|

市場調査レポート

商品コード

1906869

発酵飲料:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Fermented Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 発酵飲料:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

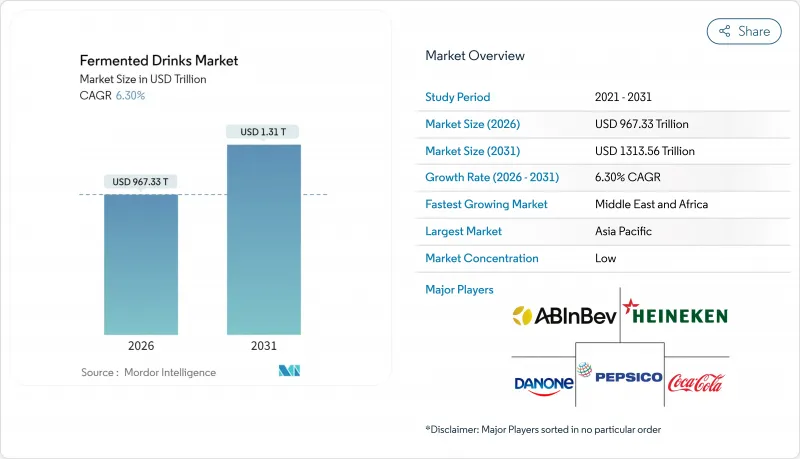

発酵飲料市場は2025年に9,100億米ドルと評価され、2026年の9,673億3,000万米ドルから2031年までに1兆3,135億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは6.30%と見込まれます。

持続的な成長の勢いは、腸内健康ソリューションへの関心の高まりから持続可能性への広範な取り組みに至るまで、長期的な変化の相乗効果を反映しており、このカテゴリーを従来のアルコール消費をはるかに超えて拡大させています。消費者は低アルコール・ノンアルコール代替品、プロバイオティクス、循環型経済の製品ストーリーに傾倒しており、メーカーは一つの購入で複数のライフスタイル優先事項に対応することが可能となっています。精密に制御された発酵技術により、優れた風味の安定性と糖分削減が実現され、ブランドは味を損なうことなく、厳格化するパッケージ表示規制への対応が可能となります。一方、アルコール度数0.5%以下の飲料に対する規制緩和により、革新的なメーカーが洗練された軽発酵製品を導入する障壁が低下し、ノンアルコール志向の消費者層にアピールしています。供給面では、高スループット微生物スクリーニング、CO2回収システム、廃棄物原料化技術への投資が進み、コスト効率・製品品質・環境性能が向上し、業界の回復力を強化しています。

世界の発酵飲料市場の動向と洞察

プロバイオティクス豊富な機能性飲料への需要増加

消費者の消化器健康への関心が高まる中、生きた菌を含む飲料の需要が過去最高を記録しています。調査によれば、プロバイオティクス飲料は生体活性物質の吸収を促進し、測定可能な免疫効果をもたらすことが示されており、特にコンブチャには抗菌作用や抗炎症作用が認められています。米国食品医薬品局(FDA)は構造機能表示の文言を明確化し、ブランドがプロバイオティクスの含有量や菌株固有の利点をより確信を持って伝えることを可能にしております。ウォーターケフィアや発酵フルーツジュースなどの植物由来製品は、乳糖不耐症やビーガン消費者に対応し、カテゴリー拡大を図ると同時に、個別化栄養の動向にも合致しております。世界の機能性飲料市場規模が490億米ドルに迫る中、発酵製法は依然として最前線に位置しております。

「ノンアルコール志向」の潮流が非アルコール飲料の選択肢を加速

健康志向の若年層がアルコール摂取を控える中、洗練された低アルコール・ノンアルコール発酵飲料の需要が加速しています。英国におけるこれらの商品の小売価値は2024年から2029年にかけて56%増加が見込まれ、持続的な成長が示唆されています。醸造所では、エタノール濃度を上げずに風味の複雑さを構築するため非伝統的な酵母を採用し、循環性目標達成に向け使用済み基質のリサイクルを進めています。プレミアム価格設定により利益率は守られており、アルコール度数の低下が収益性を損なうわけではないことが証明されています。

高品質なスコビー(SCOBY)およびケフィア粒の供給不安定性

商業生産はスターターカルチャーに依存していますが、その微生物の複雑性は標準化を困難にし、供給逼迫と価格変動を引き起こしています。ウォーターケフィア粒の生存率は基質の変化に伴い変動し、バッチ間の一貫性や保存期間の安定性を損なう恐れがあります。新興市場の小規模企業は輸入カルチャーに依存するケースが多く、コスト増とサプライチェーンリスクを伴います。微生物ライブラリーのバンク化や管理された培養施設といったバイオテクノロジーソリューションには、多くの小規模醸造所がまだ負担できない資本支出が必要です。

