|

市場調査レポート

商品コード

1693941

GEO衛星- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)GEO Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| GEO衛星- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 207 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

GEO衛星市場規模は2025年に191億4,000万米ドルと予測され、2030年には226億9,000万米ドルに達し、予測期間(2025~2030年)のCAGRは3.46%で成長すると予測されています。

液体燃料推進は予測期間中に急増する見込み

- 衛星の推進システムは、その速度と方向を変える上で重要な役割を果たします。また、軌道上で宇宙船の位置を調整するためにも使用されます。軌道に乗った後、宇宙船は地球と太陽に対して姿勢を修正するために姿勢制御を必要とします。場合によっては、衛星を軌道から移動させる必要があり、軌道に適応する能力がなければ、衛星は死んだとみなされます。そのため、パワートレインシステムの重要性が市場の成長を促進すると予想されます。燃料タイプは目的に応じて使い分けられます。液体推進剤を使用するロケットエンジンは液体推進剤を使用します。ガス燃料も使用できるが、密度が低く、従来の圧送方法では困難なため、あまり普及していないです。2020年には、パンデミックによって直面した製造・運用上の課題によって影響を受け、市場は44%減少しました。

- それを可能にした液体システムは、高効率で信頼性が高いことが証明されています。これには、ヒドラジンシステム、シングルまたはデュアル推進システム、ハイブリッドシステム、冷風/熱風システム、固体推進剤などがあります。強力な推力や素早い操縦が必要な場合に使用されます。したがって、総推力容量がミッション要件を満たすのに十分であれば、液体システムが宇宙推進技術として選ばれ続けると考えられます。

- 一方、電気推進は、商業通信衛星のステーション保持に一般的に使用されており、その高い比推力により、一部の宇宙探査ミッションの主要推進力となっています。電気推進システムの利用は2023~2029年の間に急増し、市場全体では22%の急増が見込まれます。新たな衛星打ち上げが予測期間中の市場成長を加速すると予想されます。

- 世界のGEO衛星市場は、様々な産業にわたる様々な衛星アプリケーションに牽引され、今後数年間で大きく成長すると予想されます。市場は、北米、欧州、アジア太平洋に関して分析することができ、これらは市場シェアと収益生成の面で主要な地域です。2017~2022年の間に、147機の衛星が製造され、このセグメントの様々なオペレータによってGEOに打ち上げられました。これら147機の衛星のうち、75%近くが通信目的で打ち上げられました。

- 北米は、Boeing、Lockheed Martin、ノースロップ・グラマンなど複数の大手市場参入企業の存在により、世界のGEO衛星市場を独占すると予想されています。同地域では、高速インターネット、ナビゲーションサービス、リモートセンシングアプリケーションの需要が増加しているため、市場成長に拍車がかかると予想されます。2017~2022年にかけて、この地域はGEOに製造・打ち上げられた衛星全体の30%を占めています。

- 欧州では、高速インターネットや通信サービスの需要増加により、GEO衛星市場の大幅な成長が見込まれています。ESAは先進的な衛星技術の開発に多額の投資を行っており、同地域の市場成長をさらに促進すると期待されています。2017~2022年の間に、この地域はGEOに製造・打ち上げられた衛星全体の11%を占めています。

- アジア太平洋では、同地域の政府や民間組織による衛星技術やインフラ開発への投資が増加しており、同市場の成長をさらに押し上げると期待されています。2017~2022年の間に、この地域はGEOに製造され打ち上げられた衛星全体の59%を占めました。

世界のGEO衛星市場動向

人工衛星は、他の機能に加えて、より先進的通信装置、先進的画像処理機能、先進的センサを搭載しており、その質量に寄与している

- GEO(静止地球軌道)衛星の質量は、その特定の設計、目的、統合された技術的進歩によって変化し得る。しかし、特定の動向と一般的な考慮事項が、GEO衛星の質量を長期にわたって形成してきました。長年にわたり、GEO衛星の質量は、主に技術の進歩と衛星ペイロードの複雑化に起因して増加する一般的な傾向がありました。現在、衛星は、より先進的通信機器、高解像度の画像システム、先進的センサを搭載しており、これらは、他の機能の中でも、衛星全体の質量を増加させる一因となっています。

- 高スループット衛星(HTS)は、データ容量の強化と通信速度の高速化を目的として設計されています。これらの衛星は、通信能力を最大化するために、先進的アンテナシステム、複数のスポットビーム、周波数再利用技術を採用しています。HTS衛星は、さらに複雑で大きな通信ペイロードを搭載するため、衛星質量が大きくなる可能性があります。

- GEO衛星は主に通信の中継として機能し、テレビ放送、インターネット接続、通信などのサービスを記載しています。より高い帯域幅とより先進的サービスへの需要が高まるにつれて、通信ペイロードのサイズと容積は増大しています。より大きく強力な通信機器を搭載するため、GEO衛星はより重くなっています。2017~2022年の間に、世界全体で140以上の衛星がGEOで打ち上げられました。軍事衛星の急増は、予測期間においてGEO衛星セグメントを助けると予想されています。

世界市場の成長は、固有の宇宙能力によって支えられると予想される

- 静止軌道は、地球の赤道上空約35,786kmの高度に位置する円軌道です。GEO衛星は、通信、ナビゲーション、モニタリング、リモートセンシング、天気予報、衛星放送、インターネットサービスなど、さまざまな市場アプリケーションとサービスを提供しています。2017~2022年5月までの間に、世界全体で145以上のGEO衛星が打ち上げられました。

- カナダ政府によると、カナダの宇宙産業は同国のGDPに23億米ドルを上乗せし、1万人を雇用しています。政府の報告によると、カナダの宇宙企業の90%は中小企業です。カナダ宇宙庁(CSA)の予算は控えめで、2022~23年の予算支出は3億2,900万米ドルと見積もられています。

- アジア太平洋では現在、中国、インド、日本だけが、衛星、ロケット、宇宙港の製造を含め、すべての通信衛星、地球観測衛星(EO)、航法衛星のための完全な宇宙インフラと技術を持ち、完全なエンドツーエンドの宇宙能力を有しています。この地域の他の国々は、それぞれの宇宙計画を遂行するために国際協力に依存しています。しかし、この地域の多くの国々が最新の機敏な戦略の一環として、固有の宇宙能力を開発しているもの、この動向は今後数年間である程度変化すると予想されます。2022年6月、韓国はヌリ・ロケットを打ち上げて6基の衛星を軌道に投入し、1トンを超えるペイロードの打ち上げに成功した世界で7番目の国となりました。

GEO衛星産業概要

GEO衛星市場はかなり統合されており、上位5社で88.46%を占めています。この市場の主要企業は、Airbus SE、China Aerospace Science and Technology Corporation(CASC)、Lockheed Martin Corporation、Maxar Technologies Inc.、Thalesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の質量

- 宇宙開発への支出

- 規制の枠組み

- 世界

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イラン

- 日本

- ニュージーランド

- ロシア

- シンガポール

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 1,000kg以上

- エンドユーザー

- 商業

- 軍事・政府

- 推進技術

- 電気式

- ガスベース

- 液体燃料

- 地域

- アジア太平洋

- 欧州

- 北米

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- China Aerospace Science and Technology Corporation(CASC)

- Indian Space Research Organisation(ISRO)

- Japan Aerospace Exploration Agency(JAXA)

- Lockheed Martin Corporation

- Maxar Technologies Inc.

- Mitsubishi Heavy Industries

- Northrop Grumman Corporation

- Thales

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

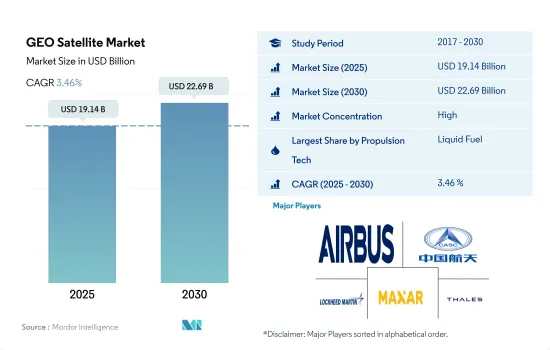

The GEO Satellite Market size is estimated at 19.14 billion USD in 2025, and is expected to reach 22.69 billion USD by 2030, growing at a CAGR of 3.46% during the forecast period (2025-2030).

Liquid fuel propulsion is expected to surge during the forecast period

- A satellite's propulsion system plays a key role in changing its speed and direction. It is also used to adjust the position of the spacecraft in orbit. After entering orbit, the spacecraft requires attitude control to correct its orientation with respect to the Earth and the Sun. In some cases, it is necessary to move the satellite out of orbit, and without the ability to adapt to orbit, the satellite is considered dead. Therefore, the importance of powertrain systems is expected to drive market growth. Different types of fuel are used for different purposes. Liquid propellants use rocket engines that use liquid propellants. Gas fuels can also be used but are less popular due to their low density and difficulty using conventional pumping methods. In 2020, the market was declined by 44%, impacted by the manufacturing and operational challenges faced by the pandemic.

- The liquid system that made it possible has proven to be highly efficient and reliable. These include hydrazine systems, single or dual propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. It is used when strong thrust or quick maneuvering is required. Therefore, liquid systems will continue to be the space propulsion technology of choice if their total thrust capacity is sufficient to meet mission requirements.

- On the other hand, electric propulsion is commonly used to hold stations for commercial communications satellites, and its high specific impulse makes it the primary propulsion for some space exploration missions. The utilization of electric propulsion systems is expected to surge during 2023-2029, and the overall market is expected to surge by 22%. New satellite launches are expected to accelerate market growth during the forecast period.

