|

市場調査レポート

商品コード

1683456

東南アジアの水力発電市場-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Southeast Asia Hydropower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 東南アジアの水力発電市場-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

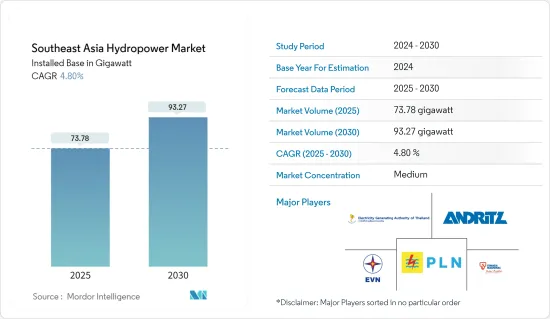

東南アジアの水力発電市場規模は、2025年の73.78ギガワットから2030年には93.27ギガワットに拡大し、予測期間中(2025~2030年)のCAGRは4.8%と予測されます。

主要ハイライト

- 長期的には、水力発電所への投資の増加や再生可能エネルギー需要の増加といった要因が市場の成長を牽引すると予想されます。

- しかし、太陽エネルギーや風力エネルギーといった他の再生可能エネルギーに比べ、水力発電の初期コストが高いことが市場の成長を抑制すると予想されます。

- 効率化のための技術進歩や水力発電プロジェクトの生産コストの低下は、東南アジアの市場参入企業に十分な機会をもたらすと期待されています。

- ベトナムは、水力発電セグメントへの投資が増加し、水力発電の設備容量が同地域で最も大きいことから、同地域最大の水力発電市場になると予想されます。

東南アジアの水力発電市場動向

大規模水力発電セグメントが市場を独占する展望

- 大規模水力発電所は、流水を利用して巨大な水車を駆動し、再生可能エネルギーを発電します。大量の水力発電を行うには、湖、リザーバー、ダムに水を貯め、発電、灌漑、家庭用水、工業用水として放出できるように調整する必要があります。

- 大規模水力発電所は、在来型水力発電ダム、揚水発電、流水発電、潮力発電の4種類に分類されます。大規模水力発電所は設置コストが高いが、特に大都市では低コストで電力を生産できます。国際再生可能エネルギー機関(International Renewable Energy Agency)によると、2022年に新規に稼働した水力発電プロジェクトの世界加重平均平準化エネルギーコスト(LCOE)は0.048米ドル/kWhでした。

- ラオス電力開発計画2020~2030によると、ラオスの水力発電容量は2025年までに14ギガワットを超えると予想されています。2025年までに、再生可能エネルギーは全エネルギーミックスの30%を占める可能性があり、水力発電はこの成長の主要な要素になると予想されています。

- 東南アジア諸国連合(ASEAN)のエネルギー協力行動計画(APAEC)2021~2025の一環として、2025年までに設備容量における再生可能エネルギー発電の割合を35%にすることを目指しており、そのためには35-40GWの導入が必要となる可能性があります。2023年3月、インドネシア政府はメンタラン・インドゥク水力発電所の建設工事を開始したが、このプロジェクトには26億米ドルの投資が必要です。1.3GW以上の容量を持つこの発電所は、PT Adaro Energy Indonesia、PT Kayan Patria Pratama Group、Sarawak Energyの合弁会社であるPT Kayan Hydropower Nusantaraによって開発されます。

- さらに、2023年のベトナム、カンボジア、ミャンマー、フィリピンなどの東南アジア諸国の水力発電設備容量は、22.639GW、1.791GW、3.269GW、3.826GWとなっています。2023年11月、フィリピンを拠点とする再生可能エネルギー生産会社Repower Energy Development Corporationは、Pure Energy Holdings Corporationの水力発電子会社であり、REDCのポートフォリオで8番目となる140万kWの最新流水式水力発電所を稼働させました。ケソン州レアル、アッパー・ラバヤット水力発電所とティバッグ水力発電所の間に位置するロウワー・ラバヤット発電所は、ラバヤット下流流の流れを利用し、年間毎時8ギガワットを発電すると推定されています。

- 以上の点から、大規模水力発電所が市場を独占すると予想されます。

ベトナムが市場を独占する見込み

- ベトナムは東南アジア最大の水力発電市場のひとつです。ベトナム電力庁(EVN)によると、2023年時点でベトナムの水力発電は2263万9,000kWで、同国の総設備容量の30%近くを占めています。

- 水力発電は同国の総発電量の30.77%近くを占め、大きな割合を占めています。ベトナム経済は、国内需要を満たすために水力発電に大きく依存していました。しかし、国内需要が急増するにつれて、電力に占める石炭火力発電の割合が増加し、その他の自然エネルギーも着実に成長しているが、総発電量に占める割合は相対的に小さくなっています。

- ベトナムは伝統的に水力発電に依存してきたため、すでに総水力ポテンシャルの60%近くを開発しており、成熟した水力発電市場となっています。ベトナムエネルギー展望によると、ベトナムは大規模・中規模水力発電(30MW以上で、通常リザーバーがつながっているものと定義される)の潜在力を十分に活用できるところまで来ています。しかし、河川流域の小規模水力発電の潜在力はまだ11GWほどあり、未開拓です。

- にもかかわらず、ベトナム政府は、2021~2030年にかけて6~7%近く増加すると予測される電力需要の増加に対処しようとする一方で、排出削減目標を達成するために、国内に残る大規模水力発電の可能性の開発に投資しています。

- 2024年1月、ベトナム電力(EVN)は、ハノイで開催された第46回ベトナム・ラオス二国間協力政府間委員会において、ラオスの26の水力発電所から2,689MWの電力を購入するための19の電力購入契約を締結しました。協定の調印はベトナムとラオスの電力協力の深化を示しました。

- 上記の要因により、ベトナムは2024~2029年の間に調査された市場を独占すると予想されます。

東南アジアの水力発電産業概要

東南アジアの水力発電市場は適度にセグメント化されています。この市場の主要企業には、Vietnam Electricity Construction JSC、Electricity Generating Authority of Thailand、PT Perusahaan Listrik Negara、Tenaga Nasional Berhad、Andrtiz AGなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの水力発電設備容量と予測(単位:GW)

- 再生可能エネルギーミックス(2023年)

- 今後予定されている主要水力発電プロジェクト一覧(東南アジア主要国別)

- 現在進行中と今後の水力発電入札リスト(東南アジア)

- 東南アジア主要水力発電コンサルティング会社・コンソーシアム一覧

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 水力発電への投資の増加

- 有利な政府施策

- 抑制要因

- その他の代替クリーンエネルギー源の採用

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- タイプ別

- 大規模水力発電

- 小水力発電

- 揚水発電

- 地域別

- ベトナム

- インドネシア

- マレーシア

- ラオス

- フィリピン

- タイ

- その他の東南アジア諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Vietnam Electricity Construction JSC

- Andritz AG

- Electricity Generating Authority of Thailand

- PT Perusahaan Listrik Negara

- Tenaga Nasional Berhad

- Toshiba Corporation

- General Electric Company

- Aboitiz Power Corporation

- Power Construction Corporation of China Ltd

- 市場ランキング分析

第7章 市場機会と今後の動向

- 効率的な水力発電タービンの技術革新

目次

Product Code: 71551

The Southeast Asia Hydropower Market size in terms of installed base is expected to grow from 73.78 gigawatt in 2025 to 93.27 gigawatt by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

Key Highlights

- In the long term, factors such as increasing investments in hydropower plants and increasing demand for renewable energy are expected to drive the market's growth.

- However, the high initial cost of hydropower compared to other forms of renewable energies like solar and wind energy is expected to restrain the growth of the market.

- Nevertheless, technological advancements in efficiency and a decrease in the production cost of hydropower projects are expected to create ample opportunities for market players in Southeast Asia.

- Vietnam is expected to be the region's largest hydropower market due to increasing investment in the sector and the highest installed capacity of hydropower energy in the region.

Southeast Asia Hydropower Market Trends

The Large Hydropower Segment is Expected to Dominate the Market

- Large-scale hydropower plants use flowing water to drive huge water turbines and generate renewable energy. To generate significant amounts of hydroelectricity, lakes, reservoirs, and dams must store and regulate water for later release for power generation, irrigation, domestic use, and industrial use.

- Large-scale hydropower plants can be classified into four types: conventional hydroelectric dams, pumped storage, run-of-the-river, and tidal. Although large hydropower plants are expensive to install, they produce electricity at a low cost, especially in large cities. According to the International Renewable Energy Agency, the global weighted average levelized cost of energy (LCOE) of newly commissioned hydropower projects in 2022 was USD 0.048/kWh.

- According to the Laos Power Development Plan 2020 -2030, the hydropower capacity of Laos is expected to exceed 14 gigawatts by 2025. By 2025, renewable energy may represent 30% of the total energy mix, and hydropower is anticipated to be a major component of this growth.

- As part of the Association of Southeast Asian Nations (ASEAN) Plan of Action for Energy Cooperation (APAEC) 2021-2025, the aim is to reach 35% renewable generation in installed power capacity by 2025, which may require the deployment of 35-40 GW. In March 2023, the Indonesian government began construction works for the Mentarang Induk hydropower plant, and the project requires a USD 2.6 billion investment. With more than 1.3 GW of capacity, the power plant will be developed by PT Kayan Hydropower Nusantara, a joint venture of PT Adaro Energy Indonesia, PT Kayan Patria Pratama Group, and Sarawak Energy.

- Moreover, in 2023, hydropower installed capacity in Southeast Asian Countries such as Vietnam, Cambodia, Myanmar, and the Philippines stood at 22.639 GW, 1.791 GW, 3.269 GW, and 3.826 GW. In November 2023, Philippine-based renewable energy producer Repower Energy Development Corporation, the hydropower subsidiary of Pure Energy Holdings Corporation, launched its newest 1.4 MW run-of-river hydropower plant, the eighth of its kind in REDC's portfolio. Located in Real, Quezon, between the Upper Labayat and Tibag hydropower plants, the Lower Labayat plant is estimated to generate 8 gigawatts per hour annually, utilizing the downstream current of the Labayat River.

- Owing to the above points, large hydropower plants are expected to dominate the market.

Vietnam is Expected to Dominate the Market

- Vietnam is one of the largest hydropower markets in Southeast Asia. According to the Electricity Authority of Vietnam (EVN), as of 2023, Vietnam had 22.639 GW of hydropower, accounting for nearly 30% of the country's total installed capacity.

- Hydropower has accounted for a significant share of the country's gross electricity generation mix, accounting for nearly 30.77% of the country's total electricity generation. The Vietnamese economy relied heavily on hydroelectricity to satiate domestic demand. However, as domestic demand increased rapidly, the share of coal-fired generation in electricity rose, along with other renewables, which have grown steadily but occupy a relatively smaller share of the total electricity generation mix.

- Due to its traditional dependence on hydroelectricity, Vietnam has already developed nearly 60% of its total hydropower potential, making it a mature hydropower market. According to the Vietnam Energy Outlook, the country is close to fully utilizing its potential for large-scale and medium-scale hydropower (defined as greater than 30 MW and typically with a connected reservoir). However, there is still untapped potential for run-of-river small-scale hydro of around 11 GW.

- Despite this, as the government tries to deal with the growing power demand, which is projected to grow by nearly 6-7% during 2021-2030 while realizing its emission reduction targets, the Vietnamese government is investing in the development of the remaining large-scale hydro potential in the country.

- In January 2024, State utility Vietnam Electricity (EVN) entered into 19 power purchase agreements for the acquisition of 2,689 MW of electricity from 26 hydropower plants in Laos during the 46th meeting of the Vietnam-Laos Intergovernmental Committee for Bilateral Cooperation in Hanoi. The signing of the agreements demonstrated deeper cooperation in electricity between Vietnam and Laos.

- Due to the above-mentioned factors, Vietnam is expected to dominate the market studied between 2024 and 2029.

Southeast Asia Hydropower Industry Overview

The Southeast Asian hydropower market is moderately fragmented. Some of the key players in this market are Vietnam Electricity Construction JSC, Electricity Generating Authority of Thailand, PT Perusahaan Listrik Negara, Tenaga Nasional Berhad, and Andrtiz AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Hydropower Installed Capacity and Forecast in GW, till 2029

- 4.3 Renewable Energy Mix, 2023

- 4.4 List of Major Upcoming Hydropower Projects, By Major Countries, Southeast Asia

- 4.5 List of On-going and Upcoming Hydropower Tenders, Southeast Asia

- 4.6 List of Major Hydropower Consulting Companies and Consortiums, Southeast Asia

- 4.7 Recent Trends and Developments

- 4.8 Government Policies and Regulations

- 4.9 Market Dynamics

- 4.9.1 Drivers

- 4.9.1.1 Increasing Investments in Hydropower Generation

- 4.9.1.2 Favorable Government Policies

- 4.9.2 Restraints

- 4.9.2.1 Adoption of Other Alternative Clean Energy Sources

- 4.9.1 Drivers

- 4.10 Supply Chain Analysis

- 4.11 Porter's Five Forces Analysis

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes Products and Services

- 4.11.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Large Hydropower

- 5.1.2 Small Hydropower

- 5.1.3 Pumped Storage

- 5.2 By Geography

- 5.2.1 Vietnam

- 5.2.2 Indonesia

- 5.2.3 Malaysia

- 5.2.4 Laos

- 5.2.5 Philippines

- 5.2.6 Thailand

- 5.2.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Vietnam Electricity Construction JSC

- 6.3.2 Andritz AG

- 6.3.3 Electricity Generating Authority of Thailand

- 6.3.4 PT Perusahaan Listrik Negara

- 6.3.5 Tenaga Nasional Berhad

- 6.3.6 Toshiba Corporation

- 6.3.7 General Electric Company

- 6.3.8 Aboitiz Power Corporation

- 6.3.9 Power Construction Corporation of China Ltd

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Innovations in Efficient Hydropower Turbines