|

市場調査レポート

商品コード

1852134

オーガニックミート:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Organic Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オーガニックミート:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月11日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

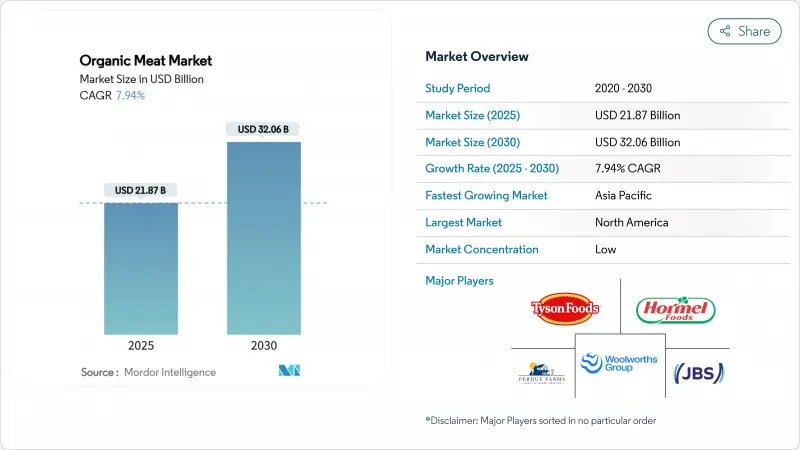

オーガニックミート市場は、2025年に218億7,000万米ドルに達し、2030年には320億6,000万米ドルに成長し、予測期間中のCAGRは7.94%と力強い伸びを記録すると予測されています。

この成長の原動力となっているのは、健康意識の高まり、都市部の高所得者層の拡大、有機認証基準の厳格化です。これらの要因は、消費者を、よりクリーンな成分プロファイルを提供し、検証可能な動物福祉慣行を遵守するプレミアム・プロテイン・オプションへと押しやっています。大手加工業者によるブロックチェーンパイロットのような、テクノロジーを駆使したトレーサビリティ・ソリューションの採用は、断片化されつつも非常にダイナミックな市場において、ブランドが価格プレミアムを維持することを可能にしています。さらに、需要が供給を上回り続けている北米とアジア太平洋では、投資家が生産能力拡大プロジェクトに積極的に資金を供給しています。欧州連合(EU)では、より多くの農地を有機農業に転換するよう生産者に奨励する政策措置がとられており、市場の成長をさらに後押ししています。

世界のオーガニックミート市場の動向と洞察

健康効果がオーガニックミート製品に対する消費者の嗜好を高める

消費者の健康志向が高まる中、オーガニックミートは、合成ホルモン、抗生物質、残留化学物質を含まないことが認められ、好まれるタンパク源としての地位を確固たるものにしています。オーガニック・トレード・アソシエーションは、米国のオーガニック農家が、抗生物質や合成成長ホルモンを使用せずに家畜を飼育し、100%オーガニックの飼料を供給し、ケージフリーの清潔な生活環境を確保するなど、厳格な基準を遵守していることを強調しています。こうした慣行は、動物福祉を重視するだけでなく、食品生産における透明性と持続可能性に対する需要の高まりにも合致しています。特にミレニアル世代とZ世代の消費者は、より健康的で倫理的に調達された製品にプレミアム価格を支払う意欲を示しており、この需要を牽引しています。オーガニックミートの魅力は、その消費と心血管系疾患や特定のがんなどの慢性疾患のリスク低減とを結びつける科学的研究によってさらに強化されています。このエビデンスは消費者の信頼を強め、健康志向のバイヤーがプレミアム価格戦略を検証しながら市場成長を推進するという自己強化サイクルを生み出します。

環境の持続可能性が有機畜産への需要を高める

環境への配慮は、ニッチな関心事から購買意思決定の重要な原動力へと変化しています。オーガニックミートの生産は、従来の方法に比べて持続可能性において明確な利点を提供します。オーガニック・センターによると、オーガニックミートの農法は、有害な合成農薬の使用を排除し、多様な生息地を育成することで、生物多様性を積極的にサポートしています。有機農業の重要な要素である管理放牧は、土壌の質を高め、合成肥料への依存を減らし、長期的な農業の持続可能性に貢献します。EUの有機農業行動計画は、2030年までに農地の25%を有機農業に転換することを目標としており、有機農業の環境面でのメリットに対する政策レベルの強い支持を反映しています。このような規制の後押しにより、市場拡大に有利な条件が整うことが期待されます。さらに、企業の持続可能性へのコミットメントが需要を牽引しており、外食事業者や小売業者は、進化する消費者の期待に沿いつつ、環境・社会・ガバナンス(ESG)目標を達成することをますます優先するようになっています。気候変動に敏感な消費者にとって、オーガニックミートの購入は単なる食生活の選択ではなく、環境保護活動の一形態として捉えられています。

オーガニックミートの高コストが、さまざまな所得レベルの消費者のアクセスを制限しています。

オーガニック・オプションの小売価格は従来の代替品よりもかなり高いため、価格への感応度がオーガニックミートの採用における最も大きな障壁となっています。この価格格差は、さまざまな所得層への市場浸透を制限しています。経済的圧力、特にインフレの時期は、この問題をさらに悪化させる。消費者は必要な支出を優先することが多く、有機製品を好むにもかかわらず、安価なタンパク源を選ぶ人が多いです。米国農務省の「オーガニック状況報告書2025」は、競争の激化と再生可能農業などの代替ラベルの台頭により、オーガニック製品の価格プレミアムが低下していることを強調しています。この動向は、生産者がより多くの消費者が利用しやすいように利幅を圧縮する必要があることを示唆しています。生産面では、高いコスト構造がさらなる課題となっています。有機飼料のプレミアムや認証プロセスに関する経費は、生産者が収益性を損なうことなく価格を引き下げる能力を制限しています。このような構造的なコスト制約が、オーガニックミートの大量市場導入の実現に大きな障害となっており、オーガニックミート市場における値ごろ感と収益性のバランスをとるための戦略的介入の必要性が浮き彫りになっています。

セグメント分析

2024年の市場シェアは家禽類が48.66%を占めトップであり、手頃な価格の有機タンパク質への消費者のシフトを裏付けています。この動向は、小売店での安定供給を保証する確立されたサプライ・チェーンによって支えられています。技術の進歩と規制の更新が有機鶏肉生産を後押ししています。特に、米国農務省(USDA)の有機家畜・家禽基準(Organic Livestock and Poultry Standards)の改訂では、動物福祉の向上を求める消費者の要望を反映し、スペースと環境の充実が重視されるようになりました。牛肉がプレミアム戦略によって市場で際立った存在感を示す一方、豚肉は急成長する市場で文化的な食生活のハードルと格闘しています。しかし、豚肉の優位性は、他とは一線を画す加工技術革新にあります。

ラムやマトンといったセグメントは上昇基調にあり、2030年までのCAGR予測は12.39%を誇る。この急増は、急成長する中東や南アジア市場の文化的嗜好によるところが大きく、そこではオーガニック認証がプレミアムを生みます。都市化が進み可処分所得が増加するにつれて、特に羊肉が文化的に崇拝されている地域では、高級蛋白質への嗜好も高まっています。このセグメントは、限られた供給課題と、有機生産者と有利な世界市場を結ぶ強固な輸出ネットワークにより、競争優位性を享受しています。一方、ジビエや特殊タンパク質など、その他の有機食肉はニッチな分野を開拓しています。職人的なブランディングと消費者への直接販売を活用し、従来の小売のハードルを回避しています。有機飼料生産と牧草地管理の進歩により、生産コストが削減され、利益率が向上しています。

2024年の市場シェアは生鮮・チルド製品が61.72%を占め、市場を独占しています。これは、優れた品質と料理の柔軟性を求める消費者の嗜好が、プレミアム価格戦略を正当化するためです。この優位性は、特にパンデミックによるライフスタイルの変化を受け、体験型ショッピングと家庭での食事作りが人気を集めている、進化する小売動向と一致しています。消費者は、家庭で調理するための高品質の食材をますます求めるようになり、新鮮な商品への需要が強まっています。小売店との提携はこの傾向をさらに浮き彫りにしており、ベルデ・ファームズは、ターゲット、パブリックス、アルバートソンズといった大手スーパーマーケット・チェーンで新鮮な有機牛肉の提供を大幅に拡大し、プレミアム・フレッシュ・ポジショニング戦略によって顕著な流通拡大を達成しています。生鮮品は、輸送コストを削減し、製品の完全性を維持するのに役立つ、より短いサプライチェーンの恩恵を受け、冷凍代替品と比較して競争力のある価格設定を可能にしています。

冷凍オーガニックミート製品は力強い成長を遂げており、2030年までのCAGRは10.37%と予測されています。この成長の原動力となっているのは、利便性に対する需要の高まりと、保存期間を延長しながら栄養価を保持する技術の進歩です。冷凍製品はまた、生鮮製品が直面する流通の制約を克服して、地理的な市場拡大を容易にします。これは、国内市場への参入を目指す小規模有機生産者にとって特に有利です。さらに、冷凍有機食肉は、一般的に生鮮代替品よりもプレミアムが低いため、有機のメリットをより手頃な価格帯で提供することで、コスト意識の高い消費者にアピールすることができます。真空シールやガス置換包装などの先進パッケージング技術は、冷凍製品の品質を向上させ、冷凍焼けを最小限に抑え、長期間保存してもオーガニックの完全性を保持するため、消費者の信頼を高め、市場の普及を促進しています。

地域分析

2024年には、北米が39.23%の市場シェアを占め、その原動力となっているのは、確立されたオーガニック・インフラと、米国農務省の全米オーガニック・プログラムの発足以来強化されてきた進化する規制の枠組みです。この地域の競争優位性は、包括的な認証制度と最近の規制の進展に根ざしています。全米有機連合が強調しているように、米国農務省は全米有機プログラムへの資金を大幅に増やし、2024年1月発効の新しい有機家畜・家禽基準を導入しました。カナダはこの成長において極めて重要な役割を果たしており、畜産事業を拡大し、NAFTA条項を活用して国境を越えた流通を強化しています。この地域の消費者直販チャネルは、パンデミックによる急成長を超えて成熟し、eコマース・プラットフォームによって、農村部の生産者がサプライ・チェーン全体を通じてオーガニックの完全性を維持しながら、都市部のプレミアム市場にアクセスできるようになっています。

アジア太平洋は、2030年までのCAGRが10.14%と予測され、最も急成長している地域と位置づけられています。この成長の原動力となっているのは、急速な経済発展と都市部における高級蛋白消費への文化的シフトです。インドの有機食品部門は計り知れない潜在力を示しており、ムンバイ、プネー、デリーなどの大都市が有機食品の検索でリードしている一方、大都市以外の地域でも採用が加速しています。地域全体の鶏肉インフラへの投資が、南アジアと東南アジアにおけるオーガニックミートの統合を促進しています。この成長は、食料安全保障を強化するための現地生産への注目によって支えられています。加えて、食を薬として重視する文化的な食の嗜好や伝統的な薬草信仰は、オーガニックミートのポジショニングと自然に合致しており、多様な所得層でプレミアム価格の受容を可能にしています。

欧州は、EUの野心的なオーガニック行動計画に支えられ、市場で強い存在感を維持しています。同計画は、2030年までに農地に占める有機農業の割合を現在の8.5%から25%に引き上げることを目標としています。2025年1月に新たなEU有機規制が導入され、より厳格な遵守要件が課されるため、小規模生産者にとっては課題となるが、市場全体の整合性と消費者の信頼は高まる。この地域は、加盟国間で調和された認証基準の恩恵を受けており、国境を越えた貿易を促進し、生産と流通における規模の経済を生み出しています。一方、中東とアフリカは、ラムやマトンに対する文化的嗜好に後押しされ、成長地域として台頭しつつあります。一方、南米は確立された畜産能力と拡大する輸出ネットワークを活用し、先進国市場におけるトレーサブルな有機タンパク質への需要の高まりに応えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 健康上のメリットが消費者のオーガニックミートの選好を促進する

- 環境の持続可能性が有機畜産への需要を高める

- 動物愛護意識が市場成長を加速

- 製品のプレミアム・ポジショニングが品質重視の消費者を引きつける

- 規制の枠組みと政府の支援が生産を後押し

- ライフスタイルの変化と都市化がプレミアム・オーガニック製品の需要を押し上げる

- 市場抑制要因

- さまざまな所得レベルの消費者へのアクセシビリティを制限する高いコスト

- 保存料がないため製品の賞味期限が短く、成長の妨げになる

- 標準化された表示の欠如が消費者を混乱させ、信頼を妨げる

- サプライチェーンの未整備が遅れの原因

- 消費者行動分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- 家禽類

- 牛肉

- 豚肉

- ラム&マトン

- その他

- 製品形態別

- 生鮮/チルド

- 冷凍

- パッケージングタイプ別

- 真空パック

- トレイ

- カートン

- その他

- 流通チャネル別

- 貿易外

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- 専門店

- オンライン小売店

- その他流通チャネル

- オントレード

- 貿易外

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング

- 企業プロファイル

- Tyson Foods Inc.

- JBS S.A.

- Woolworths Group Limited

- Perdue Farms Inc.

- Meyer Natural Foods LLC

- Scandi standard AB

- Foster Poultry Farms, LLC

- Verde Farms, LLC

- Eversfield Organic Ltd

- Les Viandes du Breton Inc.

- Cleaver's Organic(Hewitt Foods)

- Farmer Focus

- Hormel Foods Corporation(Applegate)

- OBE Organics Australia

- Swillington Organic Farm

- Valens Farms

- Corpp Cooperative

- Bell & Evans

- Waitrose Limited

- Yorkshire Valley Farms