|

市場調査レポート

商品コード

1773314

自動車用エンジンカバーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Engine Cover Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用エンジンカバーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

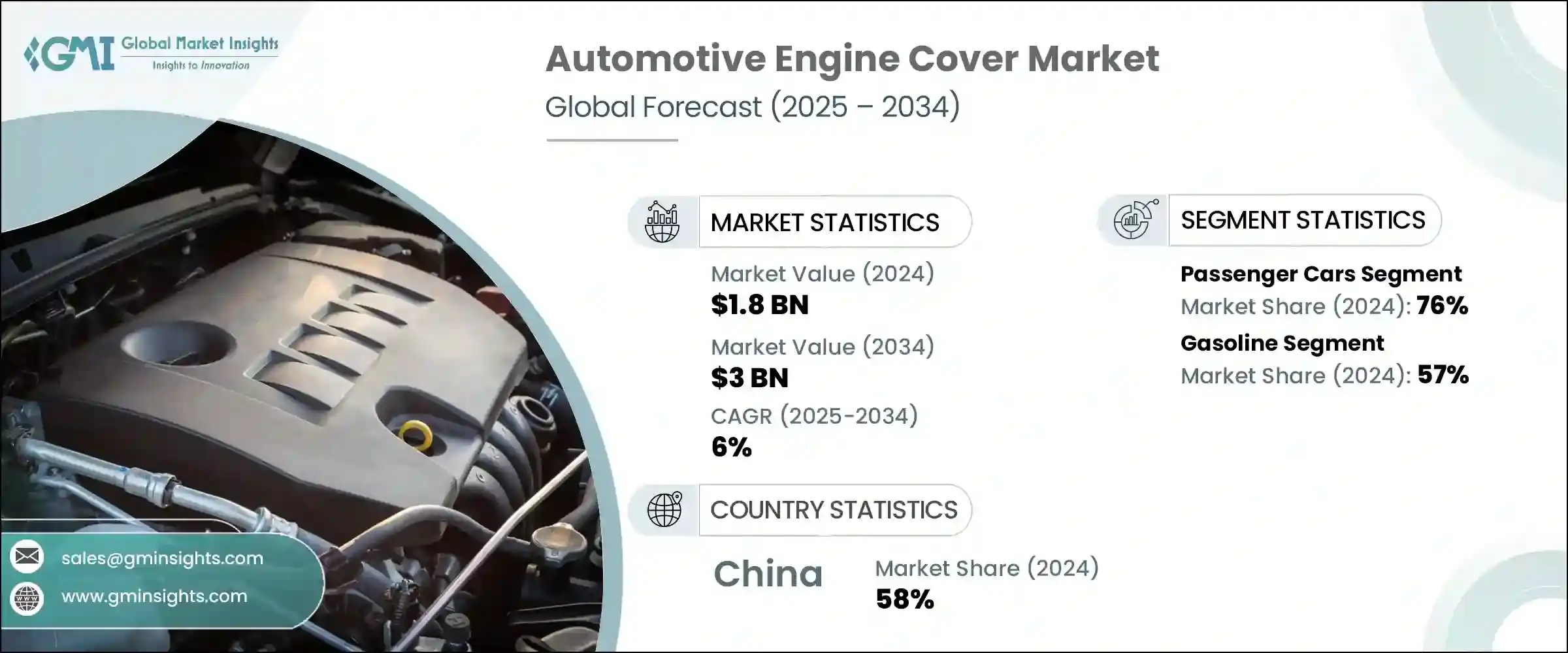

自動車用エンジンカバーの世界市場規模は、2024年に18億米ドルとなり、CAGR6%で成長し、2034年までには30億米ドルに達すると推定されています。

この成長の原動力は、世界の自動車生産台数の増加と、より軽量で効率的な自動車部品へのニーズの高まりです。業界がより高い性能と燃費を追求する方向にシフトするにつれ、エンジンカバーは基本的な筐体から、熱制御、遮音、車両デザイン全体との視覚的な調和を実現する重要な部品へと変貌を遂げています。内燃機関車とハイブリッド車の両プラットフォームが世界的に拡大し続ける中、エンジンカバーは幅広い車種と用途でパワートレイン設計の重要な要素として設計されています。

また、複合材料や熱可塑性プラスチックのような先端材料へのシフトにより、この市場は力強い牽引力を見せています。これらの材料は、耐久性、耐熱性、軽量化の適切なバランスを提供し、メーカーが厳しい排出ガス規制や燃費基準を満たすことを可能にします。相手先商標製品メーカーやTier-1サプライヤーは、コンパクトカー、スポーツ用多目的車、小型トラックの生産に対応するため、スケーラブルなモジュール式カバー設計を採用しています。これらのプラットフォームは、均一なNVH(騒音、振動、ハーシュネス)性能を達成すると同時に、市場投入までの時間を短縮し、製造の複雑さを軽減するのに役立ちます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 18億米ドル |

| 予測金額 | 30億米ドル |

| CAGR | 6% |

乗用車セグメントは2024年に76%のシェアを占め、2034年までのCAGRは6.8%と予測されます。エンジンカバーは、狭いエンジンベイとより高いエンジン出力が要求される現代の乗用車の設計に不可欠な部品となっています。セダン、ハッチバック、高級車に組み込まれることで、メーカーは性能と車内体験の両方を向上させています。軽量な熱可塑性プラスチックや強化複合材は、断熱性と高級な美観を併せ持つ、なめらかで空力特性に優れた、ブランドにふさわしいカバーを作るために使用されています。

ガソリン車セグメントは2024年に57%のシェアで市場をリードし、2034年までのCAGRは7.1%と予想されます。電動モビリティの台頭にもかかわらず、ガソリンエンジンは多くの地域で引き続き生産台数の大半を占めています。これらの自動車のエンジンカバーは、高い燃焼熱を管理し、エンジンノイズを低減すると同時に、視覚的な魅力を高めるように設計されています。メーカーは、より低い生産コストで最適化された熱遮蔽と軽量の利点を提供するために、複合材料やポリマーブレンドに目を向けています。

アジア太平洋の自動車用エンジンカバー市場は58%のシェアを占め、2024年には5億5,310万米ドルを創出しました。中国の優位性は、大規模な自動車製造インフラ、消費者需要の高まり、世界OEMと国内部品メーカーの積極的なプレゼンスによって支えられています。中国の主要企業は、多様な自動車プラットフォームに対応するため、熱可塑性プラスチックや複合材エンジンカバーの大量生産に注力しています。現地での技術革新と環境に優しい技術を奨励する政府の政策が、軽量で排出ガスを削減する部品の需要を促進しています。世界の企業は、次世代モビリティ動向に沿ったカスタム設計のエンジンカバーシステムを提供するため、世界なパートナーシップを通じて拡大を続けています。

この業界で事業を展開している主要企業には、Rochling Group、Denso Corporation、MAHLE GmbH、Woco Industrietechnik、Montaplast、Toyota Boshoku Corporation、Aisin Corporation、Valeo S.A.、ElringKlinger、Continentalなどがあります。市場各社は、先進的な製造技術を活用して、世界の燃費規制を満たす軽量で耐久性のあるエンジンカバーを提供しています。各社は、軽量化と同時に耐熱性を向上させるため、特に熱可塑性プラスチックや複合材料の配合など、材料科学の革新に投資しています。自動車メーカーとの戦略的提携は、メーカーが製品開発を進化するプラットフォームのニーズに合わせるのに役立ちます。多様な車種に対応するため、モジュラー設計やスケーラブル設計の採用が進んでおり、金型コストを最小限に抑え、生産サイクルを加速しています。デジタルシミュレーションとプロトタイピングツールは、迅速なカスタマイズを可能にし、特定のOEM規格や美的要件を満たすのに役立ちます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の自動車生産の増加

- 軽量部品の需要増加

- 内燃機関(ICE)車の成長

- OEMはコンポーネント統合に注力

- 業界の潜在的リスク・課題

- 統合パワートレインによる設計の複雑さ

- 原材料費の変動

- 市場機会

- プレミアム車および高級車販売の伸び

- 持続可能でリサイクル可能な素材の採用の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業用

- 中作業用

- 重作業用

第6章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

- 電気

- PHEV

- ハイブリッド車

- 燃料電池自動車

第7章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 複合材料

- 金属

- 熱可塑性プラスチック

- その他

第8章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- 美しいエンジンカバー

- 機能的エンジンカバー

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Aisin Corporation

- Continental

- Denso Corporation

- ElringKlinger

- Futaba Industrial

- Hanil E-Hwa Automotive Systems

- Magna International

- MAHLE

- Mann+Hummel

- Montaplast

- Motherson Sumi Systems

- Plastic Omnium

- Polytec Group

- Rochling Group

- Simoldes Plasticos

- SRG Global

- Toyota Boshoku Corporation

- Valeo S.A.

- Woco Industrietechnik

- YAPP Automotive Systems

The Global Automotive Engine Cover Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 3 billion by 2034. This growth is driven by rising global vehicle production and the increasing need for lighter, more efficient automotive components. As industry shifts toward greater performance and fuel economy, engine covers have transformed from basic enclosures into key components that deliver thermal control, sound insulation, and visual cohesion with overall vehicle design. As both internal combustion and hybrid vehicle platforms continue to expand globally, engine covers are being engineered as critical elements in powertrain design across a wide range of models and applications.

The market is also seeing strong traction due to the shift toward advanced materials like composites and thermoplastics. These materials provide the right balance of durability, heat resistance, and weight reduction, enabling manufacturers to meet tightening emission regulations and fuel efficiency standards. Original equipment manufacturers and Tier-1 suppliers are adopting scalable, modular cover designs to support production across compact cars, sport utility vehicles, and light-duty trucks. These platforms help achieve uniform NVH (noise, vibration, and harshness) performance while accelerating time to market and reducing manufacturing complexity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3 Billion |

| CAGR | 6% |

The passenger cars segment held a 76% share in 2024 and is projected to grow at a CAGR of 6.8% through 2034. Engine covers have become essential components in the design of modern passenger vehicles, where tighter engine bays and higher engine outputs demand greater heat and noise management. Their integration into sedans, hatchbacks, and luxury vehicles is helping manufacturers enhance both performance and in-cabin experience. Lightweight thermoplastics and reinforced composites are used to create sleek, aerodynamic, and brand-aligned covers, combining insulation with premium aesthetics.

Gasoline-powered vehicles segment led the market with a 57% share in 2024 and is expected to register a CAGR of 7.1% through 2034. Despite the rise of electric mobility, gasoline engines continue to dominate production volumes in many regions. Engine covers in these vehicles are designed to manage high combustion heat and reduce engine noise while enhancing visual appeal. Manufacturers are turning to composite and polymer blends to offer optimized thermal shielding and lightweight benefits at lower production costs.

Asia Pacific Automotive Engine Cover Market held a 58% share and generated USD 553.1 million in 2024. The country's dominance is supported by its large-scale automotive manufacturing infrastructure, rising consumer demand, and active presence of global OEMs and domestic component manufacturers. Leading companies in China are focusing on producing thermoplastic and composite engine covers in high volume to support diverse vehicle platforms. Government policies encouraging local innovation and greener technologies are driving demand for lightweight, emission-reducing components. Local firms continue expanding through global partnerships to deliver custom-engineered engine cover systems aligned with next-gen mobility trends.

Key companies operating in this industry include Rochling Group, Denso Corporation, MAHLE GmbH, Woco Industrietechnik, Montaplast, Toyota Boshoku Corporation, Aisin Corporation, Valeo S.A., ElringKlinger, and Continental. Market players are leveraging advanced manufacturing technologies to deliver lightweight, durable engine covers that align with global fuel efficiency mandates. Companies are investing in material science innovation, particularly in thermoplastics and composite formulations, to enhance heat resistance while reducing weight. Strategic alliances with automakers help manufacturers align product development with evolving platform needs. Modular and scalable design approaches are increasingly adopted to support a variety of vehicle models, minimizing tooling costs and speeding up production cycles. Digital simulation and prototyping tools allow rapid customization, helping firms meet specific OEM standards and aesthetic requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Material

- 2.2.5 Functionality

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Increasing demand for lightweight components

- 3.2.1.3 Growth in Internal Combustion Engine (ICE) vehicles

- 3.2.1.4 OEM focus on component integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Design complexity with integrated powertrains

- 3.2.2.2 Raw material cost volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in premium and luxury vehicle sales

- 3.2.3.2 Growing adoption of sustainable & recyclable materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.5 PHEV

- 6.6 HEV

- 6.7 FCEV

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Composites

- 7.3 Metals

- 7.4 Thermoplastics

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Functionality, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Aesthetic engine covers

- 8.3 Functional engine covers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aisin Corporation

- 11.2 Continental

- 11.3 Denso Corporation

- 11.4 ElringKlinger

- 11.5 Futaba Industrial

- 11.6 Hanil E-Hwa Automotive Systems

- 11.7 Magna International

- 11.8 MAHLE

- 11.9 Mann+Hummel

- 11.10 Montaplast

- 11.11 Motherson Sumi Systems

- 11.12 Plastic Omnium

- 11.13 Polytec Group

- 11.14 Rochling Group

- 11.15 Simoldes Plasticos

- 11.16 SRG Global

- 11.17 Toyota Boshoku Corporation

- 11.18 Valeo S.A.

- 11.19 Woco Industrietechnik

- 11.20 YAPP Automotive Systems