|

市場調査レポート

商品コード

1693944

衛星打上げロケット-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Satellite Launch Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 衛星打上げロケット-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 202 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

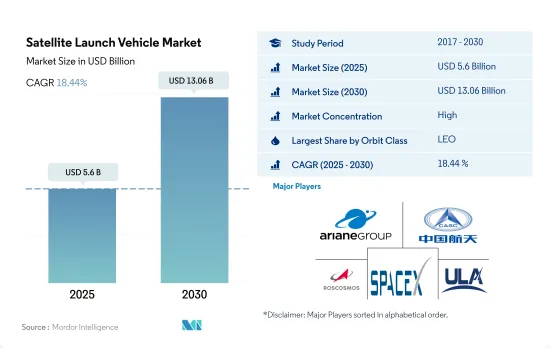

衛星打上げロケット市場規模は、2025年には56億米ドルと推定され、2030年には130億6,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは18.44%で成長する見込みです。

LEO衛星の需要が同セグメントの成長を牽引

- 打ち上げの際、衛星や宇宙船は通常、地球を周回する多くの特別な軌道の1つに配置されます。また、ロケットエンジンによって推進されるロケットを使用して、惑星間の旅に打ち上げることもできます。人工衛星は、その設計や主要目的によって、さまざまな距離で地球を周回します。それぞれの距離には、カバー範囲の拡大やエネルギー効率の低下など、利点と課題があります。地球中軌道(MEO)にある衛星には、特定の地域をモニタリングするために設計された航法衛星や特殊衛星が含まれます。NASAの地球観測システムを含むほとんどの地球科学衛星は、地球低軌道(LEO)にあります。

- これらの軌道で製造・打ち上げられる衛星は、それぞれ用途が異なります。例えば、2017~2022年にかけて、ほぼ4,131機の衛星がLEOに配備され、主に通信と地球観測に重点が置かれています。MEOで打ち上げられた57機の衛星のほとんどは、航法/全地球測位目的で作られました。同様に、GEOに打ち上げられた147機の衛星のほとんどは、通信と地球観測を目的としています。

- LEOは、その近さ、国際宇宙ステーション(ISS)の存在、赤道経路に従わなければならない強制力のなさなど、様々な利点から、最も一般的に使用されている軌道です。この軌道では、衛星は毎秒約7.8kmの速度で移動し、地球を一周するのに約90分かかります。

- 電子情報、地球科学、レーザー画像処理、電子情報、光学画像処理、気象学などのセグメントで衛星の利用が増加していることから、ロケット需要の牽引役となることが予想されます。同市場は2029年には210%の成長が見込まれ、2023年に記録された額を上回ります。

2029年にはアジア太平洋と北米が92%の累積シェアを占めると予想されます。

- 宇宙産業は最近の動向で著しい成長を遂げており、多数の企業がロケットの開発・配備の主要企業として台頭しています。北米は宇宙探査のパイオニアであり、多くの宇宙ミッションがこの地域に端を発しています。SpaceXは現在、Falcon-9、Falcon Heavy、Starshipなどの打ち上げロケットを保有し、同地域における打ち上げサービスの主要プロバイダとなっています。2017~2022年にかけて、スペースXのロケットは約2,744基の衛星を軌道に打ち上げました。

- 欧州では、アリアングループのような企業が、再使用可能な第1段を含むアリアン・ネクスト・ロケットを開発しています。ロシアのロスコスモスもまた、ロケット開発・配備の長い歴史を持つ、この産業における重要な参入企業です。同社はソユーズロケットとプロトンロケットの開発を担当し、さまざまな衛星を宇宙に打ち上げてきました。2017~2022年にかけて、ソユーズロケットは世界の様々な衛星事業者のために約611個の衛星を宇宙に打ち上げました。

- アジア太平洋では、CASCは、世界で最も信頼性の高いロケットの1つとなった長征ロケットシリーズを含む、さまざまなロケットの開発と配備を担当しています。2017~2022年にかけて、CASCの長征ロケットは世界の様々な衛星事業者のために約372基の衛星を宇宙に打ち上げました。一方、JAXAはH-IIAロケットとH-IIBロケットを開発しました。2017~2022年にかけて、JAXAのH-IIAロケットは、世界の様々な衛星事業者のために約25機の衛星を宇宙に打ち上げました。2017~2022年の間に、ISROのロケットは世界の様々な衛星事業者のために約171個の衛星を宇宙に打ち上げました。

世界の衛星打ち上げロケット市場動向

世界の衛星打上げロケット市場における需要の拡大と競合

- 北米は宇宙探査のパイオニアであり、多くの宇宙ミッションがこの地域に端を発しています。SpaceXは北米を代表する航空宇宙企業で、先進的な再使用型ロケットや宇宙船を製造・打ち上げています。現在、Falcon-9、Falcon Heavy、Starshipなどの打ち上げロケットを有し、同地域における打ち上げサービスの主要プロバイダとなっています。2017~2022年にかけて、スペースXのロケットは約2,744基の衛星を軌道に打ち上げました。

- 欧州では、アリアングループなどの企業が、アリアンロケットの再使用可能な第1段を含むアリアン・ネクスト・ロケットを開発しています。ロシアのロスコスモスもまた、ロケット開発・配備の長い歴史を持つ、この市場の重要な参入企業です。同社はソユーズロケットとプロトンロケットの開発を担当し、さまざまな衛星を宇宙に打ち上げてきました。2017~2022年にかけて、ソユーズロケットは世界の様々な衛星事業者のために約611個の衛星を宇宙に打ち上げました。

- アジア太平洋では、CASCは、世界で最も信頼性の高いロケットの1つとなった長征ロケットシリーズを含む、さまざまなロケットの開発と配備を担当しています。2017~2022年にかけて、CASCの長征ロケットは世界の様々な衛星事業者のために約372基の衛星を宇宙に打ち上げました。2017~2022年にかけて、JAXAはH-IIAロケットとH-IIBロケットを使って、世界の様々な衛星事業者のために約25基の衛星を宇宙に打ち上げました。インドの宇宙プログラムも最近の動向で著しい成長を遂げており、ISROは同国のロケット開発で重要な役割を果たしています。2017~2022年にかけて、ISROのロケットは世界のさまざまな衛星事業者のために約171基の衛星を宇宙に打ち上げました。

世界の衛星打上げロケット市場における投資機会

- 北米では、宇宙計画のための世界政府支出が2021年に過去最高の約1,030億米ドルに達しました。この地域は、世界最大の宇宙機関であるNASAが存在する、宇宙イノベーションと研究の震源地です。2022年、米国政府は宇宙プログラムに620億米ドル近くを費やし、世界で最も宇宙開発に資金を投じる国となっています。ロケット開発に割り当てられる資金に関しては、2023年度大統領予算要求概要(2022~2027年度)において、NASAは138億米ドルを受け取る見込みです。

- 2022年11月、ESAは22カ国に2023~2025年にかけて185億ユーロの予算を要求したと発表しました。39億米ドル弱を投じて開発され、当初は2020年7月の打ち上げを予定していたこのプロジェクトは、相次ぐ延期に見舞われています。フランス、ドイツ、イタリアの3カ国政府は、欧州の宇宙への独立系アクセスを確保しつつ、欧州のロケット競合を強化するため、「欧州におけるロケット開発の将来」に関する協定に署名したと発表しました。

- 2023年2月、インド政府は、ISROがさまざまな宇宙関連活動のために20億米ドルを受け取る見込みであると発表しました。主要計画に関する支出では、打ち上げ活動、ロケット、エンジン、衛星などの研究開発に944億1,000万インドルピーが割り当てられています。2021年3月、日本は宇宙関連活動に41億4,000万米ドルを支出する計画を発表しました。2023年3月、韓国は次世代キャリアロケットKSLV-2の開発に約1億1,360万米ドルを使用すると発表しました。

衛星打上げロケット産業概要

衛星打上げロケット市場はかなり統合されており、上位5社で160.48%を占めています。この市場の主要企業は、Ariane Group、China Aerospace Science and Technology Corporation(CASC)、ROSCOSMOS、Space Exploration Technologies Corp.、United Launch Alliance, LLC.です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- ロケットの所有者

- 宇宙開発への支出

- 規制の枠組み

- 世界

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イラン

- 日本

- ニュージーランド

- ロシア

- シンガポール

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 軌道クラス

- GEO

- LEO

- MEO

- ロケット

- 大型

- 小型

- 中型

- 地域

- アジア太平洋

- 国別

- 中国

- インド

- ニュージーランド

- 欧州

- 国別

- ロシア

- 北米

- 国別

- 米国

- その他

- 国別

- イラン

- その他

- アジア太平洋

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ariane Group

- China Aerospace Science and Technology Corporation(CASC)

- Indian Space Research Organisation(ISRO)

- Mitsubishi Heavy Industries

- Northrop Grumman Corporation

- ROSCOSMOS

- Space Exploration Technologies Corp.

- The Boeing Company

- United Launch Alliance, LLC.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Satellite Launch Vehicle Market size is estimated at 5.6 billion USD in 2025, and is expected to reach 13.06 billion USD by 2030, growing at a CAGR of 18.44% during the forecast period (2025-2030).

The demand for LEO satellites is driving the segment's growth

- During the launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth. It can also be launched into an interplanetary journey using a launch vehicle propelled by rocket engines. Satellites orbit the Earth at varying distances depending on their design and primary purpose. Each distance has its own benefits and challenges, including increased coverage and decreased energy efficiency. Satellites in medium Earth orbit (MEO) include navigational and specialized satellites designed to monitor a specific area. Most Earth science satellites, including NASA's Earth Observation System, are in low Earth orbit (LEO).

- Different satellites manufactured and launched in these orbits have different applications. For instance, from 2017 to 2022, almost 4,131 satellites were deployed in LEO, focusing mainly on communication and Earth observation. Most of the 57 satellites launched in MEO were built for navigation/global positioning purposes. Similarly, most of the 147 satellites in GEO were deployed for communication and Earth observation purposes.

- LEO is the most commonly used orbit due to its various advantages, such as close proximity, the presence of the International Space Station (ISS), and no compulsion to follow the equator path. In this orbit, satellites travel at a speed of around 7.8 km per second and take approximately 90 minutes to circle Earth, meaning the ISS travels around Earth about 16 times a day.

- The increasing usage of satellites in areas such as electronic intelligence, Earth science, laser imaging, electronic intelligence, optical imaging, and meteorology is expected to drive the demand for launch vehicles. The market is expected to grow by 210% in 2029, outpacing the amount recorded in 2023.

Asia-Pacific and North America are expected to occupy a major cumulative share of 92% in 2029

- The space industry has seen remarkable growth in recent years, with numerous companies emerging as major players in the development and deployment of launch vehicles. North America has been a pioneer in space exploration, with many space missions having their origins in the region. SpaceX is currently the leading provider of launch services in the region, with its launch vehicles including Falcon-9, Falcon Heavy, and Starship. During 2017-2022 SpaceX's rockets launched approximately 2,744 satellites into orbit.

- In Europe, companies like ArianeGroup are developing the Ariane Next rockets, including a reusable first stage. Russia's Roscosmos is another key player in the industry, with a long history of developing and deploying launch vehicles. The company is responsible for developing the Soyuz and Proton rockets, which have been used to launch a range of satellites into space. During 2017-2022, the Soyuz rocket launched approximately 611 satellites into space for various satellite operators globally.

- In Asia-Pacific, CASC is responsible for developing and deploying a range of launch vehicles, including the Long March series, which has become one of the most reliable launch vehicles in the world. During 2017-2022, CASC's Long March rocket launched approximately 372 satellites into space for various satellite operators globally. JAXA, on the other hand, has developed H-IIA and H-IIB rockets. During 2017-2022, JAXA's H-IIA rockets launched approximately 25 satellites into space for various satellite operators globally. During 2017-2022, ISRO's rockets launched approximately 171 satellites into space for various satellite operators globally.

Global Satellite Launch Vehicle Market Trends

Growing demand and competition in the global satellite launch vehicle market

- North America has been a pioneer in space exploration, with many space missions having their origins in the region. SpaceX is a leading aerospace company in North America that manufactures and launches advanced reusable rockets and spacecraft. It is currently the leading provider of launch services in the region, with its launch vehicles including Falcon-9, Falcon Heavy, and Starship. During 2017-2022, SpaceX's rockets launched approximately 2,744 satellites into orbit.

- In Europe, companies such as ArianeGroup are developing the Ariane Next rockets, which involve a reusable first stage for the Ariane rocket. Russia's Roscosmos is another key player in the market, with a long history of developing and deploying launch vehicles. The company is responsible for the development of the Soyuz and Proton rockets, which have been used to launch a range of satellites into space. During 2017-2022, the Soyuz rocket launched approximately 611 satellites into space for various satellite operators globally.

- In Asia-Pacific, CASC is responsible for developing and deploying a range of launch vehicles, including the Long March series, which has become one of the most reliable launch vehicles in the world. During 2017-2022, CASC's Long March rocket launched approximately 372 satellites into space for various satellite operators globally. During 2017-2022, JAXA launched approximately 25 satellites into space for various satellite operators globally using its H-IIA and H-IIB rockets. India's space program has also seen significant growth in recent years, with the ISRO playing a key role in the development of the country's launch vehicles. During 2017-2022, ISRO's rockets launched approximately 171 satellites into space for various satellite operators globally.

Investment opportunities in the global satellite launch vehicle market

- In North America, global government expenditure for space programs hit a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world. In terms of funds allocated for launch vehicle development, under FY 2023 President's Budget Request Summary from FY 2022-FY 2027, NASA is expected to receive USD 13.8 billion.

- In November 2022, ESA announced that it had asked its 22 nations to back a budget of EUR 18.5 billion for 2023-2025, with Germany, France, and Italy being the major contributors. Developed at a cost of just under USD 3.9 billion and originally set for an inaugural launch in July 2020, the project has been hit by a series of delays. The governments of France, Germany, and Italy announced that they had signed an agreement on "the future of launcher exploitation in Europe" to enhance the competitiveness of European vehicles while ensuring independent European access to space.

- In February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities. Under the Outlay on Major Schemes, INR 9,441 crore has been allocated for launch activity, R&D on rockets, engines, satellites, etc. In March 2021, Japan announced its plan to spend USD 4.14 billion on space-related activities. In March 2023, South Korea announced that approximately USD 113.6 million would be used to develop a next-generation carrier rocket, the KSLV-2.

Satellite Launch Vehicle Industry Overview

The Satellite Launch Vehicle Market is fairly consolidated, with the top five companies occupying 160.48%. The major players in this market are Ariane Group, China Aerospace Science and Technology Corporation (CASC), ROSCOSMOS, Space Exploration Technologies Corp. and United Launch Alliance, LLC. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Owner Of Launch Vehicle

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Global

- 4.4.2 Australia

- 4.4.3 Brazil

- 4.4.4 Canada

- 4.4.5 China

- 4.4.6 France

- 4.4.7 Germany

- 4.4.8 India

- 4.4.9 Iran

- 4.4.10 Japan

- 4.4.11 New Zealand

- 4.4.12 Russia

- 4.4.13 Singapore

- 4.4.14 South Korea

- 4.4.15 United Arab Emirates

- 4.4.16 United Kingdom

- 4.4.17 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Orbit Class

- 5.1.1 GEO

- 5.1.2 LEO

- 5.1.3 MEO

- 5.2 Launch Vehicle Mtow

- 5.2.1 Heavy

- 5.2.2 Light

- 5.2.3 Medium

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 By Country

- 5.3.1.1.1 China

- 5.3.1.1.2 India

- 5.3.1.1.3 New Zealand

- 5.3.2 Europe

- 5.3.2.1 By Country

- 5.3.2.1.1 Russia

- 5.3.3 North America

- 5.3.3.1 By Country

- 5.3.3.1.1 United States

- 5.3.4 Rest of World

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Rest of World

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 China Aerospace Science and Technology Corporation (CASC)

- 6.4.3 Indian Space Research Organisation (ISRO)

- 6.4.4 Mitsubishi Heavy Industries

- 6.4.5 Northrop Grumman Corporation

- 6.4.6 ROSCOSMOS

- 6.4.7 Space Exploration Technologies Corp.

- 6.4.8 The Boeing Company

- 6.4.9 United Launch Alliance, LLC.

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms