|

市場調査レポート

商品コード

1693626

欧州の小型商用車市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の小型商用車市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 274 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

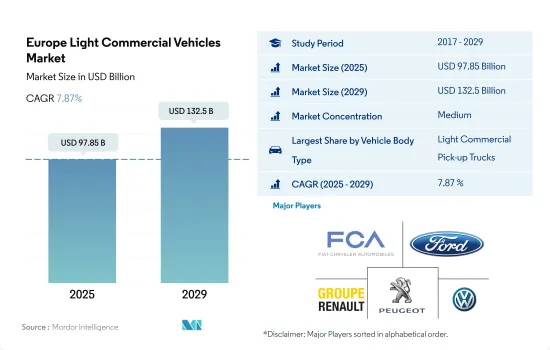

欧州の小型商用車市場規模は2025年に978億5,000万米ドルと推定・予測され、2029年には1,325億米ドルに達し、予測期間(2025-2029年)のCAGRは7.87%で成長すると予測されます。

欧州のLCV市場はインフラ投資とeコマースの急増で繁栄し、都市化とグリーンイニシアチブの中で継続的な成長が期待される

- 2022年、欧州の小型商用車(LCV)市場は販売台数で6.2%の堅調な伸びを示しました。この好調な勢いは今後も続き、2023年には3.5%の成長が予測されます。この成長の主な要因は、インフラ投資の活発化とeコマースの急増です。EUが輸送とエネルギー・プロジェクトに注力していることが、特に建設と公共事業セクターのLCV需要を刺激しています。パンデミック(世界的大流行)の際に拡大したラストワンマイル配送網の動向は、小包や食品配送用の小型商用バンの購入に拍車をかけています。

- 2017年から2023年にかけて、欧州のLCV市場は顕著な上昇を見せ、台数は38%急増しました。この急増はeコマースブームによって推進されたもので、配送ネットワークの拡大に拍車がかかり、それに伴いバンの販売台数も増加しました。さらに、小売、建設、サービスなどのセクターからの買い替え需要が極めて重要な役割を果たしました。2020年にはパンデミックによる混乱で市場が縮小したもの、デジタル化の加速の波に乗って急速に回復しました。全体として、着実な経済成長と堅調なインフラ投資が、この期間の欧州LCV市場拡大の主要因となりました。

- 欧州のLCV市場は、2024年から2030年にかけてCAGR 3.1%を記録する見通しです。この成長軌道は、継続的なインフラ開発、ラストマイル配送網の継続的拡大、都市化傾向の高まりによって推進されます。これらの要因は、サービス、食品配達、建設分野でのLCV需要の増加と相まって、有望な見通しを描いています。しかし、排出ガスや都市部へのアクセスに関する規制の進化が代替燃料バンの採用を促進する可能性があるため、市場は逆風に直面する可能性があります。

欧州の小型商用車市場の国別動向は、同地域の排出ガス削減と効率向上の推進を浮き彫りにしています。

- 欧州の主要市場では、2022年のLCV販売台数にばらつきが見られたが、これはそれぞれの経済状況を反映しています。ドイツは回復力のある経済に支えられ、6.3%の堅調な伸びを示しました。一方、英国は経済の不確実性に直面し、LCV販売台数は2.1%減少しました。フランス、イタリア、スペインは3%から5%の減少となり、マクロ経済全体の課題と一致しました。しかし、パンデミック後の状況が改善するにつれて、2023年には回復が見られ、ほとんどの国で4~6%の台数成長が見込まれます。

- 2017年から2021年にかけて、欧州の主要なLCV市場であるドイツ、フランス、イタリア、スペイン、ポーランドは健全な拡大を示し、パンデミック前のCAGRは約3~5%を記録しました。この成長は、特に建設、配送、サービスなどの産業における堅調な経済活動によって推進されました。2020年のパンデミックによる景気縮小は比較的短期間で収束したが、財政刺激策の格差や小売・接客業などの産業の脆弱性が主因となって、回復にはばらつきがあります。

- 欧州のLCV市場は、2023年から2029年まで年平均3~4%の成長が予想され、より安定した成長軌道を描いています。インフラ投資、ラストマイルデリバリーネットワークの台頭、継続的な景気回復といった要因が需要を押し上げると予想されます。しかし、高インフレ、エネルギーコスト、政治的不確実性といった要因によるリスクも存在します。さらに、市場の電動ドライブトレインへのシフトは、市場のダイナミクスをさらに形作ると思われます。欧州のLCV市場は、長期的には緩やかに拡大するとみられます。

欧州の小型商用車市場の動向

環境問題、政府の支援、脱炭素化目標が欧州の電気自動車需要と販売に拍車をかける

- 欧州各国における電気自動車の需要と販売は、ここ数年で大きく伸びています。ドイツは2022年に電気自動車の販売台数が2021年比で22%増加し、次いで英国が2022年に2021年比で18.40%増加しました。環境問題への関心の高まり、政府の厳しい規範、燃費の良さ、サービスコストの低さ、二酸化炭素排出量の少なさといった電気自動車の利点、政府による補助金などが、欧州諸国における電気自動車の成長に寄与している要因のひとつです。

- 電気商用車、特に小型トラックの需要は、欧州諸国で徐々に伸びています。さらに、各国の政府も電気自動車の導入を支援しています。2021年11月、英国政府は2040年までにすべての大型車をゼロ・エミッションにするという公約を発表しました。このような要因により、英国における2022年の電気商用車販売台数は2021年比で23.17%増加し、各国の同様の慣行が欧州全域で電気商用車の需要を高めています。

- 欧州諸国における車両の電動化は、今後数年間で飛躍的に成長すると予測されています。脱炭素化に向けた各国政府の取り組みが、欧州の電気商用車市場を牽引すると予想されます。例えば、2022年1月、ドイツの運輸大臣は、2030年までに1,500万台の電気自動車を走らせるという目標を発表しました。こうした要因により、欧州諸国では2024~2030年の間に電気自動車の販売が増加すると予想されます。

欧州の小型商用車産業の概要

欧州の小型商用車市場は適度に統合されており、上位5社で62.47%を占めています。この市場の主要企業は以下の通り。 Fiat Chrysler Automobiles N.V, Ford Motor Company, Groupe Renault, Peugeot S.A. and Volkswagen AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 物流性能指数

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 商用車

- 小型商用ピックアップトラック

- 小型商用バン

- 商用車

- 推進タイプ

- ハイブリッド車および電気自動車

- 燃料カテゴリー別

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 天然ガス

- ディーゼル

- ガソリン

- LPG

- ハイブリッド車および電気自動車

- 国名

- オーストリア

- ベルギー

- チェコ共和国

- デンマーク

- エストニア

- フランス

- ドイツ

- アイルランド

- イタリア

- ラトビア

- リトアニア

- ノルウェー

- ポーランド

- ロシア

- スペイン

- スウェーデン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Fiat Chrysler Automobiles N.V

- Ford Motor Company

- Groupe Renault

- Mercedes-Benz

- Peugeot S.A.

- Toyota Motor Corporation

- Volkswagen AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Light Commercial Vehicles Market size is estimated at 97.85 billion USD in 2025, and is expected to reach 132.5 billion USD by 2029, growing at a CAGR of 7.87% during the forecast period (2025-2029).

The European LCV market thrives on infrastructure investments and e-commerce surge, with continued growth expected amid urbanization and green initiatives

- In 2022, the light commercial vehicle (LCV) market in Europe witnessed a robust 6.2% growth in sales volume. This positive momentum is expected to carry forward, with a projected growth of 3.5% in 2023. This growth is primarily fueled by heightened infrastructure investments and the surging tide of e-commerce. The EU's focus on transportation and energy projects has stimulated demand for LCVs, especially from the construction and utilities sectors. The expansion of last-mile delivery networks, a trend amplified during the pandemic, has spurred purchases of light commercial vans for parcel and food delivery.

- From 2017 to 2023, Europe's LCV market witnessed a remarkable upswing, with volumes surging by 38%. This surge was propelled by the e-commerce boom, which fueled the expansion of delivery networks and subsequently boosted van sales. Additionally, replacement demand from sectors like retail, construction, and services played a pivotal role. While the market contracted in 2020 due to pandemic disruptions, it swiftly rebounded, riding the wave of accelerated digital adoption. Overall, steady economic growth and robust infrastructure investments were key drivers of the European LCV market's expansion during this period.

- The LCV market in Europe is poised to register a CAGR of 3.1% from 2024 to 2030. This growth trajectory will be propelled by ongoing infrastructure development, the continued expansion of last-mile delivery networks, and the rising urbanization trend. These factors, coupled with the increasing demand for LCVs in services, food delivery, and construction sectors, paint a promising outlook. However, the market may face headwinds as evolving regulations on emissions and urban access could bolster the adoption of alternatively fueled vans.

Country-specific trends within the European light commercial vehicles market highlight the region's push toward reducing emissions and enhancing efficiency

- Major European markets witnessed varying LCV sales volumes in 2022, reflecting their distinct economic landscapes. Germany, buoyed by a resilient economy, saw a robust 6.3% growth. Conversely, the United Kingdom faced economic uncertainties, leading to a contraction of 2.1% in LCV sales. France, Italy, and Spain experienced declines of 3% to 5%, aligning with broader macroeconomic challenges. However, as the post-pandemic conditions improve, 2023 is projected to witness a rebound, with most countries eyeing a volume growth of 4-6%.

- From 2017 to 2021, the prominent European LCV markets - Germany, France, Italy, Spain, and Poland - showcased healthy expansion, registering a pre-pandemic CAGR of approximately 3-5%. This growth was propelled by robust economic activities, particularly in industries like construction, delivery, and services. While the pandemic-induced contractions in 2020 were relatively short-lived, the recovery has been uneven, primarily due to disparities in fiscal stimulus measures and vulnerabilities in industries such as retail and hospitality.

- The European LCV market is poised for a steadier growth trajectory, with an anticipated annual average of 3-4% from 2023 to 2029. Factors such as infrastructure investments, the rise of last-mile delivery networks, and ongoing economic recovery are expected to bolster demand. However, risks loom from factors like high inflation, energy costs, and political uncertainties. Additionally, the market's shift toward electric drivetrains will further shape its dynamics. The European LCV market is set for a gradual expansion in the long run.

Europe Light Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Light Commercial Vehicles Industry Overview

The Europe Light Commercial Vehicles Market is moderately consolidated, with the top five companies occupying 62.47%. The major players in this market are Fiat Chrysler Automobiles N.V, Ford Motor Company, Groupe Renault, Peugeot S.A. and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Light Commercial Pick-up Trucks

- 5.1.1.2 Light Commercial Vans

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Fiat Chrysler Automobiles N.V

- 6.4.2 Ford Motor Company

- 6.4.3 Groupe Renault

- 6.4.4 Mercedes-Benz

- 6.4.5 Peugeot S.A.

- 6.4.6 Toyota Motor Corporation

- 6.4.7 Volkswagen AG

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms