|

市場調査レポート

商品コード

1644999

LPGタンカー:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)LPG Tanker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| LPGタンカー:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

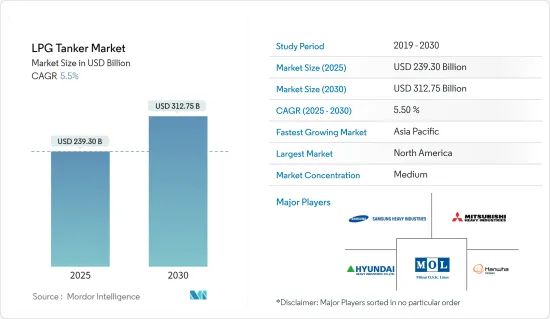

LPGタンカーの市場規模は2025年に2,393億米ドルと推定され、予測期間(2025~2030年)のCAGRは5.5%で、2030年には3,127億5,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的に市場を牽引すると予想される要因としては、今後数年間のシェールガス生産の力強い伸びと、暖房・換気・空調(HVAC)用途のLPG需要の高まりが挙げられます。

- しかし、不安定な原油価格はLPG価格の上昇と需要の減少を招き、予測期間を通じて市場の成長を抑制すると予想されます。

- タンカー船体へのセミメンブレンタンクや船首耐波システムの統合など、いくつかの技術的進歩が予測期間中に機会を生み出すと予想されます。

- 予測期間中は、主にLPG需要の増加により、北米が市場を独占すると予想されます。

LPGタンカーの市場動向

超大型ガスキャリアセグメントが大幅な成長を遂げる見込み

- 超大型ガスキャリア(VLGC)は、さまざまな国をまたがる長距離のLPGガス輸送に広く使用されています。中東とアジア諸国、西アフリカと欧州、米国といった国々の間で液化石油ガス貿易関係が拡大していることが、大型運搬船セグメントを後押しする主要要因となっています。

- VLGCは一般的に全長約250~300メートルで、中心線に沿って4~6基の貯蔵タンクを備えています。

- 各国で超大型ガス運搬船の建造が進んでいます。例えば、NYKは2023年7月、Kawasaki Heavy Industries Ltd.(KHI)から6隻目の液化石油ガス(LPG)兼用超大型LPG/液化アンモニアガス運搬船(VLGC)を受注したと発表しました。本船はKawasaki Heavy Industries Ltd.の事業所で建造され、2026年の引き渡しを予定しています。

- 2023年4月には、中国国営造船傘下の江南造船所が開発・設計・建造した世界初の大型液化ガス運搬船Harzand(容量9万3,000立方メートル)が竣工します。

- さらに、いくつかの国からのLNG輸出も増加しています。米国は世界有数のLNG輸出国です。Energy Institute Statistical Review of World Energy 2023によると、米国は2022年に1,043億立方メートルのLNGを輸出し、前年比10.13%の伸びを示しました。

- 以上のことから、LPGタンカー市場は、貿易関係の増加と新造大型ガス運搬船の採用より、プラス成長が見込まれます。

北米が市場を独占する見込み

- カナダでは、特に輸送と調理部門におけるLPG燃料の大量消費と使用を促進するために、インセンティブ、燃料補助金、流通ライセンスを提供する政府の取り組みが行われており、予測期間中にLPG市場の成長を加速させると予想されます。

- さらに、この地域の政府は、薪、牛糞、石炭のような従来の化石燃料の燃焼から発生する有害ガスによる死亡率の割合を減らすために、LPGの使用に注力しています。このような取り組みにより、LPGタンカー市場の需要は今後数年間で増加する可能性が高いです。

- 北米におけるNGL総生産量のうち、大半はLPG生産に回されています。さらに、米国、カナダ、メキシコが原油精製所からのLPG生産に貢献しているため、北米は主要なLPG生産地域のひとつとなっています。

- 2023年7月、米国政府はベネズエラへの液化石油ガス輸出を許可しました。ベネズエラ政府、Petroleos de Venezuela(PdVSA)、またはPetroleos de Venezuelaが直接・間接に50%以上の権益を保有する事業体が関与する、直接・間接を問わずベネズエラへの液化石油ガスの輸出・再輸出に関連するすべての取引・活動が認められています。

- 以上の点から、LPGタンカー市場は、新たな液化トレインの採用と他地域からの需要により、北米で飛躍的な成長が見込まれています。

LPGタンカー産業概要

LPGタンカー市場は適度に統合されています。この市場の主要企業(順不同)には、Samsung Heavy Industries、Mitsubishi Heavy Industries Ltd.、HD Hyundai Heavy Industries、Hanwha Ocean、Mitsui OSK Lines Ltd.などが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- シェールガス生産の力強い成長

- 暖房、換気、空調用LPG需要の増加

- 抑制要因

- 不安定な原油価格

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 船舶サイズ

- 超大型ガスキャリア

- 大型ガスキャリア

- 中型ガスキャリア

- 小型ガスキャリア

- 冷凍と加圧

- 完全加圧

- 半加圧

- 完全冷凍

- 超低温

- 2028年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Samsung Heavy Industries Co. Ltd

- HD Hyundai Heavy Industries Co. Ltd

- Hanwha Ocean Co., Ltd.

- K Shipbuilding Co., Ltd.

- Mitsubishi Heavy Industries Ltd.

- Kawasaki Heavy Industries Ltd.

- China Shipbuilding Trading Co. Ltd.

- Japan Marine United Corporation

- HJ Shipbuilding & Construction Company, Ltd.

- Mitsui OSK Lines Ltd.

第7章 市場機会と今後の動向

- デジタルソリューションに関する技術の進歩

目次

Product Code: 50000867

The LPG Tanker Market size is estimated at USD 239.30 billion in 2025, and is expected to reach USD 312.75 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the factors expected to drive the market include strong growth in shale gas production over the coming years and the rising demand for LPG for heating, ventilation, and air conditioning (HVAC) applications.

- However, unstable crude oil prices led to amplified LPG prices and reduced demand, which are expected to restrain market growth throughout the forecast period.

- Nevertheless, several technological advancements, such as the integration of semi-membrane tanks and bow wave resistance systems on the tanker hull, are expected to create opportunities during the forecast period.

- North America is expected to dominate the market during the forecast period, mainly due to the growing demand for LPG.

LPG Tanker Market Trends

Very Large Gas Carrier segment is expected to witness significant growth

- Very Large Gas Carriers (VLGC) are widely used to transport LPG gas for longer distances across various countries. Growing liquefied petroleum gas trade relationships between countries, such as the Middle East and Asian countries, Western Africa and Europe, and the United States, is the major factor boosting the large carrier segment.

- VLGC vessels are generally around 250-300 meters long and have four to six storage tanks along the centerline.

- There are several advancements in constructing Very large gas carriers in various countries. For instance, in July 2023, NYK announced the order of its sixth liquefied petroleum gas (LPG) dual-fuel very large LPG / liquefied ammonia gas carrier (VLGC) from Kawasaki Heavy Industries Ltd. (KHI). The ship will be built at the KHI Sakaide Works shipyard and is set for delivery in 2026.

- In April 2023, Harzand, the world's first large liquefied gas carrier with a capacity of 93,000 cubic meters developed, designed, and built by Jiangnan Shipyard under China State Shipbuilding.

- Further, there are increasing LNG exports from several countries. United States is one of the major LNG exporters globally. According to Energy Institute Statistical Review of World Energy 2023, the United States exported 104.3 billion cubic metres of LNG in 2022, with a growth rate of 10.13% from the previous year.

- Thus, the points mentioned above suggest that the LPG tanker market is expected to grow positively with the increase in trade relationships and the introduction of new, Very Large Gas Carriers.

North America is expected to dominate the market

- Government initiatives in Canada to provide incentives, fuel subsidies, and distribution licenses to promote large consumption and usage of LPG fuels, especially in the transport and cooking sectors, are anticipated to accelerate the LPG market growth during the forecast period.

- Further, the governments in the region are concentrating on using LPG to reduce the percentage of the death rate due to the harmful gases produced from the combustion of conventional fossil fuels like wood, cow dung, and coal. Such initiatives will likely increase the LPG Tanker market demand in the coming years.

- Out of the total NGL production in North America, most goes to LPG production. Moreover, the contribution of the United States, Canada, and Mexico to LPG production from the crude oil refineries makes North America one of the main LPG-producing regions.

- In July 2023, the US government authorized liquefied petroleum gas exports to Venezuela. All transactions and activities related to the exportation or re-exportation, directly or indirectly, of liquefied petroleum gas to Venezuela, involving the Government of Venezuela, Petroleos de Venezuela (PdVSA), or any entity in which PdVSA owns, directly or indirectly, a 50 percent or greater interest, are allowed.

- The points mentioned above suggest that the LPG tanker market is expected to grow exponentially in North America owing to the introduction of new liquefaction trains and demand from other regions.

LPG Tanker Industry Overview

The LPG tanker market is moderately consolidated. Some of the key players in this market (in no particular order) include Samsung Heavy Industries Co. Ltd., Mitsubishi Heavy Industries Ltd., HD Hyundai Heavy Industries Co. Ltd., Hanwha Ocean Co. Ltd., and Mitsui OSK Lines Ltd. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Strong Growth in Shale Gas Production

- 4.5.1.2 Rising demand of LPG for heating, ventilation and Air conditioning

- 4.5.2 Restraints

- 4.5.2.1 Unstable Crude Oil Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vessel Size

- 5.1.1 Very Large Gas Carrier

- 5.1.2 Large Gas Carrier

- 5.1.3 Medium Gas Carrier

- 5.1.4 Small Gas Carrier

- 5.2 Refrigeration and Pressurization

- 5.2.1 Fully Pressurized

- 5.2.2 Semi-pressurized

- 5.2.3 Fully Refrigerated

- 5.2.4 Extra Refrigerated

- 5.3 Geography [Market Size and Demand Forecast till 2028 (for regions only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 South Africa

- 5.3.4.4 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Chile

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Samsung Heavy Industries Co. Ltd

- 6.3.2 HD Hyundai Heavy Industries Co. Ltd

- 6.3.3 Hanwha Ocean Co., Ltd.

- 6.3.4 K Shipbuilding Co., Ltd.

- 6.3.5 Mitsubishi Heavy Industries Ltd.

- 6.3.6 Kawasaki Heavy Industries Ltd.

- 6.3.7 China Shipbuilding Trading Co. Ltd.

- 6.3.8 Japan Marine United Corporation

- 6.3.9 HJ Shipbuilding & Construction Company, Ltd.

- 6.3.10 Mitsui OSK Lines Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancement with Respect to Digital Solutions