|

|

市場調査レポート

商品コード

1521451

衛星地上設備:市場シェア分析、産業動向、成長予測(2024年~2029年)Satellite Ground Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 衛星地上設備:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

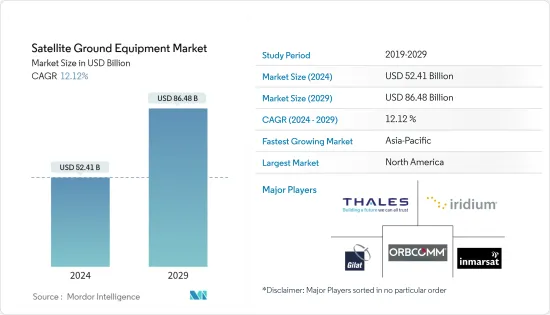

衛星地上設備市場規模は、2024年に524億1,000万米ドルと推定され、2029年には864億8,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは12.12%で成長します。

主要ハイライト

- 衛星地上設備業界は、NOC設備などの無線通信ソリューションの進歩、移動無線通信の需要増加、公共安全用途の大幅な展開により、劇的に成長しています。さらに、低軌道(LEO)衛星システム、高スループット衛星(HTS)、KuバンドとKaバンド衛星の有益なイントロダクションが、市場の有利な成長機会を増やしています。同時に、商用、政府、防衛を含む各セグメントの様々な用途に使用される自律走行車やコネクテッドカーの膨大な需要は、高度にカスタマイズ型SATCOMオンザムービングアンテナを必要とし、信頼性の高い運用が衛星地上設備市場を牽引しています。

- 衛星産業協会(SIA)のレポートによると、GNSS市場とネットワーク機器の拡大に伴い、地上機器の収益は大幅に増加しており、顧客機器の投資とリソースは横ばいか、やや減少しており、移動衛星サービスが調査した市場全体の基本的な成長ポイントになることを明らかにしています。航空機内でスマートフォンやノートパソコンを使用する乗客は、インターネットやビデオストリーミングサービスにアクセスするための機内接続から恩恵を受けることができます。船舶関係者は、海図更新、エンジン監視、気象ルーティング放送など、最新の海事情報への乗組員接続から恩恵を受ける可能性があります。バックパック端末は、過酷で緊急な条件下での接続性をサポートするため、迅速かつ確実に配備されなければならないです。

- 高スループット衛星(HTS)とは、軌道上の同じ割り当て周波数で、固定衛星システムと比べて高いスループットを提供する衛星です。HTSは、周波数と複数のスポットビームを再利用してスループットを向上させ、配信ビットあたりのコストを削減します。HTSは主に、サービスが行き届いていない地域にブロードバンド・インターネット・アクセスサービスを提供するために配備されています。ほとんどのHTS衛星は、主に企業、通信、海事セグメント向けに設計されています。宇宙・衛星システム・プロバイダーは、高速通信サービスのためにHTS衛星を打ち上げています。HTS衛星の打ち上げが増加するにつれて、地上局設備の導入が増加し、市場を牽引しています。

- 衛星放送とは、マルチメディア・コンテンツや放送信号を衛星ネットワークを通じて配信することです。放送信号は通常、テレビやラジオ局などの放送局から発信されます。その後、衛星アップリンク(アップロード)を通じて静止人工衛星に送信され、オープンまたはセキュアなチャネルを通じて他の所定の地理的位置に再配信または再送信されます。直接放送や衛星テレビは、テレビ・コンテンツの効果的な配信形態となっています。広範で制御可能なカバーエリアとはるかに広い帯域幅により、より多くのチャンネルを放送できるため、衛星テレビは非常に魅力的です。

- さらに、現在の市場には多様な衛星アンテナ・ヒーターや衛星アンテナ除氷システムがあり、18インチの住宅用衛星テレビや衛星インターネット・アンテナから、大型の商業用や企業用VSATまで、あらゆる用途に十分な機会を提供しています。衛星テレビや衛星インターネットのアンテナに雪や氷が積もると、信号が途絶えることがあります。衛星除氷システムは、衛星アンテナに雪や氷が積もるのを防ぐ一つの方法です。

- それどころか、海軍が使用しているAdvanced-EHF衛星搭載のマルチバンド端末はかなり高価です。さらに、端末の購入や設置にかかる費用は、ロケットや宇宙船の20倍から30倍にもなります。衛星と端末の開発が別々に行われることは、長い間、無駄とコスト超過の原因となってきました。例えば、空軍が宇宙船を監督する一方で、陸軍が無線を監督することもあります。地上の通信機器と衛星が同時に開発サイクルを終えることはまれです。衛星地上設備サービスのコストが高いことが、市場の拡大を制限しています。

