|

市場調査レポート

商品コード

1693655

小型商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小型商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 482 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

小型商用車の市場規模は2025年に5,169億米ドルと推定・予測され、2029年には6,599億米ドルに達すると予測され、予測期間中(2025-2029年)のCAGRは6.30%で成長する見込みです。

急成長するeコマースと物流部門が小型商用車市場に拍車をかける

- 小型商用車市場の原動力となっているのは、eコマースと物流分野です。インターネットやスマートフォンにアクセスできる人が増えたため、オンライン小売販売やeコマースが増加しています。小型商用車の購入は増加すると予測され、顧客への迅速な商品配送を支援します。

- COVID-19オンライン販売の結果、世界のeコマース市場の収入とユーザーベースは大幅に拡大しました。しかし、インターネットショッピングの人気の高まりが成長を促すと思われます。世界のeコマース市場は2020年に顕著な拡大を経験し、2021年には26兆7,000億米ドルの売上を生み出しました。オンラインショッピング利用者の数と割合はここ数年、世界的に絶えず増加しています。2020年にオンライン買い物客の数が最も増加したのは、COVID-19の大流行によるもので、これにより個人はオンラインショッピングを余儀なくされました。

- 欧州、米国、中国を含む主要経済圏におけるeコマースおよびロジスティクス産業の急速な拡大が、より現代的な流通ネットワークへの需要に拍車をかけています。そのため、小型商用車の需要は増加すると思われます。ダイムラー、日産、フォード、ルノーといった主要な小型商用車メーカーは、eコマースの売上が劇的に増加し、物流業界を強化しました。ピックアップトラックやバンは、従来から物流や消費者向け配送サービスのためのeコマース輸送の要件を満たしており、これは世界の小型商用車市場にかなりの好影響を与えると予想されます。

欧州、米国、中国といった主要経済圏にまたがるeコマースとロジスティクス部門の急成長が、より高度な物流ネットワークの必要性を後押ししています。

- eコマースとロジスティクス産業は、小型商用車市場の主な促進要因です。インターネットやスマートフォンの普及率の上昇に伴い、オンライン小売やeコマースの売上が急増しています。この動向は、より迅速な配送を可能にする小型商用車の需要を促進すると予想されます。2016年の小型商用車の世界生産台数は1,721万7,999台で、2021年には1,859万3,850台に達すると予測されています。

- COVID-19の大流行は、収益とユーザーベースの両面で、世界のeコマース部門を大幅に押し上げました。オンライン・ショッピングの人気がさらに高まるにつれて、この動向は続くと予想されます。2020年、世界のeコマース市場は大幅な成長を遂げ、2021年には26兆7,000億米ドルの売上に達します。オンラインショッピング利用者の数と割合は世界中で着実に増加しており、2020年にはパンデミックが触媒として作用し、より多くの個人をオンラインショッピングに向かわせた。

- 欧州、米国、中国といった主要経済圏にまたがるeコマースとロジスティクス分野の急成長は、より高度な物流ネットワークの必要性を促しています。その結果、小型商用車の需要は増加の一途をたどっています。特に、ダイムラー、日産、フォード、ルノーといった著名な小型商用車メーカーは、eコマース売上が大幅に急増し、物流部門を強化しています。歴史的に、ピックアップトラックとバンはeコマース輸送に最適な選択肢であり、物流と消費者配送サービスの両方に対応してきました。この動向は、世界の小型商用車市場に顕著な好影響を与えると予想されます。

世界の小型商用車市場の動向

世界の需要の高まりと政府の支援が電気自動車市場の成長を後押し

- 電気自動車(EV)は、エネルギー効率を高め、温室効果ガスや公害の排出を削減する可能性に後押しされ、自動車産業において不可欠なものとなっています。この急成長の主な要因は、環境に対する関心の高まりと政府の支援策にあります。特に、EVの世界販売台数は、2021年と比較して2022年には10.82%増と堅調な伸びを示しました。予測によると、電気乗用車の年間販売台数は2025年末までに500万台を突破し、自動車販売台数全体の約15%を占めるようになります。

- ロンドン警視庁消防局のような大手メーカーや組織は、電動モビリティ戦略を積極的に推進しています。例えば、2025年までに車両をゼロエミッション化し、2030年までにバンの40%を電動化、2040年までに完全電動化を達成するという目標を掲げています。世界的にも同様の動向が予想され、2024年から2030年にかけて電気自動車の需要と販売が急増します。

- アジア太平洋と欧州は、バッテリー技術と車両電化の進歩に牽引され、電気自動車生産を支配する態勢を整えています。2020年5月、起亜自動車欧州は「プランS」を発表し、電動化への戦略的シフトを表明しました。この決定は、起亜のEVが欧州で記録的な販売台数を達成したことを受けてのものです。起亜は2025年までに、乗用車、SUV、MPVなどさまざまなセグメントにまたがる11のEVモデルを世界に投入するという野心的な計画を掲げています。同社は、2026年までにEVの世界年間販売台数50万台の達成を目指しています。

小型商用車業界の概要

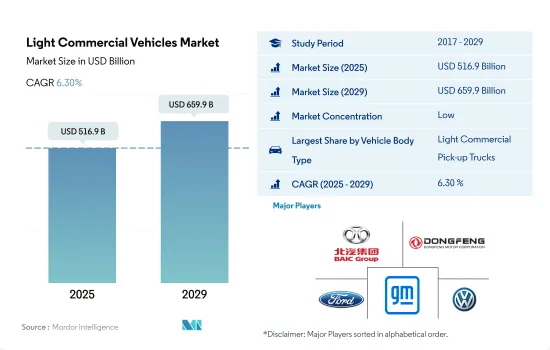

小型商用車市場は細分化されており、上位5社で24.80%を占めています。この市場の主要企業は以下の通り。 BAIC Motor Corporation Ltd., Dongfeng Motor Corporation, Ford Motor Company, General Motors Company and Volkswagen AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 一人当たりGDP

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 自動車購入のための消費支出(cvp)

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- インフレ率

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 自動車ローンの金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- Xev新モデル発表

- ロジスティクス・パフォーマンス・インデックス

- アフリカ

- アジア太平洋

- 欧州

- 中東

- 北米

- 南米

- 燃料価格

- メーカー別生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 商用車

- 小型商用ピックアップトラック

- 小型商用バン

- 商用車

- 推進タイプ

- ハイブリッド車および電気自動車

- 燃料カテゴリー別

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 燃料カテゴリー別

- 天然ガス

- ディーゼル

- ガソリン

- LPG

- ハイブリッド車および電気自動車

- 地域別

- アフリカ

- 南アフリカ

- アフリカ

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- タイ

- アジア太平洋地域のその他諸国

- 欧州

- オーストリア

- ベルギー

- チェコ共和国

- デンマーク

- エストニア

- フランス

- ドイツ

- アイルランド

- イタリア

- ラトビア

- リトアニア

- ノルウェー

- ポーランド

- ロシア

- スペイン

- スウェーデン

- 英国

- その他欧州

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- 北米

- カナダ

- メキシコ

- 米国

- 北米残り

- 南米

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ashok Leyland Limited

- BAIC Motor Corporation Ltd.

- BYD Auto Co. Ltd.

- Daimler AG(Mercedes-Benz AG)

- Dongfeng Motor Corporation

- Ford Motor Company

- General Motors Company

- Groupe Renault

- Isuzu Motors Limited

- Mahindra & Mahindra Limited

- Nissan Motor Co. Ltd.

- Rivian Automotive Inc.

- Tata Motors Limited

- Volkswagen AG

- Volvo Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Light Commercial Vehicles Market size is estimated at 516.9 billion USD in 2025, and is expected to reach 659.9 billion USD by 2029, growing at a CAGR of 6.30% during the forecast period (2025-2029).

The rapidly growing e-commerce and logistics sectors fuel the light commercial vehicles market

- The e-commerce and logistics sectors fuel the light commercial vehicle market. Online retail sales and e-commerce have been rising due to more people having access to the internet and smartphones. Light commercial vehicle purchases are projected to rise, which will assist in the prompt delivery of goods to clients.

- As a result of COVID-19 online sales, the income and user base of the global e-commerce market greatly expanded. However, the increased popularity of internet shopping will encourage growth. The global e-commerce market experienced a remarkable expansion in 2020, and by 2021, it generated USD 26.7 trillion in sales. The number and percentage of online shoppers have constantly increased globally over the last few years. The highest increase in the number of online shoppers in 2020 was caused by the COVID-19 pandemic, which forced individuals to shop online.

- The rapid expansion of the e-commerce and logistics industries across major economies, including Europe, the United States, and China, is fueling the demand for a more contemporary distribution network. Thus, the demand for light commercial vehicles will increase. Significant light commercial vehicle manufacturers, like Daimler, Nissan, Ford, and Renault, experienced a dramatic increase in e-commerce sales, which bolstered the logistics industry. Pick-up trucks and vans have traditionally filled the requirement for e-commerce transportation for logistics and consumer delivery services, which is expected to have a substantial positive impact on the global light commercial vehicle market.

The rapid growth of the e-commerce and logistics sectors, spanning major economies like Europe, the United States, and China, is driving the need for more advanced distribution networks

- The e-commerce and logistics industries are the primary drivers of the light commercial vehicle market. With the rising internet and smartphone penetration, online retail and e-commerce sales have surged. This trend is expected to drive the demand for light commercial vehicles, enabling faster deliveries. In 2016, the global production of light commercial vehicles stood at 17,217,999 units and was projected to reach 18,593,850 units by 2021.

- The COVID-19 pandemic has significantly boosted the global e-commerce sector, both in terms of revenue and user base. This trend is expected to continue as online shopping gains further popularity. In 2020, the global e-commerce market witnessed substantial growth, culminating in sales worth USD 26.7 trillion by 2021. The number and proportion of online shoppers have been steadily rising worldwide, with the pandemic acting as a catalyst in 2020, pushing more individuals toward online shopping.

- The rapid growth of the e-commerce and logistics sectors, spanning major economies like Europe, the United States, and China, is driving the need for more advanced distribution networks. Consequently, the demand for light commercial vehicles is poised to rise. Notably, prominent light commercial vehicle manufacturers such as Daimler, Nissan, Ford, and Renault have witnessed a significant surge in e-commerce sales, bolstering the logistics sector. Historically, pick-up trucks and vans have been the go-to choices for e-commerce transportation, catering to both logistics and consumer delivery services. This trend is expected to have a pronounced positive impact on the global light commercial vehicle market.

Global Light Commercial Vehicles Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Light Commercial Vehicles Industry Overview

The Light Commercial Vehicles Market is fragmented, with the top five companies occupying 24.80%. The major players in this market are BAIC Motor Corporation Ltd., Dongfeng Motor Corporation, Ford Motor Company, General Motors Company and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.8.1 Africa

- 4.8.2 Asia-Pacific

- 4.8.3 Europe

- 4.8.4 Middle East

- 4.8.5 North America

- 4.8.6 South America

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.10.1 Africa

- 4.10.2 Asia-Pacific

- 4.10.3 Europe

- 4.10.4 Middle East

- 4.10.5 North America

- 4.10.6 South America

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Light Commercial Pick-up Trucks

- 5.1.1.2 Light Commercial Vans

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 South Africa

- 5.3.1.2 Rest-of-Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Malaysia

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Rest-of-APAC

- 5.3.3 Europe

- 5.3.3.1 Austria

- 5.3.3.2 Belgium

- 5.3.3.3 Czech Republic

- 5.3.3.4 Denmark

- 5.3.3.5 Estonia

- 5.3.3.6 France

- 5.3.3.7 Germany

- 5.3.3.8 Ireland

- 5.3.3.9 Italy

- 5.3.3.10 Latvia

- 5.3.3.11 Lithuania

- 5.3.3.12 Norway

- 5.3.3.13 Poland

- 5.3.3.14 Russia

- 5.3.3.15 Spain

- 5.3.3.16 Sweden

- 5.3.3.17 UK

- 5.3.3.18 Rest-of-Europe

- 5.3.4 Middle East

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 UAE

- 5.3.4.3 Rest-of-Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.5.2 Mexico

- 5.3.5.3 US

- 5.3.5.4 Rest-of-North America

- 5.3.6 South America

- 5.3.6.1 Argentina

- 5.3.6.2 Brazil

- 5.3.6.3 Rest-of-South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ashok Leyland Limited

- 6.4.2 BAIC Motor Corporation Ltd.

- 6.4.3 BYD Auto Co. Ltd.

- 6.4.4 Daimler AG (Mercedes-Benz AG)

- 6.4.5 Dongfeng Motor Corporation

- 6.4.6 Ford Motor Company

- 6.4.7 General Motors Company

- 6.4.8 Groupe Renault

- 6.4.9 Isuzu Motors Limited

- 6.4.10 Mahindra & Mahindra Limited

- 6.4.11 Nissan Motor Co. Ltd.

- 6.4.12 Rivian Automotive Inc.

- 6.4.13 Tata Motors Limited

- 6.4.14 Volkswagen AG

- 6.4.15 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms