|

市場調査レポート

商品コード

1445432

ヒトインスリン医薬品および投与装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Human Insulin Drugs and Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヒトインスリン医薬品および投与装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

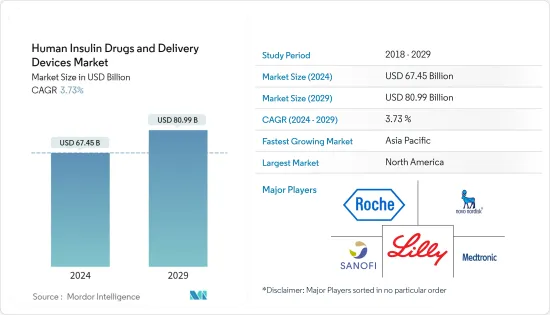

ヒトインスリン医薬品および投与装置の市場規模は、2024年に674億5,000万米ドルと推定され、2029年までに809億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.73%のCAGRで成長します。

糖尿病は、COVID-19増加の危険因子と考えられています。COVID-19のパンデミック中、糖尿病患者の感受性を低く保ち、COVID-19の重篤な経過を防ぐためには、血糖値を厳密に管理し、COVID-19合併症を予防することが重要である可能性があります。COVID-19は、インスリン薬の頻繁な使用と導入装置市場の増加により、主に糖尿病患者の糖代謝に影響を及ぼします。

糖尿病は一般的に生活習慣病と考えられています。時間が経つにつれて、世界中で人口が増加するにつれて、この病気の発生率は法外に増加しました。世界中で約1億人がインスリンを必要としています。その中には1型糖尿病に苦しむすべての人々と2型糖尿病の10~25%が含まれます。インスリンは90年以上にわたって糖尿病の治療に使用されてきましたが、世界的には、今日インスリンを必要とする人の半数以上が依然としてインスリンを購入する余裕がなく、アクセスすることができません。 1型糖尿病患者は体内でインスリンを生成しないため、インスリン薬と投与装置が必要です。2型糖尿病患者、特に経口薬で糖尿病をコントロールすることが難しい患者にもインスリンが必要です。

ヒトインスリン医薬品および投与装置の市場動向

1型糖尿病人口が予測期間に市場を牽引

1型糖尿病人口は、予測期間中に2%以上のCAGRで推移すると予想されます。

1型糖尿病の正確な原因は不明ですが、2型糖尿病は日々のライフスタイルの変化や選択によって引き起こされます。 2型糖尿病の有病率は10年前と比較して4倍になっています。 1型糖尿病(T2DM)の有病率は過去20年間で劇的に増加しましたが、これはT1DMの主な危険因子である肥満の発生率の増加によって引き起こされています。糖尿病は、米国で最も急速に増加している慢性疾患の1つです。インドは糖尿病の罹患率が高い国のトップ 3に入っています。多くの報告書や調査で、生活習慣に基づく糖尿病人口の急激な増加が記録されています。

経口抗糖尿病薬は2型糖尿病患者の標準治療とみなされていますが、血糖値の安定化を図るために従来の薬物療法と併用してインスリンを使用する必要性が高まっています。この傾向により、国内外の多くのプレーヤーがバイオシミラー市場に参入するようになっています。

インスリン分野の研究開発は、研究者が患者の使用に最適な分子を導き出し、最大限の副作用を抑制し、効率を高めようとしているため、年々増加しています。したがって、世界中で肥満と糖尿病の有病率が増加することにより、インスリンの需要が増大し、それがインスリン薬および装置の市場を牽引する可能性があります。

北米はヒトインスリン医薬品および投与装置市場を独占すると予想されています。

北米は、インスリン価格が高いにもかかわらず、ヒト用インスリン医薬品および投与装置市場を独占しています。 RANDの研究者によると、インスリン製薬会社は、米国では他のどの国よりもインスリンの料金を高く設定しています。インスリン製薬会社は、価格は政府の規制と保険会社に基づいていると述べています。被保険者の場合、自己負担額は通常、インスリン製品の定価に対する共同保険の割合として計算されます。したがって、患者共同保険の増加は、インスリン製品の定価の上昇を反映しています。コモンウェルス基金の調査によると、糖尿病を患っている保険に加入していないアメリカ人は、民間保険やメディケイドに加入している人に比べて、古くて安価な(そして効果が低い)インスリン薬を使用している可能性が高くなります。無保険患者の60~80%はインスリンの定価を全額支払っていますが、民間保険患者の9%とメディケイド受給者の3%が支払っています。

これらすべての要因にもかかわらず、北米ではインスリン以外に主要な選択肢がないため、インスリン薬および送達装置の市場は高くなっています。インスリンの手頃な価格に対処するために、商業部門でいくつかの取り組みが行われてきました。最近のバイオシミラーインスリン製品の出現は、バイオシミラーインスリンとオリジナル製品間の自動互換性の可能性と同様に、自己負担コストの削減に役立つ可能性があります。

したがって、上記の要因により、予測期間中に市場の成長を促進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 薬別

- 基礎インスリンまたは持効性インスリン

- ランタス(インスリングラルギン)

- レベミル(インスリンデテミル)

- トレシーバ(インスリンデグルデク)

- トウジョ(インスリングラルギン)

- バサグラー(インスリングラルギン)

- ボーラスまたは速効型インスリン

- NovoRapid/Novolog(インスリンアスパルト)

- ヒューマログ(インスリンリスプロ)

- アピドラ(インスリングルリシン)

- FIASP(インスリンアスパルト)

- Admelog(インスリンリスプロサノフィ)

- 従来のヒトインスリン

- ノボリン/ミックスタード/アクタピッド/インシュラタード

- フムリン

- インスマン

- 混合インスリン

- NovoMix(二相性インスリンアスパルト)

- Ryzodeg(インスリンデグルデクおよびインスリンアスパルト)

- Xultophy(インスリンデグルデクおよびリラグルチド)

- Soliqua/Suliqua(インスリングラルギンおよびリキシセナチド)

- バイオシミラーインスリン

- インスリングラルギンバイオシミラー

- ヒトインスリンバイオシミラー

- 基礎インスリンまたは持効性インスリン

- 装置別

- インスリンポンプ

- インスリンポンプ装置

- インスリンポンプリザーバー

- インスリン注入セット

- インスリンペン

- 再利用可能なペン型カートリッジ

- 使い捨てのペン型インスリン

- インスリン注射器

- インスリンジェットインジェクター

- インスリンポンプ

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- オーストラリア

- インド

- 中国

- 日本

- マレーシア

- 韓国

- タイ

- フィリピン

- ベトナム

- インドネシア

- 残りのアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- イラン

- エジプト

- オマーン

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 市場指標

- 1型糖尿病の人口

- 2型糖尿病の人口

第7章 競合情勢

- 企業プロファイル

- Novo Nordisk A/S

- Sanofi Aventis

- Eli Lilly

- Biocon

- Julphar

- Exir

- Medtronic

- Insulet

- Ypsomed

- Becton Dickinson

- 企業シェア分析

第8章 市場機会と将来の動向

The Human Insulin Drugs and Delivery Devices Market size is estimated at USD 67.45 billion in 2024, and is expected to reach USD 80.99 billion by 2029, growing at a CAGR of 3.73% during the forecast period (2024-2029).

Diabetes mellitus is considered a risk factor for increasing COVID-19. During the COVID-19 pandemic, tight control of glucose levels and prevention of diabetes complications might be crucial in patients with diabetes mellitus to keep susceptibility low and to prevent severe courses of COVID-19. COVID-19 affects glucose metabolism, mainly in patients with diabetes due to this frequent usage of insulin drugs and delivery devices market increased.

Diabetes is generally considered a lifestyle-related disease. Over time, with the increase in population around the world, the incidences of the disease have increased outrageously. Approximately 100 million people around the world need insulin, including all the people suffering from Type 1 diabetes and between 10-25% of people with Type 2 diabetes. Although insulin has been used in the treatment of diabetes for over 90 years, globally, more than half of those who need insulin today still cannot afford and access it. Insulin Drugs and delivery devices are necessary for type-1 diabetes patients because their body doesn't produce insulin internally, type-2 diabetes patients also need insulin, particularly those who have difficulty controlling their diabetes with oral medications.

Human Insulin Drugs and Delivery Devices Market Trends

Type-1 Diabetes Population Driving the Market In The Forecast Period

The type-1 diabetes population is expected to register a CAGR of over 2% during the forecast period.

The exact cause of type-1 diabetes is unknown, but type-2 diabetes is caused by day-to-day lifestyle changes and choices. The prevalence rate of type-2 diabetes has quadrupled when compared to a decade ago. The prevalence of type-1 diabetes mellitus (T2DM) has increased dramatically during the last two decades, a fact driven by the increased incidence of obesity, the primary risk factor for T1DM. Diabetes ranks among the fastest-growing chronic diseases in the United States. India is among the top three countries with a high incidence of diabetes. Many reports and surveys have documented a drastic increase in the diabetic population based on lifestyle habits.

Although oral anti-diabetic drugs are considered a standard of care for type-2 diabetes patients, there has been a rise in the need for using insulin, along with conventional medication, to help stabilize blood glucose levels. This trend has attracted many players, both local and international, to enter the biosimilar market.

The R&D in the insulin segment is rising year-on-year as researchers are trying to bring out the best molecule for patients' use, curb maximum side effects, and increase their efficiency. Thus, the increasing prevalence of obesity and diabetes across the world is likely to augment the demand for insulin, which in turn drives the market for insulin drugs and devices.

North America is Expected to Dominate the Human Insulin Drugs and Delivery Devices Market.

North America dominates the human insulin drug and delivery device market, despite having high insulin prices. According to RAND researchers, insulin drug companies charge more for insulin in the United States than in any other country. Insulin drug companies say that the price is based on government regulations and insurance providers. For the insured, out-of-pocket costs are usually calculated as a percentage of co-insurance of the list price of insulin products. Increases in patient co-insurance, therefore, reflect rising list prices of insulin products. According to a Commonwealth Fund study, uninsured Americans with diabetes are more likely to be using older, less costly (and less effective) insulin drugs compared to those with private insurance or Medicaid. 60% to 80% of uninsured patients pay the full list price for insulin, while 9% of privately insured patients and 3% of Medicaid beneficiaries do.

Despite all these factors, the market for insulin drugs and delivery devices is high in North America because there is no other major option other than insulin. There have been several initiatives carried out in the commercial sector to address insulin affordability. The recent advent of biosimilar insulin products may help reduce out-of-pocket costs, as could the possibility of automatic interchangeability between biosimilar insulin and originator products.

Thus, owing to the above factors, it is expected to drive market growth over the forecast period.

Human Insulin Drugs and Delivery Devices Industry Overview

The market is highly consolidated, with three major manufacturers holding a global market presence and the remaining manufacturers confined to other local or region-specific manufacturers. Mergers and acquisitions that happened between the players in the recent past have helped the companies strengthen their market presence. Eli Lilly and Boehringer Ingelheim have an alliance to develop and commercialize Basaglar (Insulin Glargine). Additionally, the players in the recent past helped the companies strengthen their market presence; for example, Novo Nordisk collaborated with Ypsomed to provide better insulin therapy solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Drug

- 5.1.1 Basal or Long Acting Insulins

- 5.1.1.1 Lantus (Insulin glargine)

- 5.1.1.2 Levemir (Insulin detemir)

- 5.1.1.3 Tresiba (Insulin degludec)

- 5.1.1.4 Toujeo (Insulin glargine)

- 5.1.1.5 Basaglar (Insulin glargine)

- 5.1.2 Bolus or Fast Acting Insulins

- 5.1.2.1 NovoRapid/Novolog (Insulin aspart)

- 5.1.2.2 Humalog (Insulin lispro)

- 5.1.2.3 Apidra (Insulin glulisine)

- 5.1.2.4 FIASP (Insulin aspart)

- 5.1.2.5 Admelog (Insulin lispro Sanofi)

- 5.1.3 Traditional Human Insulins

- 5.1.3.1 Novolin/Mixtard/Actrapid/Insulatard

- 5.1.3.2 Humulin

- 5.1.3.3 Insuman

- 5.1.4 Combination Insulins

- 5.1.4.1 NovoMix (Biphasic Insulin aspart)

- 5.1.4.2 Ryzodeg (Insulin degludec and Insulin aspart)

- 5.1.4.3 Xultophy (Insulin degludec and Liraglutide)

- 5.1.4.4 Soliqua/Suliqua (Insulin glargine and Lixisenatide)

- 5.1.5 Biosimilar Insulins

- 5.1.5.1 Insulin glargine biosimilars

- 5.1.5.2 Human insulin biosimilars

- 5.1.1 Basal or Long Acting Insulins

- 5.2 By Device

- 5.2.1 Insulin Pumps

- 5.2.1.1 Insulin Pump Devices

- 5.2.1.2 Insulin Pump Reservoirs

- 5.2.1.3 Insulin Infusion sets

- 5.2.2 Insulin Pens

- 5.2.2.1 Cartridges in reusable pens

- 5.2.2.2 Disposable insulin pens

- 5.2.3 Insulin Syringes

- 5.2.4 Insulin Jet Injectors

- 5.2.1 Insulin Pumps

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 Australia

- 5.3.3.2 India

- 5.3.3.3 China

- 5.3.3.4 Japan

- 5.3.3.5 Malaysia

- 5.3.3.6 South Korea

- 5.3.3.7 Thailand

- 5.3.3.8 Philippines

- 5.3.3.9 Vietnam

- 5.3.3.10 Indonesia

- 5.3.3.11 Rest of the Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Iran

- 5.3.5.3 Egypt

- 5.3.5.4 Oman

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of the Middle-East and Africa

- 5.3.1 North America

6 MARKET INDICATORS

- 6.1 Type-1 diabetes population

- 6.2 Type-2 diabetes population

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Novo Nordisk A/S

- 7.1.2 Sanofi Aventis

- 7.1.3 Eli Lilly

- 7.1.4 Biocon

- 7.1.5 Julphar

- 7.1.6 Exir

- 7.1.7 Medtronic

- 7.1.8 Insulet

- 7.1.9 Ypsomed

- 7.1.10 Becton Dickinson

- 7.2 Company Share Analysis