衛星地上設備市場の動向

防衛・官公庁が市場で大きなシェアを占める見込み

- 防衛セグメントの市場シェアは大幅に拡大する見込み。衛星ベースのイメージングのいくつかの用途は、ナビゲーション、マッピングとGIS、緊急事態と安全、ジオマーケティングと広告、エンタープライズ用途、スポーツ、拡大現実/ゲーム、mヘルス、個人追跡、ソーシャルネットワーキングを含みます。これらの用途はすべて、さまざまなニーズや使用条件を満たすようにオーダーメイドされています。コンテキスト認識用途と拡大現実用途の台頭は、位置情報サービス付きデバイスの出荷台数の増加と相まって、予測期間中に市場をさらに拡大すると予想されます。

- 2023年9月、アラブ首長国連邦のYahsatは、アラブ首長国連邦政府に衛星サービスを提供する187億AED(51億米ドル)の重要な契約を獲得しました。17年間のATP(Authorisation to Proceed)契約に基づき、ヤーサットは2026年以降、Al Yah 1衛星とAl Yah 2衛星による安全で信頼性の高い衛星通信容量を政府に記載しています。発表によると、これは2027年と2028年にそれぞれ打ち上げが予定されている2つの新しい衛星、Al Yah 4とAl Yah 5によって補完されます。2024年、Yahsatはマンデート契約に基づき、アラブ首長国連邦政府から10億米ドルの前払いを受ける。ATPマンデートは、2026年11月と12月に締結が予定されている既存の契約、キャパシティサービス契約とマネージドサービス・マンデート(MSM)に取って代わります。

- 2023年11月、航空宇宙・防衛ソリューションプロバイダーのTata Advanced Systems Ltd.は、Satellogic Inc.と提携し、インド国内で宇宙技術能力を確立・開発すると発表しました。サブメートル解像度の地球観測(EO)データ収集の参入企業であるSatellogic Inc.との提携は、同社の衛星戦略の第一歩です。

- GOVSATCOMは、EU宇宙計画(2021~2027年)の一環であり、衛星通信セグメントにおける宇宙の能力を利用して、加盟国またはEUの市民の安全保障に関連する政策の実施を可能にし、促進するものです。地上インフラのない地域(海、空、地方、北極圏など)、あるいは現在の地上インフラが不安定、損傷、破壊されている場合、GOVSATCOMへのアクセスは不可欠である(自然災害、危機、紛争などによる)。さらに、ブロードバンド・インディア・フォーラムによると、固定衛星サービス-FSS/放送衛星サービス-BSSの通信・放送ネットワーク用インターフェース要件(必須技術要件)の新規格により、地上セグメントの超小口径端末(VSAT)参入企業は最新のSATCOM技術を活用できるようになります。

- IoT(モノのインターネット)や自律システムの需要増加、軍事・防衛衛星通信ソリューションの需要増加により、調査対象市場は今後成長すると予想されます。しかし、期間中、衛星通信に対するサイバーセキュリティリスクや衛星データ伝送の干渉が市場成長を阻害すると予想されます。さらに、衛星ミッションにおける将来の技術進歩や、衛星を介した5Gネットワークの展開は、業界に収益性の高い展望をもたらす可能性が高いです。NATOによると、2023年の国内総生産に占めるポーランドの国防費は3.9%で、NATO加盟国の中で最も高く、米国の3.49%がこれに続きます。

予測期間中、北米が主要シェアを占める

- 北米の政府機関は先進的な通信技術を採用するリーダー的存在です。官民一体となった努力により、北米地域、特に米国は新しい衛星とナビゲーションシステムを導入するリーダー的存在であり、北米の衛星地上設備産業の成長を後押ししました。

- 北米には、継続的な監視を必要とする広大な沿岸地域があります。この地域での商業活動と貿易の増加も、海上安全と監視の必要性を後押ししています。さらに、検知と識別のための適切なシステムがない場合、違法行為は国の海上国境を越えてあらゆる方向から起こりうるため、根本的な脅威は海上安全の執行に独特かつ重大な課題を突きつけています。したがって、上記の要因は、予測期間中にこの地域で調査された市場に影響を与えると予想されます。

- さらに、米国は世界最大の軍事支出国です。例えば、2022年度の上院軍事委員会は、大統領提案よりも約250億米ドル高い防衛予算を承認しました。SIPRIによると、2022年の米国の国防費総額は、2018年の6,824億9,000万米ドルに対し、8,769億4,000万米ドルに達します。このような動向は、米国における研究市場の成長に有利です。

- 通信衛星の利点の活用に焦点を当てたいくつかの政府主導のイニシアチブも、北米における調査市場の成長に有利な展望を生み出しています。例えば、2022年1月、カナダのイノベーション・科学技術大臣は、地球観測の懸念とサステイナブル開発の優先事項に対処する新たなソリューションを探求するため、カナダ全土の21団体に800万米ドルを拠出すると発表しました。この資金は、カナダ宇宙庁(CSA)のsmartEarthプログラムから提供されます。このプログラムは、衛星データを活用して困難を解決し、現実世界の問題解決に貢献するカナダ企業を後押しすることを目的としています。

- さらに、需要の高まりがベンダーに北米地域でのサービス拡充を促しており、これも調査対象市場の成長に寄与しています。例えば、2023年4月、Rogers CommunicationsはLynk Globalと提携し、カナダ全土で衛星から電話への接続ソリューションを試験・提供しています。

衛星地上設備産業概要

衛星地上設備市場は、Thales Group、Inmarsat Global Limited、Iridium Communications Inc.、Gilat Satellite Networks Ltd.、Orbcomm Inc.などの大手企業の存在と、新規参入企業の増加により、半固体化しています。同市場のベンダーは、イノベーション、パートナーシップ、合併、買収などの戦略を採用し、製品ラインナップを強化し、サステイナブル競争優位性を獲得しています。

- 2023年5月、低軌道衛星会社OneWebはセントヘレナ島に地上局を設置し、同島の幹線であるエクアイアノ海底ケーブルの能力を獲得する予定です。OneWebは地域の電話会社Sureと10年間の地上局契約を結びました。OneWebはホースポイントに地上局を建設し、Sureがその施設を管理します。地上局はその後、ルパーツ・ビーチにある島のケーブル・ドック局にファイバーで接続されます。

- 2023年3月、インドを拠点とするフルスタックの宇宙工学ソリューション企業であるDhruva Spaceと、フランスを拠点とする衛星通信事業者であり世界のコネクティビティプロバイダーであるKineisは、協定覚書(MoA)に署名し、両組織が協力して宇宙と地上のインフラを立ち上げ、衛星ベースのソリューションの多様性と影響力を拡大することを明らかにしました。軌道上に9基の衛星を持つキネイスの運用サービスは、全世界をカバーしています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場洞察

- 市場概要

- 業界の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- マクロ経済要因が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- モノのインターネット(IoT)と自律システムの増加

- 衛星ベースのサービスに対する需要の増加

- 市場抑制要因

- データ伝送における干渉

第6章 市場セグメンテーション

- タイプ別

- 地上設備

- サービス別

- 業界別

- 海事

- 防衛・官公庁

- 企業

- メディア・エンターテイメント

- その他の業界

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Thales Group

- Inmarsat Global Limited

- Iridium Communications Inc.

- Gilat Satellite Networks Ltd

- Orbcomm Inc.

- Cobham SATCOM(Combham Limited)

- Thuraya Telecommunications Company

- ViaSat Inc.

- ST Engineering iDirect

- L3Harris Technologies Inc.

- Advantech Wireless Technologies Inc.(Baylin Technologies)

- KVH Industries Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Satellite Ground Equipment Market size is estimated at USD 52.41 billion in 2024, and is expected to reach USD 86.48 billion by 2029, growing at a CAGR of 12.12% during the forecast period (2024-2029).

Key Highlights

- The satellite ground equipment industry has grown dramatically due to advancements in radio communication solutions, such as NOC equipment, the increasing demand for mobile radio communications, and the significant deployment of public safety applications. Furthermore, the profitable introduction of low earth orbit (LEO) satellite systems, high throughput satellites (HTS), and Ku- and Ka-band satellites are adding to the lucrative growth opportunities in the market. Simultaneously, the humongous demand for autonomous and connected vehicles used for various applications in the sectors, including commercial government and defense, require sophisticated customized SATCOM-on-the-move antennas for highly trusted operation, driving the Satellite Ground Equipment Market.

- The Satellite Industry Association (SIA) reported that the ground equipment revenues have significantly increased, with the extension in the GNSS markets and network equipment, flat or somewhat declining customer equipment investments and resources, manifesting that mobile satellite services will become a fundamental growth point of the overall market studied. Passengers using a smartphone or laptop in the air can benefit from in-flight connectivity to access the internet or video streaming services. Ship personnel may benefit from crew connectivity with the latest maritime information, such as chart updates, engine monitoring, and weather routing broadcast. The backpack terminals must be quickly and reliably deployed to support connectivity in harsh and emergent conditions.

- A High Throughput Satellite (HTS) is a satellite that provides high throughput compared with a fixed satellite system for the same amount of allocated frequency on orbit. HTS reuses the frequency and multiple spot beams to improve throughput and reduce the cost per bit delivered. HTS is primarily deployed to provide broadband Internet access service to unserved regions. Most HTS satellites are designed mainly for the enterprise, telecom, or maritime sectors. Space and satellite system providers are launching HTS satellites for high-speed communication services. The increasing HTS launches increase the adoption of ground station equipment , thereby driving the market.

- Satellite broadcasting is the distribution of multimedia content or broadcast signals over or through a satellite network. The broadcast signals usually originate from a station such as a TV or radio station. Then they are sent via a satellite uplink (uploaded) to a geostationary artificial satellite for redistribution or retransmission to other predetermined geographic locations through an open or secure channel. Direct broadcasting or satellite television has become an effective form of distribution for television content. The broad and controllable coverage areas and much larger bandwidths enable more channels to be broadcast, making satellite television very attractive.

- Furthermore, there is a diversity of satellite dish heaters and satellite antenna de-icing systems on the market in the present scenario, providing enough opportunities for everything from 18" residential satellite television and satellite Internet dish antennas to larger commercial and enterprise VSAT uses. Collecting snow and/or ice on a satellite television or satellite Internet dish can cause signal loss. The satellite de-icing system is one way to stop snow and ice from accumulating on satellite dishes.

- On the contrary, the multi-band terminals used by the Navy, which come with Advanced-EHF satellites, are quite expensive. Furthermore, the cost of purchasing and installing the terminals can be anywhere from 20 to 30 times that of the rockets and spacecraft. The fact that satellite and terminal development initiatives are carried out separately has long been a source of waste and cost overruns. For example, the Air Force may oversee spacecraft while the Army may oversee radios. Rarely do earth-bound communication equipment and satellites reach the conclusion of their development cycles at the same time. The high cost of satellite ground equipment services is limiting the market's expansion.

Satellite Ground Equipment Market Trends

Defense and Government is Expected to Hold Significant Share of the Market

- The defense segment's market share is expected to expand significantly. The growing investment in satellite technology for weapons, regional security, surveillance, and espionage intelligence is anticipated to benefit the market.Several applications of satellite-based imaging include navigation, mapping and GIS, emergency and safety, geo marketing and advertising, enterprise applications, sports, augmented reality/games, mHealth, personal tracking, and social networking. All these applications are being tailormade to satisfy different needs and usage conditions. The rise of context-aware applications and augmented reality apps, coupled with the increasing shipments of devices with location-based services, is expected to further augment the market during the forecast period.

- In September 2023, United Arab Emirates (UAE) company Yahsat has been awarded a significant AED18.7 billion (USD5.1 billion) deal to provide satellite services to the UAE government. Under the 17-year Authorisation to Proceed (ATP) agreement, Yahsat will supply the government with secure and reliable satellite capacity afforded by the Al Yah 1 and Al Yah 2 satellites from 2026 onwards. The announcement said this will be supplemented by two new planned satellites - Al Yah 4 and Al Yah 5 - expected to launch in 2027 and 2028, respectively. In 2024, Yahsat will receive an advance payment of USD1 billion from the UAE government under the mandate agreement. The ATP mandate will replace existing agreements, the Capacity Services Agreement and the Managed Services Mandate (MSM), expected to conclude in November and December 2026.

- In November 2023, Aerospace and defense solutions provider Tata Advanced Systems Ltd announced it has partnered with Satellogic Inc. to establish and develop local space technology capabilities in India. The partnership with Satellogic, a player in sub-metre resolution Earth Observation (EO) data collection, is a first step in the company's satellite strategy.

- GOVSATCOM is part of the EU Space Programme (2021-2027), which uses space's capabilities in the field of satellite communications to enable and facilitate the implementation of Member States' or EU policies connected to citizen security. In regions with no ground infrastructure (e.g., sea, air, rural areas, the Arctic region), or if the current ground infrastructure is unstable, damaged, or destroyed, access to GOVSATCOM is essential (e.g., due to natural disasters, crises, conflicts). Further, According to the Broadband India Forum, the new standard for Interface Requirements for Communication & Broadcast Networks for fixed-satellite service-FSS/broadcasting-satellite service-BSS (mandatory technical requirements) will allow the ground segment very-small-aperture terminal (VSAT) players to take advantage of the latest SATCOM technologies (BIF).

- The market studied is expected to grow in the future due to an increase in demand for the Internet of Things (IoT) and autonomous systems and a rise in demand for military and defense satellite communication solutions. During the period, however, cybersecurity risks to satellite communication and interference in satellite data transmission are expected to stifle the market growth. Furthermore, future technological advances in satellite missions and the deployment of a 5G network via satellites will likely provide profitable prospects for the industry. Accorindg to Nato, In 2023, Poland's defense spending as a share of gross domestic product was 3.9 percent, the highest of all NATO member states, followed by the United States at 3.49 percent.

North America to Hold Major Share During the Forecast Period

- Government agencies in North America have been among the leaders in adopting advanced communication technologies. Owing to the combined efforts of public and private entities, the North American region, especially the United States, has been among the leaders in introducing new satellite and navigation systems that boosted the growth of the satellite ground equipment industry in North America.

- North America has a large coastal area that requires continuous monitoring. The increasing commercial activities and trade in the region are also propelling the need for maritime safety and surveillance. Furthermore, the underlying threat poses unique and critical challenges in enforcing maritime safety, as illegal activities can happen from all directions across the country's maritime borders if there is no proper system for detection and identification. Hence, the factors mentioned above are anticipated to influence the market studied in the region during the forecast period.

- Furthermore, the United States is the world's largest military spender. For instance, in FY 2022, the Senate Armed Services Committee approved a defense budget of about USD 25 billion higher than the President's proposal. According to SIPRI, in 2022, the total defense expenditure of the United States reached USD 876.94 billion, compared to USD 682.49 billion in 2018. Such trends favor the studied market's growth in the United States.

- Several government-led initiatives focused on leveraging the benefits of communication satellites also creates a favorable outlook for the growth of the studied market in North America. For Instance, in January 2022, the Minister of Innovation, Science and Technology of Canada announced a USD 8 million commitment in 21 organizations across Canada to explore new solutions that address Earth observation concerns and sustainable development priorities. The money will come from the Canadian Space Agency's (CSA) smartEarth program, which aims to push Canadian businesses to solve difficulties utilizing satellite data and help solve real-world concerns.

- Furthermore, the growing demand is encouraging the vendors to expand their offerings in the North American region which is also contributing to the growth of the studied market. For instance, in April 2023, Rogers Communications partnered with Lynk Global to test and deliver satellite-to-phone connectivity solutions across Canada.

Satellite Ground Equipment Industry Overview

The satellite ground equipment market is semi-consolidated owing to the presence of major players like Thales Group, Inmarsat Global Limited, Iridium Communications Inc., Gilat Satellite Networks Ltd, and Orbcomm Inc., as well as the growing entry of new players. Vendors in the market are adopting strategies such as innovations, partnerships, mergers, and acquisitions to enhance their product offerings and gain a sustainable competitive advantage.

- In May 2023, Low Earth Orbit satellite firm OneWeb is set to establish a ground station on the island of St. Helena and take ability on the island's trunk of the Equiano subsea cable. OneWeb has inscribed a 10-year ground station agreement with regional telco Sure. OneWeb is set to construct a ground station at Horse Point, with Sure set to manage the facility. The ground station will then be connected via fiber to the island's cable dock station at Rupert's Beach.

- In March 2023, India-based full-stack space-engineering solutions company Dhruva Space and France-based satellite operator and global connectivity provider Kineis have inked a Memorandum of Agreement (MoA), marking a collaboration where both organizations will collaborate to launch space and ground infrastructure to scale the variety and impact of satellite-based solutions. With nine satellites in orbit, Kineis' operational services provide global worldwide coverage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Internet of Things (IoT) and Autonomous Systems

- 5.1.2 Increasing Demand for Satellite Based Services

- 5.2 Market Restraints

- 5.2.1 Interference in Transmission of Data

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Ground Equipment

- 6.1.2 Service

- 6.2 By End-user Vertical

- 6.2.1 Maritime

- 6.2.2 Defense and Government

- 6.2.3 Enterprises

- 6.2.4 Media and Entertainment

- 6.2.5 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Thales Group

- 7.1.2 Inmarsat Global Limited

- 7.1.3 Iridium Communications Inc.

- 7.1.4 Gilat Satellite Networks Ltd

- 7.1.5 Orbcomm Inc.

- 7.1.6 Cobham SATCOM (Combham Limited)

- 7.1.7 Thuraya Telecommunications Company

- 7.1.8 ViaSat Inc.

- 7.1.9 ST Engineering iDirect

- 7.1.10 L3Harris Technologies Inc.

- 7.1.11 Advantech Wireless Technologies Inc. (Baylin Technologies)

- 7.1.12 KVH Industries Inc.