|

市場調査レポート

商品コード

1689797

医療用カートの市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Medical Carts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療用カートの市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

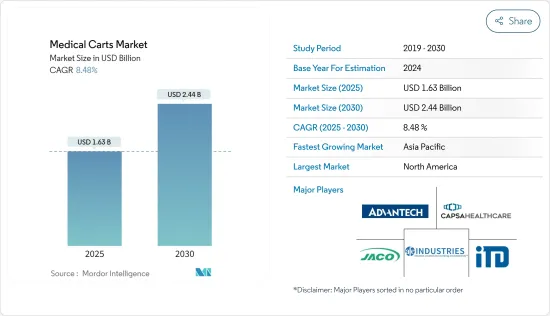

医療用カートの市場規模は2025年に16億3,000万米ドルと推定され、市場推定・予測期間(2025~2030年)のCAGRは8.48%で、2030年には24億4,000万米ドルに達すると予測されます。

医療用カートは、さまざまな医療用品、付属品、医療機器を病院や臨床現場の各部門に運搬・供給するために使用されます。あらゆる医療必需品を運搬するための医療用カートの採用が増加していることや、医療インフラの進歩といった要因が、医療現場における医療用カートの採用を後押しすると予測されています。

加えて、スポーツ関連/筋骨格系損傷の発生率の上昇や慢性疾患の有病率の増加が、患者に医薬品やその他の必要物資を供給するための医療用カートの採用を促進すると予測されています。これも予測期間中に市場成長を加速させると予想される要因の一つです。

慢性疾患の負担増は、患者管理のための医療用カート使用の増加に寄与する最も重要な要因の一つです。例えば、Cancer Australiaの2024年2月更新データによると、腎臓がんと診断された患者数は2022年の4,552人から2023年には4,600人に増加しています。腎臓がんはオーストラリアで7番目に多く診断されるがんで、65人に1人がかかると推定されています。このように、がんの負担増は日常的な治療による入院を助長し、医療用カートの導入に拍車をかけていると推定されます。このように、がんの負担は加速しており、予測期間中の市場成長を促進すると考えられます。

心臓病の有病率の上昇は市場の成長を促進すると予想されます。例えば、英国心臓財団が2023年4月に発表したデータによると、英国では約760万人が心臓疾患や循環器疾患を抱えて生活しています。このような慢性疾患の負担の増大は、医療用品、医薬品、その他の資材を運ぶための医療用カートの需要を促進すると予想されます。このように、慢性疾患の負担増は予測期間中の市場成長を促進すると予想されます。

スポーツに関連した怪我の負担増は、予測期間中の市場拡大をさらに促進すると予測されています。例えば、ジョンズ・ホプキンス大学の2024年1月の最新情報によると、年間約3,000万人の幼児が何らかの組織型スポーツに参加しており、毎年350万人以上の怪我を引き起こしています。このように、スポーツや筋骨格系の怪我の増加により、入院件数が増加し、予測期間中に医療用カートの採用に拍車がかかると予想されます。

緊急事態や緊急入院の増加により、治療に必要な医療用品や付属品を正確に運ぶための医療用カートの需要が高まると予想されます。例えば、NHSの2023年11月のデータによると、救急外来受診者数は2022年の218万8,028人から2023年には221万9,618人に増加しました。このように、救急外来受診者の増加は、予測期間中の市場の成長を押し上げると予測されています。

一方、中低所得国の医療インフラが貧弱であることや、先進的な医療製品の普及が遅れていることが、予測期間中の市場成長を妨げると予測されます。

医療用カートの市場動向

救急カートセグメントは予測期間中に大きな成長を記録する見込み

救急カートセグメントは予測期間中に大きな市場シェアを占めると予測されます。これは、複数の救急治療室が存在し、救急治療室でこれらのカートが使用されていることに起因しています。これらのカートには、虚血性脳卒中や大量出血を伴う重傷などの緊急事態に対応する医療機器、消耗品、薬剤が搭載されています。

したがって、医療緊急事態や交通事故の増加は、予測期間中にセグメントの成長を加速させると予測されています。例えば、英国政府の2024年2月更新データによると、同国では2023年に約2万7,796人が交通事故で重傷を負りました。同じ情報源によると、10万4,014人が軽傷を負りました。このように、交通事故が多発することで、入院患者数が増加し、救急治療室での救急カートの需要が高まる可能性が高いです。

アマロ法律事務所が2023年3月に更新したデータによると、交通事故は米国における緊急事態の主要原因であり、少なくとも全米で年間730万件の自動車事故が発生していると推定されています。この情報源はまた、米国では毎日推定1万9,937件の自動車事故が発生しているとも述べています。このように、交通事故が多発することで医療上の緊急事態が発生し、患者管理のために救急部で救急医療カートの需要が高まっています。

このセグメントは、外傷性脳卒中などのさまざまな医療緊急事態における救急医療カートとトロリーの採用増加から恩恵を受けると予測されています。例えば、Academic Emergency Medicine誌が2023年4月に発表した記事によると、救急医療用カートは外傷や火傷などの緊急事態において、医療用付属品や消耗品に素早くアクセスするために多く採用されています。したがって、救急医療カートのこのような用途は、予測期間中にセグメントの成長を促進すると予測されています。

北米が予測期間中に大きな市場シェアを占める見込み

北米は予測期間を通じて大きな市場シェアを占めると予測されます。公的・私的医療支出の増加、病院数の増加、手術件数の増加などがその要因です。同地域における疾病や傷害の有病率の増加が市場の成長に拍車をかけると予想されます。

同地域における慢性疾患の負担増は、予測期間中に医療用カートの需要を促進すると予測されています。例えば、2023年3月のアルツハイマー病協会の報告書によると、アルツハイマー病と認知症は米国における主要な神経疾患の1つであり、2023年には65歳以上の米国人推定670万人がアルツハイマー病と認知症を患っています。同地域では慢性疾患の負担が増加しているため、入院患者の増加が予想され、予測期間中に医療用カートの需要に拍車がかかるとみられています。

また、北米における救急外来受診の増加も市場の成長に拍車をかけると予想されます。例えば、米国疾病予防管理センター(CDC)の2023年11月のデータによると、米国では約1億3,980万人が救急外来を受診しており、患者100人当たりの受診件数は42.7件となっています。したがって、この地域における救急外来受診者数の増加は、医療用品の流れを合理化するための医療用カートの採用に拍車をかけると予想されます。

北米には幅広い製品を提供する市場参入企業が多数存在します。そのため、同地域には多数の企業が存在し、各企業が戦略的な取り組みをいくつか行っていることから、予測期間中に市場の拡大が加速すると予想されます。例えば、2022年7月、Holo Industries LLCは、医療用カート、患者モニター、その他の製品向けに、表面接触やタッチポイントを実質的に排除することで患者や病院スタッフを保護し、HAIのトランスミッションを低減する、変革的なホログラフィックインサートのHoloMed製品ラインを発売しました。したがって、このような革新的な製品の発売は、予測期間中の地域別市場の成長を促進すると予測されます。

このように、慢性疾患の負担の増加、救急外来受診の増加、市場参入企業によるいくつかの戦略的イニシアティブといった上述の要因は、予測期間にわたって地域市場の成長を後押しすると予想されます。

医療用カート産業概要

医療用カートの市場競争は中程度で、複数の大手企業が参入しています。これらの企業は、戦略的提携を確立し、市場で事業展開している他の企業と協力しています。したがって、市場参入企業によるこのような戦略的イニシアチブは、予測期間中の市場成長を促進すると予測されます。市場で事業展開している主要企業には、Advantech、AFC Industries Inc.、Capsa Healthcare、Jaco Inc.、ITD GmbH、Jaco Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 金額ベースの患者ケアを重視した医療インフラへの投資の増加

- 高齢者の増加と相まって、筋骨格系損傷やその他の慢性疾患などの緊急症例の増加

- 医療用カートに関連する技術の進歩に伴う、重要な外科手術における医療用カートの需要の増加

- 市場抑制要因

- 熟練医療専門家の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- カートタイプ別

- 麻酔カート

- 救急カート

- 処置用カート

- その他のカートタイプ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Advantech Co. Ltd

- AFC Industries Inc.

- Capsa Healthcare

- ITD GmbH

- The Harloff Company

- Joson-care Enterprise Co. Ltd

- Jaco Inc.

- Bergmann Group

- Midmark Corporation

- Ergotron Inc.

- MPE Inc

第7章 市場機会と今後の動向

The Medical Carts Market size is estimated at USD 1.63 billion in 2025, and is expected to reach USD 2.44 billion by 2030, at a CAGR of 8.48% during the forecast period (2025-2030).

Medical carts are used to carry and supply various medical supplies, accessories, and healthcare equipment to every department of a hospital or clinical setting. Factors such as the increasing adoption of medical carts to carry all medical essentials and advancements in healthcare infrastructure are projected to boost the adoption of medical carts in healthcare settings.

In addition, the rising incidence of sports-associated/musculoskeletal injuries and the growing prevalence of chronic diseases are projected to bolster the adoption of medical carts to supply medicines and other necessary supplies to patients. This is another factor expected to accelerate market growth over the forecast period.

The higher burden of chronic diseases is one of the most important factors contributing to the increasing use of medical carts for patient management. For instance, according to the February 2024 updated data of Cancer Australia, the number of kidney cancer cases diagnosed increased from 4,552 in 2022 to 4,600 in 2023. Kidney cancer is the seventh most commonly diagnosed cancer in Australia, and it is estimated that one in 65 people will be diagnosed with the condition. Thus, the higher burden of cancer is estimated to foster hospitalizations due to routine medical treatments, fuelling the adoption of medical carts. Thus, the accelerating burden of cancer is likely to fuel market growth over the forecast period.

The rising prevalence of heart diseases is expected to drive the market's growth. For instance, according to the data released by the British Heart Foundation in April 2023, around 7.6 million people were living with a heart or circulatory disease in the United Kingdom. The escalating burden of such chronic conditions is expected to propel the demand for medical carts to carry medical supplies, medications, and other materials. Thus, the higher burden of chronic diseases is expected to foster market growth over the forecast period.

The increasing burden of sports-related injuries is further projected to augment market expansion over the forecast period. For instance, according to the January 2024 update from Johns Hopkins University, around 30 million children participated in some kind of organized sports annually, which caused more than 3.5 million injuries each year. Thus, the increasing incidence of sports and musculoskeletal injuries is expected to increase the number of hospitalizations, fueling the adoption of medical carts over the forecast period.

The increasing number of emergencies and emergency hospitalizations is expected to foster demand for medical carts to deliver medical supplies and accessories required for treatment accurately. For instance, according to November 2023 data from NHS, emergency department admissions rose from 2,188,028 people in 2022 to 2,219,618 in 2023. Thus, the increase in emergency department visits is projected to boost the growth of the market during the forecast period.

On the other hand, poor healthcare infrastructure in low and middle-income countries and the slow uptake of advanced healthcare products are projected to hamper market growth over the forecast period.

Medical Carts Market Trends

The Emergency Carts Segment is Expected to Record Significant Growth Over the Forecast Period

The emergency carts segment is expected to account for a significant market share over the forecast period. This can be attributed to the presence of several emergency care units and the use of these carts in emergency rooms. These carts are equipped with medical devices, supplies, or drugs for emergencies such as ischemic stroke and severe injuries with profuse bleeding.

Thus, the increasing number of medical emergencies and road accidents are projected to accelerate segmental growth over the forecast period. For instance, according to the February 2024 updated data from the UK government, around 27,796 people were severely injured in road accidents in the country in 2023. As per the same source, 104,014 people were slightly injured. Thus, the high instances of road accidents are likely to foster demand for emergency carts in emergency rooms due to higher hospitalizations.

According to the data updated by the Amaro Law Firm in March 2023, car accidents were a leading cause of emergencies in the United States, and at least 7.3 million motor vehicle accidents were estimated to have occurred annually across the country. The source also stated that an estimated 19,937 car crashes occurred every day in the United States. Thus, the significant number of road accidents is likely to create medical emergencies, fuelling the demand for emergency medical carts in emergency departments for patient management.

The segment is projected to benefit from the increased adoption of emergency medical carts and trollies in different medical emergencies like trauma stroke. For instance, according to an article published by the Academic Emergency Medicine journal in April 2023, emergency medical carts are highly employed in emergencies like trauma and burns to quickly access medical accessories and supplies. Thus, such applications of emergency medical carts are projected to boost the growth of the segment over the forecast period.

North America is Expected to Hold A Significant Market Share Over the Forecast Period

North America is expected to hold a significant share of the market throughout the forecast period. Increasing public and private healthcare expenditures, the growing number of hospitals, and an increase in surgery volumes are factors that can be attributed to this. The market's growth is expected to be fueled by the increase in the prevalence of diseases and injuries in the region.

The growing burden of chronic diseases in the region is projected to facilitate the demand for medical carts over the forecast period. For instance, as per the Alzheimer's Association's report from March 2023, Alzheimer's disease and dementia were among the major neurological disorders in the United States, and an estimated 6.7 million Americans aged 65 and older were living with Alzheimer's and dementia in 2023. The growing burden of chronic diseases in the region is expected to increase hospital admissions, thereby fueling the demand for medical carts over the forecast period.

The market's growth is also expected to be fueled by the increasing emergency department visits in North America. For instance, according to November 2023 data from the Centers for Disease Control and Prevention (CDC), around 139.8 million people visited emergency departments in the United States, with 42.7 visits per 100 patients. Thus, the increase in the number of emergency department visits in the region is expected to spur the adoption of medical carts to streamline the flow of healthcare supplies.

North America has a large number of market players offering a wide range of products. Thus, the presence of a large number of companies in the region and several strategic initiatives undertaken by them are anticipated to accelerate market expansion over the forecast period. For instance, in July 2022, Holo Industries LLC launched a transformative HoloMed line of holographic inserts for medical carts, patient monitors, and other products that protect patients and hospital staff by virtually eliminating surface contact and touchpoints, thereby reducing the transmission of HAIs. Thus, such innovative product launches are projected to foster regional market growth over the forecast period.

Thus, the above-mentioned factors, such as the higher burden of chronic diseases, increasing emergency department visits, and several strategic initiatives undertaken by the market players, are expected to boost regional market growth over the forecast period.

Medical Carts Industry Overview

The medical carts market is moderately competitive and consists of several major players. They are engaged in establishing a strategic alliance and collaborating with other companies operating in the market. Thus, such strategic initiatives undertaken by market participants are projected to foster market growth over the forecast period. Some of the key players operating in the market include Advantech Co. Ltd, AFC Industries Inc., Capsa Healthcare, Jaco Inc., ITD GmbH, and Jaco Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Investments in Healthcare Infrastructure with Enhanced Focus on Value-based Patient Care

- 4.2.2 Growing Incidences of Emergency Cases, such as Musculoskeletal Injuries and Other Chronic Conditions Coupled with Rising Geriatric Population

- 4.2.3 Increased Demand for Medical Carts in Critical Surgical Procedures along with Technological Advancements associated with Medical Carts

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Healthcare Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD)

- 5.1 By Cart Type

- 5.1.1 Anesthesia Carts

- 5.1.2 Emergency Carts

- 5.1.3 Procedure Carts

- 5.1.4 Other Cart Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Advantech Co. Ltd

- 6.1.2 AFC Industries Inc.

- 6.1.3 Capsa Healthcare

- 6.1.4 ITD GmbH

- 6.1.5 The Harloff Company

- 6.1.6 Joson-care Enterprise Co. Ltd

- 6.1.7 Jaco Inc.

- 6.1.8 Bergmann Group

- 6.1.9 Midmark Corporation

- 6.1.10 Ergotron Inc.

- 6.1.11 MPE Inc