|

市場調査レポート

商品コード

1430565

世界の検眼機器 - 市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Optometry Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の検眼機器 - 市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

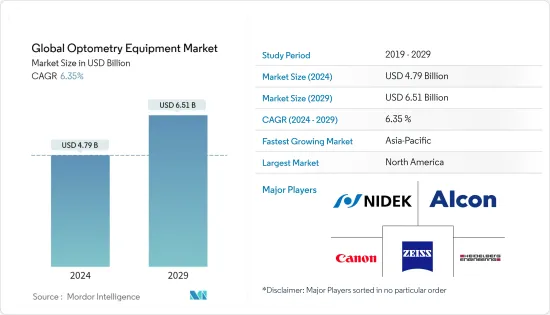

検眼機器の世界市場規模は2024年に47億9,000万米ドルと推定・予測され、2029年には65億1,000万米ドルに達し、予測期間(2024-2029年)のCAGRは6.35%で成長すると予測されています。

COVID-19は検眼機器市場に大きな影響を与えました。2020年10月に発表された「The impact of COVID-19 pandemic on ophthalmology services:are we ready for the aftermath?"(眼科サービスにおけるCOVID-19パンデミックの影響:余波への備えはできているか)」と題された調査によると、眼科は最も多忙で外来患者の多い専門科の1つを代表し、英国では毎年約750万件の外来予約と50万件以上の外科手術が行われています。最近のパンデミック封鎖では、何千もの眼科臨床の診察や手術がキャンセルされ、患者の視力に永久的かつ重大な害を及ぼす可能性があった。とはいえ、遠隔診察やバーチャル診療のおかげで、検眼機器の需要はすぐにパンデミック以前のレベルにまで急増しそうです。例えば、2021年1月に発表された「新興諸国におけるパンデミック時の眼科医療へのアクセスにおける遠隔相談の有用性」というタイトルの論文によると、デジタルイニシアチブは、封鎖中に眼科医療サービスを部分的に維持することができました。さらに、パンデミック中およびそれ以降も、遠隔診察の利用率を向上させるための重点的な戦略が必要でした。したがって、上記の要因の通り、COVID-19は検眼機器市場に大きな影響を与えました。

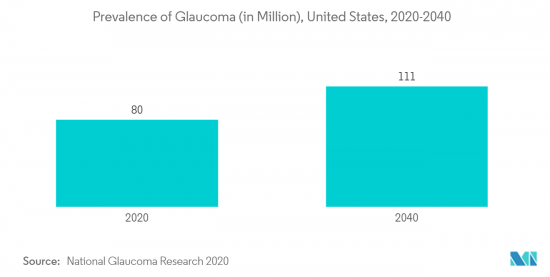

検眼機器市場の成長要因には、眼疾患の有病率の上昇や検眼機器分野の技術進歩などがあります。眼病は、個人の肉体的・精神的健康に悪影響を及ぼす世界の健康問題です。多くの先進国や発展途上国では、眼疾患が潜在的な脅威として浮上しています。例えば、BrightFocus Foundationの2021年最新情報によると、300万人以上のアメリカ人が緑内障を患っており、そのうち270万人(40歳以上)が最も一般的な緑内障である開放隅角緑内障に罹患しています。さらに、国立眼科研究所の2022年最新情報によると、2010年から2050年の間に、白内障に罹患した人の数は2,440万人から5,000万人に倍増すると推定されています。したがって、眼に関連する疾患の負担の増加、スクリーニングと診断の増加は、調査対象市場の成長に大きな影響を与えると予測されます。

さらに、眼科分野における政府の取り組みや研究開発の増加が市場の成長を促進しています。例えば、世界保健機関(WHO)の2021年7月の最新情報によると、国連総会で各国政府は、眼科医療サービスを国民皆保険の重要な要素とし、持続可能な開発における視力喪失の影響の増大に対処するためのさらなる努力を約束する新たな決議を採択しました。さらに、検眼分野での買収合併や製品発売が市場成長を後押ししそうです。例えば、2022年4月、カールツァイスメディテックは、ソリューションプロバイダーとしてのポジショニングをさらに強化するため、手術器具メーカー2社(Kogent Surgical, LLCおよびKatalyst Surgical, LLC)を買収しました。この買収は、事業規模を拡大し、手術ソリューションの提供に貢献し、経常収益を増やすことに主眼を置いています。したがって、このような戦略的企業買収や政府の取り組みは、調査対象市場の成長に大きな影響を与えると予測されます。

前述の要因から、検眼機器市場は予測期間中に成長する可能性が高いです。しかし、検眼機器の高価格や認知度の低さ、低所得国での眼科医療へのアクセスの低さが市場成長を抑制しています。

検眼機器市場の動向

OCTスキャナーセグメントが予測期間中に大きな市場シェアを占める見込み

光干渉断層計(OCT)は、光波を利用して網膜の断面写真を撮影する非侵襲的な画像検査です。主な収益要因は、緑内障、スコトーマ、その他の網膜疾患などの眼疾患の有病率の増加によるものです。

網膜疾患の高い有病率と競合他社の存在。製品の発売、合併、買収、光干渉断層計に関連する研究は、市場の成長を促進します。例えば、キヤノンは2021年7月、1回のスキャンで最大23×20mmの高解像度画像を撮影できる広視野掃引光干渉断層計(OCT)「Xephilio OCT-S1」を発売しました。この製品は、アジア太平洋白内障屈折矯正外科学会-シンガポール国立眼科センター(APACRS-SNEC)の合同イベントで、眼科医療従事者に披露されました。キヤノンのディープスキャニング掃引光源技術により、約80度という非常に広い角度での操作が可能になった。

さらに、「Advances in Optical Coherence Tomography Imaging Technology and Techniques for Choroidal and Retinal Disorders」というタイトルで2022年8月に発表された論文によると、脈絡膜や網膜の病気を治療するための現在の診療におけるいくつかの欠点を克服するために、OCT技術が使用されています。これらの研究開発は、基礎的な科学研究の発展と脈絡膜疾患の病態生理学の理解に役立つと思われます。これらのアプリケーションは、超広視野OCTのような技術によって実証されたように、周辺部でのOCT機能によって網膜疾患の検出とモニタリングを支援することができます。

従って、上記の要因から、OCTスキャナは予測期間中にセグメントの成長を牽引すると予想されます。

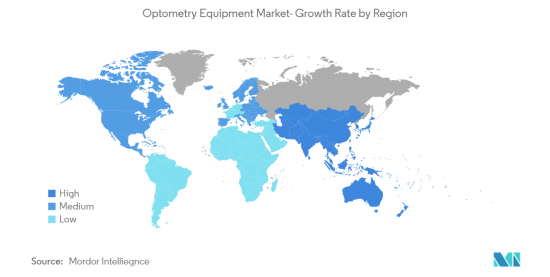

北米が検眼機器市場を独占、予測期間も同様

北米地域の市場成長を促進する主な要因には、眼疾患の新興国市場や高齢者人口の増加、高度に発達したヘルスケアインフラ、同地域における主要市場プレイヤーの存在などがあります。

2021年、カナダ眼科学会は緑内障啓発月間に、緑内障は毎年80万人以上のカナダ人を罹患させていると述べた。啓発月間では、カナダにおける高齢化人口の増加のような事実が、この病気の負担の増加につながり、緑内障は今後数年でカナダで流行病になる可能性があると述べられ、市場成長を後押しすると期待されています。また、2020年6月にInvestigative Ophthalmology &Visual Science誌に掲載された研究によると、メキシコでは2030年までに緑内障患者数が106万人に達し、2040年には127万人、2050年には143万人に増加すると推定されています。さらに、市場プレイヤーは市場シェアを拡大するために、製品投入、発展、買収、提携、合併、拡大など様々な戦略を採用しました。例えば、2020年9月、トプコンは米国市場でAladdin-Mソフトウェアを発売しました。このソフトウェアは、角膜曲率、瞳孔動態、軸長メトリクスを測定し、円錐角膜スクリーニングのための機能を組み込んでいます。

政府の取り組み、研究開発、デジタルヘルスケアシステムの導入が増加し、予測期間中の市場成長を後押しします。例えば、2022年6月にNational Eye Institute(NEI)に掲載されたニュースによると、National Eye Institute(NEI)の研究者は、シャープで中心的な視覚に必要な光を感知する網膜の小さな部分である黄斑を冒す新しい病気を特定しました。科学者たちは、まだ命名されていない新しい黄斑ジストロフィーに関する発見を報告しました。したがって、このような調査は検眼機器の採用を増加させ、市場成長を後押しします。

検眼機器産業の概要

検眼機器市場は適度な競争があり、眼科診断や治療用の製品を提供する大小さまざまな外科/医療機器製造企業で構成されています。市場参入企業には、アルコン、カールツァイス・メディテックAG、キヤノン、ハイデルベルグ・エンジニアリングGmbH(ハイデルベルグ・エンジニアリング社)、NIDEKなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 眼疾患の有病率の上昇

- 眼科医療機器の技術進歩

- 視覚障害抑制のための政府イニシアチブの増加

- 市場抑制要因

- 眼科検査機器の高コスト

- 低所得国における眼科医療への認識不足とアクセスの低さ

- 産業の魅力- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 検査タイプ別

- 網膜検査

- OCTスキャナー

- 眼底カメラ

- 視野計

- 検眼鏡

- 網膜鏡

- 角膜検査

- 波面収差計

- 鏡面顕微鏡

- その他の角膜検査

- 一般検査

- オートレフラクター

- 眼科超音波システム

- 眼圧計

- フォロプター

- ケラトメーター

- レンズメーター

- その他一般検査

- 網膜検査

- エンドユーザー別

- 眼科クリニック

- 病院

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Alcon

- Canon Inc.