- The global GEO satellite market is expected to grow significantly in the coming years, driven by various satellite applications across different industries. The market can be analyzed concerning North America, Europe, and Asia-Pacific, which are the major regions in terms of market share and revenue generation. Between 2017 and 2022, 147 satellites were manufactured and launched by various operators in this segment into GEO. Of these 147 satellites, nearly 75% were launched for communication purposes.

- North America is expected to dominate the global GEO satellite market due to the presence of several leading market players, such as Boeing, Lockheed Martin, and Northrop Grumman. The increasing demand for high-speed internet, navigation services, and remote sensing applications in the region is expected to fuel market growth. Between 2017 and 2022, the region accounted for 30% of the total satellites manufactured and launched into GEO.

- In Europe, the GEO satellite market is expected to grow significantly due to the increasing demand for high-speed internet and communication services. The ESA has been investing heavily in the development of advanced satellite technology, which is expected to further drive the growth of the market in the region. During 2017-2022, the region accounted for 11% of the total satellites manufactured and launched into GEO.

- In Asia-Pacific, increasing investments in the development of satellite technology and infrastructure by governments and private organizations in the region are expected to further boost the growth of the market. During 2017-2022, the region accounted for 59% of the total satellites manufactured and launched into GEO.

Global GEO Satellite Market Trends

Satellites are equipped with more sophisticated communication devices, advanced imaging capabilities, and advanced sensors that, in addition to other functions, contribute to their mass

- The mass of GEO (geostationary Earth orbit) satellites can vary depending on their specific design, purpose, and the technological advancements integrated. However, certain trends and general considerations have shaped the mass of GEO satellites over time. Over the years, there has been a general trend of increasing the mass of GEO satellites, mainly due to advances in technology and the increasing complexity of satellite payloads. Satellites now carry more advanced communications equipment, high-resolution imaging systems, and sophisticated sensors that, among other capabilities, contribute to their overall mass.

- High-throughput satellites (HTS) are designed to provide enhanced data capacity and faster communication speeds. These satellites employ advanced antenna systems, multiple spot beams, and frequency reuse techniques to maximize their communication capabilities. The additional complexity and larger communication payloads of HTS can result in higher satellite masses.

- GEO satellites primarily serve as relays for communications, providing services such as television broadcasting, internet connectivity, and telecommunications. The size and volume of the communication payload have increased as the demand for higher bandwidth and more advanced services has increased. To accommodate larger and more powerful communications equipment, GEO satellites have become heavier. During 2017-2022, over 140 satellites were launched in GEO globally. The surge in the number of military satellites is expected to aid the GEO satellite segment in the forecast period.

The growth of the global market is expected to be supported by indigenous space capabilities

- A geostationary orbit is a circular orbit located at an altitude of approximately 35,786 km above the Earth's equator. GEO satellites offer a range of market applications and services such as communications, navigation, surveillance, remote sensing, weather forecasting, satellite broadcasting, and internet services. Between 2017 and May 2022, over 145+ GEO satellites were launched globally.

- The Canadian space industry adds USD 2.3 billion to the country's GDP and employs 10,000 people, according to the government. The government reports that 90% of Canadian space firms are small- and medium-sized businesses. The Canadian Space Agency's (CSA) budget is modest, with its budgetary spending for 2022-23 estimated at USD 329 million.

- In Asia-Pacific, currently, only China, India, and Japan have full end-to-end space capacity and complete space infrastructure and technology for all communication, Earth observation (EO), and navigation satellites, including for the manufacturing of satellites, rockets, and spaceports. Other countries in the region rely on international cooperation to carry out their respective space programs. However, this trend is expected to change to some extent over the coming years, although many countries in the region are developing indigenous space capabilities as part of their latest agile strategies. In June 2022, South Korea launched the Nuri rocket, putting six satellites into orbit, making it the seventh country in the world to successfully launch a payload weighing more than one ton.

GEO Satellite Industry Overview

The GEO Satellite Market is fairly consolidated, with the top five companies occupying 88.46%. The major players in this market are Airbus SE, China Aerospace Science and Technology Corporation (CASC), Lockheed Martin Corporation, Maxar Technologies Inc. and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Global

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 France

- 4.3.7 Germany

- 4.3.8 India

- 4.3.9 Iran

- 4.3.10 Japan

- 4.3.11 New Zealand

- 4.3.12 Russia

- 4.3.13 Singapore

- 4.3.14 South Korea

- 4.3.15 United Arab Emirates

- 4.3.16 United Kingdom

- 4.3.17 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 above 1000kg

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 China Aerospace Science and Technology Corporation (CASC)

- 6.4.3 Indian Space Research Organisation (ISRO)

- 6.4.4 Japan Aerospace Exploration Agency (JAXA)

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 Maxar Technologies Inc.

- 6.4.7 Mitsubishi Heavy Industries

- 6.4.8 Northrop Grumman Corporation

- 6.4.9 Thales

- 6.4.10 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms