|

市場調査レポート

商品コード

1693442

ソルガム種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Sorghum Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ソルガム種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 379 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

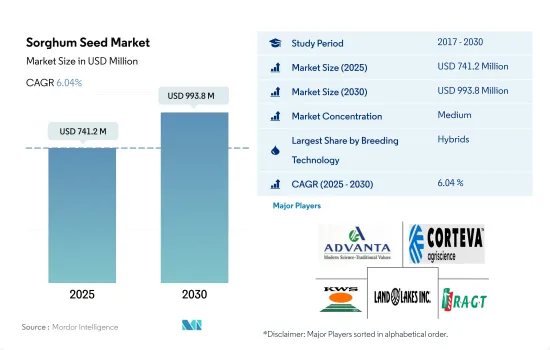

ソルガム種子の市場規模は2025年に7億4,120万米ドルと推定され、2030年には9億9,380万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.04%で成長します。

ハイブリッド種子の売上は、病気や宿根に対する耐性やストレス耐性が高いことを好む生産者の嗜好によって牽引されています。

- 2022年には、ソルガム種子のハイブリッド種子が世界のソルガム種子市場で70.2%の主要シェアを占め、開放受粉品種とハイブリッド派生種子のシェアは29.8%でした。ハイブリッド分野は2023-2030年の間に金額ベースで52.4%成長すると推定されます。ハイブリッドは穀物収量の増加に大きく貢献しました。アジアでは穀物生産性が40%向上しました。

- ハイブリッド種子は高コストであるため、ソルガムの開放受粉品種とハイブリッド派生品種は予測期間中に37.2%増加すると推定されます。ナイジェリアはアフリカ最大の開放受粉品種およびハイブリッド派生品種の作付面積を有し、OPV全体の作付面積の約20%を占めています。

- 世界のハイブリッドソルガム種子市場では、非遺伝子組み換えソルガム種子のみが入手可能です。非遺伝子組み換えソルガム種子は世界のソルガム種子市場の約70%を占めています。非遺伝子組換えソルガム種子セグメントは成長すると推定され、予測期間中にCAGR 6.8%を記録します。

- 北米はハイブリッドソルガムの主要生産国です。同地域で栽培されているソルガムの80%以上をハイブリッド品種が占めています。ハイブリッド品種ソルガムの導入は、輸出需要の高まりとこの地域の人口増加によって推進されています。北米では米国がハイブリッド品種の使用で大きなシェアを占めており、同国で栽培されているソルガムの98%を占めています。

- 大規模農家は、ハイブリッド種子に比べて収量が低く、病気にかかりやすく、栽培に多くの面積を必要とするため、開放受粉種子品種を使用しないです。そのため、ハイブリッド種子に関連するさまざまな利点から、ハイブリッド分野は成長すると推定されます。

北米はハイブリッド種子と商業種子の採用率が高いため市場を独占

- 北米は世界最大のソルガム生産国のひとつです。この地域は2022年の世界のソルガム種子市場の45.6%を占めています。ソルガムは米国で栽培されている穀物としては第3位で、世界のソルガム生産量の30%近くを占めています。米国におけるソルガム栽培面積は2017年から2022年にかけて30%増加したが、これは家畜飼料やバイオ燃料生成など様々な用途での需要が増加しているためです。

- 2022年には、アフリカが世界のソルガム種子市場の18.9%のシェアを占め、2017年から2022年の間に37.1%の大幅な伸びを示しました。ナイジェリアはアフリカ最大のソルガム生産国で、2022年にはアフリカのソルガム種子市場の51.4%を占める。

- アジア太平洋では、ソルガムは主要穀物作物のひとつです。この地域は2022年の世界のソルガム種子市場の16.4%を占めています。2022年のソルガム栽培面積は710万haで、前年より15.6%増加しました。2022年の世界のソルガム種子市場では、中国が21.6%の主要シェアを占めています。

- 2022年にはブラジルとアルゼンチンが世界のソルガム種子市場の9.5%を占める。中国がブラジルとアルゼンチンからソルガムの輸入需要を増やしているため、同国政府は国内需要を満たすためにソルガム生産者に財政支援を行っています。

- フランスはソルガムの主要生産国であり輸出国でもあり、2022年には欧州のソルガム種子市場の42.7%を占める。フランスの栽培面積は2017年から2022年の間に約50%増加しました。

- 中東は、2022年の世界のソルガム種子市場の1.9%の市場シェアを占めており、水をあまり必要としない作物であるにもかかわらず、比較的著しく少ないです。

世界のソルガム種子市場の動向

気候条件と水不足によりソルガムの栽培面積はアフリカが優勢

- ソルガムは食用および飼料用として世界的に栽培されている重要な穀物です。ソルガムは半乾燥熱帯地域で最も広く栽培されているが、そこでは水の利用可能量が限られており、頻繁に干ばつに見舞われます。世界のソルガム栽培面積は2016年から2022年にかけて8.2%減少しました。農家は投資収益率が高いため、ソルガムよりも米、小麦、その他の換金作物を好み、ソルガムの栽培面積の減少につながっています。

- アフリカはソルガム栽培面積が最も大きく、2022年には世界のソルガム栽培面積の69.5%を占める。栽培面積は2016年から2022年の間に6.2%の減少を示したが、これは農家が需要の増加によりトウモロコシを含む他の作物にシフトしたためです。

- アジア太平洋では、2022年のソルガム栽培面積は540万ヘクタールで、世界のソルガム栽培面積の13.3%を占める。ソルガム栽培面積を押し上げる要因は、他の作物よりも乾燥した土地や限界的な土地でも収量と生育が可能なことです。ソルガムの特徴的な遺伝子と構成により、他の作物では生育できないような様々な気候条件でも生育することができます。

- 北米では、ソルガムの栽培面積は2017年から2022年の間に13%増加し、2022年には410万ヘクタールに達しました。米国だけで、2022年の北米のソルガム栽培面積の64.6%を占めています。ソルガムの輸出需要の高まり、特に中国の巨大な飼料産業からの需要が、同国で商業的に運営されているソルガム農場からの種子販売を後押ししています。そのため、作付面積は予測期間中に増加すると見込まれます。南米と欧州はソルガムの市場が緩やかで、栽培面積が少ないです。

幅広い適応性、耐病性、早熟などの形質を持つソルガム種子は、加工産業の需要を満たすために高い成長を示しています。

- ソルガムは主にアフリカや北米で穀物や家畜飼料の飼料として栽培されています。水不足が深刻なアフリカでは主食のひとつです。また、水不足に耐えられる穀物作物のひとつでもあります。牛の頭数の増加や、過去5年間のこの地域の気象条件の変化(アフリカの干ばつなど)に伴い、干ばつに強い品種が普及しつつあります。さらに、天候や土壌条件の変化に伴い、生物学的および生物学的ストレスが増加しているため、悪条件下でも高品質の作物を生産して高収益を得ようとする生産者により、より幅広い適応性を持つ品種が採用されるようになっています。Advanta Seeds社、KWS Saat &Co.社、Land O'Lakes社などの企業は、この高い需要に応えるため、より広い適応性形質を提供しています。

- 耐病性形質、ならびにべと病、根腐病、うどんこ病モザイク・ウイルス、およびその他の病害に対する耐性も、非常に人気が高く、広く栽培されている主要な形質です。これらの病害は、圃場条件下での収量に大きな損失をもたらします。したがって、これらの品種はこれらの病気に抵抗し、作物の生産性を高める。さらに、害虫(ステムボーラー、シュートフライ、ミズハモグリバエ)に対する抵抗性、低タンニン含量および高タンニン含量、早生・中生品種、粒の色(赤、白、パールホワイトなど)といった他の形質も、主に世界的に利用されています。KWSのFenixusとBRS 310-Graniferousは作物の早熟化に役立つ製品です。

- 消費者、加工産業、酪農家からの需要の増加により、高度形質に対する需要は今後増加すると予想されます。

ソルガム種子産業の概要

ソルガム種子市場は適度に統合されており、上位5社で48.04%を占めています。この市場の主要企業は以下の通りです。 Advanta Seeds-UPL, Corteva Agriscience, KWS SAAT SE & Co. KGaA, Land O'Lakes Inc. and RAGT Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニック・ハイブリッド

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 地域

- アフリカ

- 育種技術別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- ミャンマー

- パキスタン

- フィリピン

- タイ

- その他アジア太平洋地域

- 欧州

- 育種技術別

- 国別

- フランス

- ドイツ

- イタリア

- ルーマニア

- ロシア

- スペイン

- ウクライナ

- その他欧州

- 中東

- 育種技術別

- 国別

- イラン

- サウジアラビア

- その他中東

- 北米

- 飼育技術別

- 国別

- メキシコ

- 米国

- その他北米地域

- 南米

- 育種技術別

- 国別

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Capstone Seeds

- Corteva Agriscience

- Kaveri Seeds

- KWS SAAT SE & Co. KGaA

- Land O'Lakes Inc.

- RAGT Group

- Royal Barenbrug Group

- S&W Seed Co.

- Seed Co. Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92504

The Sorghum Seed Market size is estimated at 741.2 million USD in 2025, and is expected to reach 993.8 million USD by 2030, growing at a CAGR of 6.04% during the forecast period (2025-2030).

Hybrid seed sales are driven by the growers' preference to have higher resistance to diseases and lodging and stress resistance

- In 2022, sorghum hybrid seeds held a major share of 70.2% of the global sorghum seed market, while open-pollinated varieties and hybrid derivatives had a 29.8% share. The hybrid segment is estimated to grow by 52.4% in terms of value during 2023-2030. Hybrids contributed significantly to increased grain yields. Grain productivity has increased by 40% in Asia.

- Due to the high cost of hybrid seeds, the open-pollinated varieties and hybrid derivatives of sorghum are estimated to increase by 37.2% during the forecast period. Nigeria holds Africa's largest land under open-pollinated varieties and hybrid derivatives, accounting for about 20% of overall OPV acreage.

- Only non-transgenic sorghum seeds are available in the global hybrid sorghum seed market. Non-transgenic sorghum seeds account for approximately 70% of the global sorghum seed market. The non-transgenic sorghum seeds segment is estimated to grow, registering a CAGR of 6.8% during the forecast period.

- North America is the leading producer of hybrid sorghum. Hybrid varieties accounted for more than 80% of the sorghum grown in the region. Introducing hybrid sorghum varieties is driven by the rising export demand and the region's growing population. The United States holds a major share in using hybrid varieties in North America, accounting for 98% of sorghum cultivated in the country.

- Large-scale farmers do not use open-pollinated seed varieties, as they have lower yields, are more susceptible to disease, and need a lot of areas to grow compared to hybrid seeds. Thus, the hybrid segment is estimated to grow because of the various benefits associated with hybrids.

North America dominated the market due to higher adoption of hybrids and commercial seeds

- North America is one the largest sorghum producers in the world. The region accounted for 45.6% of the global sorghum seed market in 2022. The sorghum was the third-largest cereal grain grown in the United States, accounting for nearly 30% of all sorghum production worldwide. The area under sorghum cultivation in the United States increased by 30% between 2017 and 2022 because of the increased demand for various uses such as livestock feed and biofuel generation.

- In 2022, Africa accounted for an 18.9% share of the global sorghum seed market which showed a significant growth of 37.1% between 2017 and 2022. Nigeria is the largest sorghum producer in Africa, accounting for 51.4% of the African sorghum seed market in 2022.

- In Asia-Pacific, sorghum is one of the major cereal crops. The region accounted for 16.4% of the global sorghum seed market in 2022. The acreages under sorghum cultivation were 7.1 million ha in 2022, 15.6% more than the previous year. China holds a major share of 21.6% in the global sorghum seed market in 2022.

- In 2022, Brazil and Argentina accounted for 9.5% of the global sorghum seed market. The country's government is providing financial support to sorghum growers to meet the domestic demand due to the increasing demand from China to import sorghum from Brazil and Argentina.

- France is a major sorghum grower and exporter, accounting for 42.7% of the market for sorghum seeds in Europe in 2022. France's cultivation area increased by almost 50% between 2017 and 2022.

- The Middle East has a market share of 1.9% of the global sorghum seed market in 2022, which is comparatively significantly less despite the crop requiring less water.

Global Sorghum Seed Market Trends

Africa dominated the area under cultivation for sorghum due to its climatic conditions and water scarcity

- Sorghum is an important cereal crop grown globally for food and feed. It is most widely grown in the semi-arid tropics, where water availability is limited and frequently subjected to drought. The global sorghum cultivation area decreased by 8.2% from 2016 to 2022. Farmers prefer rice, wheat, and other cash crops over sorghum due to the high return on investment, leading to a decline in the acreage for sorghum.

- Africa has the largest area under cultivation for sorghum, which accounted for 69.5% of the global sorghum cultivation area in 2022. The acreage showed a decline of 6.2% between 2016 and 2022 due to the farmer's shift toward other crops, including corn, due to higher demand.

- In Asia-Pacific, the acreage under sorghum cultivation was 5.4 million hectares in 2022, representing 13.3 % of the global sorghum cultivation area. A factor driving the acreage under sorghum is its ability to yield and grow in dry and marginal land more than other crops. Its distinct genetics and composition allow it to grow in various climatic conditions where other crops cannot.

- In North America, the area under cultivation of sorghum increased by 13% between 2017 and 2022, which reached 4.1 million hectares in 2022. The United States alone accounted for 64.6% of North America's sorghum acreage in 2022. The rising export demand for sorghum, especially from the massive Chinese feed industry, is boosting seed sales from the commercially operated sorghum farms in the country. Thus, the acreage is expected to increase during the forecast period. South America and Europe have moderate markets for sorghum, and the cultivation area is low in these regions.

Sorghum seeds with traits such as wider adaptability, disease resistance, and early maturity are witnessing high growth to meet the demand of processing industries

- Sorghum is mainly cultivated in Africa and North America as a grain and forage for cattle feed. It is one of the staple foods in Africa, where water scarcity is high. It is also one of the grain crops that can withstand low water conditions. With the increase in the cattle population and changes in weather conditions over the past five years in the region (such as droughts in Africa), varieties tolerant to drought are becoming popular. Furthermore, with the changing weather and soil conditions, there has been an increase in biotic and abiotic stress, which has led to the growth of broader adaptability varieties being adopted by the growers to earn high profits by producing high-quality crops in adverse conditions. Companies such as Advanta Seeds, KWS Saat & Co., and Land O' Lakes are providing wider adaptability traits to meet this high demand.

- Disease-resistant traits, as well as resistance to downy mildew, root rots, downy mosaic virus, and other diseases, are other major traits that are very popular and widely cultivated. These diseases cause significant yield losses during field conditions. Therefore, these varieties resist these diseases and increase the productivity of the crops. Additionally, other traits such as resistance to pests (stem borers, shoot-fly, and midge fly), low and high tannin content, early-medium matured varieties, and the color of the grains (red, white, pearl white, etc.) are primarily used globally. KWS Fenixus and BRS 310 - Graniferous by KWS are the products that help in the early maturity of the crop.

- The demand for advanced traits is expected to increase in the future due to increased demand from consumers, the processing industry, and dairy farmers.

Sorghum Seed Industry Overview

The Sorghum Seed Market is moderately consolidated, with the top five companies occupying 48.04%. The major players in this market are Advanta Seeds - UPL, Corteva Agriscience, KWS SAAT SE & Co. KGaA, Land O'Lakes Inc. and RAGT Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Egypt

- 5.2.1.2.2 Ethiopia

- 5.2.1.2.3 Ghana

- 5.2.1.2.4 Kenya

- 5.2.1.2.5 Nigeria

- 5.2.1.2.6 South Africa

- 5.2.1.2.7 Tanzania

- 5.2.1.2.8 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Myanmar

- 5.2.2.2.6 Pakistan

- 5.2.2.2.7 Philippines

- 5.2.2.2.8 Thailand

- 5.2.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Romania

- 5.2.3.2.5 Russia

- 5.2.3.2.6 Spain

- 5.2.3.2.7 Ukraine

- 5.2.3.2.8 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.4.2.2 Saudi Arabia

- 5.2.4.2.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Mexico

- 5.2.5.2.2 United States

- 5.2.5.2.3 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Capstone Seeds

- 6.4.3 Corteva Agriscience

- 6.4.4 Kaveri Seeds

- 6.4.5 KWS SAAT SE & Co. KGaA

- 6.4.6 Land O'Lakes Inc.

- 6.4.7 RAGT Group

- 6.4.8 Royal Barenbrug Group

- 6.4.9 S&W Seed Co.

- 6.4.10 Seed Co. Limited

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms