|

市場調査レポート

商品コード

1640629

パネル化モジュール建築システム:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Panelized Modular Building Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| パネル化モジュール建築システム:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

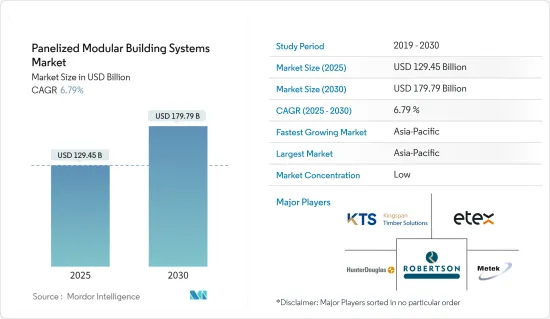

パネル化モジュール建築システム市場規模は、2025年に1,294億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.79%で、2030年には1,797億9,000万米ドルに達すると予測されます。

2020年と2021年前半に発生したCOVID-19パンデミックは、政府による禁止や制限のために世界の建設セクターを大幅に縮小させ、パネル化モジュール建築システム市場の成長を制限しました。住宅用不動産は最悪の打撃を受け、主要都市で厳格な封鎖措置がとられた結果、住宅登録が停止され、住宅ローンの実行が遅れました。しかし、規制解除後、建設セクターは順調に回復しています。住宅販売の増加、新規プロジェクトの立ち上げ、新規オフィスや商業スペースの需要増加が市場の回復を主導しています。

主要ハイライト

- 中期的には、オフサイト建設需要の高まりと、エネルギー効率の高いプレハブ住宅における構造用断熱パネルの需要増加が、調査対象市場の成長を増大させる主要な促進要因となっています。さらに、エネルギー効率の高い建物建設を支援する政府の優遇措置や施策が、プロジェクト請負業者がパネル化された建築システムを新築や改築に取り入れることを後押ししています。

- その反面、プレハブ資材を現場に搬入するための輸送ロジスティクスが必要であることが、予測期間中に対象産業の成長を抑制すると予想される主要要因となっています。

- 新興経済諸国におけるインフラや商業建設への投資の増加や、ビルディング・インフォメーション・モデリング(BIM)の導入は、間もなく世界市場に有利な成長機会を生み出すと考えられます。

- 予測期間中、アジア太平洋が市場を独占すると予想されます。この成長は、ルーフパネル、フロアパネル、ウォールモジュール、その他様々な製品の住宅、商業、産業、インフラセグメントでの需要が堅調であることに起因しています。

パネル化モジュール建築システム市場動向

市場を独占する住宅セグメント

- 住宅産業は、世界のパネル化モジュール建築システム市場の主要なエンドユーザー産業です。これらのシステムは、設計の柔軟性と精密さを提供し、コストと工期を削減します。この利点は、恒久的な住宅に対する需要の高まりや、建設プロジェクトの納期短縮に対する嗜好の高まりと相性が良いです。

- 住宅建設や解体作業で発生する瓦礫の減少による手間の最小化、住宅建設業者による収益性の高い建設ペースの維持の継続的追求、プレハブ建築のプラクティスと完全に調和したエネルギー効率の高い住宅地の建設に対する意識の高まりといった要因が、住宅セグメントにおけるパネル化モジュール建築システムの市場浸透を促進しています。

- 米国と欧州諸国では移民の数が増加しており、既存の住宅インフラへの圧力が高まっています。そのため、先進的インフラと不動産空間を持つこれらの国々では、再建築・改修プロジェクトや新規住宅建設が徐々に増加しています。

- 米国政府は2022年、同国の光熱費を削減するため、低所得地域の約45万戸の住宅をエネルギー効率の高い構造に変えるために31億6,000万米ドルを投資する計画を発表しました。

- 欧州連合(EU)の施策立案者は2021年、エネルギー使用量と温室効果ガス排出量を削減するため、2030年までにエネルギー効率の悪い建物すべてを改築するよう勧告しました。

- ドイツでは、新連立政権が毎年40万戸の新規住宅建設を計画しており、そのうち10万戸には公的補助金が出る予定です。

- 中国は世界最大の建設市場です。中国はパンデミック(世界的大流行)の危機から立ち直り、多くの住宅建設が始まった。中国のEvergrande Groupは2022年に60万戸の住宅建設を約束しています。香港の住宅当局は、低価格住宅の建設を推進するため、いくつかの対策を打ち出しました。当局は2030年までの10年間で30万1,000戸の公共住宅を供給することを目標としています。

- インドは、今後7年間で住宅に約1兆3,000億米ドルの投資を行う可能性があります。新たに6,000万戸の住宅が建設される見込みです。2024年には、手ごろな価格の住宅が約70%増加すると予想されています。インド政府の「2022年までにすべての人に住宅を」もまた、産業にとって重要なゲームチェンジャーです。2022年までに都市部の貧困層向けに2,000万戸以上の手頃な住宅を建設することを目指したこの構想は、2024年まで延長され、2,950万戸のプッカハウスを供給することを目標としています。

- 以上のような事実と要因を考慮すると、住宅建設用途でのパネル化モジュール建築システムの利用と需要は、予測期間中に拡大すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、大きな市場シェアで世界市場を独占しており、予測期間中もその優位性を維持すると予測されます。アジア太平洋は、低い製造コスト、安価な労働力の調達、著しく大規模な顧客基盤を背景に、インドと中国を主要受益者とする直接投資が大幅に流入しています。この地域の良好な経済情勢は、住宅、ホテル、ショッピングモール、高層ビル、スタジアムなどの需要を押し上げています。

- 住宅・都市・農村開発省の予測によると、中国の建設部門は2025年までGDPの6%を維持すると予想されています。こうした予測を踏まえ、中国政府は2022年1月、建設部門をより持続可能で質の高いものにすることを主眼とした5ヵ年計画を発表しました。中国は、建設現場からの汚染や廃棄物を減らすため、プレハブ建築の建設を増やす計画です。さらに、建設産業は近代化された手法に移行し、低炭素生産方式を確立し、建築物の品質を向上させることになります。

- さらに、中国政府は大規模な建設計画を打ち出しており、今後10年間で2億5,000万人の農村人口を新たな大都市に移住させる計画も含まれています。

- Invest India Reportによると、インドの建設産業は2025年までに1兆4,000億米ドルの市場規模に達する見込みで、100都市の変貌と手頃な価格の住宅を目標とするスマートシティ・ミッションに関する計画によって支えられています。国家投資促進の下、インドではインフラに1兆4,000億米ドルの投資予算が組まれており、その24%が再生可能エネルギー、19%が道路と高速道路、16%が都市インフラ、13%が鉄道となっています。

- 日本は超高層ビルや高層建築のセグメントで重要な地域です。日本では多くの高級マンションや集合住宅が建設中です。例えば、Mitsubishi Stateは日本で最も高いビルを建設中で、50戸の高級アパートから成り、1戸当たり月額家賃は4万3,000米ドルです。このプロジェクトは東京駅の近くに建設中で、2027年までに完成する予定です。

- 韓国政府は、2025年までにソウルやその他の都市に83万戸の住宅を供給する大規模再開発プロジェクトを実施する計画を発表しました。この計画では、ソウルに32万3,000戸、京畿道と仁川に29万3,000戸が建設されます。釜山、大邱、大田といった重要な都市も、4年間で22万戸の新築住宅の恩恵を受ける。

- 上記のすべての要因が、予測期間中のアジア太平洋におけるパネル化モジュール建築システム市場の成長を促進すると考えられます。

パネル化モジュール建築システム産業概要

パネル化モジュール建築システム市場はセグメント化されており、多くの参入企業が取るに足らないシェアを持ち、個別に市場需要に影響を与えています。市場の主要企業(順不同)には、Kingspan Timber Solutions(Kingspan Group)、Robertson Group Ltd、Etex Building Performance、Hunter Douglas Group、Metek PLCなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- オフサイト建設需要の高まり

- エネルギー効率の高いプレハブ住宅における構造用断熱パネル需要の増加

- 政府による奨励金と施策の後押し

- 抑制要因

- 輸送ロジスティクスの要件

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 技術スナップショット

- 規制施策分析

第5章 市場セグメンテーション(市場規模(売上高))

- パネルタイプ別

- 壁モジュール

- 屋根パネル

- 床パネル

- その他

- 製品タイプ別

- 木造フレーム

- 軽量鉄骨構造

- コンクリート

- その他

- エンドユーザー産業別

- 住宅

- 商業

- インフラ

- 産業・施設

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Algeco

- Etex Building Performance

- Frame Homes UK

- Fusion Building Systems

- Hunter Douglas Group

- Innovare

- Kingspan Timber Solutions(Kingspan Group)

- KLH UK Limited

- Merronbrook Ltd

- Metek PLC

- Modern Prefab Systems Pvt. Ltd Inc.

- Oregon Timber Frame Ltd

- Pinewood Structures

- Robertson Group Ltd

- Saint-Gobain Bruggemann Holzbau GmbH

- SIP Building Systems

- SIPs Eco Panel Systems Ltd

- Taylor Lane Timber Frame Limited

- Thorp Precast Ltd

- Walker Timber Engineering

第7章 市場機会と今後の動向

- 新興経済諸国におけるインフラと商業建設への投資の増加

- ビルディング・インフォメーション・モデリング(BIM)の導入

The Panelized Modular Building Systems Market size is estimated at USD 129.45 billion in 2025, and is expected to reach USD 179.79 billion by 2030, at a CAGR of 6.79% during the forecast period (2025-2030).

The COVID-19 pandemic in 2020 and the first half of 2021 drastically curtailed the global construction sector due to imposed government bans and restrictions, thereby limiting the panelized modular building systems market growth. Residential real estate was the worst hit as strict lockdown measures across significant cities resulted in the suspension of home registrations and slow home loan disbursements. However, the construction sector has been recovering well since restrictions were lifted. An increase in house sales, new project launches, and increasing demand for new offices and commercial spaces have been leading the market recovery.

Key Highlights

- Over the medium term, the rising demand for off-site construction and increasing demand for structural insulated panels in energy-efficient prefabricated homes are the major driving factors augmenting the growth of the market studied. Furthermore, favorable government incentives and policies supporting energy-efficient building construction are propelling the project contractors to incorporate panelized building systems in new and renovation constructions.

- On the flip side, the requirement of transportation logistics to bring the prefabricated materials on-site is the key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the increasing investment in infrastructure and commercial constructions in developing economies and the implementation of building information modeling (BIM) will likely create lucrative growth opportunities for the global market soon.

- Asia-Pacific is expected to dominate the market during the forecast period. This growth is attributed to the bullish demand for roof panels, floor panels, wall modules, and various other products in the residential, commercial, industrial, and infrastructure sectors.

Panelized Modular Building Systems Market Trends

Residential Segment to Dominate the Market

- The residential industry is the primary end-user industry for the global panelized modular building systems market. These systems offer design flexibility and precision in building with controlled costs and reduced construction time. This advantage goes well with the growing demand for permanent housing and rising preference for a shorter delivery time of construction projects.

- Factors like minimized hassles due to reduced debris from home construction and demolition activities, home builders' continued pursuit of maintaining a profitable construction pace, and growing awareness toward the construction of energy-efficient residential places which are in perfect sync with the prefabricated construction practices are driving the market penetration of the panelized modular building systems in the residential segment.

- The rising number of migrants in the United States and European countries has increased the pressure on existing residential infrastructure. Hence, these countries, dwelling with advanced infrastructure and real estate spaces, are witnessing a gradual lead in reconstruction and renovation projects and new residential constructions.

- In 2022, the US government announced its plans to invest USD 3.16 billion to transform around 450,000 homes in low incomes areas to energy-efficient structures to cut down the country's utility bills.

- To cut down energy use and GHG emissions, the European Union policymakers, in 2021, have recommended renovations of all worst energy-rating buildings by 2030, keeping residential buildings on priority.

- In Germany, the new coalition government has planned to build 400,000 new housing units every year, of which 100,00 units will be publicly subsidized.

- China is the world's largest construction market. As China recovered from the pandemic doom, many residential constructions kick-started in the country. China's Evergrande Group has committed to building 600,000 homes in 2022. The housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years till 2030.

- India is likely to witness an investment of around USD 1.3 trillion in housing over the next seven years. It is likely to witness the construction of 60 million new homes. The availability of affordable housing is expected to rise by around 70% in 2024. The Indian government's 'Housing for All by 2022' is also a significant game-changer for the industry. This initiative which aimed to build more than 20 million affordable homes for the urban poor by 2022, has been extended to 2024 with a target of delivering 29.5 million pucca houses.

- Considering all the above facts and factors, the usage and demand of panelized modular building systems for residential construction applications are expected to grow in the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominated the worldwide market with a significant market share and is projected to maintain its dominance during the forecast period. The Asia-Pacific region, with low manufacturing costs, cheap labor sourcing, and a remarkably large customer base, has a substantial inflow of FDI, with India and China being the primary beneficiaries. The region's favorable economic climate has boosted demand for houses, hotels, shopping malls, high-rise buildings, and stadiums.

- As per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025. Considering the given forecasts, the Chinese government unveiled a five-year plan in January 2022 focused on making the construction sector more sustainable and quality driven. China plans to increase the construction of prefabricated buildings to reduce pollution and waste from construction sites. Further, the construction industry will be transitioning to modernized practices, establishing low carbon-production modes and improving the quality of buildings, consequently increasing the demand for panelized modular building systems in the country.

- Additionally, the Chinese government has rolled out massive construction plans, which include making provisions for the movement of 250 million rural people to its new megacities over the next ten years, creating significant scope for panelized modular building systems in the future.

- As per the Invest India Report, India's construction industry is heading to reach USD 1.4 trillion market size by 2025, supported by schemes about the smart city mission targeting the transformation of 100 cities and affordable housing. Under National Investment Promotion, India has an investment budget of USD 1.4 trillion on infrastructure - 24% on renewable energy, 19% on roads and highways, 16% on urban infrastructure, and 13% on railways.

- Japan is a significant area in the field of skyscrapers and high-rise buildings. Many luxury apartments and residential complexes are under construction in Japan. For instance, Mitsubishi State is constructing Japan's tallest building, comprising 50 luxury apartments, each generating USD 43,000 monthly rent. The project is being built near the Tokyo station and will reach completion by 2027.

- The South Korean government has outlined its plan to execute large-scale redevelopment projects to supply 830,000 housing units in Seoul and other cities by 2025. From the planned construction, Seoul will get 323,000 new houses, and 293,000 will be built near Gyeonggi Province and Incheon. Significant cities like Busan, Daegu, and Daejeon will also benefit with 220,000 new houses in 4 years.

- All factors above are likely to fuel the growth of the panelized modular building systems market in Asia-Pacific over the forecast period.

Panelized Modular Building Systems Industry Overview

The panelized modular building systems market is fragmented, with many players holding insignificant shares to individually affect the market demand. Some of the major players in the market (in no particular order) include Kingspan Timber Solutions (Kingspan Group), Robertson Group Ltd, Etex Building Performance, Hunter Douglas Group, and Metek PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Off-site Construction

- 4.1.2 Increasing Demand for Structural Insulated Panels in Energy-efficient Prefabricated Homes

- 4.1.3 Supportive Government Incentives and Policies

- 4.2 Restraints

- 4.2.1 Transportation Logistics Requirements

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

- 4.6 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 By Panel Type

- 5.1.1 Wall Modules

- 5.1.2 Roof Panels

- 5.1.3 Floor Panels

- 5.1.4 Other Panel Types

- 5.2 By Product Type

- 5.2.1 Timber Frame

- 5.2.2 Light Gauge Structural Steel Framing

- 5.2.3 Concrete

- 5.2.4 Other Product Types

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.3.4 Industrial and Institutional

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Algeco

- 6.4.2 Etex Building Performance

- 6.4.3 Frame Homes UK

- 6.4.4 Fusion Building Systems

- 6.4.5 Hunter Douglas Group

- 6.4.6 Innovare

- 6.4.7 Kingspan Timber Solutions (Kingspan Group)

- 6.4.8 KLH UK Limited

- 6.4.9 Merronbrook Ltd

- 6.4.10 Metek PLC

- 6.4.11 Modern Prefab Systems Pvt. Ltd Inc.

- 6.4.12 Oregon Timber Frame Ltd

- 6.4.13 Pinewood Structures

- 6.4.14 Robertson Group Ltd

- 6.4.15 Saint- Gobain Bruggemann Holzbau GmbH

- 6.4.16 SIP Building Systems

- 6.4.17 SIPs Eco Panel Systems Ltd

- 6.4.18 Taylor Lane Timber Frame Limited

- 6.4.19 Thorp Precast Ltd

- 6.4.20 Walker Timber Engineering

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investment in Infrastructure and Commercial Constructions in Developing Economies

- 7.2 Implementation of Building Information Modeling (BIM)