|

市場調査レポート

商品コード

1693443

油糧種子(播種用種子)-市場シェア分析、産業動向、成長予測(2025~2030年)Oilseed (seed For Sowing) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 油糧種子(播種用種子)-市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 488 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

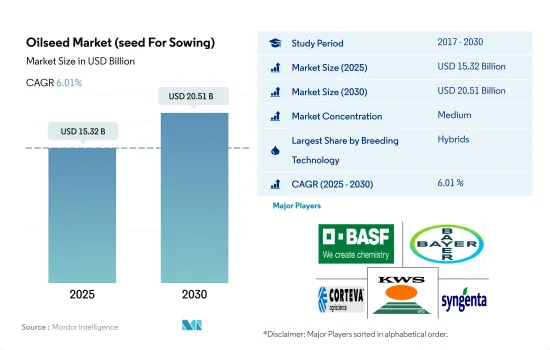

油糧種子市場(播種用種子)の市場規模は2025年に153億2,000万米ドルと推定され、2030年には205億1,000万米ドルに達し、予測期間(2025~2030年)のCAGRは6.01%で成長すると予測されます。

高収量、害虫抵抗性、油質改善形質によりハイブリッドが市場を独占

- ハイブリッド種子は高収量で、異なる地域や気象条件に適応し、害虫抵抗性があり、ハイブリッド種子を使用することで高品質の油作物が生産されるため、世界的にはハイブリッド種子が開放受粉品種よりも高いシェアを占めています。

- ハイブリッドの中では、遺伝子組み換えハイブリッド種子が世界の油糧種子市場を独占し、2022年のシェアは56.2%で、2017~2022年の間に72.5%増加しました。これは、世界中でトランスジェニック種子が受け入れられつつあることに加え、農業従事者が必要な生産量を満たすためにトランスジェニック種子を使用するようになっているため、栽培面積が増加していることによる。

- 世界全体では、2022年にはハイブリッド油糧種子市場の非遺伝子組み換え作物シェアは43.8%となったが、これは欧州で遺伝子組み換え作物が禁止され、非遺伝子組み換え食品を消費することの利点について人々の意識が高まっているためです。

- 2022年には、除草剤耐性ハイブリッド種子市場が世界のトランスジェニック油糧種子市場の76.5%を占め、大豆が47億5,000万米ドルで最大の市場であり、次いでカノーラが8億1,080万米ドルです。油糧種子用のトランスジェニック作物形質のうち、除草剤耐性形質が最も農業従事者に採用されています。雑草は作物生産における主要な問題であり、作物収量を20~25%減少させる原因となっているからです。

- 開放受粉種子品種は雑草に侵されやすく、病気に対する耐性がないため、ハイブリッド種子品種に比べ利用が少ないです。そのため、雑草や害虫による作物の損失を最小限に抑えるため、生産者は耐病性や耐虫性などの特性を持つハイブリッド種子を使用します。このように、より高い収量やペットに対する耐性といった利点が、予測期間中ハイブリッド種子セグメントを牽引します。

北米が世界の油糧種子市場を独占し、大豆、カノーラ、ヒマワリのシェアが高い

- 油糧種子作物は2022年に世界の種子市場の19.6%を占め、これは過去期間中に29.5%増加しました。

- 2022年には、北米が最大の油糧種子生産国であり、52億米ドルを占めました。米国はこの地域で最大の国で、輸出市場からの需要、高収量種子品種の入手可能性、タンパク質が豊富な飼料に対する世界の需要の増加により、2022年には世界の油糧種子市場の30%を占めました。

- 中国は第2位の国で、2022年の世界の油糧種子市場の14.4%を占めました。中国の油糧種子市場は、大豆、キャノーラ、菜種、マスタード作物で占められており、2022年にはそれぞれ市場の74.7%と16.1%を占めます。

- 南米では、ブラジルやアルゼンチンなどの油糧作物の栽培面積の増加や主要生産国により、2022年の世界の油糧種子市場の市場規模は30億4,000万米ドルであり、これらは合わせて世界の油糧種子市場の16.7%を占めています。

- 欧州では、油糧種子は2022年に同地域の種子市場に15億米ドル寄与しました。ひまわりと大豆がこの地域の主要な油糧種子作物であり、2022年にはロシア、ウクライナ、トルコが独占していました。

- アフリカは、2022年の油糧種子市場で4億9,730万米ドルを占めました。南アフリカは、価格の上昇と消費者からの需要、食用油加工工場の拡大により、2022年のアフリカの油糧種子市場の42.2%を占め、大きなシェアを占めました。

- 価格の上昇、消費者からの需要、食用油加工工場の拡大が、この地域の油糧種子市場を牽引しています。したがって、油糧種子市場は予測期間中に成長すると予測されます。

世界の油糧種子市場(播種用種子)の動向

飼料部門からの需要増加、輸出マージンの増加、適正価格により、大豆が油糧種子の栽培面積の大半を占めました。

- 2022年の世界の連作作物作付面積(15億ヘクタール)の18.4%を油糧種子が占めます。油糧種子の栽培面積は大豆が最も多く、菜種とヒマワリがこれに続きます。油糧種子の栽培面積は2017~2022年にかけて9%増加し、2022年には2億8,960万ヘクタールに達するが、これは主に魅力的な価格による油糧種子需要の増加によるものです。世界的には、南米と北米の大豆栽培面積が最大のシェアを占め、2022年には76.4%を占めました。しかし、これらの地域の市場価格の低迷により、大豆の栽培面積は変動しました。

- アジア太平洋では、2017年の大豆栽培面積は1,620万haであったが、2022年には1,920万haに増加しました。栽培面積の増加は、家畜飼料部門からの需要の増加、輸出マージンの増加、国内と国際市場における便利な価格によるものです。予測期間中、作付面積は増加すると予測されます。

- ひまわりは世界的に栽培されている主要な油糧作物のひとつです。世界のヒマワリの作付面積の大部分は欧州が占めています。2017~2022年の間に、ヒマワリの栽培面積は21.5%増加しました。ハンガリー、ブルガリア、チェコ共和国、スロバキアの農業従事者がこの動向を主導したのは、ヒマワリの種子が高値で売れたからです。

- アジア太平洋は、その他の油糧種子の主要地域です。2022年のその他油糧種子の栽培面積は3,270万ヘクタールでした。落花生、ひまし油、亜麻仁の消費需要の増加、国内外市場での手頃な価格が、この地域の栽培面積を押し上げると推定されます。したがって、加工産業からの需要の増加と油糧種子価格の上昇が、予測期間中の種子市場を牽引すると推定されます。

ヒマワリ油の需要増加と様々な産業からの大豆の需要増加が、耐病性、幅広い適応性、高オレイン酸・高リノール酸含有品種の必要性を高めています。

- 大豆種子は、良好な気象条件のもと、米国、ブラジル、中国などで主に栽培されています。気候や土壌条件の変化により、石油加工会社からの大豆の需要が高まり、ミナミ茎カンカー、根こぶ線虫(RKN)、フィトフトラ菌(Phytophthora sojae)を防ぐため、耐病性、耐乾性、高収量、高オレイン酸含量などの形質が人気を集めています。例えば、ランド・オー・レイクスは、エンリストやラウンドアップ・レディのブランドで種子品種を展開しており、改良種子品種に対する需要の高まりに対応しています。コルテバ・アグリスサイエンス(Corteva Agriscience)、KWS SAAT SE & Co.KGaA、Land O'Lakes、Burrus Seeds、Syngenta AGなどの大手企業がこれらの種子形質を提供しています。

- ヒマワリは広く栽培されている主要な油糧作物のひとつです。米国では、ヒマワリ生産量の10%~20%が、殻付きカーネル、ホールシード、ヒマワリ種子を含むナッツと果実のミックスに使用されています。穀粒はグラノーラバーやパンなどの加工食品にも使用されます。改良された形質を持つ種子品種に対する需要は、予測期間中に増加すると予想されます。さらに、オレイン酸やリノール酸を含む高含油量は大きな需要があります。パーム油の使用禁止後、ヒマワリ油の需要が増加しています。このように、高含油量はヒマワリのような作物への需要を増加させ、高収入のリターンを増加させています。Corteva Agriscience、Groupe Limagrain、Syngenta AGといった企業の65A25、P62LL109、LG 50760 CL、Xi Arkoといった製品にはこの形質が含まれています。

- ウイルスに対する高い抵抗性などの先進的形質を持つ新しいハイブリッド種子品種が各社から提供され、加工産業からの需要が高いことから、予測期間中の市場の成長に役立つと予想されます。

油糧種子(播種用種子)産業概要

油糧種子(播種用種子)市場は適度に統合されており、上位5社で54.67%を占めています。この市場の主要企業は、BASF SE、Bayer AG、Corteva Agriscience、KWS SAAT SE & Co. KGaA、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある形質

- ダイズとヒマワリ

- 育種技術

- 列作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- カノーラ、菜種、マスタード

- 大豆

- ヒマワリ

- その他の油糧種子

- 地域

- アフリカ

- 育種技術別

- 作物別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 作物別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 育種技術別

- 作物別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他の欧州

- 中東

- 育種技術別

- 作物別

- 国別

- イラン

- サウジアラビア

- その他の中東

- 北米

- 育種技術別

- 作物別

- 国別

- カナダ

- メキシコ

- 米国

- 北米その他

- 南米

- 育種技術別

- 作物別

- 国別

- アルゼンチン

- ブラジル

- その他の南米地域

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Corteva Agriscience

- Euralis Semences

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Nufarm

- RAGT Group

- Syngenta Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92505

The Oilseed Market (seed For Sowing) size is estimated at 15.32 billion USD in 2025, and is expected to reach 20.51 billion USD by 2030, growing at a CAGR of 6.01% during the forecast period (2025-2030).

Hybrids dominated the market due to the higher yield, pest resistance, and improved oil quality traits

- Globally, hybrids accounted for a higher share than open-pollinated varieties because hybrid seeds are high-yielding, adaptable to different regions and weather conditions, pest resistant, and high-quality oil crops are produced by using hybrid seeds.

- Among the hybrids, transgenic hybrid seeds dominated the global oilseed market, with a share of 56.2% in 2022, which increased by 72.5% during 2017- 2022. This is due to the growing acceptance of transgenic seeds worldwide as well as the increase in areas under cultivation as farmers are increasingly using them to meet the required production.

- Globally, in 2022, the non-transgenic share was 43.8% of the hybrid oilseed market because of the transgenic crops banned in Europe and growing awareness among the people about the benefits of consuming non-GMO food.

- In 2022, the herbicide-tolerant hybrid seed market accounted for 76.5% of the global transgenic oilseed market, with soybean being the largest market, valued at USD 4.75 billion, followed by canola with USD 810.8 million in 2022. Among the transgenic crop traits for oilseeds, the herbicide-tolerant trait is the most adopted by farmers, as weeds are the major problem in crop production and cause a reduction of 20%-25% in crop yield.

- Open-pollinated seed varieties are used less compared to hybrid seed varieties because open-pollinated seed varieties are not resistant to diseases and can be attacked easily by weeds. Thus, to minimize crop loss due to weeds and insects, growers use hybrid seed traits that have characteristics such as disease tolerance and insect resistance. Thus, benefits such as higher yield and resistance to pets drive the hybrid seed segment during the forecast period.

North America dominated the global oilseed market, with soybean, canola, and sunflower having higher shares

- Oilseed crops contributed 19.6% of the global seed market in 2022, which was an increase of 29.5% during the historical period.

- In 2022, North America was the largest producer of oilseeds and accounted for USD 5.2 billion. The United States was the largest country in the region, which accounted for 30% of the global oilseed market in 2022 because of the demand from export markets, the availability of high-yield seed varieties, and an increase in global demand for protein-rich feeds.

- China was the second largest country, which accounted for 14.4% of the global oilseed market in 2022. The Chinese oilseeds market is dominated by soybean, canola, rapeseed, and mustard crops, which accounted for 74.7% and 16.1% of the market in 2022, respectively.

- South America had a market of USD 3.04 billion in the global oilseed market in 2022 due to an increase in the cultivation area and leading producers of oilseed crops, such as Brazil and Argentina, which together accounted for 16.7% of the global oilseed market.

- In Europe, oil seeds contributed USD 1.5 billion to the region's seed market in 2022. Sunflower and soybean are the major oilseed crops in the region, which were dominated by Russia, Ukraine, and Turkey in 2022.

- Africa accounted for USD 497.3 million in the oilseed market in 2022. South Africa occupied a major share, which accounted for 42.2% of the African oilseed market in 2022 due to the increase in the prices and demand from consumers and the expansion of edible oil processing plants.

- An increase in the prices, demand from consumers, and the expansion of edible oil processing plants are driving the oilseed market in the region. Thus, the oilseed market is estimated to grow in the forecast period.

Global Oilseed Market (seed For Sowing) Trends

Soybean dominated the area under oilseeds due to the increased demand from the feed sector, increase in export margins, and reasonable prices

- Oilseeds accounted for 18.4% of global row crop acreage (1.5 billion hectares) in 2022. Soybeans accounted for most oilseed acreage, followed by rapeseed and sunflower. The area under cultivation for oilseeds increased by 9% between 2017 and 2022 and reached 289.6 million hectares in 2022, which is mainly due to increased demand for oilseeds with attractive prices. Globally, South America and North America had the largest share of soybean cultivation acreage, which accounted for 76.4% in 2022. However, the acreage of the soybean fluctuated due to poor market prices in these regions.

- In Asia-Pacific, the area under soybean cultivation was 16.2 million hectares in 2017, which increased to 19.2 million ha in 2022. The increase in the area was due to the increased demand from the livestock feed sector, an increase in export margins, and convenient prices in the domestic and international markets. The acreage is estimated to increase during the forecast period.

- Sunflowers are one of the major oilseed crops cultivated globally. Europe accounted for a large portion of the acreage in global sunflowers. Between 2017 and 2022, the area under cultivation of sunflowers increased by 21.5%. Farmers in Hungary, Bulgaria, the Czech Republic, and Slovakia led this trend because sunflower seeds were selling for high prices.

- Asia-Pacific is the major region in the other oilseed segment. The area under other oilseeds cultivation was 32.7 million hectares in 2022. The increased demand for groundnuts, castor, linseed consumption, and affordable prices on both domestic and foreign markets are estimated to drive the acreage in the region. Thus, increased demand from processing industries and higher prices for oilseeds are estimated to drive the seeds market during the forecast period.

The increasing demand for sunflower oil and the higher demand for soybean from various industries drive the need for disease-resistant, wider adaptability, and high oleic and linoleic content varieties

- Soybean seed is majorly cultivated in countries such as the United States, Brazil, and China due to favorable weather conditions. Traits such as disease resistance, drought tolerance, high yielding, and high oleic content have been gaining popularity due to changes in the climate and soil conditions with high demand for soybean from oil processing companies and preventing southern-stem canker, Root-Knot Nematode (RKN), and Phytophthora sojae. For instance, Land O' Lakes has seed varieties under the brand Enlist and Roundup Ready to meet the increasing demand for improved seed varieties. Other major companies such as Corteva Agriscience, KWS SAAT SE & Co. KGaA, Land O'Lakes, Burrus Seeds, and Syngenta AG offer these seed traits.

- Sunflower is one of the major oilseed crops widely cultivated. In the United States, 10%-20% of sunflower production is used in shelled kernels, whole seeds, and nut and fruit mixes containing sunflower seed. Kernels are also used in processed foods, such as granola bars and bread. The demand for seed varieties with improved traits is expected to increase during the forecast period. Moreover, high oil content with oleic and linoleic has significant demand. The demand for sunflower oil is increasing after a ban on palm oil. Thus, the high oil content increases the demand for crops such as sunflowers and increases the higher income returns. Products such as 65A25, P62LL109, LG 50760 CL, and Xi Arko by companies such as Corteva Agriscience, Groupe Limagrain, and Syngenta AG contain this trait.

- The availability of new hybrid seed varieties by companies with advanced traits, such as higher resistance to viruses and high demand by processing industries, is expected to help in the growth of the market during the forecast period.

Oilseed (seed For Sowing) Industry Overview

The Oilseed Market (seed For Sowing) is moderately consolidated, with the top five companies occupying 54.67%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, KWS SAAT SE & Co. KGaA and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Soybean & Sunflower

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Canola, Rapeseed & Mustard

- 5.2.2 Soybean

- 5.2.3 Sunflower

- 5.2.4 Other Oilseeds

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Breeding Technology

- 5.3.1.2 By Crop

- 5.3.1.3 By Country

- 5.3.1.3.1 Egypt

- 5.3.1.3.2 Ethiopia

- 5.3.1.3.3 Ghana

- 5.3.1.3.4 Kenya

- 5.3.1.3.5 Nigeria

- 5.3.1.3.6 South Africa

- 5.3.1.3.7 Tanzania

- 5.3.1.3.8 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Breeding Technology

- 5.3.2.2 By Crop

- 5.3.2.3 By Country

- 5.3.2.3.1 Australia

- 5.3.2.3.2 Bangladesh

- 5.3.2.3.3 China

- 5.3.2.3.4 India

- 5.3.2.3.5 Indonesia

- 5.3.2.3.6 Japan

- 5.3.2.3.7 Myanmar

- 5.3.2.3.8 Pakistan

- 5.3.2.3.9 Philippines

- 5.3.2.3.10 Thailand

- 5.3.2.3.11 Vietnam

- 5.3.2.3.12 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Breeding Technology

- 5.3.3.2 By Crop

- 5.3.3.3 By Country

- 5.3.3.3.1 France

- 5.3.3.3.2 Germany

- 5.3.3.3.3 Italy

- 5.3.3.3.4 Netherlands

- 5.3.3.3.5 Poland

- 5.3.3.3.6 Romania

- 5.3.3.3.7 Russia

- 5.3.3.3.8 Spain

- 5.3.3.3.9 Turkey

- 5.3.3.3.10 Ukraine

- 5.3.3.3.11 United Kingdom

- 5.3.3.3.12 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Breeding Technology

- 5.3.4.2 By Crop

- 5.3.4.3 By Country

- 5.3.4.3.1 Iran

- 5.3.4.3.2 Saudi Arabia

- 5.3.4.3.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Breeding Technology

- 5.3.5.2 By Crop

- 5.3.5.3 By Country

- 5.3.5.3.1 Canada

- 5.3.5.3.2 Mexico

- 5.3.5.3.3 United States

- 5.3.5.3.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Breeding Technology

- 5.3.6.2 By Crop

- 5.3.6.3 By Country

- 5.3.6.3.1 Argentina

- 5.3.6.3.2 Brazil

- 5.3.6.3.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Euralis Semences

- 6.4.6 Groupe Limagrain

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Nufarm

- 6.4.9 RAGT Group

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms