|

市場調査レポート

商品コード

1445722

獣医参考研究所: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Veterinary Reference Laboratory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 獣医参考研究所: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 106 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

獣医基準検査室の市場規模は、2024年に49億7,000万米ドルと推定され、2029年までに78億6,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.58%のCAGRで成長します。

COVID-19のパンデミックにより、獣医学的疾患の研究開発活動と、ペットに必要なさまざまな医薬品の物流供給が混乱しました。例えば、2022年5月にフロンティアーズが発表した記事によると、英国では、犬がガンを含む慢性疾患と診断されると、パンデミック中にケアを求める確率が減少しました。これは、緊急でない問題の治療を受けることが困難だったことと獣医師へのアクセスが不足していたと報告されています。 しかし、COVID-19の感染者数が減少し、規制が緩和されたことにより、調査対象となった市場は長年にわたってその潜在力を最大限に取り戻すことが期待されています。

市場の成長を牽引する主な要因は、コンパニオンアニマル/ペットの養子縁組の増加、ペット保険の需要の増加、動物のヘルスケア費の増加、PCR検査、迅速検査、その他の検査手順の需要の増加です。

コンパニオンアニマルの採用の増加は、市場の成長を促進する主要な要因です。たとえば、「European Pet Food Industry: Facts and Figures 2022」レポートが発行したデータによると、2021年のドイツの犬の数は1,030万頭、猫は1,670万頭でした。同じ情報源によると、少なくとも1匹の猫を飼っているドイツの家庭の割合は21%で、2021年には犬1頭が19%でした。これは、人口の間で猫の養子縁組が犬よりも高かったことを示しています。

さらに、2022年に発表されたペットフード製造業者協会(PFMA)の2022年ペット数データによると、2022年には英国で3,490万匹のペットがいると推定されています(犬1,300万匹、猫1,200万匹)。同様に、2022年に欧州ペットフード産業:事実と数字2021が発表したデータによると、2021年に英国で1,200万頭の犬と1,200万頭の猫が報告されました。同じ情報源によると、少なくともペットフードを所有している英国の世帯の推定割合は、 2021年には、猫 1頭が33%、犬1頭が27%でした。したがって、ペットの受け入れの増加により、獣医基準検査機関の需要が増加すると予想されます。

主要市場企業による発展により、市場の成長が促進されると予想されます。たとえば、2021年 9月、Heska Corporationは、迅速アッセイ診断検査の大手開発者であるBiotech Laboratories USA LLCの過半数の所有権を取得しました。

したがって、ペットの採用の増加や主要市場企業による開発の増加などの要因が市場の成長を促進すると予想されます。しかし、ポイントオブケア(POC)サービス用のポータブルデバイスの需要の高まりとペットの世話費用の高騰が、この成長を妨げると予想されます。

獣医基準研究所の市場動向

コンパニオンアニマルセグメントは、予測期間中にかなりの市場シェアを保持すると予想されます

コンパニオンアニマル部門は、コンパニオンアニマルにおける慢性疾患や感染症の罹患率の高さ、ペットの採用の増加、平均寿命の延長により病気のリスクがさらに高まっていることから、獣医基準検査市場で大きなシェアを占めると予想されています。例えば、2021年3月にFrontiersが発表した記事によると、犬の主な死因はがんであると考えられているが、これは多くの症例が臨床症状が発現した進行段階で特定され、予後が不良であることも一因となっています。したがって、コンパニオンアニマルにおけるがんの有病率の上昇により、獣医学参考検査機関の利用が増加すると予想されます。

2022年 11月にオーストラリア動物医薬品(AMA)が発表したデータによると、オーストラリアはペットの健康、栄養、十分なアクセサリーを維持するために年間330億米ドル以上を費やしています。 330億米ドルの支出のうち、14%が獣医師に、9%がヘルスケア製品に費やされています。同じ情報源によると、2022年のオーストラリアにおける獣医師サービスと犬のヘルスケア製品に対する年間世帯支出はそれぞれ631ドルと323ドルでした。同様に、猫の獣医師サービスとヘルスケア製品に対する年間世帯支出は388ドルと388ドルでした。したがって、ペットケア支出の増加もこの部門の成長を促進すると予想されます。

European Pet Food Industry:Facts and Figures 2021レポートが発行したデータによると、2021年にドイツでは1,030万匹の犬と1,670万匹の猫が報告されました。同じ情報源によると、少なくとも1匹の猫を飼っているドイツの家庭の割合は21%でした。 2021年には犬1頭が19%でした。これは、人口の間で猫の養子縁組率が犬よりも高かったことを示しています。

2022年に更新されたドイツハイムティアマルクトのデータによると、2021年にはドイツの世帯の47%がペットを飼っており、その中には3,470万匹の犬、猫、小動物、観賞用の鳥が含まれています。また、同じ情報源によると、ドイツでは犬の引き取り数に比べて猫の引き取り数が多かったそうです。ドイツの世帯の26%には約1,670万匹の猫が住んでいます。一方、世帯の21%には1,030万匹の犬が住んでいます。したがって、ペットの普及の増加もセグメントの成長を促進すると予想されます。

したがって、コンパニオンアニマルにおけるさまざまな慢性疾患や感染症の有病率の上昇やペットの採用の増加などの要因が、この部門の成長を後押しすると予想されます。

北米は予測期間中にかなりの市場シェアを持つと予想される

北米地域は長年にわたって獣医基準市場で大きなシェアを占めており、動物個体数(特にペット)の多さと病気の負担の増加、より良い獣医ケアの存在、および獣医ケアの存在により、予測期間中も同様の傾向を示すと予想されています。サービスの向上と、この地域の獣ヘルスケア支出の増加。

2022年 9月のカナダ動物衛生研究所(CAHI)のデータによると、2022年にはカナダの世帯の半数以上(60%)が少なくとも1匹の犬または猫を飼っていました。データはまた、犬の数が790万匹に増加したことも詳細に示しています。ネコの数は2022年には850万頭まで増加しました。したがって、動物の数ベースが大きいため、動物のがんの負担はより高くなることが予想され、それがこの地域の成長を促進すると予想されます。

北米では、米国はこの地域で最も多くの動物の数を擁する国の一つであり、動物医療費が高く、動物がん症例の負担が大きいため、獣医腫瘍学市場で大きなシェアを握ると予想されています。たとえば、2021年から2022年の米国ペット製品協会(APPA)の全国ペット所有者調査によると、米国の世帯の約70%、つまり約9,050万世帯がペットを所有しており、猫と犬は合計でペットを飼っている主要なペットでした。人口はそれぞれ4,530万人と6,900万人。同情報源によると、ペットの飼い主は獣医の外科受診に犬に約458ドル、猫に約201ドルを費やし、定期的な獣医の診察には犬と猫にそれぞれ242ドルと178ドルを費やしたといいます。このデータは、この国に多くのペットが存在し、ペットに対する支出が他の地域と比べて通常高いことを示しています。

主要市場企業による発展も市場の成長を促進すると予想されます。たとえば、2021年 12月、Neogen Corporationはワシントンに本拠を置くコンパニオンアニマルの遺伝子検査会社Genetic Veterinary Sciences Inc.を買収しました。

したがって、動物のさまざまな病気の有病率の上昇、ペットの採用の増加、主要市場企業による開発の増加などの要因が、この地域の市場の成長を促進すると予想されます。

獣医基準研究所業界の概要

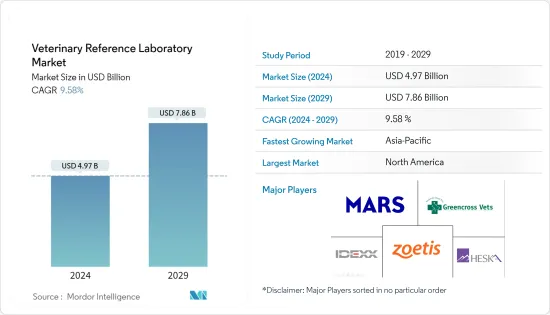

市場は本質的に適度に統合されています。主要市場企業は、より高い競争力を獲得するために、地域拡大戦略、合併・買収、共同調査イニシアチブなどの重要なビジネス戦略に取り組んできました。主要な企業には、IDEXX Laboratories Inc.、GD Animal Health、Greencross Limited、Heska Corporation、Zoetis Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- コンパニオンアニマル/ペットの養子縁組の増加

- ペット保険の需要の増加

- 動物ヘルスケア費の増大

- PCR検査、迅速検査、その他の検査手順の需要の増大

- 市場抑制要因

- ポイントオブケア(POC)サービス用のポータブルデバイスの需要の高まり

- 高額なペットの世話費用

第5章 市場セグメンテーション

- サービスの種類別

- 臨床化学

- 血液学

- 免疫診断

- 分子診断学

- その他のサービスタイプ

- 用途別

- 病理学

- 細菌学

- ウイルス学

- 寄生虫学

- その他の用途

- 動物の種類別

- コンパニオンアニマル

- 家畜

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 企業プロファイルと競合情勢

- 企業プロファイル

- IDEXX Laboratories Inc.

- GD Animal Health

- Greencross Limited

- Heska Corporation

- Zoetis Inc.

- Mars Inc.

- Neogen Corporation

- Boehringer Ingelheim International GmbH

- Veterinary Diagnostic Laboratory-University of Minnesota

第7章 市場機会と将来の動向

The Veterinary Reference Laboratory Market size is estimated at USD 4.97 billion in 2024, and is expected to reach USD 7.86 billion by 2029, growing at a CAGR of 9.58% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the R&D activities of veterinary diseases and the logistics supply of various essential pharmaceutical products for pets. For instance, according to an article published by Frontiers in May 2022, in the United Kingdom, a dog's chronic illness diagnosis, including cancer, reduced the odds of seeking care during the pandemic, reportedly due to difficulties in accessing care for non-urgent issues and lack of access to veterinarians. However, with the declining COVID-19 cases and ease of restrictions, the studied market is expected to regain its full potential over the years.

The major factors driving the growth of the market are the increase in companion animal/pet adoption, the increasing demand for pet insurance, the growing animal healthcare expenditure, and the growing demand for PCR testing, rapid testing, and other testing procedures.

The rising adoption of companion animals is a major factor driving the market's growth. For instance, according to the data published by the European Pet Food Industry: Facts and Figures 2022 report, Germany had 10,300,000 dogs and 16,700,000 cats in 2021. As per the same source, the percentage of German households owning at least one cat was 21%, and one dog was 19% in 2021. This shows that the adoption of cats was higher among the population than dogs.

Additionally, as per the Pet Food Manufacturer's Association (PFMA)'s Pet Population 2022 data published in 2022, 34.9 million pets were estimated in the United Kingdom in 2022 (13 million dogs and 12 million cats). Similarly, according to the data published by the European Pet Food Industry: Facts and Figures 2021 in 2022, 12,000,000 dogs and 12,000,000 cats were reported in the United Kingdom in 2021. As per the same source, the estimated percentage of UK households owning at least one cat was 33%, and one dog was 27% in 2021. Thus, the increasing adoption of pets is expected to increase the demand for veterinary reference laboratories.

The developments by key market players are expected to increase the market's growth. For instance, in September 2021, Heska Corporation acquired majority ownership of Biotech Laboratories USA LLC, a leading developer of rapid assay diagnostics testing.

Thus, factors such as the rising pet adoption and the increasing developments by key market players are expected to boost the market's growth. However, rising demand for portable devices for point-of-care (POC) services and high pet care costs are expected to hinder this growth.

Veterinary Reference Laboratory Market Trends

Companion Animal Segment is Expected to Hold a Significant Market Share Over the Forecast Period

The companion animal segment is expected to hold a major share of the veterinary reference laboratory market due to the high prevalence of chronic and infectious diseases in companion animals, growing pet adoption, and increasing life expectancy, further increasing the risk of diseases. For instance, according to an article published by Frontiers in March 2021, cancer is considered the leading cause of death in dogs, partly because many cases are identified at an advanced stage when clinical signs have developed and the prognosis is poor. Thus, the rising prevalence of cancer in companion animals is expected to increase the usage of veterinary reference laboratories.

According to the data published by Animal Medicines Australia (AMA) in November 2022, Australia spends over USD 33 billion annually to keep pets healthy, nourished, and well-accessorized. Out of the USD 33 billion spending, 14% is spent on veterinarians and 9% on healthcare products. According to the same source, the annual household spending for veterinarian services and healthcare products for dogs was USD 631 and USD 323, respectively, in Australia in 2022. Similarly, the annual household spending for veterinarian services and healthcare products for cats was USD 388 and USD 280, respectively, in Australia in 2022. Thus, the rising pet care expenditure is also expected to enhance the segment's growth.

