|

市場調査レポート

商品コード

1666572

衛星地上局の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Satellite Ground Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 衛星地上局の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月31日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

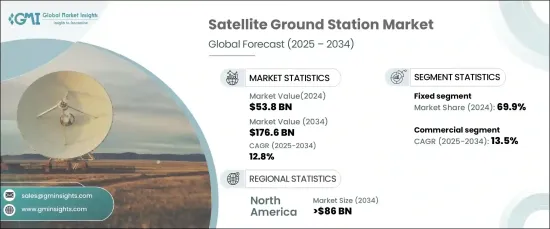

衛星地上局の世界市場は目覚ましい成長を遂げ、2024年には538億米ドルに達し、2025年から2034年までのCAGRは12.8%と予測されています。

この成長は、特に放送・通信分野での衛星を利用したサービス需要の急増によるところが大きいです。デジタルメディアが拡大を続ける中、ダイレクト・トゥ・ホーム(DTH)サービス、高画質放送、オーバー・ザ・トップ(OTT)プラットフォームの台頭により、シームレスな通信と効率的なデータトランスミッションを確保するための堅牢な地上局インフラに対する大きなニーズが生まれています。その他の特典として、遠隔通信、気象監視、全地球測位などの目的で衛星システムへの依存度が高まっていることが、最先端の衛星地上局の需要をさらに高めています。

技術の進歩も市場拡大の主な要因です。高スループット衛星(HTS)の採用は、衛星システムの容量を劇的に改善し、より高速で信頼性の高いデータ転送を可能にしました。これと並行して、アンテナ技術と自動化の革新が地上局の性能と運用効率を高めています。ソフトウェア定義ネットワーク(SDN)と人工知能(AI)の統合は、これらのステーションの運用方法に革命をもたらし、予知保全、リアルタイム監視、システム適応性の強化などの機能を導入しました。これらの技術的進歩により、衛星地上局は進化する通信需要への対応力を高め、サービス品質を維持しながら膨大なデータトラフィックを処理する能力を向上させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 538億米ドル |

| 予測金額 | 1,766億米ドル |

| CAGR | 12.8% |

市場セグメンテーションをプラットフォームタイプ別に見ると、2024年の市場シェアは固定地上局が69.9%を占め最大でした。これらの地上局は、通信、放送、地球観測を含む様々なアプリケーションにおいて、常に信頼性の高い衛星通信を維持するために不可欠です。固定衛星地上局は、安全で広帯域のデータトランスミッションを提供するため、継続的な運用が必要な政府、軍事、商業用途に不可欠です。

機能面では、通信分野が最も急成長しており、予測期間中のCAGRは13.5%と予測されています。通信に特化した地上ステーションは、衛星テレビ、インターネット接続、軍事通信システムなどの重要なサービスをサポートします。これらの地上局は、衛星と地上ネットワーク間の広帯域データ接続を保証するもので、従来のインフラが限られているか利用できない遠隔地では特に不可欠です。

地域別の成長を見ると、北米が衛星地上局市場を独占し、2034年までに860億米ドルに達する見込みです。特に米国は、確立された宇宙インフラ、継続的な技術進歩、通信・放送・地球観測における衛星サービスへの旺盛な需要から恩恵を受け、主要なプレーヤーとなっています。この地域の需要は、先進的な自動化システムの開発と、特に低軌道(LEO)における新しい衛星コンステレーションの台頭によってさらに増幅され、衛星地上局運用のさらなる革新と効率化を推進しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 衛星放送サービスの普及拡大

- 衛星地上局の継続的な技術進歩

- リモートセンシング用途での衛星サービス需要の増加

- 宇宙研究機関を支援する政府の積極的な取り組み

- 地球観測画像と分析ソリューションの普及

- 業界の潜在的リスク・課題

- 規制と政策の欠如

- 恒常的な帯域幅の問題

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- 機器

- アンテナシステム

- RFシステム

- データ処理ユニット

- テレメトリー・トラッキング&コマンド(TT&C)

- ソフトウェア

- サービスとしての地上局(GSaaS)

第6章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- 固定型

- 携帯型

- ハンドヘルド

- バッグマウント

- モバイル

第7章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- 通信

- 地球観測

- 宇宙調査

- ナビゲーション

- その他

第8章 市場推計・予測:周波数別、2021年~2034年

- 主要動向

- Lバンド(1GHzまで)

- 中周波数帯(1GHz~10GHz)

- Sバンド

- Cバンド

- Xバンド

- 高周波帯域(10 GHz~30 GHz)

- Ku帯

- Kaバンド

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 防衛

- 陸軍

- 空軍

- 海軍

- 政府機関

- 国土安全保障

- 行政

- 宇宙研究センター

- 大学・研究所

- 民間

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Airbus

- ESS Weathertech

- General Dynamics Mission Systems, Inc.

- Kongsberg Defence&Aerospace

- Kratos Defense &Security Solutions, Inc.

- L3Harris Technologies

- Lockheed Martin Corporation

- Mitsubishi Electric Corporation

- Orbit Communications Systems Ltd.

- Raytheon Technologies Corporation

- Safran Defense &Space, Inc.

- Swedish Space Corporation

- Telespazio S.p.A.

- Thales

- Viasat, Inc.

The Global Satellite Ground Station Market is poised for remarkable growth, reaching USD 53.8 billion in 2024, with projections indicating a strong CAGR of 12.8% from 2025 to 2034. This growth is largely driven by the surge in demand for satellite-based services, especially in the broadcasting and communication sectors. As digital media continues to expand, the rise of direct-to-home (DTH) services, high-definition broadcasting, and over-the-top (OTT) platforms has created a significant need for robust ground station infrastructure to ensure seamless communication and efficient data transmission. Additionally, the market is benefiting from the growing reliance on satellite systems for purposes such as remote communication, weather monitoring, and global positioning, further fueling the demand for cutting-edge satellite ground stations.

Technological advancements are another key driver for market expansion. The introduction of high-throughput satellites (HTS) has dramatically improved the capacity of satellite systems, enabling faster and more reliable data transfers. Alongside this, innovations in antenna technologies and automation have boosted the performance and operational efficiency of ground stations. The integration of software-defined networks (SDN) and artificial intelligence (AI) has revolutionized how these stations operate, introducing capabilities like predictive maintenance, real-time monitoring, and enhanced system adaptability. These technological strides have made satellite ground stations more responsive to evolving communication demands, increasing their ability to handle massive data traffic while maintaining service quality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $53.8 billion |

| Forecast Value | $176.6 billion |

| CAGR | 12.8% |

Market segmentation by platform type reveals that fixed ground stations held the largest market share in 2024, accounting for 69.9%. These stations are critical for maintaining constant and reliable satellite communications across various applications, including telecommunications, broadcasting, and Earth observation. Fixed satellite ground stations offer secure, high-bandwidth data transmission, making them indispensable for government, military, and commercial use, where continuous operations are a necessity.

On the functional side, the communication segment stands out as the fastest-growing, with a projected CAGR of 13.5% during the forecast period. Communication-focused ground stations support essential services such as satellite TV, internet connectivity, and military communication systems. These stations ensure high-bandwidth data connections between satellites and terrestrial networks, which is especially vital in remote areas where traditional infrastructure is limited or unavailable.

Looking at regional growth, North America is set to dominate the satellite ground station market, with expectations to reach USD 86 billion by 2034. The United States, in particular, is a key player, benefiting from its established space infrastructure, continuous technological advancements, and strong demand for satellite services in communication, broadcasting, and Earth observation. The demand in this region is further amplified by the development of advanced automated systems and the rise of new satellite constellations, particularly in Low Earth Orbit (LEO), driving further innovation and efficiency in satellite ground station operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increased penetration of satellite-based broadcasting services

- 3.6.1.2 Continuous technological advancements in satellite ground stations

- 3.6.1.3 Rising satellite service demand for remote sensing applications

- 3.6.1.4 Favorable government initiatives to support space research agencies

- 3.6.1.5 Proliferation of Earth observation imagery and analytics solutions

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Lack of regulations and government policies

- 3.6.2.2 Constant bandwidth issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Solution, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Equipment

- 5.2.1 Antennas systems

- 5.2.2 RF systems

- 5.2.3 Data processing units

- 5.2.4 Telemetry Tracking and Command (TT&C)

- 5.3 Software

- 5.4 Ground Station as a Service (GSaaS)

Chapter 6 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Fixed

- 6.3 Portable

- 6.3.1 Hand-Held

- 6.3.2 Bag-Mounted

- 6.4 Mobile

Chapter 7 Market Estimates & Forecast, By Functions, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Communication

- 7.3 Earth observation

- 7.4 Space research

- 7.5 Navigation

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Frequency, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 L-band (up to 1 GHz)

- 8.3 Medium-frequency bands (1 GHz to 10 GHz)

- 8.3.1 S-band

- 8.3.2 C-band

- 8.3.3 X-band

- 8.4 High-frequency bands (10 GHz to 30 GHz)

- 8.4.1 Ku-band

- 8.4.2 Ka-band

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Defense

- 9.2.1 Army

- 9.2.2 Air-Force

- 9.2.3 Navy

- 9.3 Government

- 9.3.1 Homeland security

- 9.3.2 Public administration

- 9.3.2.1 Space research centers

- 9.3.2.2 Universities and research labs

- 9.4 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Airbus

- 11.2 ESS Weathertech

- 11.3 General Dynamics Mission Systems, Inc.

- 11.4 Kongsberg Defence& Aerospace

- 11.5 Kratos Defense & Security Solutions, Inc.

- 11.6 L3Harris Technologies

- 11.7 Lockheed Martin Corporation

- 11.8 Mitsubishi Electric Corporation

- 11.9 Orbit Communications Systems Ltd.

- 11.10 Raytheon Technologies Corporation

- 11.11 Safran Defense & Space, Inc.

- 11.12 Swedish Space Corporation

- 11.13 Telespazio S.p.A.

- 11.14 Thales

- 11.15 Viasat, Inc.