|

|

市場調査レポート

商品コード

1548897

ゲームの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゲームの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

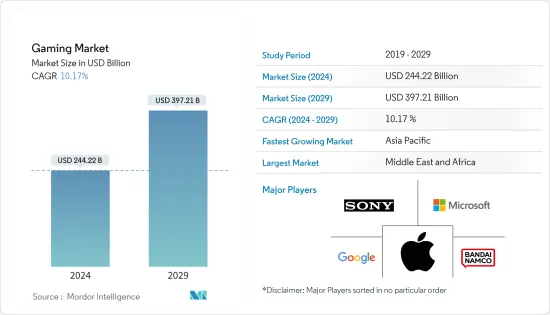

世界のゲームの市場規模は、2024年に2,442億2,000万米ドルと推定され、2029年には3,972億1,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR10.17%で成長すると予測されています。

主なハイライト

- 世界のゲーム業界は、インターネット接続の増加、スマートフォンの普及拡大、5Gのような広帯域ネットワークの導入より需要が増加しています。また、複数の通信事業者が商用5Gサービスを開始し、人口普及率も高まっていることから、モバイルベンダーが5Gスマートフォンを市場に投入する新たな機会が生まれています。

- ゲーム業界における継続的な技術進歩も、業界の成長を大きく後押ししています。これらの技術進歩は、ゲームの作成方法を向上させ、ユーザーの全体的なゲーム体験を向上させます。新興経済諸国のゲーム開発者は、ゲーム体験の向上に絶えず努めています。プレイステーション、Xbox、Windows PCなど、さまざまなプラットフォーム向けのコードを開発し、最適化することで、これを実現しています。このような努力の結果、クラウドプラットフォームを通じてゲーマーに統一された製品が提供されます。

- NewGenAppsによると、2025年までにARおよびVRゲームの世界のユーザー数は2億1,600万人に増加すると推定されています。テクノロジー企業幹部、新興企業創業者、投資家を対象とした世界規模の調査によると、回答者の59%がVR(仮想現実)技術開発への投資はゲームが主流になると考えています。また、暗号通貨が世界の現象であり続ける中、ゲーム開発者がゲーム内製品、化粧品、アンロックされたキャラクターの購入や取引に暗号通貨を活用する新しい方法を考案しているように、世界中のさまざまな業界が自社の製品やサービスに暗号通貨を組み込む方法を見出しています。

- ゲーム市場のシェアは、eスポーツのようなゲームプラットフォームの導入が増加していることが大きな要因となっています。eスポーツは、現在の市場シナリオにおいて市場シェアが大幅に増加しており、それによって世界中のゲーム産業全体を牽引しています。eスポーツ市場全体は今後数年間で成長すると予想されています。eスポーツの観客とプレイヤーの大半はミレニアル世代です。そのため、eスポーツのパブリッシャーは、ゲームプレイ体験をパーソナライズし、コンソール、PC、モバイルを通じてさまざまなプラットフォームでゲームを提供することで、これらの顧客をターゲットにしています。

- ゲーム業界では、非代替性トークン(NFT)が急増し、P2E(Play-to-Eearn)モデルの採用が拡大しています。これらの動向は、ゲーム開発、ゲームプレイ、収益の流れを再構築し、プレイヤーや開発者に交流と収益の新たな機会を提供しています。

- ゲーム業界の動向によると、同市場では著作権侵害や偽ゲームサイトなどの詐欺事件が増加しています。新たな進化を遂げる不正動向により、オンラインゲームをはじめとする業界全体でアカウント乗っ取り攻撃が増加しています。ゲームのハッキングはさらに増加しており、その結果、顧客アカウントに関連する詐欺や個人情報の盗難が発生しています。

ゲーム業界の動向

コンソールゲームのゲームタイプセグメントが大きな市場シェアを占める

- 過去数年間、ゲーマー層の拡大と継続的な技術の進歩・向上により、ゲーム機の需要は着実に増加しています。ゲームの数や種類が多様化したことで、消費者がゲームに費やす時間は増加しています。さらに、ユニークなゲームやゲームコンテンツも継続的に生み出されています。

- ZarkCentralが共有したデータによると、消費者がゲームに費やす時間は増加しており、世界平均で週7.11時間となっています。欧州諸国のゲーマーが最もゲームに費やす時間が長く、1週間あたり約7.98時間でした。adjoe GmbHによると、ゲーマーはシミュレーションゲームアプリで毎日平均20分を費やしています。さらに、ゲームの数や種類は年々多様化しています。

- 2023年、Googleとインドのゲームに特化したベンチャー・キャピタル・ファンドであるLumikaiの調査によると、インドのゲーマーはリアルマネーゲームに週平均4.7時間を費やし、最も高いエンゲージメントを示しました。これに対し、ハイパーカジュアルゲームは週平均2.6時間に過ぎません。

- 現在、多くのゲームがハードウェアを必要とし、家庭用ゲーム機がブラウジングや他のさまざまなアプリケーションの提供など多目的に使用されるようになったことが、ゲーム産業の成長をさらに後押ししています。4Kや8Kテレビなど、複数の提供アクセサリーをサポートする製品の発売は、家庭用ゲーム機の需要を効果的に押し上げています。家庭用ゲーム機は、他の選択肢よりも優れたゲーム体験を提供します。

- ビデオゲーム会社と消費者は、物理的なゲームディスクから離れ、デジタルダウンロードの利便性を好み続けています。マイクロソフト、ソニー、任天堂などの大手ゲーム会社は、オンラインサービスに加入している人に無料でデジタルゲームを提供しています。複数の企業が、ゲームを購入・プレイするための新しいプラットフォームやサービスを開発しています。

アジア太平洋が最大の市場に

- アジア太平洋には、中国、日本、韓国のような先進技術ハブから、インド、インドネシアなどの新興経済諸国まで、多様な経済諸国が存在します。この多様性が、多様な消費者の嗜好や消費能力を活用しようとするゲーム企業にとって有利な環境を生み出しています。

- そのため、この地域の企業は、この地域のゲーマー数の増加に対応するため、新しいゲーム製品やソフトウェアを継続的に発表しています。例えば2024年5月、AsusはAMDの最新チップを搭載した新しいハンドヘルドゲーム機「Rog Ally」を発売したと発表しました。同社はまた、より良いユーザー体験を提供するために、より大きなバッテリーとより優れた熱源を搭載するとしています。

- 2023年12月にも、テンセント・ホールディングスは大予算のコンソールゲーム「ラストセンチネル」を発表しました。 テンセントは国際市場への進出、中国の消費者の嗜好の変化への対応、大予算のコンソールゲームへのリソースの投入に注力しています。こうした動きは、同地域でゲームソリューションに対する需要が高まっていることを示しています。

- 技術革新、モバイルゲームの人気の高まり、eスポーツへの関心の高まりは、日本市場を大きく牽引しています。アクセスが容易で手ごろな価格のモバイルゲームは、日本でのゲーム普及率を高め、モバイルゲーム開発者にとって有利な市場となっています。この勢いは、多人数参加型ゲームがソーシャル・メディア・プラットフォームと統合され、プレイヤー間のコミュニティやつながりを育むソーシャルゲームの台頭によってさらに加速しています。

- 複数の世界ゲーム企業が、提携や買収などの戦略的イニシアティブを通じて日本市場に参入しています。たとえば、小島プロダクションは2024年2月、映画とゲームの要素を組み合わせたまったく新しいIPであるアクション・スパイゲームを開発中であると発表しました。同社はこのゲームをソニーと共同で開発する予定です。

ゲーム市場概要

ゲーム市場のシェアは、ソニー、マイクロソフト、任天堂、テンセント・ホールディングス・リミテッド、エレクトロニック・アーツなどの大手ゲーム会社によって高度に統合されています。コンソールゲームの最大手企業は、ソニー(プレイステーション)、マイクロソフト(Xbox)、任天堂(Switch)です。これらのゲーム会社は研究開発に投資し、ゲーマーに高品質のグラフィックス、高い演算能力、高速性を提供する技術を開発しています。ゲーム機の販売台数では、2023年にはソニーのプレイステーションPS5が約2,090万台で市場をリードし、任天堂(Switch)が1,797万台、Xbox XSが314万台で続きます(2023年9月)。他のゲーム会社もゲームやeスポーツ業界に参入しています。

例えば、2023年11月、世界のデベロッパーおよびパブリッシャーであるNCSOFTは、ソニー・インタラクティブエンタテインメント(SIE)と提携しました。この提携は、モバイル分野を中心に複数のグローバルな事業領域にまたがります。ソニーにとって、NCSOFTとの提携は極めて重要な動きであり、PlayStationブランドの影響力をコンソールの枠を超えて拡大し、より多様なユーザーをターゲットにするというビジョンに沿ったものです。

2023年8月、バンダイナムコとゲーム中心のブロックチェーンネットワークであるOasysは、AI主導のバーチャルペットゲームを開発するために協力しました。ゲームの中心となるのは、NFTベースのデジタルクリーチャー「RYU」です。アイコニックな「たまごっち」からインスピレーションを得たRYUは、ユーザーとのインタラクションに応じてユニークな個性と能力を発揮します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- インターネット普及率の上昇

- クラウドゲームの出現

- eスポーツベッティングやファンタジーサイトなどのゲームプラットフォームの採用

- 市場抑制要因

- 著作権侵害、法規制、ゲーム取引中の不正行為に関する懸念などの問題

第6章 市場セグメンテーション

- ゲームタイプ別

- モバイルゲーム

- コンソールゲーム

- ダウンロード/ボックスPC

- eスポーツ

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- アジア

- 中国

- 日本

- 韓国

- オーストラリアとニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イラン

- エジプト

- 北米

第7章 競合情勢

- 企業プロファイル

- Sony Corporation

- Microsoft Corporation

- Apple Inc.

- Realnetworks LLC(Gamehouse)

- Bandai Namco Holdings Inc.

- Take-Two Interactive Software Inc.

- Nexon Co. Ltd

- Nintendo Co. Ltd

- Beijing Elex Technology Co. Ltd

- Electronic Arts Inc.

- Ubisoft Entertainment SA

- Square Enix Holdings Co. Ltd

- ZeptoLab UK limited

- Tencent Holdings Ltd

- Sega Sammy Holdings Inc.

- Capcom Co. Ltd

- NetEase Inc.

- 37 Interactive Entertainment

- Jam City Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Gaming Market size is estimated at USD 244.22 billion in 2024, and is expected to reach USD 397.21 billion by 2029, growing at a CAGR of 10.17% during the forecast period (2024-2029).

Key Highlights

- The global gaming industry is experiencing increased demand due to rising internet connectivity, growing smartphone adoption, and the introduction of high-bandwidth networks like 5G. In addition, several operators have launched commercial 5G services with significant population penetration, opening new opportunities for mobile vendors to introduce 5G smartphones in the market.

- The continuous technological advancements in the gaming industry are also significantly propelling the industry's growth. They enhance the way games are created and improve users' overall gaming experience. Game developers in emerging economies continually strive to enhance the gaming experience. They achieve this by developing and optimizing codes for various platforms, including PlayStation, Xbox, and Windows PC. These efforts result in a unified product delivered to gamers via cloud platforms.

- According to NewGenApps, by 2025, the global user base of AR and VR games is estimated to increase to 216 million. According to a worldwide survey of technology company executives, startup founders, and investors, 59% of the respondents believe gaming will dominate the investment in developing VR (Virtual Reality) technology. In addition, as cryptocurrency continues to be a global phenomenon, various industries across the world are identifying ways to incorporate crypto into their products and services as game developers are inventing new methods to leverage cryptos for purchasing and trading in-game products, cosmetics, and unlocked characters.

- The gaming market share is significantly driven by the rising adoption of gaming platforms like E-sports. E-sports are witnessing a significant increase in market share in the current market scenario, thereby driving the overall gaming industry across the world. The entire e-sports market is anticipated to grow over the coming years. Most of the audience and players of E-sports are millennials. Thus, esports publishers target these customers by personalizing the gameplay experience and offering the game on different platforms through the console, PC, and mobile.

- The gaming industry is witnessing a surge in Non-Fungible Tokens (NFTs) and a growing adoption of the play-to-earn (P2E) model. These trends are reshaping game development, gameplay, and revenue streams, providing players and developers with fresh opportunities for interaction and income.

- According to gaming industry trends, the market is witnessing rising fraud cases, such as copyright infringement and fake gaming sites, among others. Emerging and evolving fraud trends are increasing account takeover attacks across industries, especially online gaming. Game hacking is further increasing, resulting in fraud related to customer accounts and personal identity thefts.

Gaming Industry Trends

Console Games Gaming Type Segment Holds Significant Market Share

- Over the past few years, the demand for gaming consoles has steadily increased, driven by a growing gamer base and ongoing technological advancements and improvements. The amount of time consumers spend on gaming has increased as the number of games and the variety are diversified. Moreover, unique games and gaming content are also being created continuously.

- According to the data shared by ZarkCentral, the amount of time consumers spend on gaming is rising, with the global average being 7.11 hours per week. Gamers in European countries spent the most time gaming, with almost 7.98 hours per week. As per adjoe GmbH, gamers spent 20 minutes daily on average with the simulation gaming app. Moreover, the number of games and the variety have diversified over the years.

- In 2023, Indian gamers, as per a survey by Google and Lumikai, an Indian gaming-focused venture capital fund, devoted an average of 4.7 hours weekly to real-money gaming, marking the highest engagement. In comparison, hyper-casual games saw an average of just 2.6 hours per week.

- Currently, the hardware requirement of many games and the multipurpose use of home consoles for purposes such as browsing, providing various other applications, etc., have further enabled gaming industry growth. The release of supportive multiple provision accessories, such as 4K and 8K TVs, effectively drives the demand for home consoles. They provide a better gaming experience than other options available.

- Video game companies and consumers continue to move away from physical game disks and prefer the convenience of digital downloads. Major gaming companies, such as Microsoft, Sony, and Nintendo, offer free digital games to people who are subscribed to their online services. Multiple companies are developing new platforms and services to buy and play games.