- Carl Zeiss Meditec AG

- Bausch Health Companies Inc(Bausch+Lomb)

- Essilor Luxottica(Essilor International SA)

- Johnson & Johnson

- Heidelberg Engineering GmbH(Heidelberg Engineering Inc.)

- HEINE Optotechnik

- Nidek Co. Ltd

- Halma plc(Keeler Ltd)

- Revenio Group PLC(iCare Finland OY)

- AMETEK PIP Holdings, Inc(Reichert Technologies)

- Oculus Inc.

第7章 市場機会と今後の動向

The Global Optometry Equipment Market size is estimated at USD 4.79 billion in 2024, and is expected to reach USD 6.51 billion by 2029, growing at a CAGR of 6.35% during the forecast period (2024-2029).

COVID-19 had a significant impact on the optometry equipment market. As per the study published in October 2020, titled "The impact of COVID-19 pandemic on ophthalmology services: are we ready for the aftermath?", ophthalmology represented one of the busiest and most heavily outpatient-oriented specialties, with approximately 7.5 million outpatient appointments and more than 500,000 surgical procedures in the United Kingdom each year. The recent pandemic lockdown resulted in the cancellation of thousands of ophthalmic clinical visits and surgeries, which could potentially lead to permanent and significant harm to patients' vision. Even though, owing to teleconsultations and virtual care practices, the demand for optometry equipment is likely to soar to its pre-pandemic levels soon. For instance, as per the article published in January 2021, under the title 'Utility of teleconsultation in accessing eye care in a developing country during COVID-19 pandemic', the digital initiatives were able to partially maintain eye care services during the lockdown. Additionally, focused strategies to improve teleconsultation utilization were required during the pandemic and beyond. Hence, as per the factors mentioned above, COVID-19 had a significant impact on the optometry equipment market.

Some of the factors responsible for the growth of the optometry equipment market include the rising prevalence of eye diseases and technological advancements in the field of optometry equipment. Eye disease is a global health concern that negatively impacts individuals' physical and mental health. In many developed and developing countries, eye conditions have emerged as potential threats. For instance, as per the 2021 update from BrightFocus Foundation, more than 3 million Americans are living with glaucoma, and 2.7 million of whom-aged 40 and older are affected by its most common form, open-angle glaucoma. Moreover, as per the 2022 update from National Eye Institute, between 2010 and 2050, the estimated number of people who have had cataracts is likely to be doubled from 24.4 million to 50 million. Hence, the rising burden of eye-related disorders and increased screening and diagnosis of the same is projecting a great impact on the growth of the market studied.

Furthermore, increased government initiatives and research and development in the field of ophthalmology are fuelling market growth. For instance, as per the July 2021 update from World Health Organization, at the United Nations General Assembly, governments adopted a new resolution pledging further efforts to make eye care services a crucial component of universal health coverage and address the growing impact of vision loss on sustainable development. Moreover, the acquisition merger and product launches in the field of optometry are likely to boost market growth. For instance, in April 2022, Carl Zeiss Meditec acquired two manufacturers of surgical instruments (Kogent Surgical, LLC and Katalyst Surgical, LLC) to further strengthen its positioning as a solution provider. This acquisition is mainly focused to scale the businesses and contribute to its surgical solution offering and add recurring revenue. Hence, such strategic company acquisitions and government initiatives are projecting a great impact on the growth of the market studied.

As per the aforementioned factors, the optometry equipment market is likely to grow over the forecast period. However, the high cost of eye examination equipment and lack of awareness, and low accessibility to eye care in low-income economies restrain the market growth.

Optometry Equipment Market Trends

OCT Scanner Segment is Expected to Hold Significant Market Share Over the Forecast Period

Optical coherence tomography (OCT) is a non-invasive imaging test that uses light waves to take cross-section pictures of the retina. The primary factors attributed to the major revenue are due to the growing prevalence of eye conditions, such as glaucoma, scotoma, and other retinal diseases.

The high prevalence of retinal diseases, and the presence of competitors. Product launches mergers, acquisitions, and research relating to optical coherence tomography fuel the market growth. For instance, in July 2021, Canon launched Xephilio OCT-S1, a wide-field swept-source Optical Coherence Tomography (OCT) capable of capturing high-resolution images of up to 23 x 20 mm in a single scan. The product was unveiled to the eyecare medical practitioners at the Asia Pacific Association of Cataract and Refractive Surgeons- Singapore National Eye Centre (APACRS-SNEC) joint event. Canon's deep scanning swept-source technology enables it to operate at an extremely wide angle of around 80 degrees.

Furthermore, as per the article published in August 2022 under the title 'Advances in Optical Coherence Tomography Imaging Technology and Techniques for Choroidal and Retinal Disorders', to overcome several shortcomings in the present practices for treating choroidal and retinal illnesses, OCT technology is used. These developments are likely to aid in the development of fundamental scientific research and the comprehension of the pathophysiology of chorioretinal disorders. These applications can assist in the detection and monitoring of retinal illnesses with OCT capabilities at the periphery, as demonstrated by technologies like ultrawide-field OCT.

Hence as per the factors mentioned above, OCT Scanner is expected to drive the segment growth over the forecast period.

North America Dominates the Optometry Equipment Market and Excepted to do Same in the Forecast Period

Some of the factors driving the market growth in the North American region include increasing incidence rates of eye diseases and the rising aged population, highly developed healthcare infrastructure, and the presence of key market players in the region.

In 2021, the Canadian Ophthalmological Society, during Glaucoma Awareness Month, stated that glaucoma affects more than 800,000 Canadians every year. In the awareness month, facts, like the rising aging population in Canada, lead to an increase in the burden of the disease, and it was stated that glaucoma has the potential to become an epidemic in Canada in the coming years, which is expected to boost the market growth. Additionally, as per a study published in the Investigative Ophthalmology & Visual Science in June 2020, in Mexico by 2030, the number of people with glaucoma is estimated to reach 1.06 million, increasing to 1.27 million in 2040 and to 1.43 million in 2050. Moreover, The market players adopted various strategies, such as product launches, developments, acquisitions, collaborations, mergers, and expansions, to increase market share. For instance, in September 2020, Topcon launched the Aladdin-M software in the United States market. The software measures corneal curvature, pupil dynamics, and axial length metrics and incorporates features for keratoconus screening.

Increased Government initiatives, research and developments, and implementation of digital healthcare systems boost the market growth over the forecast period. For instance, as per the news published in June 2022 in National Eye Institute (NEI), researchers from the National Eye Institute (NEI) have identified a new disease that affects the macula, a small part of the light-sensing retina needed for sharp, central vision. Scientists reported their findings on the novel macular dystrophy, which is yet to be named. Hence these types of research increase the adoption of optometry equipment thereby boosting the market growth.

Optometry Equipment Industry Overview

The Optometry Equipment Market is moderately competitive and consists of various small and large surgical/medical device manufacturing companies offering products for ophthalmic diagnostics and treatments. Some market players include Alcon, Carl Zeiss Meditec AG, Canon Inc., Heidelberg Engineering GmbH (Heidelberg Engineering Inc.), and NIDEK CO. LTD, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Eye Diseases

- 4.2.2 Technological Advancements in Ophthalmic Devices

- 4.2.3 Increasing Government Initiatives to Control Visual Impairment

- 4.3 Market Restraints

- 4.3.1 High Cost of Eye Examination Equipment

- 4.3.2 Lack of Awareness and Low Accessibility to Eye Care in Low-income Economies

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Type of Examination

- 5.1.1 Retina Examination

- 5.1.1.1 OCT Scanner

- 5.1.1.2 Fundus Camera

- 5.1.1.3 Visual Field Analyzer

- 5.1.1.4 Ophthalmoscope

- 5.1.1.5 Retinoscope

- 5.1.2 Cornea Examination

- 5.1.2.1 Wavefront Aberrometer

- 5.1.2.2 Specular Microscope

- 5.1.2.3 Other Cornea Examinations

- 5.1.3 General Examination

- 5.1.3.1 Autorefractor

- 5.1.3.2 Ophthalmic Ultrasound System

- 5.1.3.3 Tonometer

- 5.1.3.4 Phoropter

- 5.1.3.5 Keratometer

- 5.1.3.6 Lensometer

- 5.1.3.7 Other General Examinations

- 5.1.1 Retina Examination

- 5.2 By End User

- 5.2.1 Eye Clinic

- 5.2.2 Hospital

- 5.2.3 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Alcon

- 6.1.2 Canon Inc.

- 6.1.3 Carl Zeiss Meditec AG

- 6.1.4 Bausch Health Companies Inc (Bausch + Lomb)

- 6.1.5 Essilor Luxottica (Essilor International SA)

- 6.1.6 Johnson & Johnson

- 6.1.7 Heidelberg Engineering GmbH (Heidelberg Engineering Inc.)

- 6.1.8 HEINE Optotechnik

- 6.1.9 Nidek Co. Ltd

- 6.1.10 Halma plc (Keeler Ltd)

- 6.1.11 Revenio Group PLC (iCare Finland OY)

- 6.1.12 AMETEK PIP Holdings, Inc (Reichert Technologies)

- 6.1.13 Oculus Inc.