|

市場調査レポート

商品コード

1910676

電力変圧器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Power Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電力変圧器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 310 Pages

納期: 2~3営業日

|

概要

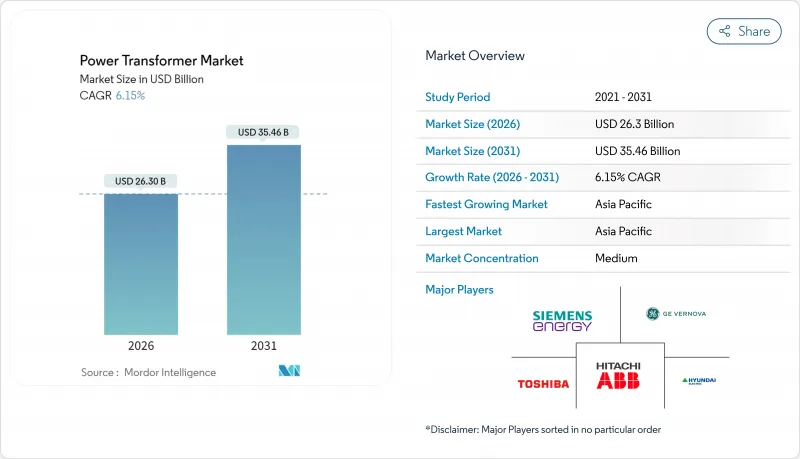

電力変圧器市場は、2025年に247億8,000万米ドルと評価され、2026年の263億米ドルから2031年までに354億6,000万米ドルに達すると予測されております。

予測期間(2026-2031年)におけるCAGRは6.15%と見込まれております。

この成長勢いは、産業の電化プログラム、大規模な再生可能エネルギー接続、送電網強化の義務化が相まって、高電圧機器への記録的な資本流入をもたらしていることを反映しています。調達部門が供給安定性を追求する中、工場の受注残が2年以上に及ぶ状況により、納期の確実性が最優先の購入基準となりました。電力会社、独立系発電事業者、ハイパースケールデータセンター運営者は、鋼材発注よりかなり前に変圧器容量を事実上前売りする複数年の購入契約を締結しています。アジア太平洋地域は供給と需要の両面で中核を担っていますが、輸送時間の短縮と地政学的リスクの軽減を目的としたニアショアリングにより、北米と欧州でも並行して容量拡充が進められています。これらの要因が相まって、電力変圧器市場全体において製品仕様、サービスモデル、利益機会が再定義されつつあります。

世界の電力変圧器市場の動向と洞察

再生可能エネルギー発電の統合化進展

風力・太陽光発電の拡大に伴い、数分以内に最大80%の電圧変動を調整可能で、双方向電力フローに対応できる変圧器が求められています。国際エネルギー機関(IEA)は、2030年までに再生可能エネルギー容量が2倍以上に増加すると予測しており、これは負荷時タップ切換装置(OLTC)と動的高調波フィルタを備えた数千台の系統連系昇圧ユニットの導入を意味します。電力会社が軽量化と瞬時の電圧サポートを要求する中、ソリッドステートおよびハイブリッドトポロジーは試作段階から限定量産へと進展しています。これに対しメーカーは、セグメント単位で出荷され、現場で組み立てられ、新たな設計サイクルを必要とせずに132kVから400kVの定格範囲で柔軟に対応可能なモジュラーコアで対応しています。発注時点で組み込まれたデジタルツインモデルにより、資産所有者は単一の積層板を切断する前に熱的余裕をシミュレートでき、次世代アーキテクチャ導入に伴うリスクを低減できます。

老朽化する電力網と大規模送配電設備の更新需要

北米の大規模電力変圧器の70%以上が25年以上稼働しており、現在の銘板容量を超える交換需要が急増しています。欧州でも戦後設備の同時期寿命到達により同様の危機に直面。国立再生可能エネルギー研究所は、深度電化シナリオ下で2050年までに配電レベル需要が260%増加すると予測しています。電力会社は溶解ガス分析、音響エミッションセンサー、赤外線スキャンを用いて変圧器群の優先順位付けを行っていますが、過負荷状態に数十年間さらされた結果、多くのユニットが絶縁破壊に陥っています。改修専門業者は現在、現場でタンクのコア交換を実施しており、完全交換と比較してリードタイムを3分の2短縮し、カーボンフットプリントを削減しています。それでもなお、投資の先送りは故障リスクを高め、新規電力変圧器市場に対する基本需要をさらに強化する結果となっています。

高額な設備投資と複数年に及ぶ回収期間

2020年以降、変圧器価格は最大80%上昇し、資本予算を膨らませるとともに単純償却期間を5年以上も延長させています。電力会社はリース・リースバックやエネルギー・アズ・ア・サービス契約による資金調達を組み合わせて対抗し、資産を貸借対照表から除外しています。連邦政府へのロビー活動では、電力変圧器市場のコスト急騰を緩和するため、国内コア鋼材供給支援として12億米ドルの支援を求めています。一方、ガスインオイルセンサーやブッシング取り付け型温度プローブを活用した状態監視型保守は寿命を延長しますが、運用上の複雑さを増し、サイバーセキュリティリスクも高めます。

セグメント分析

100MVAを超える大型変圧器は、電力会社が複数の空気絶縁変電所を400kVおよび765kV回廊を軸に設計された単一の高容量変電所へ統合する動きに伴い、2031年までに7.28%という最速のCAGRで受注が見込まれます。この定格区分に属する電力変圧器市場規模は、2020年代末までに124億7,000万米ドルを超え、総価値の3分の1以上を占める見込みです。電力会社はMVA当たりの効率向上と保守スケジュールの簡素化を目的に大型ユニットを導入し、初期投資を長期的な損失削減効果と交換しています。

中型変圧器は、標準化、物流の容易さ、工場サイクルの短縮により、2025年時点で51.87%のシェアを維持しました。しかしながら、大型コア対応のための工場設備更新に伴い、中型クラスのリードタイムも延長しており、生産量に一部制約が生じています。10MVA未満の小型定格は、特にアジア太平洋地域の農村電化計画において、変電所の設置面積を制限する人口密度や地形条件から、配電網において依然として不可欠です。全体として、電力変圧器市場は汎用性の高い中型ユニットと、超大容量ソリューションへの流れとのバランスを保ち続けております。

2025年には油冷式設計が80.68%のシェアで市場を独占しました。鉱物油はキロワット当たりの放熱コスト面で圧倒的な優位性を持ち、比類のない熱的余裕を提供するためです。しかしながら、人口密集都市部における厳格な防火規制により、空冷式は年間7.35%の成長率で拡大しており、これは変圧器市場全体の伸び率を2ポイント上回っています。合成エステル油は中間的な選択肢として、引火点を300℃まで高め、生分解性の目標を達成していますが、価格プレミアムが普及の妨げとなっています。

空冷式モデルは強制通風プレナムとフィン付き放熱器構造を採用し、油冷式との損失差を最小限に抑えます。非可燃性冷却剤により保険会社が保険料割引を適用するデータセンターのユーティリティインターフェースベイで主流です。サプライヤーは現在、現場交換用にスライド式モジュラーファントレイを備えたプラグアンドプレイ空冷器を提供しており、数分のダウンタイムしか許容されないハイパースケールのメンテナンス期間に対応しています。

地域別分析

アジア太平洋地域は2025年に41.88%のシェアで電力変圧器市場を牽引し、2031年までCAGR6.73%で拡大が見込まれます。中国の垂直統合型サプライチェーンはコスト曲線を圧縮し輸出量を支えますが、一部の海外バイヤーは地政学的リスク分散のためインドやベトナムの工場へ調達先を多様化させています。インドの生産連動型奨励制度(PLI)は新たなコイル巻線・タンク製造工場の設立を支援し、農村電化目標は送電網・配電ユニット双方の受注を加速させています。日本と韓国はプレミアム設計、5脚コア、アモルファス材料に注力し、これらは資金力のある北米の公益事業者に輸出されています。

北米は成熟市場ながら供給制約があり、連邦税額控除や資金プールが国内建設に伴う資本コスト増を相殺しています。プレインズ&イースタン高圧直流送電線のようなプロジェクトでは、現在国内3工場のみが製造可能なコンバータ変圧器が求められており、このギャップは海外OEMとの合弁事業で解消されつつあります。カナダは米国との水力連系系統を近代化し、メキシコはニアショア電子工場を誘致することで産業用変電所の需要を拡大しています。

欧州では再生可能エネルギーの普及と老朽化設備の代替が両立されています。ドイツのエネルギー転換政策により、沿岸風力拠点へ400kV送電網の経路変更が進み、フランスでは原子力発電所の改修に電力を供給する225kV送電回廊のアップグレードが実施されています。スカンジナビア諸国では、フロン規制の厳格化によりSF6フリーのガス絶縁技術が急速に普及しており、先行OEMメーカーは地球温暖化係数(GWP)中立の代替技術に精通することが求められています。東欧諸国では、EUの結束基金を活用してソ連時代の油紙絶縁変圧器を排除する送電網更新が進み、電力変圧器市場に新たな需要が生まれています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 再生可能エネルギー発電の統合化が進展しております

- 老朽化した電力網と大規模な送配電設備の更新計画

- より厳格な送電網信頼性基準及び高電圧直流送電(HVDC)相互接続

- 鉄道及び電気バスネットワークの電化

- データセンター向け超高圧柔軟コアLPTの需要

- グリーン水素電解装置?昇圧変圧器の必要性

- 市場抑制要因

- 高額な設備投資と複数年にわたる回収期間

- 方向性電磁鋼板及び銅の価格変動性

- 地政学的な要因による重要変圧器部品の貿易制限

- 経験豊富な変圧器設計技術者の世界の不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 電力定格別(MVA)

- 大型(100 MVA以上)

- 中規模(10~100 MVA)

- 小規模(10MVA以下)

- 冷却方式別

- 空冷式

- 油冷式

- フェーズ別

- 単相

- 三相

- エンドユーザー別

- 電力事業

- 産業

- 商業用

- 住宅用

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、パートナーシップ、PPA)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Hitachi Energy(ABB)

- Siemens Energy AG

- GE Vernova

- Toshiba Energy Systems & Solutions

- Hyundai Electric & Energy Systems

- Mitsubishi Electric Corporation

- Hyosung Heavy Industries

- Bharat Heavy Electricals Limited

- CG Power & Industrial Solutions

- SPX Transformer Solutions

- TBEA Co. Ltd.

- JiangSu HuaPeng Transformer

- Shandong Taikai Transformer

- Schneider Electric

- Eaton Corporation

- Fuji Electric

- LS Electric

- WEG SA

- Wilson Transformer Company

- Saudi Transformers Co.

- Elsewedy Electric

- Hammond Power Solutions

- TriDelta Meidensha