Asia Pacific to be the Largest Market

- Asia-Pacific encompasses diverse economies, from advanced technological hubs like China, Japan, and South Korea to rapidly developing nations such as India, Indonesia, and others. This diversity creates a favorable environment for gaming companies looking to capitalize on varied consumer preferences and spending capacities.

- Hence, companies in the region are continuously launching new gaming products and software to accommodate the growing number of gamers in the region. For instance, in May 2024, Asus announced that it had launched a new handheld gaming console, Rog Ally, equipped with the latest chip from AMD. The company also said it will come with a bigger battery and better thermals to provide a better user experience.

- Again, in December 2023, Tencent Holdings introduced Last Sentinel, a big-budget console game. Tencent focuses on expanding into the international market, catering to Chinese consumers' changing preferences, and engaging resources in big-budget console games. These developments indicate the growing demand for gaming solutions in the region.

- Technological innovations, the growing popularity of mobile gaming, and the soaring interest in E-sports majorly drive the market in Japan. With its ease of access and affordability, mobile gaming has increased the gaming penetration rate in Japan, making it a lucrative market for mobile game developers. This momentum is further fueled by the rise of social gaming, where multiplayer games are integrated with social media platforms, fostering community and connectedness among players.

- Several global gaming companies have entered the Japanese market through strategic initiatives such as partnerships and acquisitions. For instance, in February 2024, KOJIMA PRODUCTIONS Co. Ltd announced that it has an action espionage game in the pipeline, a brand-new IP combining film and gaming elements. The company plans to develop this game in collaboration with Sony.

Gaming Market Overview

The gaming market share is highly consolidated with the biggest gaming companies like Sony, Microsoft, Nintendo, Tencent Holdings Limited, and Electronic Arts Inc., among others. The biggest companies in the console gaming landscape are Sony (PlayStation), Microsoft (Xbox), and Nintendo (Switch). These gaming companies are investing in R&D and developing technology that offers gamers high-quality graphics, high computing power, and faster speed. In terms of console units sold, in 2023, Sony's PlayStation PS5 led the market with around 20.9 million units sold, followed by Nintendo (Switch) with 17.97 million units and Xbox XS 3.14 million units (September 2023). Other gaming companies are also entering the gaming and esports industry.

For instance, in November 2023, NCSOFT, a global developer and publisher, partnered with Sony Interactive Entertainment (SIE). This collaboration spans multiple global business domains, focusing on the mobile sector. For Sony, teaming up with NCSOFT is a pivotal move, aligning with its vision to extend the PlayStation brand's influence beyond consoles, targeting a more diverse audience.

In August 2023, Bandai Namco and Oasys, a gaming-centric blockchain network, collaborated to develop an AI-driven virtual pet game. The game centers around a set of NFT-based digital creatures named RYU. Drawing inspiration from the iconic Tamagotchi, these RYU creatures evolve unique personalities and abilities in response to user interactions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Internet Penetration

- 5.1.2 Emergence of Cloud Gaming

- 5.1.3 Adoption of Gaming Platforms, such as E-sports Betting and Fantasy Sites

- 5.2 Market Restraints

- 5.2.1 Issues such as Piracy, Laws and Regulations, and Concerns Relating to Fraud During Gaming Transactions

6 MARKET SEGMENTATION

- 6.1 By Gaming Type

- 6.1.1 Mobile Games

- 6.1.2 Console Games

- 6.1.3 Downloaded/Box PC

- 6.1.4 E-sports

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Russia

- 6.2.2.5 Spain

- 6.2.2.6 Italy

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 South Korea

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Mexico

- 6.2.6 Middle East and Africa

- 6.2.6.1 United Arab Emirates

- 6.2.6.2 Saudi Arabia

- 6.2.6.3 Iran

- 6.2.6.4 Egypt

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Sony Corporation

- 7.1.2 Microsoft Corporation

- 7.1.3 Apple Inc.

- 7.1.4 Realnetworks LLC (Gamehouse)

- 7.1.5 Bandai Namco Holdings Inc.

- 7.1.6 Take-Two Interactive Software Inc.

- 7.1.7 Nexon Co. Ltd

- 7.1.8 Nintendo Co. Ltd

- 7.1.9 Beijing Elex Technology Co. Ltd

- 7.1.10 Electronic Arts Inc.

- 7.1.11 Ubisoft Entertainment SA

- 7.1.12 Square Enix Holdings Co. Ltd

- 7.1.13 ZeptoLab UK limited

- 7.1.14 Tencent Holdings Ltd

- 7.1.15 Sega Sammy Holdings Inc.

- 7.1.16 Capcom Co. Ltd

- 7.1.17 NetEase Inc.

- 7.1.18 37 Interactive Entertainment

- 7.1.19 Jam City Inc.