ボトルウォーター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Bottled Water - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939110

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

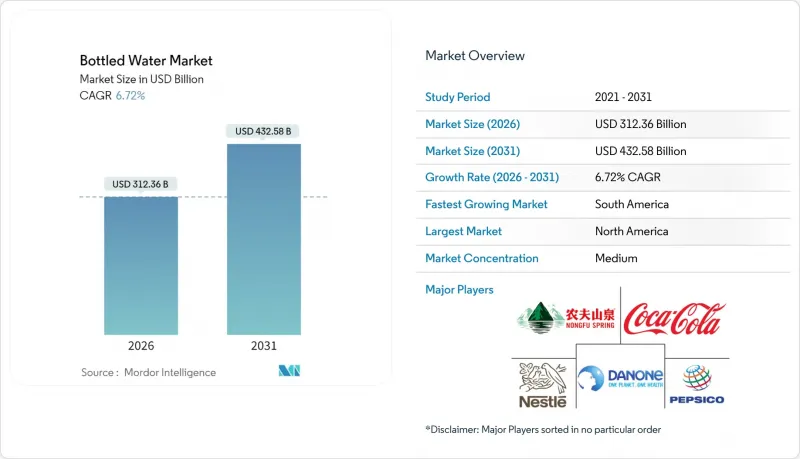

ボトルウォーター市場は、2025年の2,927億米ドルから2026年には3,123億6,000万米ドルへ成長し、2026年から2031年にかけてCAGR6.72%で推移し、2031年までに4,325億8,000万米ドルに達すると予測されております。

規制当局による使い捨てプラスチックの規制強化を受け、業界関係者はプレミアム化戦略に注力し、平均販売価格の引き上げに成功しております。健康増進、水分補給、ブランドストーリーを重視する消費者の増加が、このカテゴリーの価値向上を牽引しております。一方、浄化技術や包装技術の進歩が、規制対応コストの上昇を相殺する一助となっております。ボトルウォーター業界の主要企業は、コスト圧力への対応と業界内での評判維持を目的に、合併の加速、提携関係の構築、再生素材への投資を進めております。しかしながら、地域密着型の競合他社も、職人的なブランディングや戦略的な流通チャネル展開により存在感を示しつつあります。こうした動きを受け、ボトルウォーター市場は単なる利便性から、健康・持続可能性・ブランド体験を包括的に重視する方向へと移行しつつあります。

世界のボトルウォーター市場の動向と洞察

プレミアム化と「許容される贅沢」のポジショニング

消費者の心理変化により、ミネラルウォーターの購入は単なる必需品から、健康志向のライフスタイルに基づく選択へと変容しました。この進化はブランドに価格決定力をもたらし、従来の商品市場の常識に課題があります。2023年には、農夫山泉がこの動向を体現し、426億7,000万元(58億米ドル)の収益を上げました。愛国主義的な反発に直面しながらも、同社は天然湧水製品においてプレミアムポジショニング戦略を活用しました。「許容される贅沢」という概念が重要な役割を果たしており、消費者は高級水の購入を単なる贅沢品ではなく健康への投資と捉えることができます。この認識の変化により、ブランドは大衆市場向け製品よりも200~400%高い価格設定が可能となり、かつ販売数量の持続的な成長も享受しています。電解質強化水やビタミン強化水といったカテゴリーはこの潮流に乗り、プレミアム価格を正当化する明確な健康効果を提示しています。このアプローチは特に先進国市場で共感を呼び、可処分所得の高さが健康意識への選択的支出をボトルウォーター市場で実現可能にしています。

利便性と環境配慮を実現する革新的な包装ソリューション

規制圧力と環境問題への消費者意識の高まりを受け、包装業界は革新に注力しています。技術的ブレークスルーは企業が持続可能性基準を満たすだけでなく、市場での差別化機会も提供しています。顕著な進展として、2024年11月にサントリーが使用済み食用油由来のバイオパラキシレンを用いた世界初の商用PETボトルを発表しました。サントリーグループが強調するように、この取り組みは年間4,500万本の飲料用PETボトル生産を目標としており、従来の石油由来素材と比較してCO2排出量の削減を約束しています。一方、欧州連合(EU)はプラスチック使用規制を強化しています。使い捨てプラスチック指令では、2025年までにPETボトルの再生材含有率を25%、2030年までに30%に引き上げることを義務付けています。こうした規制により、バリューチェーン全体の企業がイノベーション投資を加速させており、欧州委員会も同様の見解を示しています。技術面では、KHSフレッシュセーフ社のPETプラスマックスガラスコーティングが注目を集めています。これはハイブリッドソリューションを提供し、PETの再生可能性を維持しつつ、ガラス並みの優れたバリア特性を実現します。韓国では、立法措置が市場を変革中です。2026年までに、ボトルウォーターの外部ラベルが禁止されることになり、この変化がラベルレスボトル技術の採用を促進しています。ドミノ・プリンティング・サイエンシズが指摘するように、この変更により、ボトルウォーター業界では年間2,460万トンのプラスチック廃棄物が削減される可能性があります。

マイクロプラスチックおよびナノプラスチックの健康への懸念

科学の調査により、ボトルウォーターにおけるマイクロプラスチック汚染が広範に存在することが明らかになり、消費者の信頼を損なうとともに規制当局の監視を招き、市場基盤を脅かしています。米国国立衛生研究所(NIH)の調査によれば、ボトルウォーターには1リットルあたり平均24万個のプラスチック粒子が含まれており、その大部分がナノプラスチックであることが示されています。特に、検出された粒子の90%はポリアミドとポリエチレンテレフタレート(PET)と特定されています。2024年8月、FDAはマイクロプラスチックおよびナノプラスチックに関するウェブページを公開し、ボトルウォーターを含む様々な食品への存在を確認しました。しかしながらFDAは、これらの粒子と健康リスクを結びつける決定的な証拠が不足している点を指摘。これにより規制上の曖昧さが生じ、業界の投資判断に影響を与える可能性があると、食品包装フォーラムが強調しています。主要ブランドは、マイクロプラスチック含有量に関する誤解を招く広告を理由に集団訴訟に直面。裁判所は、健康リスクの立証された証拠ではなく、消費者欺瞞の主張に焦点を当て、これらの訴訟の進行を認めています。国際ボトルウォーター協会(IBWA)は、汚染問題への対応を求める圧力が高まっており、ボトルウォーター業界の基準強化と厳格な検査プロトコルの導入を提唱しています。環境保護団体は消費者啓発キャンペーンを通じて健康影響への懸念を拡大しており、ボトルウォーター市場において、異なる包装材料や高度なろ過システムを採用した高価格帯の代替品への消費者の移行を促す可能性があります。

セグメント分析

2025年時点で、スティルウォーターはボトルウォーター市場の72.88%という圧倒的なシェアを占めており、消費者の根強い嗜好と強固な流通ネットワークが裏付けられています。一方、機能性水およびフレーバーウォーターのセグメントは上昇傾向にあり、2031年までに8.12%のCAGRが見込まれています。この変化は、水分補給の消費パターンにおける顕著な進化を示しています。プレミアムウォーター製品への転換は、基本的な水分補給をウェルネス中心のライフスタイル選択へと昇華させる成功戦略を浮き彫りにしています。天然炭酸水動向とミキサーとしての役割に支えられ、炭酸水は着実な成長を続けています。同時に、機能性ウォーターセグメントは多様化が進み、ビタミン強化タイプ、電解質スポーツタイプ、植物由来フルーツフレーバータイプへと分岐し、それぞれが異なる健康目標に対応しています。

ビタミン強化水はサプリメント市場に参入し、手軽な栄養補給を提供します。これは単なる水分補給以上のものを求める健康志向の消費者に訴求します。電解質を配合しスポーツ向けに販売される水は、拡大するフィットネス文化の波に乗っています。活気あるジム会員数とアウトドア活動が特徴の都市部市場では、こうした専門的な水分補給ソリューションへの顕著な需要が見られます。一方、植物由来成分やフルーツを配合したウォーターは、風味を重視する層のニーズに応えつつ、健康志向のイメージを保つバランスを保っています。ウェルネスコミュニティで懸念される人工添加物を避けている点が特徴です。サプライサイド・飲食品・ジャーナルが指摘する消費者意識調査の知見によれば、機能性ウォーターはプレミアム価格が設定されています。これは主に、具体的な健康効果への認識によるもので、ボトルウォーター業界において従来の商品代替品に対する持続可能な優位性を確立しています。

2025年現在、PETボトルはコスト優位性と確立されたリサイクルインフラにより、ボトルウォーター市場で61.05%のシェアを占めています。一方、ガラス瓶は持続可能性への関心の高まりとプレミアムポジショニングの推進を背景に、8.74%のCAGRで成長を続けています。この包装材の移行は、環境への配慮と製品保護の強化が認識されることで、消費者がプレミアム価格を支払う用意があることを示しています。アルミ缶・ボトルは特に炭酸水や機能性飲料分野でニッチ市場を開拓中です。金属の質感がブランド差別化と店頭での視認性向上に寄与しているためです。ガラス包装は高価格帯ながら完全リサイクル性と化学的不活性性を備え、プラスチック溶出を懸念する健康志向消費者の支持を得ています。

しかしながら、ガラス製品の重量増は輸送コストの障壁となり、流通効率に課題をもたらします。とはいえ、プレミアムブランドは高い利益率と戦略的な市場ポジショニングにより、こうしたコストを巧みに相殺しています。サントリーグループが示すように、バイオベース素材や最先端バリアコーティングといったPETの革新技術は、コスト競争力を損なうことなく持続可能性のギャップ解消を目指しています。EUの再生材含有率義務化(2025年までに25%達成)は、PET技術の進歩を促すだけでなく、欧州委員会も指摘するようにサプライチェーンの再構築を促しています。一方、植物由来プラスチックやハイブリッドソリューションといった代替包装材は、ボトルウォーター市場全体でコストと性能面の課題により商業的成功が妨げられているもの、潜在的なゲームチェンジャーとして台頭しつつあります。

本ボトルウォーターレポートは、製品タイプ(静水、炭酸水、機能性/フレーバーウォーター)、包装材料(PETボトル、ガラス瓶、アルミ缶・アルミボトル、その他)、価格帯(大衆向け、プレミアム/高級)、流通チャネル(オントレード、オフトレード)、地域(北米、欧州、アジア太平洋、南米、中東・アフリカ)別に分析されています。市場予測は金額ベース(米ドル)で提供されます。

地域別分析

2025年、北米は確立されたインフラとプレミアム消費習慣を背景に、ボトルウォーター市場で28.11%という圧倒的なシェアを占めています。同地域の先進的な物流網と広範な再生PET(rPET)回収ネットワークは、機能性水分補給を求める消費者の増加に対応しています。小売業者は、より高価格帯の電解質水、アルカリ性水、フレーバーウォーターの製品ラインに、大きな棚スペースを割り当てています。さらに米国環境保護庁によれば、複数州で導入されたデポジット返還制度によりリサイクル率は70%超に達しています。しかしながら、カリフォルニア州とワシントン州が再生材含有率の規制を強化していることから、懸念が生じています。これらの規制により従来のPET容器のコスト上昇が懸念されるのです。一方、食料品チェーンはオーガニックに焦点を当てたプライベートブランドを展開し競合を激化させており、ボトルウォーター業界の中堅ナショナルブランドに圧力をかけています。

南米は9.88%という最高CAGRを誇り、急成長を遂げています。急速な都市化、インフラ課題、可処分所得の増加がこの急増を後押ししています。ブラジルの大都市では、断続的な水道水の水質問題により、中流家庭が包装水を必需品と見なすようになりました。政府の水道事業公社パートナーシップ計画が長期的な水不足の解決を約束する一方で、当面の信頼性問題が消費者をマルチパック購入へと駆り立てています。チリとコロンビアでは、健康志向のライフスタイルやガラス瓶・再生PET容器を好む観光客の流入により、プレミアム化動向が顕著です。地域生産は分散しているもの、多国籍ボトラーが地元水源の権利獲得を目的に小規模ブランドを買収する動きが見られ、業界再編の兆候が確認されます。

アジア太平洋地域は世界のボトルウォーター消費において主要な役割を担う一方、購買力と規制の厳格さには大きな格差が見られます。中国の都市部消費者は高級ミネラルウォーターに傾倒しています。対照的に、インドのボトルウォーター業界はBIS規格の施行状況にばらつきがあり、技術投資に影響を与えています。インドネシアでは列島国家という特性から流通上の課題が生じ、従来のPET小売に加え、リフィルステーション形式の増加につながっています。中東およびアフリカの一部地域では、高収益が見込める砂漠観光や駐在員向けに深層帯水層からの水源開発が進められています。しかしながら、政治的不安定や物流上の課題が市場成長の持続的拡大を妨げています。こうした地域ごとの特性は、持続的な市場拡大のためには、現地生産の重要性、カスタマイズされた供給戦略、そして積極的な規制対応が不可欠であることを浮き彫りにしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- プレミアム化と「許容される贅沢」のポジショニング

- 利便性と環境影響を考慮した革新的な包装ソリューション

- 新興メガシティにおける移動中の水分補給需要の拡大

- 高度な浄化・ボトリング技術の採用

- 水ストレス地域における深層帯水層からの水資源調達

- 観光・ホスピタリティ業界の拡大

- 市場抑制要因

- マイクロプラスチックおよびナノプラスチックの健康への懸念

- 使い捨てプラスチック規制の勢い

- カーボンフットプリント表示とスコープ3の精査

- 政府による厳格な禁止措置と罰則

- 消費者行動分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- スティルウォーター

- スパークリングウォーター

- 機能性/フレーバーウォーター

- ビタミン強化

- 電解質・スポーツ飲料

- 植物由来/フルーツ風味

- 包装材料別

- ペットボトル

- ガラスボトル

- アルミ缶およびボトル

- その他

- 価格別

- マス

- プレミアム/ラグジュアリー

- 流通チャネル別

- オントレード

- オフトレード

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア/食料品店

- ホーム&オフィススペース

- オンライン小売

- その他の小売店以外での販売チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Nestle SA

- Danone SA

- The Coca-Cola Company

- PepsiCo Inc.

- Nongfu Spring Co. Ltd

- Suntory Holdings Ltd

- BlueTriton Brands Inc.

- Fiji Water Company LLC

- Bisleri International Pvt Ltd

- VOSS of Norway ASA

- Hint Inc

- JUST Goods, Inc.(Just Water)

- Wahaha Group Co. Ltd

- CENTR Brands Corporation(Centr)

- Disruptive Beverages Inc.(Ayala's Herbal Water)

- Keurig Dr. Pepper(Bai, Core Hydration)

- Crag Spring Water

- Callaway Blue Spring Water

- Vitamin Well

- Saratoga Springs Water

第7章 市場機会と将来の動向

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日