|

市場調査レポート

商品コード

1444100

医療用飼料添加物:市場シェア分析、業界動向と統計、成長予測(2024-2029)Medicated Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療用飼料添加物:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

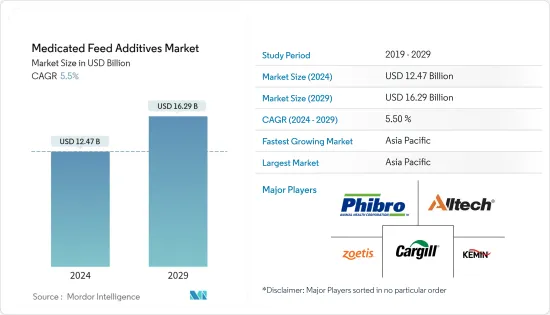

医療用飼料添加物の市場規模は、2024年に124億7,000万米ドルと推定され、2029年までに162億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.5%のCAGRで成長します。

2020年の市場は、COVID-19によって悪影響を受けました。世界のパンデミックは、さまざまな地域のさまざまな産業の適切な機能に影響を与えています。通関、輸出許可、輸入許可、植物検疫証明書に影響を与えました。これは主に政府機関の人員削減によるもので、これにより貿易向けの委託が遅れ、農家が入手できるいくつかの医療用飼料添加物製品が減少しました。食品業界からの需要の抑制と取引コストの増加は、予測期間中に世界中で医療用飼料添加物の生産コストを押し上げる波及効果をもたらすと予想されます。

中期的には、動物から人間に自然に感染する可能性が高い人獣共通感染症や食中毒の発生率の増加により、家畜におけるそのような病気の発生を最小限に抑えることができる重要な飼料添加物の使用量が増加しています。医療用飼料添加物は、飼料の品質と栄養成分を改善します。これらの添加物は動物の成長と発育を助け、飼料摂取量を増やします。栄養豊富な高級肉への意識の高まりにより、医療用飼料添加物の使用量が増加しています。

アジア太平洋における健康意識の高まりにより、植物性タンパク質と動物性タンパク質の需要が急増しました。しかし、最近の伝染病の発生により、特に欧州や北米などの地域では肉の品質が重大な問題となっています。この地域における動物性たんぱく質の利用の増加は、畜産農家に多大な圧力をかけ、徐々にさまざまな科学的農法に移行しつつあります。

医療用飼料添加物市場動向

抗生物質の禁止が他の部門の成長につながる

食品システムにおける抗生物質の使用は、多くの国の規制機関の間で懸念を増大させています。欧州連合は2006年には動物飼料への抗生物質の使用を禁止しました。 2017年以来、米国食品医薬品局は動物飼料サプリメントとしての抗生物質の使用を禁止しました。多くの国や地域がこれに追随すると予想されており、畜産における抗生物質の使用量削減に役立つ他の添加物に焦点が移っています。最近では2019年、インド政府は、インド政府の調査で家畜を肥やすために広く使用されていることが明らかになった後、世界で最も致死性の高いスーパーバグの蔓延を阻止するため、農場での「最後の希望」抗生物質の使用を禁止しました。他の抗生物質コリスチンは、養鶏産業での望ましくない使用のため禁止されました。これらの禁止により、プロバイオティクス、有機酸、エッセンシャルオイル、プレバイオティクス、免疫サポート、上皮サポート、肉の品質と生産を改善するためのエネルギー源などの抗生物質代替品の摂取が増加すると予想されます。抗生物質に関連するますます厳格化する規制の枠組みと、その代替品としてのプロバイオティクスの有効性の向上が、医療用飼料添加物市場のプロバイオティクス分野の力強い成長につながる主な要因になると予想されます。

アジア太平洋が世界市場をリード

2019年、特に中国や東南アジア諸国でのアジア太平洋地域の飼料生産は若干の停滞に見舞われました。しかし、この地域は依然として医療用飼料添加物市場において最大の地理的セグメントです。 2018年、中国政府は2020年までに家畜の飼料に使用される抗生物質を全廃することを目指す試験的プログラムを開始しました。この政策の実施は国内の飼料産業に影響を与えています。さまざまな成長段階の動物のニーズを満たすための原料組成などの飼料配合のアップグレード、および飼料加工技術のアップグレードや配合変更の推進の必要性などの飼料生産管理は、影響を与えると予想される重要な要素です。国内の飼料メーカー。さらに、成長促進剤としての抗生物質の使用の禁止、費用対効果、有害な残留影響に対する意識の高まりにより、持続可能な家畜生産においてハーブ飼料添加物の重要性が高まっています。畜産部門は、アスコルビン酸、プレバイオティクス、プロバイオティクス、ハーブ抽出物などのいくつかの飼料添加物から恩恵を受けています。

医療用飼料添加物業界の概要

薬用飼料市場は統合されており、世界および地域のトッププレーヤーが主要な市場シェアを占めています。研究開発への大規模な投資を通じて品質を重視することは、市場の主要な世界的企業が最も採用している戦略でした。大規模な投資は、既存の顧客ベースを維持するための新製品を作成するための製品ラインの拡張と革新に向けられています。市場の主要企業は、Cargill Inc.、Phibro Animal Health Corporation、Zoetis Inc.、Bluestar Adisseo、Archer Daniels Midland Company、Alltech Inc.、およびKemin Industriesなどです

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- 抗生物質

- ビタミン

- 酸化防止剤

- アミノ酸

- プレバイオティクス

- プロバイオティクス

- 酵素

- その他のタイプ

- 混合タイプ

- サプリメント

- 濃縮物

- プレミックス

- ベースミックス

- 動物の種類

- 反芻動物

- 豚

- 家禽

- 水産養殖

- 他の種類の動物

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- ロシア

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Phibro Animal Health Corporation

- Provimi Animal Nutrition

- Zoetis Inc.

- Cargill Inc.

- Archer Daniels Midland Company

- CHS Inc.

- Purina Animal Nutrition(Land O'Lakes)

- Adisseo France SAS

- Kemin Industries

- Alltech Inc.

- Biostadt India Limited

- Zagro

- HI-PRO Feeds

第7章 市場機会と将来の動向

第8章 COVID-19の市場への影響

The Medicated Feed Additives Market size is estimated at USD 12.47 billion in 2024, and is expected to reach USD 16.29 billion by 2029, growing at a CAGR of 5.5% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. The global pandemic has shown an impact on the proper functioning of various industries in various regions. It affected customs clearances, export permits, import permits, and phytosanitary certificates. This was primarily due to reduced staffing of government offices, which delayed the consignments meant for trade and reduced the availability of several medicated feed additive products to the farmers. Suppressed demand from the food joints and increased transaction costs is expected to have a knock-on effect that will push the cost of the medicated feed additives production up across the world during the forecast period.

Over the medium term, increasing incidences of zoonotic and foodborne diseases, which have high chances of being naturally transmitted from animals to humans, led to the rising usage of the key feed additives that can minimize the occurrence of such diseases in farm animals. Medicated feed additives improve the quality and nutritional content of the feed. These additives help in the growth and development of animals and increase feed intake. An increase in the awareness of high-quality meat, which is rich in nutrients, has resulted in an increase in the usage of medicated feed additives.

The increases in health awareness in Asia-Pacific led to a surge in demand for plant and animal proteins. However, the recent epidemic outbreaks have made meat quality a critical issue, especially in regions like Europe and North America. The increase in applications of animal protein in the region exerted massive pressure on livestock farmers, who are gradually shifting to various scientific methods of farming.

Medicated Feed Additives Market Trends

Ban on Antibiotics Leading to Growth in Other Segments

The usage of antibiotics in the food system is causing increasing concerns among the regulatory bodies in many countries. As early as 2006, the European Union banned the usage of antibiotics in animal feed. Since 2017, the United States Food & Drug Administration has banned the use of antibiotics as animal feed supplements. With many countries and regions expected to follow suit, the focus has shifted to other additives that can help reduce the usage of antibiotics for livestock farming. Recently, in 2019, the Indian government banned the use of a 'last hope' antibiotic on farms to try to halt the spread of some of the world's most deadly superbugs after a Bureau investigation revealed it was being widely used to fatten livestock. Other antibiotic colistin was banned due to its unwanted use in the poultry industry. These bans are expected to increase the uptake of antibiotic alternatives, such as probiotics, organic acids, essential oils, prebiotics, immune support, epithelial support, and an energy source for improving meat quality and production. The increasingly stringent regulatory framework related to antibiotics and the increased efficacy of probiotics as a substitute is expected to be the major factors leading to the robust growth of the probiotics segment of the medicated feed additives market.

Asia-Pacific Leads the Global Market

Feed production in Asia-Pacific suffered a minor setback in 2019, on account of the spread of the African Swine Fever, especially in China and Southeast Asian countries. However, the region remains the largest geographical segment in the medicated feed additives market. In 2018, the Chinese government launched a pilot program aiming at the elimination of antibiotics used in livestock feed by 2020. The implementation of this policy has been creating an impact on the feed industry in the country. Upgradation of feed formulations, such as raw material composition, for meeting the needs of animals at different growth stages, and feed production management, such as the need to upgrade the feed processing technology and drive the formulation change, are the crucial factors expected to affect the feed manufacturers in the country. Furthermore, the ban on antibiotic use as growth promoters, cost-effectiveness, and increased awareness about harmful residual effects has resulted in herbal feed additives gaining importance in sustainable livestock production. The animal husbandry sector gets benefits from several feed additives such as ascorbic acid, prebiotic, probiotic, and herbal extracts.

Medicated Feed Additives Industry Overview

The medicated feed market is consolidated, with the top global and regional players occupying major market shares. The focus on quality through extensive investments in R&D was the most adopted strategy of the leading global players in the market. Major investments are directed toward product line expansions and innovations for creating new products to retain the existing customer base. The major players in the market are Cargill Inc., Phibro Animal Health Corporation, Zoetis Inc., Bluestar Adisseo Co. Ltd, Archer Daniels Midland Company, Alltech Inc., and Kemin Industries, among others. For instance, in 2021, Cargill launched its Poultry feed with essential oils under improved Nutrena?iR) Naturewise?iR) formulas. The natural essential oils help in the promotion of egg weight, size, and production, enhanced palatability, and a fresh aroma direct from the bag.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Antibiotics

- 5.1.2 Vitamins

- 5.1.3 Antioxidants

- 5.1.4 Amino Acids

- 5.1.5 Prebiotics

- 5.1.6 Probiotics

- 5.1.7 Enzymes

- 5.1.8 Other Types

- 5.2 Mixture Type

- 5.2.1 Supplements

- 5.2.2 Concentrates

- 5.2.3 Premixes

- 5.2.4 Base Mixes

- 5.3 Animal Type

- 5.3.1 Ruminants

- 5.3.2 Swine

- 5.3.3 Poultry

- 5.3.4 Aquaculture

- 5.3.5 Other Animal Types

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Phibro Animal Health Corporation

- 6.3.2 Provimi Animal Nutrition

- 6.3.3 Zoetis Inc.

- 6.3.4 Cargill Inc.

- 6.3.5 Archer Daniels Midland Company

- 6.3.6 CHS Inc.

- 6.3.7 Purina Animal Nutrition (Land O' Lakes)

- 6.3.8 Adisseo France SAS

- 6.3.9 Kemin Industries

- 6.3.10 Alltech Inc.

- 6.3.11 Biostadt India Limited

- 6.3.12 Zagro

- 6.3.13 HI-PRO Feeds