|

市場調査レポート

商品コード

1685953

構造用接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Structural Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 構造用接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

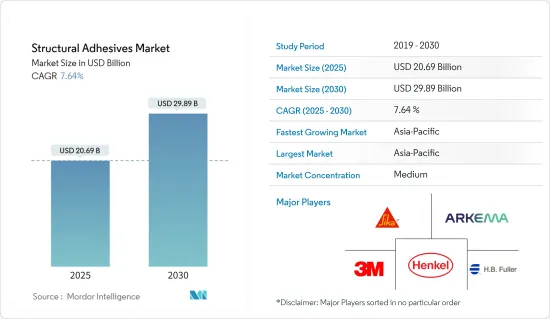

構造用接着剤の市場規模は2025年に206億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは7.64%で、2030年には298億9,000万米ドルに達すると予測されます。

市場は2020年にCOVID-19によってマイナスの影響を受けました。しかし、建設、自動車、風力エネルギーなど様々なエンドユーザー産業からの消費増加により、2021年には大幅に回復しました。

主なハイライト

- 短期的には、新興経済諸国における投資の増加と世界の建設・自動車セクターからの需要増加が市場開拓を牽引する可能性があります。

- しかし、環境と健康に対する懸念の高まりが市場の成長を妨げると予想されます。

- 水中構造用接着剤に関する調査の増加は、今後の市場成長の機会となりそうです。

- アジア太平洋が市場を独占し、中国での消費が最も顕著でした。

構造用接着剤市場の動向

建設業界からの需要増加

- 建設分野では、構造用接着剤は荷重や応力に耐える材料の接着に使用されます。これらの接着剤は、接着強度に影響を与えることなく、優れた耐衝撃性、破壊靭性、構造的柔軟性を提供します。

- 建設分野では、構造用接着剤は、コンクリート、耐荷重材料、アルミニウムやスチールなどの金属、プラスチック、人工木材などに耐久性を提供します。耐久性とは別に、構造用接着剤はエネルギー効率が高く、審美的に魅力的です。また、メンテナンスの必要性も低減します。これらの特性は、建物のファサードや橋のライフサイクルを延ばします。

- 建設業界で使用される構造用接着剤には、アクリル系構造用接着剤、スチール用接着剤、アンカー用接着剤、注入用接着剤、炭素繊維補強用接着剤、乾式吊り下げ用接着剤、シリコーン系構造用接着剤などがあります。

- 世界の建設活動の活発化に伴い、構造用接着剤の需要は予測期間中に増加すると予測されています。世界の建設市場は、2021年には約7兆2,000億米ドルと評価され、2022年には3.6%の成長率を示す可能性が高いです。

- アジア太平洋地域の建設セクターは世界最大であり、人口増加、中間所得層の増加、都市化により健全なペースで拡大しています。また、中国とインドにおける住宅建設市場の拡大により、アジア太平洋地域で最も高い成長が見込まれています。中国国家統計局によると、2021年の同国の建設工事生産額は25兆9,200億人民元(~4兆300億米ドル)で、2020年の23兆2,700億人民元(~3兆6,200億米ドル)から増加しています。

- 北米の建設業界では米国が大きなシェアを占めています。カナダとメキシコも建設部門に大きく貢献しています。米国国勢調査局によると、同国の新規建設額は2020年の1兆4,995億7,000万米ドルから増加し、2021年には1兆6,264億4,400万米ドルに達します。

- したがって、上記のすべての要因は、調査された市場の需要に大きな影響を与えると思われます。

市場を独占するアジア太平洋地域

- アジア太平洋地域は、2021年の構造用接着剤の世界市場を独占しました。中国は世界最大の構造用接着剤消費国の一つです。

- 2022年1月に発表された中国の5ヵ年計画によると、同国の建設業界は2022年に約6%の成長率を記録すると推定されています。中国は、建設現場からの汚染や廃棄物を減らすため、プレハブ建築の建設を増やす計画です。

- さらに、国家開発改革委員会(National Development and Reform Commission)によると、中国政府は約1,420億米ドルを投資すると推定される26のインフラプロジェクトを承認しました。これらのプロジェクトは現在進行中であり、2023年までに完了すると推定されています。

- 中国は世界最大の自動車メーカーです。OICAによると、同国の自動車生産台数は2021年に2,608万台に達し、2020年の2,523万台から3%増加しました。自動車生産台数の増加は、特にハイエンドの自動車製造セクターにおいて、構造用接着剤の需要を促進すると推定されます。

- さらに、ストックホルム国際平和研究所(SIPRI)によると、米国に次いで世界第2位の軍事費支出国である中国は、2021年に推定2,930億米ドルを軍事費に充てる。これは2020年比で4.7%の増加です。2021年の中国の予算は、2025年まで続く第14次5カ年計画の下での最初のものでした。

- インドの巨大な建設部門は、2022年までに世界第3位の建設市場になると予想されています。スマートシティプロジェクトや2022年までの万人向け住宅建設など、インド政府が実施するさまざまな政策が、低迷する建設業界に弾みをつけると期待されています。

- 自動車部門と航空宇宙部門は、構造用接着剤の他の重要なユーザーです。OICAによると、2021年にインドで生産された自動車は約439万9,112台で、2020年の338万1,819台に比べ30%増加しました。

- 上記の要因は、予測期間中、アジア太平洋地域における構造用接着剤の需要に影響を与えると予想されます。

構造用接着剤産業の概要

世界の構造用接着剤市場は部分的に断片化された性質を持っており、様々な国内外のプレーヤーが存在しています。主なプレーヤーは、Henkel AG & Co. KGaA, Sika AG, 3M, H.B. Fuller Company, Arkemaなどです(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋地域の新興経済諸国における投資の増加

- 世界の建設セクターと自動車セクターからの需要増加

- 抑制要因

- 環境と健康に対する懸念の高まり

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 樹脂タイプ別

- エポキシ

- ポリウレタン

- アクリル

- シアノアクリレート

- メタクリル酸メチル

- その他の樹脂タイプ

- エンドユーザー産業別

- 建築

- 自動車

- 航空宇宙

- 風力エネルギー

- その他のエンドユーザー産業

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 合併、買収、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema

- Bondloc UK Ltd

- DuPont

- Engineered Bonding Solutions LLC

- Forgeway Ltd

- H. B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- LG Chem

- Parker Hannifin Corp.

- Sika AG

- RS Industrial

第7章 市場機会と今後の動向

- 成長する水中構造用接着剤の調査

The Structural Adhesives Market size is estimated at USD 20.69 billion in 2025, and is expected to reach USD 29.89 billion by 2030, at a CAGR of 7.64% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. However, it recovered significantly in 2021, owing to rising consumption from various end-user industries, such as construction, automotive, and wind energy.

Key Highlights

- Over the short term, the increasing investments in developing Asia-Pacific economies and increasing demand from the global construction and automotive sectors may drive the market studied.

- However, growing environmental and health concerns are expected to hinder the growth of the studied market.

- The growing research on underwater structural adhesives is likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the market, with the most significant consumption recorded in China.

Structural Adhesives Market Trends

Increasing Demand from the Construction Industry

- In the construction sector, structural adhesives are used to bond materials to withstand loads or stresses. These adhesives offer good impact resistance, fracture toughness, and structural flexibility without affecting bond strength.

- In the construction sector, structural adhesives provide durability to concrete, load-bearing materials, metals such as aluminum and steel, plastics, engineered woods, etc. Apart from durability, structural adhesives are energy-efficient and aesthetically appealing. They also reduce the need for maintenance. These characteristics extend the life cycle of building facades and bridges.

- Some essential structural adhesives used in the construction industry include acrylic structural adhesives, steel glue, anchor glue, pouring glue, carbon fiber reinforcement glue, dry-hanging adhesives, and silicone structural adhesives.

- With growing construction activity worldwide, the demand for structural adhesives is projected to increase during the forecast period. The global construction market was valued at around USD 7.2 trillion in 2021 and is likely to witness a growth rate of 3.6% in 2022.

- The construction sector in the Asia-Pacific region is the largest in the world and is expanding at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization. The highest growth for housing is also expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. According to the National Bureau of Statistics of China, the output value of the construction works in the country in 2021 was CNY 25.92 trillion (~USD 4.03 trillion), increasing from CNY 23.27 trillion (~ USD 3.62 trillion) in 2020.

- The United States occupies a significant share of the North American construction industry. Canada and Mexico also contribute significantly to the construction sector. According to the US Census Bureau, the value of new construction put in place in the country accounted for USD 1,626,444 million in 2021, increasing from USD 1,499,570 million in 2020.

- Therefore, all the factors mentioned above are likely to impact the demand in the market studied significantly.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global structural adhesives market in 2021. China is one of the world's largest consumers of structural adhesives.

- According to China's Five-Year Plan, unveiled in January 2022, the country's construction industry is estimated to register a growth rate of approximately 6% in 2022. China plans to increase the construction of prefabricated buildings to reduce pollution and waste from construction sites.

- Moreover, as per the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects with an estimated investment of around USD 142 billion. These projects are in progress and are estimated to be completed by 2023.

- China is the largest manufacturer of automobiles in the world. According to the OICA, the automotive production in the country reached 26.08 million in 2021, which increased by 3% compared to 25.23 million vehicles produced in 2020. The increase in automotive production is estimated to drive the demand for structural adhesives, especially in the high-end vehicle manufacturing sector.

- Furthermore, as per the Stockholm International Peace Research Institute (SIPRI), China, the world's second-largest spender on the military after the United States, allocated an estimated USD 293 billion to its military in 2021. This was an increase of 4.7% compared to 2020. The 2021 Chinese budget was the first under the 14th Five-Year Plan, which runs until 2025.

- India's massive construction sector is expected to become the world's third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project and Housing for all by 2022, are expected to prove an impetus to the slowing construction industry.

- The automotive and aerospace sectors are the other significant users of structural adhesives. According to OICA, around 4,399,112 vehicles were produced in India in 2021, which increased by 30% compared to 3,381,819 units in 2020.

- The factors above are expected to affect the demand for structural adhesives in the Asia-Pacific region over the forecast period.

Structural Adhesives Industry Overview

The global structural adhesives market is partially fragmented in nature, with the presence of various international and domestic players. Some of the major players include Henkel AG & Co. KGaA, Sika AG, 3M, H.B. Fuller Company, and Arkema (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase in Investments in Developing Economies in Asia-Pacific

- 4.1.2 Increasing Demand from the Global Construction and Automotive Sectors

- 4.2 Restraints

- 4.2.1 Growing Environmental and Health Concerns

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Cyanoacrylate

- 5.1.5 Methyl Methacrylate

- 5.1.6 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Construction

- 5.2.2 Automotive

- 5.2.3 Aerospace

- 5.2.4 Wind Energy

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Bondloc UK Ltd

- 6.4.4 DuPont

- 6.4.5 Engineered Bonding Solutions LLC

- 6.4.6 Forgeway Ltd

- 6.4.7 H. B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 Illinois Tool Works Inc.

- 6.4.11 LG Chem

- 6.4.12 Parker Hannifin Corp.

- 6.4.13 Sika AG

- 6.4.14 RS Industrial

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Research on Underwater Structural Adhesives