|

市場調査レポート

商品コード

1689945

3Dプリンティング用フィラメント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)3D Printing Filament - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 3Dプリンティング用フィラメント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

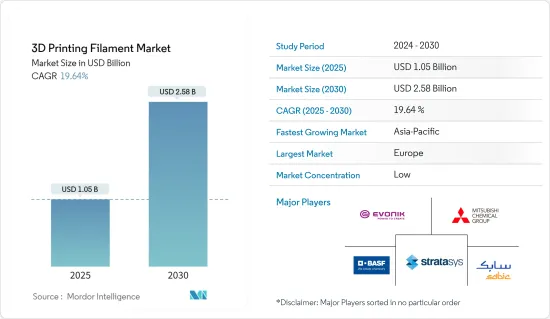

3Dプリンティング用フィラメント市場規模は、2025年に10億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは19.64%で、2030年には25億8,000万米ドルに達すると予測されます。

COVID-19の発生は、世界各地での操業停止、製造活動やサプライチェーンの混乱、生産停止を引き起こし、これらすべてが2020年の市場にマイナスの影響を与えました。しかし、2021~2022年には状況が改善し始め、予測期間中、市場は前年比で成長すると見込まれます。

主なハイライト

- 製造用途における3Dプリンティング用フィラメントの利用拡大が、3Dプリンティングに伴うマスカスタマイゼーションとともに、予測期間中の市場成長を牽引するとみられます。

- 逆に、3Dプリンティングに必要な設備投資額が高いことが、市場の成長を阻害する可能性があります。

- 医療業界における3Dプリンティングの技術革新と3Dプリンティング材料の進歩は、今後研究される市場の成長機会として機能する可能性があります。

- 予測期間中、欧州が最大の市場シェアで市場を独占すると予想されます。

3Dプリンティング用フィラメント市場動向

医療・歯科セグメントからの需要増加が市場成長を促進する可能性

- 医療・歯科産業は、3Dプリンティング用フィラメントを使用する主要産業です。3Dプリンティング用フィラメントの用途全体の約30~35%に寄与しています。

- さまざまなフィラメントを使用する3Dプリンティング技術により、医療・歯科業界の用途として、組織やオルガノイド、手術器具、患者固有の手術モデル、カスタムメイドの補綴物の作成が可能になりました。これらの3Dプリントされた物体は、業界の進歩と開発に大きく貢献しています。

- 3Dプリンティングによって製造される医療機器には、整形外科や頭蓋のインプラント、手術器具、クラウンなどの歯科修復物、外付け補綴物などがあります。

- 2023年3月、Invibioは医療機器の溶融フィラメント積層造形用に特別に設計されたフィラメントを追加することで、インプラントグレードのPEEK-OPTIMAポリマーの選択肢を広げました。

- 2022年8月、3Dセラミックプリンティング企業であるLithozは、製品の受注増加により上半期が同社史上最も好調であったと報告しました。同社は様々な医療、歯科、産業用途向けに幅広いセラミック3Dプリンターを提供しています。

- 上記のような要因から、この分野は予測期間中に急速に成長すると見られています。

欧州が市場を独占

- ドイツはGDPで欧州最大の経済国です。ドイツ、英国、フランスは、世界的に最も急速に経済が発展している国のひとつです。

- 2023年10月現在、欧州の国内総生産(GDP)の平均約11%がヘルスケアに費やされており、国民1人当たりの医療技術への支出は約312ユーロ(337米ドル)です。

- MedTech Europeによると、欧州には33,000社を超える医療技術企業が存在します。そのほとんどはドイツにあり、イタリア、英国、フランス、スイスがこれに続きます。中小企業(SME)が医療技術産業の約95%を占めています。

- ドイツの航空宇宙産業には、全国に2,300社以上の企業があり、中でも北ドイツに企業が集中しています。バイエルン州、ブレーメン州、バーデン=ヴュルテンベルク州、メクレンブルク=フォアポンメルン州を中心に、航空機の内装部品や素材の生産拠点が多いです。

- 国際貿易省によると、英国のエレクトロニクス産業は毎年160億ポンド(約195億3,000万米ドル)の地元経済に貢献しています。同国は現在、欧州で利用可能なエレクトロニクス設計産業の40%のシェアを占めています。同産業における現在の専門知識は、集積回路(IC)、RFID、オプトエレクトロニクス、電子部品に集中しています。

- フランスは、Airbus、Safran、Embraer、Daher-Socataといったメーカーの主要製造拠点であるため、航空機の製造・組立業務が最近増加しています。

- さらに、Air &Cosmos-Internationalによると、フランスは最新の軍事計画法(LPM)に基づき、2024年から2030年の間に4,130億ユーロ(4,471億3,000万米ドル)を国防費に費やすと予想されています。これは、将来的に同国の3Dプリンティング用フィラメント消費を大幅に押し上げる可能性があります。

- 上記の要因はすべて、この地域における3D印刷用フィラメントの需要を押し上げると予想されます。

3Dプリンティング用フィラメント産業の概要

3Dプリンティング用フィラメント市場は非常に細分化されており、少数の大手企業がかなりの部分を占めています。同市場で事業を展開している主要企業(順不同)には、Stratasys Ltd、SABIC、BASF SE、Evonik Industries AG、三菱化学などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 製造用途での利用拡大

- 3Dプリンティングによるマスカスタマイゼーション

- 抑制要因

- 3Dプリンティングプロセスにおける高い設備投資要件

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- 金属

- チタン

- ステンレス

- その他の金属

- プラスチック

- ポリエチレンテレフタレート(PET)

- ポリ乳酸(PLA)

- アクリロニトリル・ブタジエン・スチレン(ABS)

- ナイロン

- その他のプラスチック

- セラミックス

- その他のタイプ

- 金属

- 用途

- 航空宇宙・防衛

- 自動車

- 医療・歯科

- エレクトロニクス

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- ベトナム

- インドネシア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- ノルディック

- トルコ

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ナイジェリア

- カタール

- エジプト

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Covestro Ag

- DOW

- DSM

- Evonik Industries Ag

- Keene Village Plastics

- Mitsubishi Chemical Corporation

- SABIC

- Solvay

- Shenzhen Esun Industrial Co. Ltd

- Stratasys

第7章 市場機会と今後の動向

- 医療業界における3Dプリンティングイノベーション

- 3Dプリンティング材料の進歩

The 3D Printing Filament Market size is estimated at USD 1.05 billion in 2025, and is expected to reach USD 2.58 billion by 2030, at a CAGR of 19.64% during the forecast period (2025-2030).

The COVID-19 outbreak caused nationwide lockdowns across the world, disruption in manufacturing activities and supply chains, and production halts, all of which had a negative impact on the market in 2020. However, conditions began to improve in 2021-2022, and the market is expected to grow year-on-year during the forecast period.

Key Highlights

- The growing usage of 3D printing filaments in manufacturing applications, along with mass customization associated with 3D printing, is expected to drive the market growth during the forecast period.

- Conversely, high capital investment requirements in 3D printing may hinder the market's growth.

- 3D printing innovation in the medical industry and advancements in 3D printing materials may act as growth opportunities for the market studied in the future.

- Europe is expected to dominate the market with the largest market share during the forecast period.

3D Printing Filament Market Trends

Increased Demand from the Medical and Dental Segment May Facilitate Market Growth

- The medical and dental industry is the leading industry that uses 3D printing filaments. It contributes to around 30-35% of the total applications of 3D printing filaments.

- 3D printing technology using different filaments allowed the creation of tissues and organoids, surgical tools, patient-specific surgical models, and custom-made prosthetics as applications in the medical and dental industry. These 3D-printed objects significantly contribute to the advancement and development of the industry.

- Medical devices produced by 3D printing include orthopedic and cranial implants, surgical instruments, dental restorations such as crowns, and external prosthetics.

- In March 2023, Invibio broadened its selection of implantable-grade PEEK-OPTIMA polymers by adding a filament specifically designed for fused filament additive manufacturing of medical devices.

- In August 2022, Lithoz, a 3D ceramic printing company, reported the first half of the year as the most successful in its history due to the increased order of its products. The company offers a wide range of ceramic 3D printers for various medical, dental, and industrial applications.

- Owing to all the above-mentioned factors, this segment is expected to grow rapidly in the market studied over the forecast period.

Europe to Dominate the Market

- Germany is the largest economy in Europe in terms of GDP. Germany, the United Kingdom, and France are among the fastest-emerging economies globally.

- As of October 2023, an average of approximately 11% of Europe's gross domestic product (GDP) was spent on healthcare, and expenditure on medical technology per capita was around EUR 312 (USD 337).

- According to MedTech Europe, over 33,000 medical technology companies are present in Europe. Most of them are located in Germany, followed by Italy, the United Kingdom, France, and Switzerland. Small and medium-sized companies (SMEs) make up around 95% of the medical technology industry.

- The German aerospace industry includes more than 2,300 firms located across the country, with Northern Germany recording the highest concentration of firms. The country hosts many production bases for aircraft interior components and materials, largely in Bavaria, Bremen, Baden-Wurttemberg, and Mecklenburg-Vorpommern.

- According to the Department for International Trade, the electronics industry in the United Kingdom contributes GBP 16 billion (~USD 19.53 billion) each year to the local economy. The country currently holds 40% of the share in the available electronics design industry in Europe. Current expertise within the industry is focused on integrated circuits (ICs), RFIDs, optoelectronics, and electronic components.

- France has been witnessing an increase in aircraft manufacturing and assembly operations in recent times as it is a major manufacturing base for manufacturers such as Airbus, Safran, Embraer, and Daher-Socata.

- Moreover, according to Air & Cosmos-International, France is expected to spend EUR 413 billion (USD 447.13 billion) on defense between 2024 and 2030 under its latest military programming law (LPM). This can substantially boost the country's consumption of 3D printing filament in the future.

- All the factors mentioned above are expected to boost the demand for 3D printing filament in the region.

3D Printing Filament Industry Overview

The 3D printing filament market is highly fragmented, with a few major players dominating a significant portion. Some of the major companies (not in any particular order) operating in the market include Stratasys Ltd, SABIC, BASF SE, Evonik Industries AG, and Mitsubishi Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Manufacturing Applications

- 4.1.2 Mass Customization Associated with 3D Printing

- 4.2 Restraints

- 4.2.1 High Capital Investment Requirement in 3D Printing Process

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Metals

- 5.1.1.1 Titanium

- 5.1.1.2 Stainless Steel

- 5.1.1.3 Other Metals

- 5.1.2 Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polylactic Acid (PLA)

- 5.1.2.3 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.2.4 Nylon

- 5.1.2.5 Other Plastics

- 5.1.3 Ceramics

- 5.1.4 Other Types

- 5.1.1 Metals

- 5.2 Application

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Medical and Dental

- 5.2.4 Electronics

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Vietnam

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Covestro Ag

- 6.4.3 DOW

- 6.4.4 DSM

- 6.4.5 Evonik Industries Ag

- 6.4.6 Keene Village Plastics

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 SABIC

- 6.4.9 Solvay

- 6.4.10 Shenzhen Esun Industrial Co. Ltd

- 6.4.11 Stratasys

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 3D Printing Innovation in the Medical Industry

- 7.2 Advancements in 3D Printing Materials