|

市場調査レポート

商品コード

1686271

キサンタンガム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Xanthan Gum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| キサンタンガム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

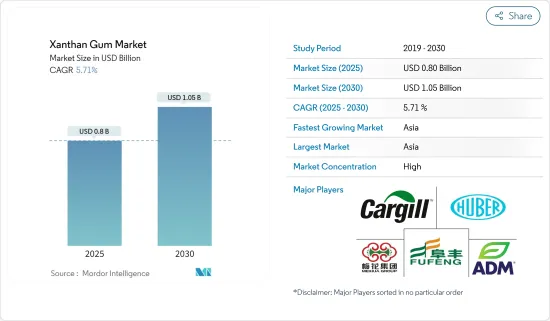

キサンタンガムの市場規模は2025年に8億米ドルと推定され、予測期間(2025-2030年)のCAGRは5.71%で、2030年には10億5,000万米ドルに達すると予測されます。

主なハイライト

- キサンタンガムは、植物由来の糖類とバクテリアに由来します。増粘・安定化作用があるため、主に食品産業で使用されています。また、食品の食感、一貫性、風味、保存性、外観を改善する効果もあります。さらに、キサンタンガムはその強力な機能特性により、ベーカリー製品、フルーツジュース、スープ、アイスクリーム、ソース、グレイビーソース、グルテンフリー製品などの配合に使用されています。

- また、明確な規制ガイドラインが市場の成長を後押ししています。例えば、米国食品医薬品局(FDA)は、連邦規則集(CFR)21の下で、キサンタンガムを人間が直接消費するために使用することを安全であると認めています。ただし、FDAはキサンタンガムを食品に使用する際の条件を定めています。

- キサンタンは菜食主義者やベジタリアンに優しいハイドロコロイドであり、ハラルやコーシャの要求にも容易に適合します。そのため、菜食主義者の消費者層をターゲットとするメーカーにとっては、動物由来のハイドロコロイドの代替品として有望です。

- 新興国市場の有力企業は、新製品の開発、合併、拡大、買収、他社との提携に注力し、ブランドの存在感を高め、市場シェアを拡大しています。例えば、2022年7月、CP Kelco社は米国と中国の工場施設でキサンタンガムを含むバイオガムの生産能力を拡大しました。

キサンタンガムの市場動向

飲食品がキサンタンガムの最大消費者

キサンタンガムはベーカリー製品の食感を改善し、パサパサになるのを防ぐと主張しています。キサンタンガムは保湿効果もあり、全体的な保存期間と受容性を高めるため、ベーカリー製品の消費量の増加がキサンタンガムの使用を促進しています。さらに、無糖やグルテンフリーのチョコレートの需要が高まっているため、メーカーは従来のグルテンを含む原料が不足しているレシピで、弾力性と構造を持つキサンタンガムをグルテンの代替品として使用しています。中期的には、健康的で機能的な菓子類へのニーズの高まりとともに、市場の拡大が予想されます。また、様々な食肉製品の生産量の増加や食肉加工品の需要の高まりにより、食肉原料の輸出入も世界的に増加しています。そのため、食肉製品の増粘剤、懸濁剤、安定剤、乳化剤として使用されるキサンタンガムの需要が伸びています。キサンタンガムは、ハム、ランチョンミート、赤ウインナー、その他のひき肉製品に使用することで、保水力や柔らかさを向上させることができます。

アジア太平洋が市場を独占

アジア太平洋地域が最大の市場シェアを占めており、飲食品セクターの急速な拡大により今後も支配的であり続けると思われます。また、都市化、生活水準の向上、小売店の拡大、支持的な経済要因が市場成長を後押しすると予測されます。例えば、中国経済は大きく成長しており、急速な都市化と所得の増加は中国人の食生活の多様化に寄与し、グルテンフリーのような高価値製品の需要を生み出し、キサンタンガムの需要を増加させています。さらに、この地域のいくつかの国の政府によって開始された投資や探査プロジェクトの増加が市場を後押ししています。例えば、アラブ首長国連邦は2022年7月、インド全土にフードパークを設置するために20億米ドルを投資する計画を発表しました。さらに、消費者の健康的なライフスタイルへの志向の高まりや、高品質な食品素材に対する意識の高まりが、同地域におけるキサンタンガムなどの食品添加物の需要に拍車をかけています。

キサンタンガム産業の概要

キサンタンガム市場は、多くの国内企業や多国籍企業が市場シェアを争っています。カーギル社、アーチャー・ダニエルズ・ミッドランド社、富豊集団、美華控股集団、J.M.フーバー社などです。製品革新は、有力企業が採用する魅力的な戦略的アプローチです。合併、拡大、買収、他社との提携は、ブランドの存在感を高め、市場シェアを高めるためにこれらの企業が採用する他の一般的な戦略です。さらに、規模の経済と消費者の高いブランド・ロイヤルティが、これらの企業に優位性を与えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 幅広い用途と機能性

- グルテンフリー製品に対する需要

- 市場抑制要因

- 経済的に可能な代替品の容易な入手

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 形態

- 液体

- 乾燥

- 用途

- 飲食品

- ベーカリー製品

- 菓子類

- 食肉製品

- 冷凍食品

- 乳製品

- 飲料

- その他

- 医薬品

- パーソナルケアと化粧品

- 石油精製

- その他の用途

- 飲食品

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- Cargill Incorporated

- Foodchem International Corporation

- The Archer-Daniels-Midland Company

- Deosen Biochemical Ltd.

- C.E. Roeper GmbH

- Ingredion Incorporated

- Solvay S.A

- International Flavours and Fragrances Inc

- Mitsubishi Corporation

- JM Huber Corporation

第7章 市場機会と今後の動向

The Xanthan Gum Market size is estimated at USD 0.80 billion in 2025, and is expected to reach USD 1.05 billion by 2030, at a CAGR of 5.71% during the forecast period (2025-2030).

Key Highlights

- Xanthan gum is derived from plant-based sugars and bacteria. It is mainly used in the food industry due to its thickening and stabilizing properties. Besides, it also improves the texture, consistency, flavor, shelf life, and appearance of food products. Additionally, due to its robust functional properties, xanthan gum is employed in formulations of bakery products, fruit juices, soups, ice cream, sauces, gravies, gluten-free products, and others.

- In addition, clear regulatory guidelines are fueling the market growth. For instance, the United States Food and Drug Administration (FDA) recognized using xanthan gum for direct human consumption as safe under the Code of Federal Regulations (CFR) 21. However, the regulatory body has set apart some prescribed conditions for using xanthan gum in food products.

- Xanthan is a vegan- and vegetarian-friendly hydrocolloid that readily complies with halal and kosher claims. Thus, it remains a promising substitute for other animal-sourced hydrocolloids for manufacturers willing to cater to a vegan consumer base.

- Prominent players in the market focus on developing new products, mergers, expansion, acquisitions, and partnerships with other companies to enhance brand presence and expand their market share. For instance, in July 2022, CP Kelco expanded its bio-gum production capacity, including xanthan gum, at its United States and China plant facilities.

Xanthan Gum Market Trends

Food and Beverage Industry is the Biggest Consumer of Xanthan Gum

Xanthan gum claims to improve the texture of bakery products and prevent them from becoming crumbly and dry. As it also helps retain moisture and enhance overall shelf life and acceptability, the increasing consumption of bakery products drives the use of xanthan gum. Furthermore, due to the growing demand for sugar-free and gluten-free chocolates, manufacturers use xanthan gum as a replacement for gluten because of its elasticity and structure in recipes lacking traditional gluten-containing ingredients. Over the medium term, the market is anticipated to expand with the rising need for healthy and functional confectionery products. The import-export of raw meat products is also increasing worldwide due to the increasing production of various meat products and rising demand for processed meat. Therefore, the demand for xanthan gum is growing as it is used as a thickening, suspending, stabilizing, and emulsifying agent in meat products. It can be used in ham, luncheon meat, red sausage, and other minced meat products to improve the water-holding capacity and tenderness.

Asia-Pacific Dominates the Market

Asia Pacific holds the largest market share and will continue to dominate due to the rapid expansion of the food and beverage sector. Also, urbanization, rising standard of living, expansion of retail stores, and supportive economic factors are projected to boost market growth. For instance, the Chinese economy is growing significantly, and the rapid urbanization and income growth contribute to diversifying the Chinese diet and creating a demand for high-value products like gluten-free, thereby increasing the demand for xanthan gum. In addition, increased investments and exploration projects initiated by governments of several countries across the region fuel the market. For instance, in July 2022, the United Arab Emirates announced its plans to invest USD 2 billion to set up food parks across India. Further, rising consumer inclination toward healthier lifestyles and increasing awareness about quality food ingredients are spurring demand for food additives such as xanthan gums in the region.

Xanthan Gum Industry Overview

The xanthan gum market is consolidated, with many domestic and multinational players competing for market share. Some prominent players in the market include Cargill Inc., Archer Daniels Midland Company, Fufeng Group, MeiHua Holdings Group Co. Ltd., and J. M. Huber Corporation. Product innovation is a compelling strategic approach adopted by leading players. Mergers, expansion, acquisitions, and partnerships with other companies are other common strategies adopted by these players to enhance brand presence and boost their market share. Further, economies of scale and high brand loyalty among consumers give these companies an upper edge.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Wide Applications and Functionality

- 4.1.2 Demand For Gluten-Free Products

- 4.2 Market Restraints

- 4.2.1 Easy Availability of Economically Feasible Alternatives

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Form

- 5.1.1 Liquid

- 5.1.2 Dry

- 5.2 Application

- 5.2.1 Food and Beverages

- 5.2.1.1 Bakery Products

- 5.2.1.2 Confectionery

- 5.2.1.3 Meat Products

- 5.2.1.4 Frozen Food

- 5.2.1.5 Dairy Products

- 5.2.1.6 Beverages

- 5.2.1.7 Others

- 5.2.2 Pharmaceuticals

- 5.2.3 Personal care and Cosmetics

- 5.2.4 Oil Refinery

- 5.2.5 Other Applications

- 5.2.1 Food and Beverages

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emrates

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategies Adopted by Leading Players

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Cargill Incorporated

- 6.3.2 Foodchem International Corporation

- 6.3.3 The Archer-Daniels-Midland Company

- 6.3.4 Deosen Biochemical Ltd.

- 6.3.5 C.E. Roeper GmbH

- 6.3.6 Ingredion Incorporated

- 6.3.7 Solvay S.A

- 6.3.8 International Flavours and Fragrances Inc

- 6.3.9 Mitsubishi Corporation

- 6.3.10 JM Huber Corporation