|

市場調査レポート

商品コード

1686658

水力発電-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Hydropower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 水力発電-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

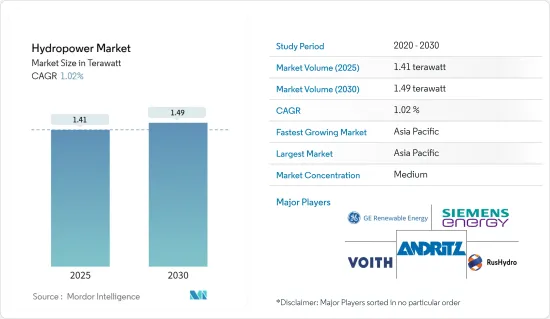

水力発電市場規模は2025年に1.41テラワットと推定され、予測期間中(2025年~2030年)のCAGRは1.02%で、2030年には1.49テラワットに達すると予測されます。

主なハイライト

- 中期的には、政府支援に裏打ちされた新規水力発電プロジェクトの増加や、信頼性の高い電力需要の高まりといった要因が、予測期間中の市場を牽引すると予想されます。

- 一方、水力発電プロジェクトが環境に及ぼす悪影響は、予測期間中の市場成長を妨げる可能性が高いです。

- とはいえ、水力発電の増加を目的とした新たな技術動向は、今後数年間、水力発電市場に大きな機会をもたらすと予想されます。

- アジア太平洋は、同地域の様々な国で水力発電プロジェクトへの投資が増加しているため、市場を独占すると推定されます。

水力発電市場の動向

市場を独占する大規模水力発電(100MW以上)セグメント

- 大規模水力発電は、大型水車の駆動に使用される流水から得られる再生可能エネルギー発電の一形態です。都市向けに大量の水力発電を行うには、発電、灌漑、家庭用または工業用として後で放流するための水を貯め、調整するための湖、貯水池、ダムが必要です。大規模な水力発電施設は簡単にオン・オフができるため、水力発電は一日を通してピーク時の電力需要を満たす上で、他のほとんどのエネルギー源よりも信頼性が高くなっています。

- 従来の水力発電ダム、揚水発電、流水発電は、世界中の大規模水力発電所のさまざまなタイプです。

- 国際再生可能エネルギー機関によると、2022年には世界で約75億5,000万米ドルが水力発電に投資されたが、2021年には約78億3,000万米ドルが投資されました。新しい水力発電容量への絶え間ない投資は、世界的に大規模水力発電セグメントの成長を牽引しています。また、大規模水力発電の平均設置コストは比較的低いです。

- 中国、ブラジル、米国、カナダ、インド、日本は、世界中で大規模水力発電プロジェクトを展開している主要国です。よりクリーンなエネルギー源へのシフトや、世界の主要先進国および新興経済諸国全体で総発電量に占める再生可能エネルギーの割合を増やす計画といった要因が、予測期間中に大規模水力発電分野を牽引すると予想されます。

- 主要水力発電国に加え、東南アジア地域の小国も大規模水力発電開発を急速に進めています。メコン経済を活性化させるためのエネルギー需要の増加は、水力発電開発に対する水域諸国の強い関心を引き付けています。ここ数十年の間に、この地域全体で水力発電プロジェクトに大規模な投資が行われてきました。

- 例えば、ラオス政府は、総容量195万kWの12の水力発電ダムプロジェクトを完成させる計画を発表しました。水力発電開発は、2030年までに近隣諸国に約20,000MWの電力を輸出するというラオス政府の計画の中心的な優先事項です。

- 2022年5月、Drax Group PLCはクルアチャン発電所に6億1,600万米ドルを投資しました。同社はクルアチャン発電所に600MWの地下揚水発電容量を追加する計画でした。同社は2030年までにクルアチャン発電所の容量を倍増させる計画で、2024年に現地での作業を開始します。同社はベン・クルアチャンの洞窟をくり抜き、発電所と関連インフラを収容するために約200万トンの岩盤を掘削する計画です。

- したがって、上記の要因から、予測期間中は大規模水力発電(100MW以上)分野が世界の水力発電市場を独占すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、近年水力発電市場を独占しており、予測期間中もその支配力を維持すると思われます。国際再生可能エネルギー機関(International Renewable Energy Agency)によると、2022年現在、中国は413.5GWの設備容量を持ち、水力発電市場の世界的リーダーです。

- 中国は、2060年までにカーボンニュートラルを実現し、2025年までに石炭消費をピークアウトさせるという計画を発表しました。これにより、再生可能エネルギー分野への投資が増加し、2022年には約2,250万kWの水力発電が新たに設置されました。

- 2023年5月、中国の国家開発改革委員会(NDRC)は、西蔵自治区に約84億3,000万米ドルの資本支援を受ける新しい水力発電所の建設を承認すると発表しました。年間平均発電量は112億8,000万キロワット時を超えます。

- さらに2023年2月には、インドがアルナーチャル・プラデーシュ州の国家水力発電公社(NHPC)のディバン水力発電プロジェクト(2,880メガワット(MW))に39億米ドルを投資することを承認しており、このプロジェクトの建設には9年かかると見積もられています。

- したがって、上記の要因から、予測期間中、アジア太平洋が世界の水力発電市場を独占すると予想されます。

水力発電産業の概要

水力発電市場は半固体化しています。主な企業としては、GE Renewable Energy、Siemens Energy AG、Andritz AG、Voith GmbH &Co.KGaA、PJSC RusHydroなどがあります。

2022年3月、アンドリッツとタイ発電公社(EGAT)は、タイおよび周辺の東南アジア諸国における水力発電プロジェクトのビジネスチャンスを共同で模索・拡大するための覚書に調印しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの設置容量と予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 信頼性の高い電力需要の増加

- 水力発電に対する政府支援の増加

- 抑制要因

- 水力発電プロジェクトの環境への悪影響

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 規模

- 大規模水力発電(100MW以上)

- 小水力発電(10MW未満)

- その他の規模(10~100MW)

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- GE Renewable Energy

- Siemens Energy AG

- Andritz AG

- Voith GmbH & Co. KGaA

- China Yangtze Power Co. Ltd

- PJSC RusHydro

- Electricite de France SA(EDF)

- Iberdrola SA

- Market Ranking/Share Analysis

第7章 市場機会と今後の動向

- 水力発電の増加を目指す新たな技術動向

The Hydropower Market size is estimated at 1.41 terawatt in 2025, and is expected to reach 1.49 terawatt by 2030, at a CAGR of 1.02% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, gactors such as the increasing number of new hydropower projects backed by government support and the rising demand for reliable electricity are expected to drive the market during the forecast period.

- On the other hand, negative environmental consequences of hydropower projects are likely to hinder the market growth during the forecast period.

- Nevertheless, emerging technological trends aimed at increasing hydropower generation are expected to provide significant opportunities for the hydropower market in the coming years.

- Asia-Pacifc is estimated to dominate the market due to increasing investment in hydropower projects across the various countries in the region.

Hydropower Market Trends

The Large Hydropower (Greater Than 100 MW) Segment to Dominate the Market

- Large-scale hydropower is a form of renewable energy generation derived from flowing water, which is used to drive large water turbines. In order to generate large amounts of hydroelectricity for cities, lakes, reservoirs, and dams are needed to store and regulate water for later release for power generation, irrigation, and domestic or industrial use. Since large-scale hydropower facilities can easily be turned on and off, hydropower has become more reliable than most other energy sources for meeting peak electricity demands throughout the day.

- Conventional hydroelectric dams, pumped storage, and run-of-the-river are the different types of large-scale hydropower plants worldwide.

- As per International Renewable Energy Agency, around USD 7.55 billion was invested in hydropower globally in 2022, whereas around USD 7.83 billion was invested in 2021. The constant investment in new hydropower capacity globally drives growth in large hydropower segments. Also, the average cost of large hydropower installation is comparatively low.

- China, Brazil, the United States, Canada, India, and Japan are the major countries in the deployment of large-scale hydropower projects across the world. Factors such as a shift towards cleaner energy sources and plans to increase the share of renewable energy in the total power generation mix across all the major developed and emerging economies across the world are expected to drive the large hydropower segment during the forecast period.

- In addition to the major hydropower countries, smaller countries from the Southeast Asia region are also moving forward rapidly in the large hydropower development. Increasing demand for energy to boost the Mekong economy has attracted riparian countries' keen interest in hydropower development. Over the last few decades, this has been evidenced by extensive investment in hydropower projects across the region.

- For instance, the Lao government announced that it plans to complete 12 hydropower dam projects with a total capacity of 1,950 MW. Hydropower development is a central priority of the Lao government's plan to export around 20,000 MW of electricity to its neighboring countries by 2030.

- In May 2022, Drax Group PLC invested USD 616 million in the Cruachan power station. The company planned to add 600 MW of underground pumped storage hydropower capacity to the Cruachan power station. The company plans to double the Cruachan facility's capacity by 2030, and work on-site begins in 2024. The company plans to hollow out a cavern in Ben Cruachan and excavate around two million tons of rock to house the power station and related infrastructure.

- Therefore, based on the factors mentioned above, the large hydropower (greater than 100 MW) segment is expected to dominate the global hydropower market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asian-Pacific region has dominated the hydropower market in recent years, and it is likely to maintain its dominance during the forecast period. According to International Renewable Energy Agency, as of 2022, China is the global leader in the hydropower market, with an installed capacity of 413.5 GW.

- China announced its plan to become carbon neutral by 2060 and peak coal consumption by 2025. This led to increased investment in the renewable sector, and in 2022, around 22.5 GW of new hydropower was installed.

- In May 2023, the National Development and Reform Commission (NDRC) of China announced to approval construction of a new hydropower plant in the Xizang Autonomous region which will have capital backing of around USD 8.43 billion. The annual average electricity volume produced by the plant will surpass 11.28 billion kilowatt-hours.

- Further, in February 2023, India approved a USD 3.9 billion investment for the 2,880 megawatts (MW) Dibang hydropower project in Arunachal Pradesh, National Hydroelectric Power Corporation (NHPC), and it is estimated that this project will take nine years to build.

- Therefore, based on the factors mentioned above, Asia-Pacific is expected to dominate the global hydropower market during the forecast period.

Hydropower Industry Overview

The hydropower market is semi-consolidated. Some of the major players include (not in particular order) GE Renewable Energy, Siemens Energy AG, Andritz AG, Voith GmbH & Co. KGaA, and PJSC RusHydro, among others.

In March 2022, ANDRITZ and the Electricity Generating Authority of Thailand (EGAT) signed a Memorandum of Understanding (MoU) to jointly explore and expand business opportunities for hydropower projects in Thailand and surrounding Southeast Asian countries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Demand for Reliable Electricity

- 4.5.1.2 Increasing Government Support for Hydropower Gneeration

- 4.5.2 Restraints

- 4.5.2.1 Negative Environmental Consequences of Hydropower Projects

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Size

- 5.1.1 Large Hydropower (Greater Than 100 MW)

- 5.1.2 Small Hydropower (Smaller Than 10 MW)

- 5.1.3 Other Sizes (10-100 MW)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 GE Renewable Energy

- 6.3.2 Siemens Energy AG

- 6.3.3 Andritz AG

- 6.3.4 Voith GmbH & Co. KGaA

- 6.3.5 China Yangtze Power Co. Ltd

- 6.3.6 PJSC RusHydro

- 6.3.7 Electricite de France SA (EDF)

- 6.3.8 Iberdrola SA

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Technological Trends Aimed at Increasing Hydropower Generation