セグメント分析

2025年時点でビールは発酵飲料市場規模の62.74%を占め、その定着した消費パターンと広範な流通網を裏付けています。醸造メーカーは、クラシックなラガービールとノンアルコール製品群の間で迅速なSKU切り替えを可能にするため、工場の改修を進めています(クロムバッハ社の1億ユーロ規模の近代化計画がその一例です)。循環型醸造の取り組みでは、CO2を回収し、使用済み穀物を高付加価値原料として再利用することで、プレミアムなポジショニングを支えながら炭素排出量を削減しています。並行して、アサヒグループなどの大手企業は、独自開発のポストバイオティクスを活用し、中核製品群内の機能性拡張製品で差別化を図っています。

コンブチャは現時点ではニッチ市場ですが、飲料カテゴリー中最も高い13.05%のCAGRで拡大を続けており、茶ベースからフラボノイドやフェノール成分が豊富なリンゴジュースや黒ニンジンジュースへと展開範囲を広げています。微生物マッピングへの投資によりバッチ間の風味安定性が確保され、一般小売店での取り扱い拡大を支えています。常温保存可能な製品ラインは冷蔵流通への依存度を低減し、さらなる普及を促進しています。

地域別分析

アジア太平洋地域は文化的背景と強固な国内サプライチェーンにより発酵製品市場を牽引しております。ヒマラヤ地域住民は高地での栄養補給に発酵飲料を頼っており、心代謝機能への有益性を示す臨床研究がこれを裏付けております。都市部のミレニアル世代は古代の伝統と現代の健康動向を融合させ、コンブチャを積極的に取り入れております。インド、タイ、ベトナムの政府は小規模加工業者への助成金を通じ、農村部の雇用創出と製品革新を促進しております。

中東・アフリカ地域では、人口増加と未発達な小売ネットワークが発酵飲料の機会を創出しています。可処分所得の高い湾岸地域の消費者は高級製品を好むため、サフラン風味のケフィアなど独自フレーバーの開発が進んでいます。サハラ以南アフリカではコールドチェーンの制約から、常温保存可能または粉末状のプロバイオティクス製品への需要が高まっています。欧州と北米では、成熟した小売市場において、免疫サポート、エネルギー補給、美容効果といった機能性表示による差別化が求められており、透明性の高い菌株表示がこれを支えています。ソフトドリンク産業課税の拡大といった規制変更が製品設計に影響を与え、課税対象となる糖分レベルを削減するための精密制御発酵が促進されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- プロバイオティクス豊富な機能性飲料への需要増加

- 「節酒志向」の潮流がノンアルコール飲料の選択肢を加速

- 低糖質・常温保存可能な飲料を実現するクラフト発酵技術

- 食品廃棄物の基質への循環型経済的アップサイクリング

- アルコール度数0.5%未満の即飲製品に対する規制緩和

- 新規風味のための精密発酵スターターカルチャー

- 市場抑制要因

- 高品質なスコビー及びケフィア粒の供給不安定性

- 砂糖税およびパッケージ前面表示の制約

- 新興市場におけるコールドチェーン依存度

- 微生物汚染によるリコールリスク

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- 持続可能性と環境への影響

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 飲料タイプ別

- アルコール発酵飲料

- ビール

- サイダー

- 日本酒

- その他のアルコール飲料

- ノンアルコール発酵飲料

- コンブチャ

- ケフィア

- 発酵乳飲料

- その他のノンアルコール飲料

- アルコール発酵飲料

- 流通チャネル別

- オントレード

- オフトレード

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア/食料品店

- 専門店

- オンライン小売店

- パッケージングタイプ別

- ボトル(ガラス製・PET製)

- 缶

- テトラパック/紙パック

- 樽・バレル

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- Anheuser-Busch InBev SA/NV

- Heineken N.V.

- Carlsberg Group

- Paine Schwartz Partners(Suja Life LLC)

- The Boston Beer Company

- GT's Living Foods

- PepsiCo Inc.(KeVita)

- The Coca-Cola Company(Health-Ade)

- Danone SA

- Nestle SA

- Yakult Honsha Co. Ltd

- Bright Food(Group)Co. Ltd

- Schreiber Foods Inc.

- Bio-tiful Dairy Ltd

- Asahi Group Holdings

- Pernod Ricard SA

- Fentimans Ltd

- Remedy Drinks

- Kombucha Wonder Drink

- Lactalis Group