology Companies

- 5.2.2 Academic and Research Institutes

- 5.2.3 Food Industry

- 5.2.4 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 LAMPIRE Biological Labs Inc.

- 6.1.2 Merck KGaA

- 6.1.3 SeraCare

- 6.1.4 MP BIOMEDICALS

- 6.1.5 Thermo Fisher Scientific

- 6.1.6 TCS Biosciences

- 6.1.7 ROCKY MOUNTAIN BIOLOGICALS

- 6.1.8 Bovogen Biologicals

- 6.1.9 Tissue Culture Biologicals

- 6.1.10 Kraeber & Co GmbH

- 6.1.11 Lake Immunogenics Inc.

- 6.1.12 Auckland BioSciences Ltd