According to the data published by the European Pet Food Industry: Facts and Figures 2021 report, 10,300,000 dogs and 16,700,000 cats were reported in Germany in 2021. As per the same source, the percentage of German households owning at least one cat was 21%, and one dog was 19% in 2021. This shows that the adoption of cats was higher among the population than dogs.

According to Der Deutsche Heimtiermarkt data, updated in 2022, 47% of the households in Germany had pets in 2021, including 34.7 million dogs, cats, small animals, and ornamental birds. Also, as per the same source, the number of cats adopted was higher in Germany compared to the adoption of dogs. About 16.7 million cats live in 26% of German households, compared to 10.3 million dogs in 21% of households. Thus, the rising pet adoption is also expected to boost segment growth.

Hence, factors such as the rising prevalence of various chronic and infectious diseases in companion animals and the growing pet adoption are expected to boost the segment's growth.

North America is Expected to Have a Significant Market Share Over the Forecast Period

The North American region has held a significant share in the veterinary reference market over the years and is expected to show the same trend over the forecast period due to the large animal population (especially pets) and increasing disease burden, presence of better veterinary care and services, and increasing veterinary healthcare expenditure in the region.

According to the data from the Canadian Animal Health Institute (CAHI) in September 2022, more than half of Canadian households (60%) owned at least one dog or cat in 2022. The data also detailed that the dog population increased to 7.9 million while the cat population increased to 8.5 million in 2022. Thus, with a large population base of animals, the burden of cancer among animals is expected to be higher, which is anticipated to drive growth in the region.

In North America, the United States is expected to hold a significant share of the veterinary oncology market as the country has one of the highest numbers of animals in the region, coupled with high animal health expenditure and a high burden of animal cancer cases. For instance, according to the 2021-2022 American Pet Product Association (APPA) National Pet Owners Survey, about 70% of the US households owned a pet, i.e., about 90.5 million homes, and cats and dogs were the major pets with a total population of 45.3 million and 69 million, respectively. As per the same source, pet owners spent about USD 458 for dogs and USD 201 for cats for surgical vet visits, and for the routine vet, they spent USD 242 and USD 178 for dogs and cats, respectively. This data shows the presence of a large pet population in the country and spending on them, which is usually high compared to other regions.

The developments by key market players are also expected to boost the market's growth. For instance, in December 2021, Neogen Corporation acquired a Washington-based companion animal genetic testing company Genetic Veterinary Sciences Inc.

Hence, factors such as the rising prevalence of various diseases in animals, the growing pet adoption, and the increasing developments by key market players are expected to boost the market's growth in the region.

Veterinary Reference Laboratory Industry Overview

The market is moderately consolidated in nature. The key market players have undertaken crucial business strategies like regional expansion strategies, mergers and acquisitions, and collaborative research initiatives to gain a higher competitive edge. Some of the key players are IDEXX Laboratories Inc., GD Animal Health, Greencross Limited, Heska Corporation, and Zoetis Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Companion animal/Pet Adoption

- 4.2.2 Increasing Demand for Pet Insurance

- 4.2.3 Growing Animal Healthcare Expenditure

- 4.2.4 Growing Demand for PCR testing, Rapid Testing, and Other Testing Procedures

- 4.3 Market Restraints

- 4.3.1 Rising Demand for Portable Devices for Point-of-care (POC) Services

- 4.3.2 High Pet Care Cost

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Service Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Haematology

- 5.1.3 Immunodiagnostics

- 5.1.4 Molecular Diagnostics

- 5.1.5 Other Service Types

- 5.2 By Application

- 5.2.1 Pathology

- 5.2.2 Bacteriology

- 5.2.3 Virology

- 5.2.4 Parasitology

- 5.2.5 Other Applications

- 5.3 By Animal Type

- 5.3.1 Companion Animal

- 5.3.2 Livestock Animal

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPANY PROFILES AND COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IDEXX Laboratories Inc.

- 6.1.2 GD Animal Health

- 6.1.3 Greencross Limited

- 6.1.4 Heska Corporation

- 6.1.5 Zoetis Inc.

- 6.1.6 Mars Inc.

- 6.1.7 Neogen Corporation

- 6.1.8 Boehringer Ingelheim International GmbH

- 6.1.9 Veterinary Diagnostic Laboratory-University of Minnesota